Micro/smallcap investor and board member at $BOF. Long term ideas on my blog below. Personal thoughts, not financial advice.

Joined October 2023

- Tweets 530

- Following 1,013

- Followers 2,922

- Likes 3,953

21 Photos and videos

Pinned Tweet

31 Jan 2025

$CURI latest piece at link in bio.

Curiosity Stream is one of the largest documentary streaming platforms and is expected to double earnings through AI licensing deals and improvements in the core business. Despite this, the equity trades at a low 2.5x forward cash flows. 1/n

5

5

46

14,495

D&A Metropolitan retweeted

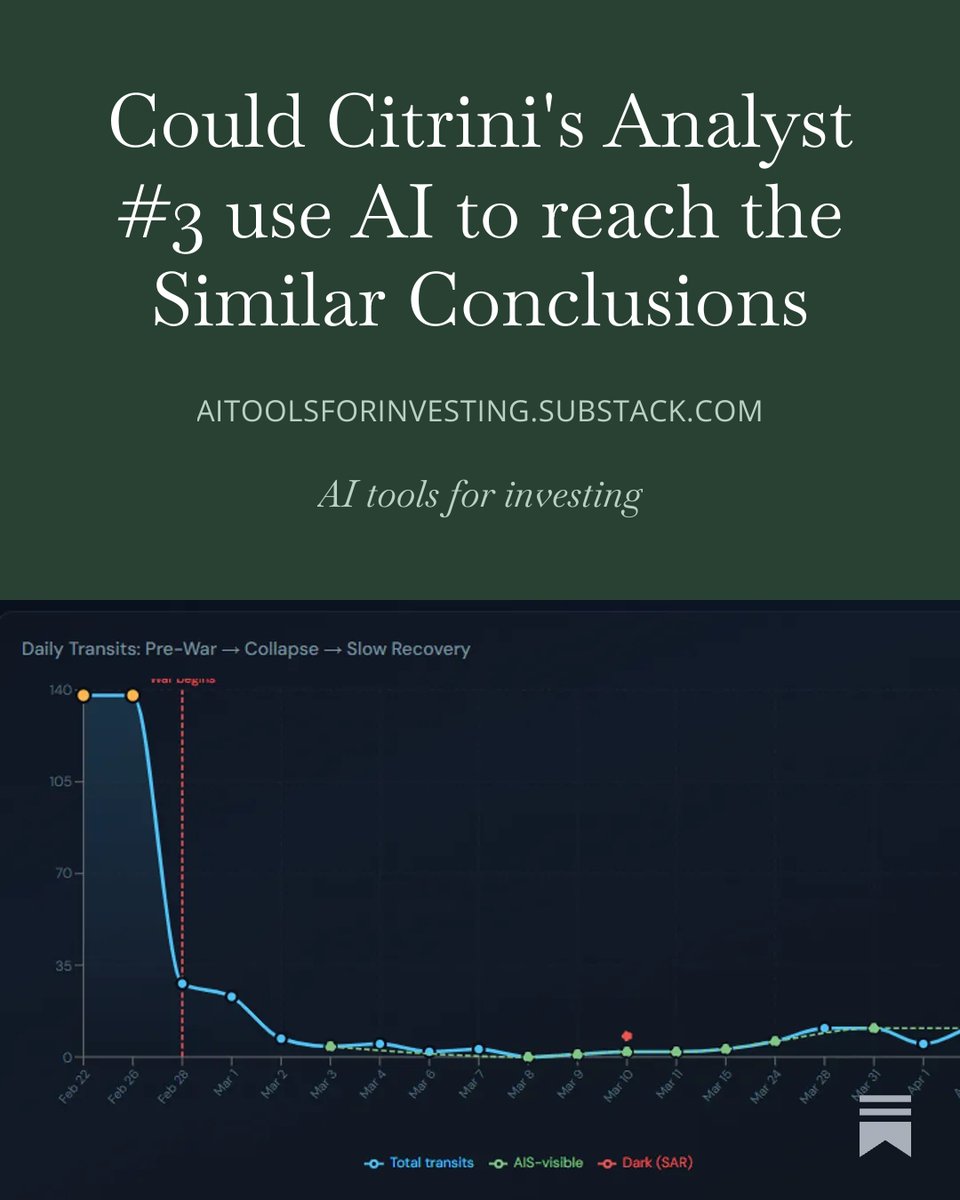

I'm launching a new newsletter about using AI tools to investing.

