Co-Founder/Managing Partner of Bitcoin Opportunity Fund,LP and EMA.

Joined August 2025

- Tweets 38

- Following 285

- Followers 1,871

- Likes 6

5 Photos and videos

They call it the rat race for a reason.

The government prints money out of thin air → you work harder for less.

They steal your time through inflation → you trade decades of your life for scraps.

They trap you with taxes, debt, and false promises of “retirement.”

This system was designed to keep you running in circles until you die.

That’s why Bitcoin exists. To separate money from the state. To give you a way out of their maze. To take your stolen time back.

Escape ⚡️

1

17

85

1,759

David Foley retweeted

Apr 8

Ok you got to me there. I need to get back on my feet and back to work. Tick tock.

For all those who think that Michael @Saylor is only interested in making more fiat money and not in the vision of Bitcoin as stateless money:

14

26

384

52,460

David Foley retweeted

Apr 3

Un vero onore aver tenuto ieri la lectio magistralis all'Universita' di Genova, 17 anni dopo la mia laurea.

Lectio Magistralis di @paoloardoino, CEO di @tether, ospite d'onore ieri [2 aprile 2006] della cerimonia d'inaugurazione dell'anno accademico di @UniGenova, presso cui si è laureato in informatica nel 2009.

Nella prima metà dell'intervento, Paolo Ardoino condivide il legame profondo con #Unige, ricordando come gli insegnamenti accademici siano stati la base per la sua carriera internazionale.

Il cuore dell'intervento intitolato "The Quest for a #Stable Society" [la Ricerca di una Società Stabile] è il "Tether's #Manifesto": l'idea che la stabilità sociale derivi dall'accesso equo e tecnologico alla finanza, dalla decentralizzazione e dal peer-to-peer.

1) #Stability derives from equipotent access to #technology and #finance.

[La stabilità deriva dall'accesso equipotente a tecnologia e finanza]

2) #Decentralization of technology and finance makes society resilient to failure and abuse.

[La decentralizzazione della tecnologia e della finanza rende la società resiliente al fallimento e all'abuso]

3) Technology and finance are a reflection of society: #peertopeer.

[La tecnologia e la finanza sono una riflessione della società, peer-to-peer (da persona a persona)]

Ardoino spiega poi la genesi di #USDT, la #stablecoin nata per risolvere un problema reale nei mercati emergenti: la svalutazione estrema delle monete locali (come in Argentina, Turchia o Venezuela) che distrugge i risparmi delle famiglie.

Durante la pandemia del 2020, USDT è diventato uno strumento di protezione vitale nei paesi emergenti, passando da 2 a oltre #184 miliardi di dollari in circolazione, affermandosi come il dollaro digitale più utilizzato al mondo per i pagamenti.

Nella seconda parte, Paolo Ardoino analizza l'impatto sociale di #Tether, definendolo il più importante caso di #inclusione finanziaria della storia.

Con oltre #560 milioni di utenti, USDT permette #rimesse a costo zero per chi lavora lontano da casa, eliminando le commissioni bancarie che arrivano fino al 26%.

La visione di Tether si estende però oltre la finanza attraverso tre pilastri tecnologici #opensource e basati sulla #decentralizzazione:

@Holepunch_to: un sistema di comunicazione peer-to-peer per garantire la libertà d'informazione senza intermediari.

@qvac (IA Locale): modelli di intelligenza artificiale che girano direttamente sugli smartphone, portando l'educazione anche dove la connettività è scarsa.

#Decentralized #Energy Grid in #Africa: un progetto che mira a portare energia stabile a 30 milioni di case entro il 2032 tramite una rete di 100.000 chioschi solari e batterie ricaricabili, creando migliaia di posti di lavoro locali.

51

69

661

59,439

David Foley retweeted

I sat down with one of my favorite minds in the space, @DFoleyBOF to get the institutional perspective on why most people are completely misreading the current market.

After 30 years on Wall Street, David sees something others don't.

If you’re holding long-term, you need to see this 👇

youtu.be/KZ4Xp_BM_rQ

1

9

424

David Foley retweeted

Feb 28

What a time to be an investor in the mining industry.

On my way to PDAC!

