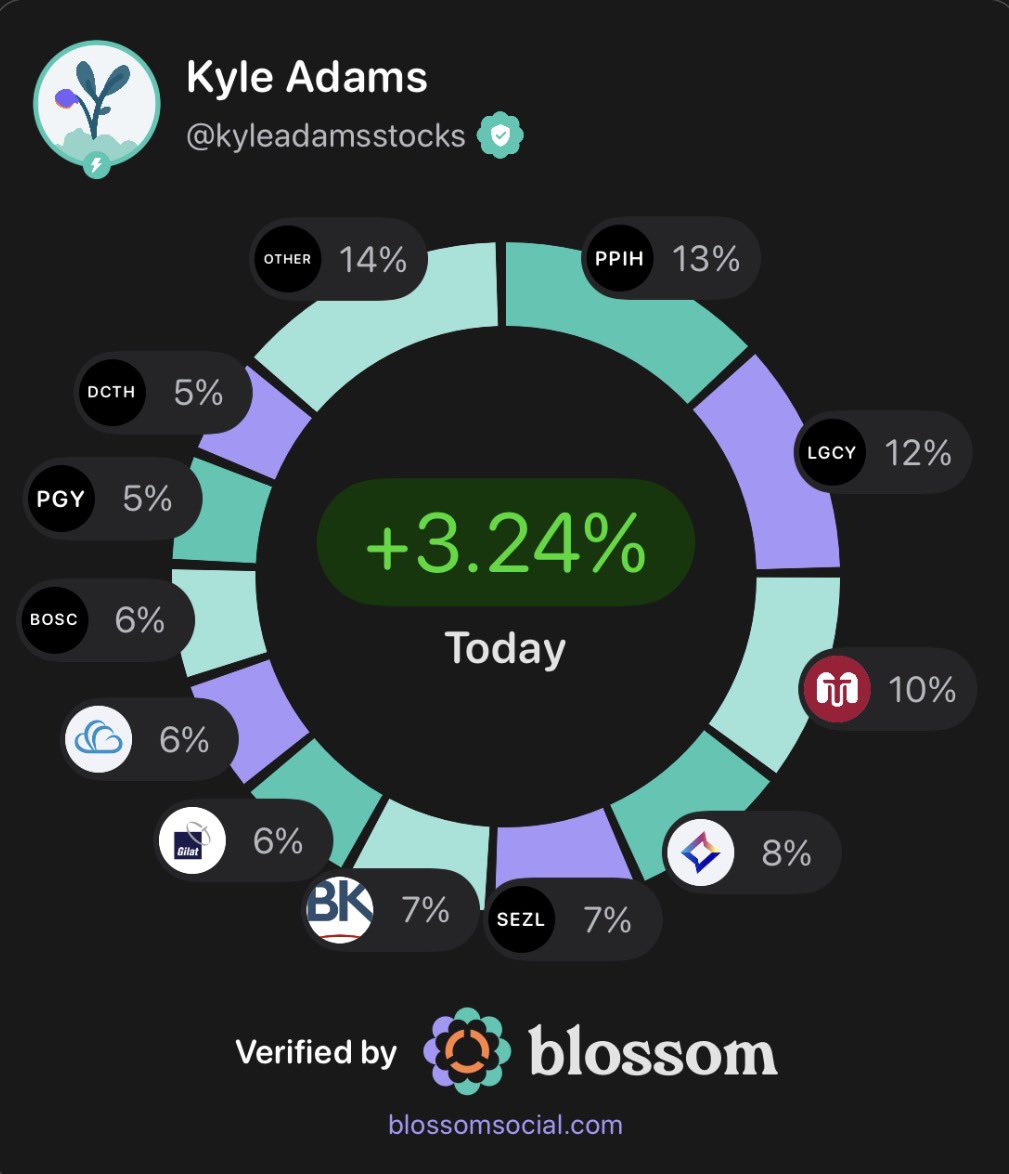

30 | Investing to $1,000,000 in my taxable brokerage | Crazy enough to jump out of planes for fun | not financial advice