My first article on whether Citrini's Analyst #3 could use AI to reach similar conclusions is out now.

Please subscribe and let me know what you think.

Link in the comments

Thanks for @Uzocapital for convincing me to start this

3

4

29

13,144

D&A Metropolitan retweeted

Feb 11

$DBO.TO if this update is underwhelming to you, I recommend reading it more closely and thinking through what the drivers of this thesis are.

1. To state the obvious (which the company repeats in every press release) the royalty business is driven by content and therefore quarterly comparisons (both sequential and YoY) are not instructive. What matters for the royalty stream is: 1) forward box office $'s (estimates for 2026 are well above last years); 2) how the change in royalties compares to the box office (outperformed again); and 3) systems growth (which drives royalty growth independent of "same store" growth.

2. That last piece is the only thing in their control topline wise, and they just had the best quarter ever in that department (all time high of 86)...active screen count up 5% sequentially.

3. Crucially. Cash increased by $6m in the quarter, but half of that is attributable to an in flow related to deferred revenue (balance jumped from 700K to 4.1m in three months). That suggests a meanginful wave of continued systems growth imminent, and apparently an increased customer financing component (which I need to confirm with mgmt, but that's my interpretation, and would be meaningful for cash flow dynamics and roics.)

4. Cost control. 61% operating profit despite 4% topline growth YoY. Opex increase $100K QoQ, but that was all driven by R&D and S&M (i.e. investment), while Admin costs dropped.

5. DTA recorded. I don't need to explain what that implies.

6. Note the language in the press release regarding the cash balance: "Our cash balance of $16.2 million provides the Company with the financial flexibility to continue its mission of expanding its operations and customer base in a strategic and methodical manner.”

There was no such language in prior press releases. Are they looking at financing structures for partners that want the format but lack the balance sheet to pay up front? Not clear, but see @JonCukierwar write up.

Feb 11

A 20% earnings yield?...

$10m trailing EBITDA on roughly equivalent tangible invested capital, >25% margins, no debt with excess cash, and just grew the screen count 5% in a single quarter(!)...a record period for installations. (that latter piece is the most important part of the update by far if you understand what the value drivers are here). A refinery multiple on this would be uniquely preposterous.

It might sell off because it's a microcap that fintwit piled into with borrowed conviction, but its already more than a 60% discount to IMAX's multiple on NTM numbers at today's share price with more growth and runway.

6

6

55

20,674

D&A Metropolitan retweeted

18 Dec 2025

Talked through $dbo.to thesis with @BobbyKKraft earlier this week.

18 Dec 2025

[NEW PODCAST] D-BOX Technologies $DBO.TO and Premium Formats in the Theatrical Ecosystem with Dylan Marrello, Founder & Portfolio Manager at Marrello Capital @ragingbullcap

We discuss:

- How premium formats are reshaping movie economics

- D-BOX’s royalty-driven model and operating leverage

- Screen expansion, pricing power, and key growth levers

- Risks, valuation, and where D-BOX fits vs peers

Watch here: youtube.com/watch?v=rHJp3n3J…

Listen here: microcapnewsletter.substack.…

6

2

45

10,039

5 Dec 2025

Excellent writeup on $dbo.to. FY27 estimates have significant upside too given that royalty revenue per screen has grown significantly in recent years. If consumer adoption continues we could see an additional 10-20% tailwind to royalties. Long

18

2,928

28 Nov 2025

$ZOMD.v Looks cheap but between management's reluctance to spend cash/provide guidance, feels like a value trap

3

18

3,013

24 Nov 2025

$TRBR.V

Happy ending for Trubar shareholders with the company being sold for ~3x 2025 sales, although a little surprised they elected to sell the company this early

1

1

13

2,460

D&A Metropolitan retweeted

24 Nov 2025

$TRBR being acquired for $1.64 in canadian monies

this is my crown achievement as a fake PM, with my Analyst Emeritus @DMetropolitan having sent me a pitch for feedback about 18 months ago

my feedback: goodco/badco is usually a terrible thesis, but this sounds great!

1

11

1,736

17 Nov 2025

Strong day from $AENT even with the market puking. Earnings were very strong with double digit topline growth. Margins were softer than I anticipated due to strength in gaming, but demand across all segments was exceptionally strong. Momentum should carry into Q2

Disc: Long

12 Nov 2025

$AENT reporting after close. Not expecting anything exciting on the top line given tough comps and challenges in gaming segment, but looking for gross margins to hold 15.8% and commentary on new licensing deals.