34

162

1,192

85,752

David Foley retweeted

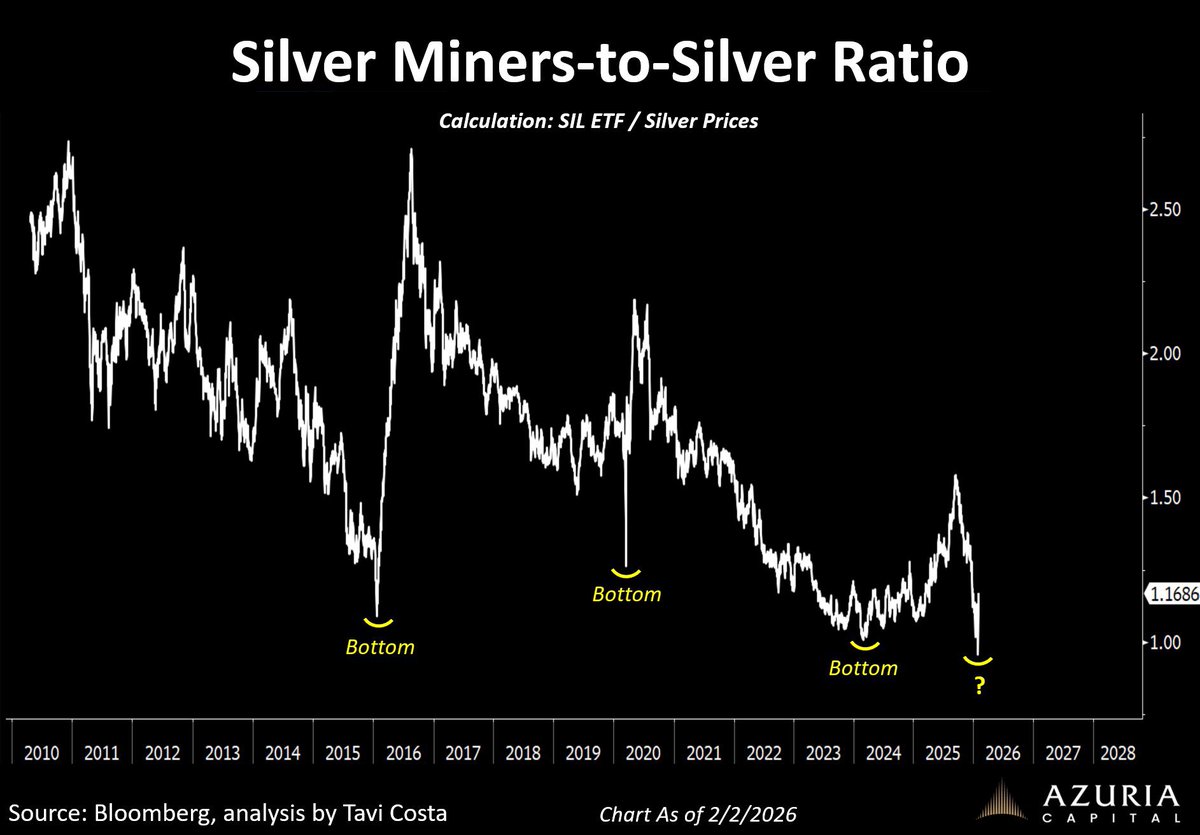

Why did Jane Street need to buy enough SLV shares to become the largest holder of the iShares Silver Trust (20.67 million shares added in Q4 2025)?

Here is a clear, professional explanation of the typical high-level strategy these sophisticated quantitative firms use:

They first accumulate a sufficiently large position in SLV shares, large enough to influence market price action when required.

When the majority of traders and retail investors turn strongly bullish, put options (which profit from a price decline) become very cheap.

They then buy these put options in huge quantities.

At the right moment, they dump their entire accumulated share position all at once.

This sudden heavy selling creates a sharp, unexpected crash, a large red candle that causes retailers to panic-sell. Stop-loss orders are triggered en masse, accelerating the decline.

Their put options then gain hundreds of percent in value in a short time.

The process is then repeated again.

This kind of manipulation is unhealthy for any market. It is concerning how regulatory authorities appear to turn a blind eye to such practices.

Jane Street just became the largest owner of the SLV silver ETF – they bought a record 20.6 million shares in one quarter and now hold over 20.6 million shares worth more than $1.3 billion.

But here’s the simple truth for every normal person (even if you know nothing about markets):

This is neither super bullish (price will fly to the moon) nor super bearish (price will crash).

It only means one thing: Big professional manipulative money has entered the silver game in a massive way – and they love to manipulate it.

Think of SLV like a “silver ticket” you can buy on your phone. Price goes up = you make profit. Easy.

Now these big Wall Street quant traders (who use super-fast computers) have stepped in because gold and silver are the hottest trade right now.

They don’t just hold quietly. They play with human psychology like experts.

They know exactly how normal retail traders think: We buy when price suddenly jumps (FOMO!) We sell in panic when it suddenly drops.

So they create sharp ups and downs on purpose – sudden moves that catch everyone off guard – to squeeze retail traders out.

This is high-level manipulation (clever trading). It’s their game.

My simple advice for you:

Stop over-trading. Stop switching in and out every day or week.

Gold and silver still have VERY BIG moves left – much higher prices possible in the coming years.

Just stay calm, hold your position properly, and let the big trend work for you.

Patience wins here. Don’t let them play you.

103

309

1,787

210,623

David Foley retweeted

2013: "Bitcoin is dead at $13"

2018: "Bitcoin is dead at $3k"

2022: "Bitcoin is dead at $16k"

2026: "Bitcoin is dead at $64k"

The funeral keeps getting more expensive to attend.