Joined January 2019

- Tweets 17,672

- Following 1,282

- Followers 15,593

- Likes 53,974

2,000 Photos and videos

Kyle Adams retweeted

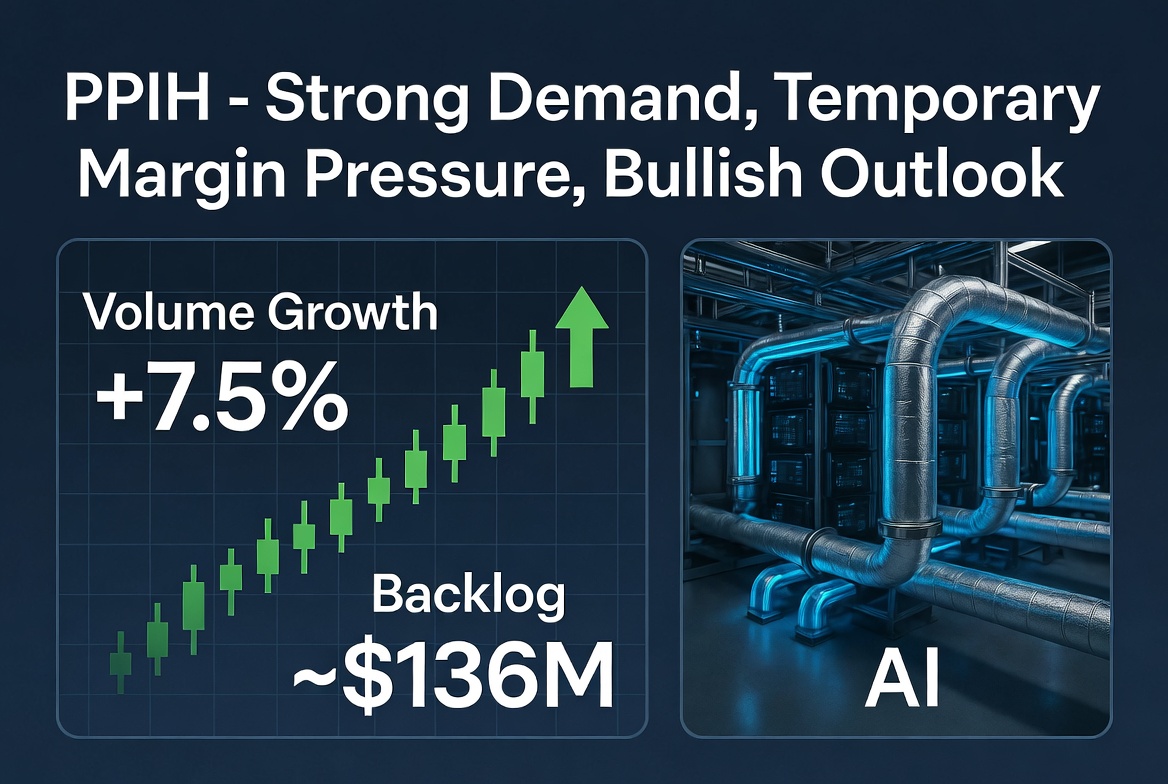

$PPIH Q1 2026 Reflection: Demand Remains Robust, Margins Temporarily Hit, Outlook Bullish

DEMAND 📈

- Revenue increased and most importantly, it was due to volume in both NA and MENA regions. It means that demand is still very strong.

- It is also confirmed by the backlog compared to Q4'25 where new orders that came in Q1 are 65m, pushing a total backlog to 146m.

- One part of revenue was not realized due to the Middle East conflict, but at least no projects have been cancelled.

- On LinkedIn, you can see a number of open positions, and most of them have been created recently, especially for the NA data center segment. So the demand is "real"; no one opens the positions if they don't see a good return on those.

MARGINS ⚠️

- Gross profit has been hit pretty strongly. There is no breakdown by the cause, it seems its a mixture of things: ramping production in Ohio and Qatar, sales mix in Canada, higher margin projects in MENA delayed.

- My read on it is that the majority of them are temporary.; besides Canada, which might or might not be. MENA situation will get resolved eventually, leading to both repair new work for PPIH; Once operations in Ohio are set, NA will benefit greatly from operating leverage

OUTLOOK 🔮

Mngt expects both higher revenue and profit vs 2025. This is super interesting. So even with the current Iran situation affecting the whole region, extra costs associated with starting the production,...they still expect to increase profit. It means that the rest of the year we should see very strong results and looking further ahead with operations stabilising, 2027 might be the first year to show the real strength of the company, benefiting from "back to normal" demand in the Middle East AI demand from North America

VALUATION 💵

Currently, I think the market is taking the short-term view of the company, overemphasizing the operating issues that took place in Q1.

We have a company with 220m of market cap that did 20.7m of profit in 2025 and this year, despite all the issues mentioned above, is guiding to a higher profit.

Just to get to the same level as in 2025, not even grow(as mngt said), the average quarterly profit for the next 3 quarters needs to be 6m. If we are to annualize that, we are getting to 24m, not catering for the operating leverage that will take place and the potential data center demand that's difficult to quantify.

#DataCenter #AI

2

6

7

1,315

Jun 9

Agree with this take on $PPIH.

Wouldn’t be a seller of the stock here since backlog is going up, and they say net income will improve the following quarters.

If backlog decreased as well, then that would be bearish, but project work is still there, and with the Iran crisis coming to an end soon, then work should resume.

Slightly disappointing ER from $PPIH this morning. EPS came in quite low due to Middle East project uncertainty.

More importantly though, backlog has increased, primarily driven by new AI-related projects in their new Ohio facility.

AI-related rerate thesis is still in play.

5

6

27

4,165

Kyle Adams retweeted

Jun 6

Here’s some Substack authors we’ve interviewed via Skull Sessions or personally met / conversed with that we highly recommend you check out. They focus on quality, in depth analysis and are good peeps.