1

12

2,306

12 Nov 2025

$AENT reporting after close. Not expecting anything exciting on the top line given tough comps and challenges in gaming segment, but looking for gross margins to hold 15.8% and commentary on new licensing deals.

1

6

3,231

12 Nov 2025

I'm long $DBO.to but wouldn't be surprised to see some profit taking after the recent rally. Quarter should be flattish/down slightly QoQ but with royalty revenue increasing at its current pace, we should start seeing smoother earnings and a very strong back half. Still cheap IMO with a long runway

12 Nov 2025

I'll be very happy to be proven wrong, but $DBO.TO $DBOXF will probably come in lower YoY and QoQ, mostly due to fewer new theatrical installs in August and September (though these appear to have picked back up in November).

Expecting the sim business to continue showing strength, with a good boost this quarter from the Vegas Arcade opening. Royalties should be flattish QoQ, a testament to how well the product is performing even with a light release schedule.

I have trimmed 25% of my position since the stock is up 120% in 5 months when the idea was shared. There is a possibility of an overreaction to the downside as the comps could look weak optically.

8

1,884

30 Oct 2025

$AMPG It was clear that they wanted to raise capital which was clearly a drag on the stock. After this, the overhang should be gone although it may have been better to slam the ATM.

No position currently

8

1,579

D&A Metropolitan retweeted

26 Oct 2025

Idea thread #2!

What's your favorite special situation? (Spin/m&a/etc any market cap).

Add a sentence explaining why you like it valuation.

I will compile the responses and share them with everyone.

Please retweet for visibility. Thx in advance! 🙏

27

18

89

79,585

D&A Metropolitan retweeted

26 Oct 2025

An interesting trade idea out now.

Checkout at the usual link

$GOOG

1

1

6

3,412

24 Oct 2025

Posted a writeup on $AENT. It's currently trading at ~5x EBITDA and ~6x EPS despite an impending return to growth in 26/27 and numerous catalysts for a rerating. Full writeup in the usual place.

1

22

7,907

D&A Metropolitan retweeted

24 Oct 2025

Initiating coverage of CEMATRIX Corporation (CEMX.TO): Buy rating, $0.82 target price.

CEMX is a company that doesn’t screen well on LTM fundamentals, and most investors dismiss it as excessively lumpy. Zooming out, however, the flywheel effect of product validation from prior project successes becomes apparent, despite a capital-intensive business model transition that resulted in a multi-year, relatively range-bound performance.

Now, the setup is different. The company has a new CEO, its balance sheet has improved, and shares were reduced for the first time in its history. The seasonally low 2024 is setting the stage for record highs in FY25 and FY26. With profitable operations and a net cash position, there is not only no need for further dilution, but an accretive acquisition is also on the horizon.

The CEO phrased it perfectly: “In fact, the other day I went looking for a company with a market cap under C$50M, revenue over C$50M, with positive cash flow, and positive adj. EBITDA. I could only find one in Canada.” While the company may have now surpassed this C$50M threshold, the analogy still holds true.

2

9

33

13,967

23 Oct 2025

It's been a while but publishing a new writeup on a cheap consumer name tomorrow. Check it out at the usual place

1

2

19

2,745

D&A Metropolitan retweeted

6 Oct 2025

Global $450M small cap L/S, generalist firm hiring an analyst, will report to PM & Senior Analyst. Ideal candidate has <4yrs work experience, VIC member or substack author, demonstrated passion for public markets, curious, eager to learn. Please send to hfreflection@gmail.com

17

24

344

138,886

19 Sep 2025

Kyle does great work, definitely worth checking out

19 Sep 2025

I am starting a Substack.

First post will be after my conversation with $PPIH leadership, so likely next weekend.

It will be entirely free to start, then I may look at charging a small amount, but probably not for a while.

Long overdue.

1

1

8

3,192

D&A Metropolitan retweeted

17 Sep 2025

$DBO.TO sometimes tiny market caps present you with opportunities so obvious that you feel you must be missing something. Occasionally it just really is that simple. One of the easiest lay ups in recent memory.

13 Aug 2025

$DBO.TO As expected, major inflection in royalties. This is a double from here just putting a reasonable multiple on current run rate. I think it gets sold for at least 60c in the next year. 🫡

d-box.com/en/news/dbox-techn…

6

2

45

25,909