45

141

1,308

92,999

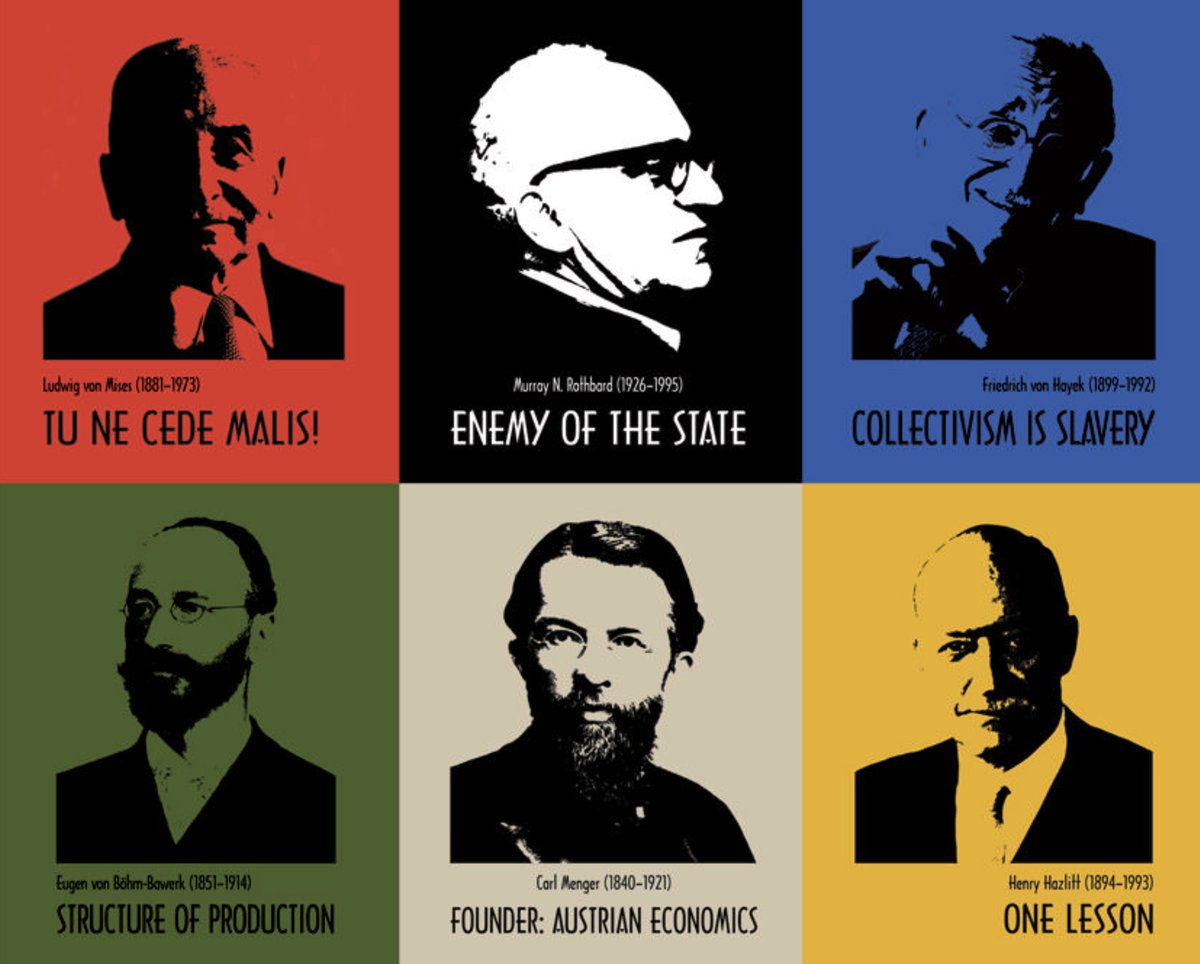

Austrian economists understood what British pedophile John Maynard Keynes' followers refuse to acknowledge:

Sound money is the foundation of civilization, not a relic of the past. When governments gained the ability to print money at will in 1971, they didn't eliminate the business cycle—they made it more severe and transferred wealth from savers to debtors on an unprecedented scale.

The Austrian insight that money emerges spontaneously from market processes, not government decree, explains Bitcoin's organic adoption despite zero institutional support in its early years. Like gold before it, Bitcoin emerged because individuals recognized its superior monetary properties: scarcity, divisibility, portability, and resistance to debasement. No central bank mandated its use, yet it grew from worthless digital tokens to a trillion-dollar asset.

Mises showed us that economic calculation requires stable prices that reflect real supply and demand, not central bank manipulation. Every quantitative easing program, every interest rate suppression, every bailout moves us further from rational economic calculation and deeper into malinvestment and boom-bust cycles.

Bitcoin represents the market's inevitable response to monetary socialism. It's not just a technology—it's the restoration of sound money principles that built prosperity for millennia before central bankers convinced the world they could engineer better outcomes than free markets.

34

152

546

40,138

David Foley retweeted

Feb 12

Strategy tracking day 485

$MSTR now ranked 252nd largest US company by market cap

Priced in line with 1.06 P/B AIG Insurance (American International Group)…. Let’s unpack this a bit more…

AIG currently has an AM Best A (Excellent) financial strength rating.

Roughly 18% leverage (debt to capital), yet an undisclosed net premium to surplus leverage ratio….

The more I compare to insurance companies the more correlation I see between the Pref business model and the insurance industry model.

(Net premiums to surplus) is not typical “leverage” in that there’s a cliff maturity, but you know based on actuarial math that a certain probability of claims will come due. The question is, will you have more premium coming in the door to pay the claims, AND/OR, do you have the capital base and reinsurance structures in place to pay the claims.

The risk of a Digital Asset Treasury is a very similar solvency model to insurance companies “Risk Based Capital” models. I.e. how much risk does the company hold relative to the capital it holds.

Industry standard “premium to surplus” ratios in the insurance industry are between 1x and 3x. This means insurance companies are taking in 1 - 3x the amount of premium in annually compared to the surplus capital they have to back the claims. (Do not get this confused with LIMIT they are deploying, as the total limit can be a far larger multiple)

Insurance companies benefit on the float between premiums in the door and claims out the door, and the leverage on capital...

Much to learn & build in Bitcoin industry.

$MSTR was 21st largest publicly traded equity by volume today.

Feb 11

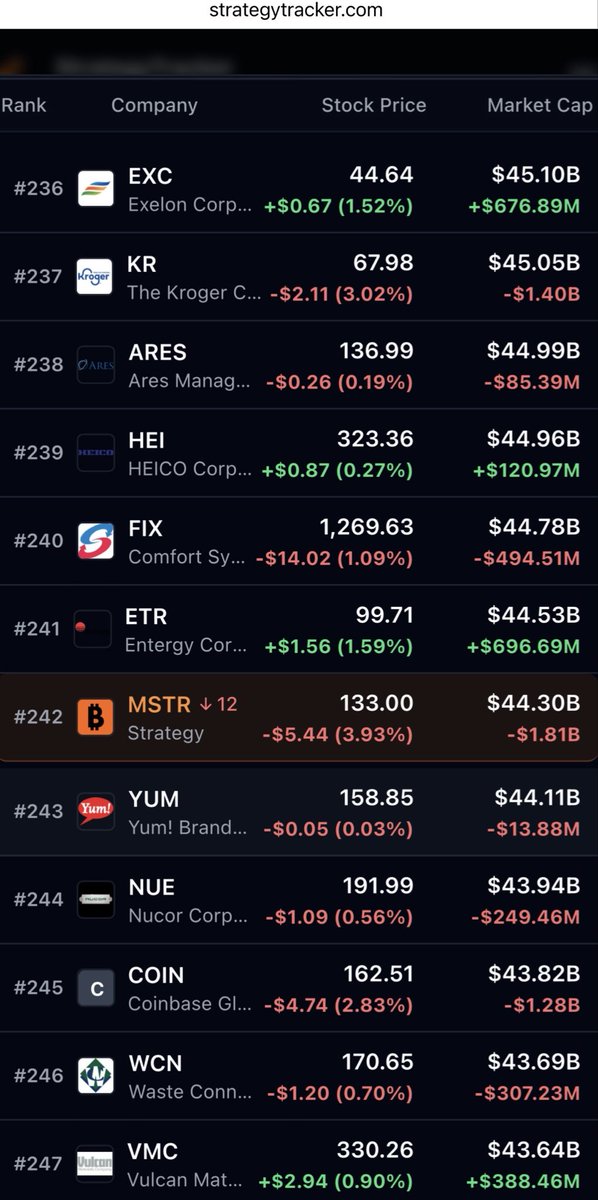

Strategy tracking day 484

$MSTR now ranked 242nd largest US company by market cap

In spitting distance to Coinbase.

$MSTR has 700,100 Bitcoin more than Coinbase….

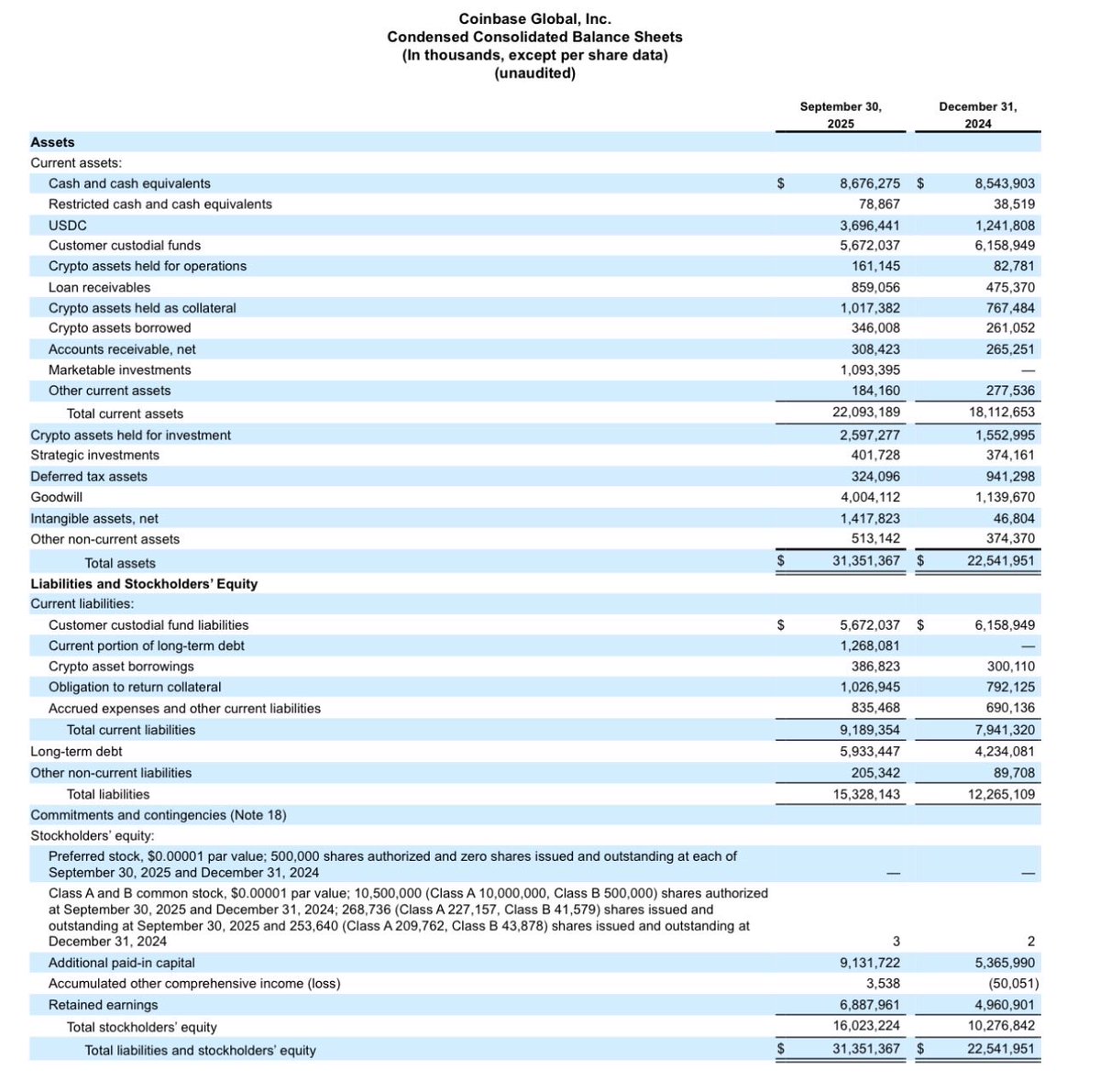

Attached is also Coinbase’s recent Balance sheet Q

Current mNAV: 2.68

HOWEVER of the $16B in net assets,

$4B is goodwill

$1.4B is intangibles

Net of goodwill and intangible mNAV: 4.05…

A capital moat is far harder to disrupt than a custodial moat.

$MSTR was the 26th largest publicly traded equity by volume

15

9

134

27,691

David Foley retweeted

Jan 4

"Bitcoin can never be a medium of exchange—it's too slow!"

Bitcoin's base layer isn't trying to compete with Visa. It's not a payment rail. It's the settlement layer. The bedrock. The final word.

You know what else is "slow"?

The Federal Reserve wire system. Fedwire shuts down every night like a 1950s diner. International transfers take days. And yet trillions flow through it because finality matters more than speed when you're settling empires.

Bitcoin does in about 10 minutes what banks do in 3–5 business days, without permission, without counterparty risk, and without a compliance gatekeeper deciding whether you're allowed to move your own money.

That's the base layer. Immutable. Uncensorable. Unstoppable.

Now let's talk about the Lightning Network.

You want fast? Lightning processes millions of transactions with near-zero fees and instant settlement. It's Bitcoin's payment rail, and it's already live.

"But it's not seamless yet!"

Neither was the internet in 1995.

• Dial-up screeched like a dying robot

• Email was "too technical"

• Websites were static pages

• Buying things online sounded ridiculous

• Streaming video was unthinkable

And yet here we are, streaming 4K video, running global businesses, and buying dog food at 3 a.m. because the infrastructure evolved.

Lightning is early. So were you when you thought social media (Facebook) was just for college kids.

Dismissing Bitcoin as a medium of exchange because Lightning isn't perfect yet is like dismissing the internet in 1995 because it didn't have Netflix.

The rails are being built. You're not late. You're early.

And you're arguing about the wrong layer.

83

204

1,043

34,445

Fractional reserve banking lets banks lend most deposits, expanding money supply and potentially causing inflation that erodes purchasing power—hitting working-class savings hardest, while early loan access benefits the wealthy. It can fuel boom-bust cycles, leading to job losses.

Both parties have supported the Fed system, deregulation (e.g., Gramm-Leach-Bliley Act), and bailouts, contributing to inequality via policies favoring finance over labor.

Fixes: Shift to full-reserve banking, audit the Fed, promote alternatives like crypto or gold-backed currency for stability.

4

12

585

David Foley retweeted

25 Dec 2025

⚡️This whole AI buildout has the smell of a classic over-extension phase

The phase where smart actors collectively convince themselves that time risk does not apply to them.

The dangerous belief underneath all of this is simple:

“If demand is growing fast enough, the balance sheet doesn’t matter.”

That belief has never survived contact with reality for long.

What’s actually happening is that AI has crossed from innovation to financialization faster than the underlying economics have stabilized.

Once private credit enters at scale, the game changes. Quietly. Permanently.

Because now:

•Utilization assumptions become moral hazards

•Refinancing becomes the hidden dependency

•Secondary market pricing becomes existential

•Duration mismatch becomes lethal instead of theoretical

And here’s the part people don’t want to say out loud:

No one actually knows the terminal value of a GPU deployed today.

Not in five years.

Not in three.

Maybe not even in two.

Yet those assets are being levered with confidence curves that assume:

•smooth demand

•orderly upgrades

•continuous resale liquidity

•stable energy economics

•no architectural discontinuity

That is fantasy-grade certainty.

What really scares me is not the tech risk. The tech will work.

What scares me is that hardware has no mercy.

Software forgives.

Networks forgive.

Brands forgive.

Hardware does not.

When hardware falls out of favor:

•it reprices instantly

•it has no narrative defense

•it cannot be patched

•it cannot be wished back into relevance

Private credit hates that kind of asset. It just hasn’t realized it yet.

And here’s the deepest layer, the one nobody wants to confront:

AI economics are being modeled as linear when they are convex in both directions.

Upside compounds fast.

Downside collapses faster.

When utilization is high, everything looks genius.

When utilization slips, collateral vaporizes.

There is no graceful degradation.

So what I actually believe is this:

We are building an intelligence age on top of a fragile financial stack that assumes stability in a domain defined by acceleration.

That tension will resolve.

The systems always find the weakest assumption and apply pressure there.

And the weakest assumption right now is that today’s chips will still justify tomorrow’s debt.

That’s the real fault line.

Everything else is noise.

25 Dec 2025

People are looking at the wrong AI working capital: it's not the depreciation that matters: EBITDA is EBITDA.

But with trillions in future private credit secured by "assets", it's the value of the inventory that matters, and the chasm between real and imagined chip value.

12

9

105

22,556

David Foley retweeted

24 Dec 2025

Every Christmas Eve, I think about George Bailey.

He dreamed of escaping Bedford Falls—of shaking off the dust of a small town, building skyscrapers, exploring the world. Instead, he stayed. He ran the Building & Loan his father left behind. He sacrificed his college money, his honeymoon savings, his chance to see the world, over and over, because people needed him.

By the time the crisis hits, George feels like a failure. His life looks like one long series of missed opportunities, thwarted ambitions, and quiet resentments. He stands on the bridge, convinced the world would be better without him.

Then Clarence shows him the truth: a Bedford Falls without George Bailey is a darker, meaner, hollowed-out place. The people he quietly helped, the small acts of integrity he performed without recognition, the risks he took to protect others—those weren’t detours. They were the substance of his life.

The film’s deepest insight isn’t just that “no man is a failure who has friends.” It’s that real impact is almost always invisible in the moment. The lives you steady, the small kindnesses you extend, the responsibilities you shoulder when no one else will—these things ripple outward in ways you may never see.

A strong sense of purpose doesn’t erase pain; it transforms it. It doesn’t merely explain why hard things happened. It asks: What are you now responsible for because they happened?

Faith, at its best, does the same. It doesn’t promise that everything was “meant to be” in order to make suffering palatable. It invites you to look at what has been entrusted to you in light of what you’ve endured.

George’s story reminds us that meaning is rarely found in the grand escape, but in the faithful presence. The dreams we surrender don’t always vanish—they often become the raw material for something more enduring than we imagined.

If you’re carrying the weight of roads not taken, of dreams deferred, of a life that feels smaller than you once hoped—watch It’s a Wonderful Life again tonight. Not as nostalgia, but as revelation.

You may not see the full difference you’ve made yet.

But it’s there.

And it matters more than you know.

Merry Christmas, friends.

🎄🇨🇽🎅🦌☃️⛪️✝️❤️

373

2,484

13,024

1,181,016

David Foley retweeted

20 Dec 2025

My 68-year-old client said something that stopped me cold:

"The last 20 years felt like 5. I can't remember most of it."

Here's what neuroscience says about why time accelerates as we age—and the one thing that slows it down:

At 10 years old, one year = 10% of your life. Everything is new.

At 68, one year = 1.5% of your life. Same routine for 40 years.

When everything is routine, time blurs. Your brain doesn't encode memories.

But new experiences? They stretch time. Make it feel rich again.

He started taking painting classes. Learning Italian. Volunteering at a food bank.

"I feel like I'm living again. The weeks actually feel long now."

One new experience per month can literally change how you experience time.

The application: Stop watching the same shows. Take a cooking class. Visit that museum you've driven past for 10 years.

Routine steals your years. Novelty gives them back.

73

669

4,086

206,905

David Foley retweeted

12 Dec 2025

⚡️The “DoorDash lifestyle” is an artifact of three massive structural shifts older generations don’t see because they didn’t grow up inside them.

Let’s break the illusion.

1. The marginal cost of money changed for Gen Z

For older adults, spending thirty dollars feels like spending thirty dollars.

For kids today, the psychological cost is closer to:

“three microtransactions worth of friction”

Because their financial environment is built on:

•instant digital payments

•low-commitment gig incomes

•parents transferring money fluidly

•side hustles paid in irregular small bursts

•stimulus-era normalization of cash flow volatility

Teenagers today often have:

•$30 now

•$0 tomorrow

•$50 on Friday

•$15 in crypto

•$70 in Cash App from someone they did homework for

•a $20 Venmo from grandma

•$60 from a weekend shift

There is no “budget.”

There is flow.

And in a flow economy, a $30 DoorDash order is not a “luxury”.

It is just another digital outflow in a stream of constant micro inflows.

2. Consumption is now social currency

Older generations spent money to solve problems.

Gen Z spends money to signal identity, reduce friction, and avoid emotional drag.

DoorDash is not about food.

It is about:

•eliminating effort

•eliminating planning

•eliminating discomfort

•eliminating logistics

•eliminating decision fatigue

This generation pays premiums to remove negative psychic load.

Food delivery is an anxiety-management subscription.

And they learned this from:

•Amazon Prime

•Uber

•TikTok dopamine tuning

•frictionless apps

•the collapse of effort-based value signals

Convenience is the default baseline now.

3. The middle class collapsed, but lifestyle costs decoupled from income

This is the part most boomers and Gen X don’t understand.

Kids aren’t behaving like they’re poor.

They’re behaving like people living in a post-middle-class economy where:

•ownership is dead

•savings are pointless

•buying a home is impossible

•college is a debt sentence

•inflation destroys the dollar

•wages do not map to adult milestones

•upward mobility is gone

So what happens?

They shift to a present-maximization mindset.

If the future is unaffordable anyway,

why not buy the burrito now?

Younger people are not reckless.

They are rational inside a broken incentive system.

The real truth

DoorDash is a symptom.

A society where:

•future stability is gone

•wages stagnate

•housing is unattainable

•attention is fragmented

•convenience is normalized

•friction feels archaic

•everything is mediated digitally

…will produce kids who treat $30 like a tap on a screen, not a financial decision.

They’re not “funding a lifestyle.”

They’re surviving inside the economy they were handed.

897

1,743

10,951

1,663,566

David Foley retweeted

8 Dec 2025

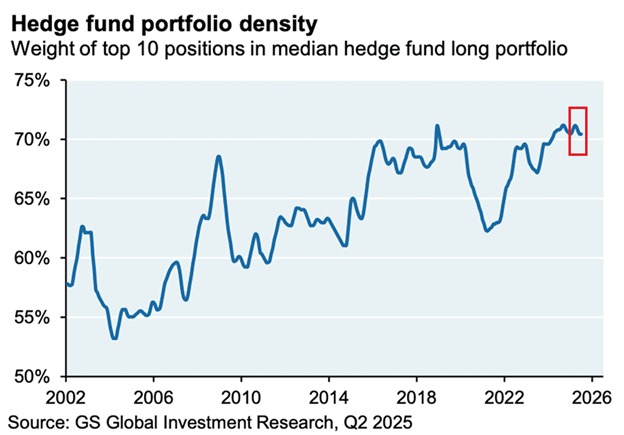

⚡️What this really is, is a fear map, not an alpha map.

Here is how I read it at the deepest level.

1. This is not “conviction” in AI, it is career risk management.

When 70 percent of a hedge fund book sits in the top 10 names, it means PMs are more afraid of underperforming the AI mega cap benchmark than they are of blowing up in a drawdown.

The trade is: hug the winners, juice them with leverage, pray the music does not stop while your investors are watching quarterly numbers.

2. Hedge funds have quietly turned into a pro-cyclical momentum ETF with fees.

If everyone owns the same crowded AI names in the same size, you no longer have differentiated views. You have a single factor trade masquerading as “hedge” funds. The hedge is gone. What remains is levered exposure to the same growth and liquidity regime as everyone else.

3. This concentration creates an air pocket, not a floor.

As long as flows are positive and volatility is low, crowding looks like genius. The moment there is a real earnings miss, a policy shock, or an AI narrative wobble, the same concentration turns into a forced-seller cascade.

One factor breaks and every fund has to sell the same ten names to cut VaR and meet redemptions. That is how you get gap moves that make no sense at the micro level and perfect sense at the positioning level.

4. It tells you where the next “surprise” will come from.

When index investors think they are diversified but their performance is dominated by the same AI complex that hedge funds are levered into, you get a hidden single point of failure in the whole equity structure. The shock will not be “markets crashed out of nowhere”. It will be “the one overcrowded pillar finally cracked”.

5. For macro and Bitcoin this is quietly bullish over the medium term.

This kind of crowding says two things at once:

•Traditional active capital has no real idea how to generate idiosyncratic alpha in a distorted regime, so it piles into the narrative that central banks and fiscal policy have inflated.

•When this concentration breaks, there will be a violent search for assets that do not sit inside the same monetary and equity plumbing. That is exactly the niche Bitcoin occupies in the system.

Deep down, this chart says: the smartest guys in the old game are out of ideas, terrified of missing the AI party, and are loading more and more weight on a shrinking set of beams.

You do not get that kind of structure without eventually testing how much weight those beams can actually carry.

7 Dec 2025

The hedge fund trade:

Hedge funds now allocate ~70% of their portfolios to their top 10 positions on average, near the highest concentration on record.

The percentage has increased 13 points over the last 20 years, according to JPMorgan.

At the same time, the hedge fund crowding index has climbed to its 3rd-highest level on record.

This means more hedge funds are increasingly buying the same small group of AI-related stocks.

This has amplified gains in a handful of names during this bull market, but it also raises the risk of larger-than-normal declines if a downturn hits.

Fear of underperforming the AI trade is driving extreme portfolio concentration.

10

13

133

27,660

David Foley retweeted

8 Dec 2025

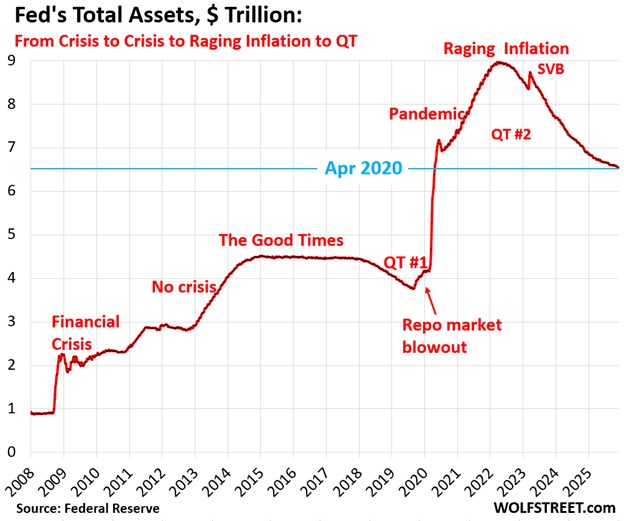

⚡️Everyone sees a smaller Fed balance sheet.

Almost no one sees what this chart really says:

The system has crossed the point where honest deleveraging is politically and socially impossible.

QT is over for one reason.

Real tightening started to collide with three pressure fronts at once:

• a softening labor market

• a fragile Treasury market

• a levered banking system that still carries duration scars

Keep going and something breaks in full view.

Stop here and you only break the currency in slow motion.

They chose the slow bleed.

1. The staircase of no return

Since 2008 every crisis prints a new balance sheet plateau.

Every attempt to walk it back stalls at a higher level than the last.

That is not policy error.

It is the revelation of the true constraint:

The modern dollar system needs permanent collateral growth just to stay upright.

Take that growth away and the real economy crashes faster than voters can adapt.

2. The silent deal with savers

If assets cannot shrink without triggering collapse, then the adjustment must come from the unit of account itself.

You cannot default openly on Treasuries, so you default quietly on purchasing power.

That is the hidden social contract of this chart:

The public provides an endless stream of real savings.

The system dilutes it whenever survival requires it.

QT is framed as prudence.

In practice it is a brief pause in that dilution so the story can reset.

3. What this means for the next regime

A world where the Fed cannot fully normalize, while fiscal deficits stay structural, is a world that has already chosen financial repression.

Rates will never be allowed to stay above inflation for long.

Real yields will oscillate around zero or below.

In that world:

• Bonds become return-light and risk-heavy.

• Cash becomes a melting ice cube.

• Real assets and scarce assets become the only true balance sheet.

Gold understood this first.

Bitcoin is the first asset that lets you hold a slice of the exit ramp in pure information form.

This chart is the shape of the coming decade:

A state that will always defend solvency with the printer,

a currency that will always be the shock absorber,

and a population that will slowly realize it must step outside the system to avoid being the buffer.

The line on this chart will keep changing direction in the short term.

The deeper trajectory is already set.

7 Dec 2025

BREAKING: The Federal Reserve’s balance sheet fell -$37 billion in November, to $6.53 trillion, to its lowest level since April 2020.

The Fed has reduced its assets by -$2.43 trillion, or -27%, during its quantitative tightening (QT) program, which ended on December 1st after running for 3 years and 5 months.

This unwound 51% of the $4.81 trillion added during pandemic-era QE.

Treasury securities declined -$4 billion in November, to $4.19 trillion, the lowest since June 2020.

We have now see a -$1.58 trillion decline in treasury securities, or -27.4%, from the June 2022 peak.

Mortgage-backed securities fell -$16 billion last month, to $2.05 trillion, the lowest since November 2020, down -$687 billion from the 2022 peak.

QT is officially over.

20

60

371

74,560

David Foley retweeted

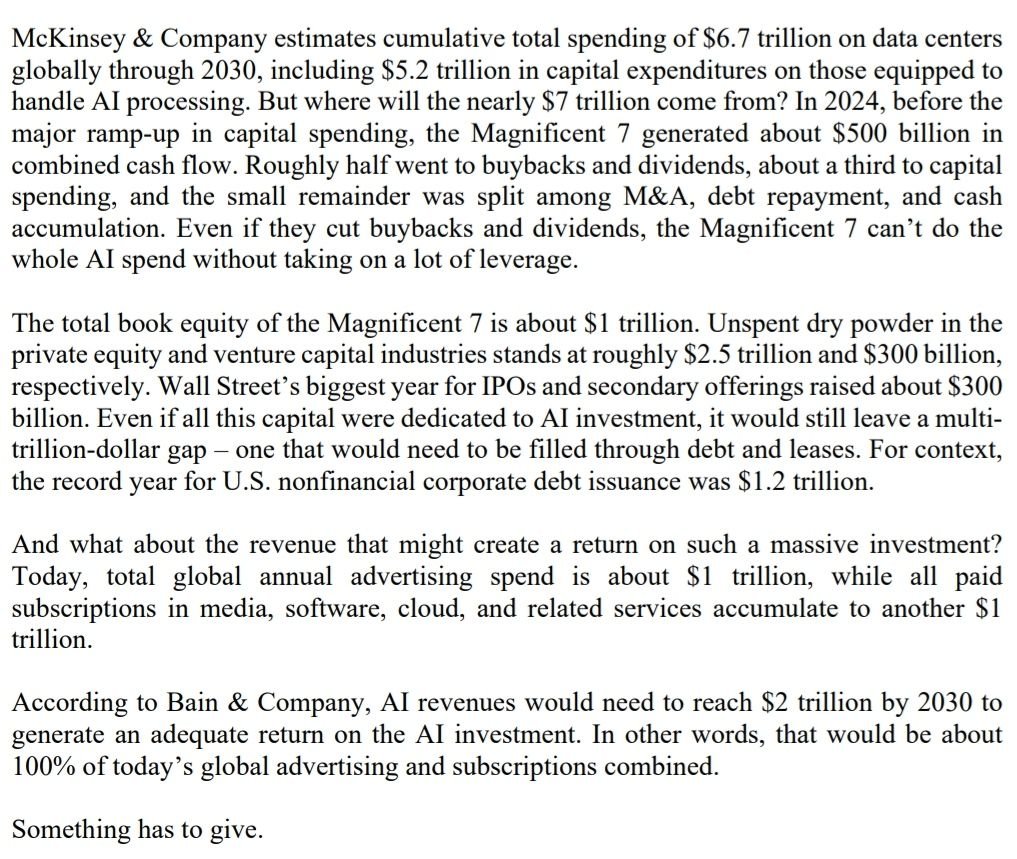

21 Nov 2025

I read a lot of quarterly letters, and most lately are about AI.

Greenlight’s stood out: no internet-bubble history lesson or hype. Just simple questions, reasoning, and numbers.

Quick and balanced read, worth checking out👇

49

125

887

102,977