@AurelionRsch

@Pixelresearch_

@GfI_Himmelreich

@AKWilk

@Mike10947310

@TheBigBerbowski

@StockJabber

@dgkunze1

@realLigerCub

@leevalueroach

@DeepSailCapital

@QTRResearch

@SebKrog

@bmb21

@Investing501

@yuvaltaylor

@100baggers

@pernasresearch

@onecentinvest

@CyclopSpaceTech

@UnderlyingValue

@HugoNavarroPer2

@Stocks_Stones

@KyleAdamsStocks

@SCMRE111

@realThomasNiel

@smcap_thinking

4

17

38

17,136

Apr 30

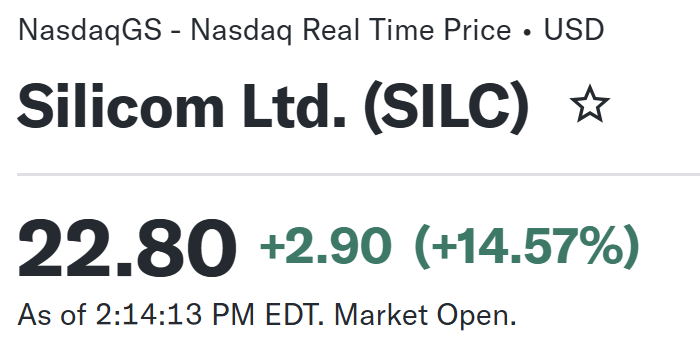

Now way over 100% up on $SILC.

Very bullish earnings / call. The company is in an inflection point for the next few years and trending towards beating their upper guidance on design wins.

Apr 25

About 100% up on my $SILC position.

Lot of design wins, and we are entering a period of growth, so expect momentum to continue.

Not as much of a no brainer around $30, but still holding my shares.

6

1

22

7,217

Apr 25

About 100% up on my $SILC position.

Lot of design wins, and we are entering a period of growth, so expect momentum to continue.

Not as much of a no brainer around $30, but still holding my shares.

Jan 6

$SILC

Not a name I talk about a lot, but quietly winning a lot of design wins to set them up for growth again.

This company / stock has been a loser for many years, but I believe it is waking up, and about to enter a cycle of growth.

Yesterday, they announced a customer is expanding their deployment with them signifgantly by more than double for their edge devices.

“A global networking and security-as-a-service customer expanded its January 2026 deployment of Silicom Edge devices into multiple additional use cases, raising the expected annual revenues from that customer from $3–4M to $8–10M.”

1

2

22

14,639

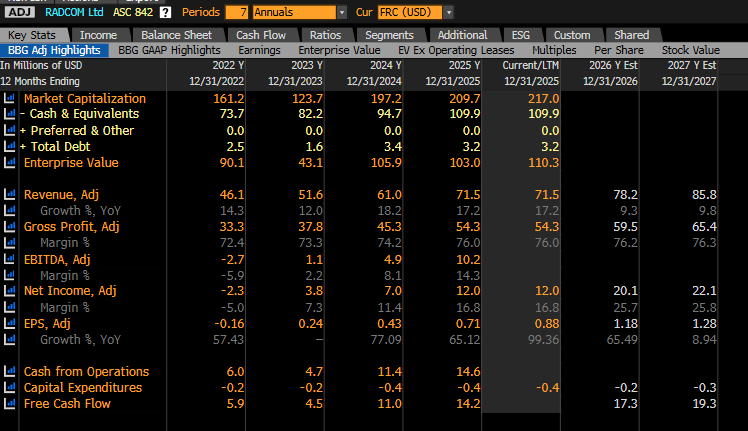

Feels we might be in for some interesting times at Radcom $RDCM.

Activists popping up left and right. Lynrock Lake is at ~20% and has been pushing for a strategic review (clearly a sale).

Value Base (5.4%) looking to clean up the board.

Good growth (leaning into AI/5G tailwinds), 75% gross margins, plenty of operating leverage, ramping cash flow, ~60% of market cap in net cash, ~10x forward PE.

Relatively high customer concentration though, and pretty lumpy business.

3

6

46

23,451

Kyle Adams retweeted

Apr 22

$PPIH Boring by Design, Interesting by Numbers

It's my most ambitious write up. I hope you like it.

Likes, retweets, feedback are appreciated.

Thank you for your endless support. 🫶

12

10

72

23,521

Apr 17

Been away for a little bit busy with work, but going to start posting again soon :)

What’s everyone’s favorite micro/small cap today?

18

29

6,308

Kyle Adams retweeted

$TMDX did 48 flights and grossed an $3,264,000 (est) in the last 24 hours.

They are on track to do 3,240 flights and gross $220,320,000 (est) this quarter.

Link - singularityresearchfund.com/…

Disclaimer: This information is for educational purposes only and does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and you should not treat any of the content as such.

3

7

62

16,877

Mar 31

We continue our policy of issuing a conservative initial outlook, with updates provided as the year progresses. While we maintain strong exposure to the defense markets, ongoing geopolitical tensions lead us to initially project 2026 at a level consistent with 2025 revenues of $51 million and net income of $3.6 million.

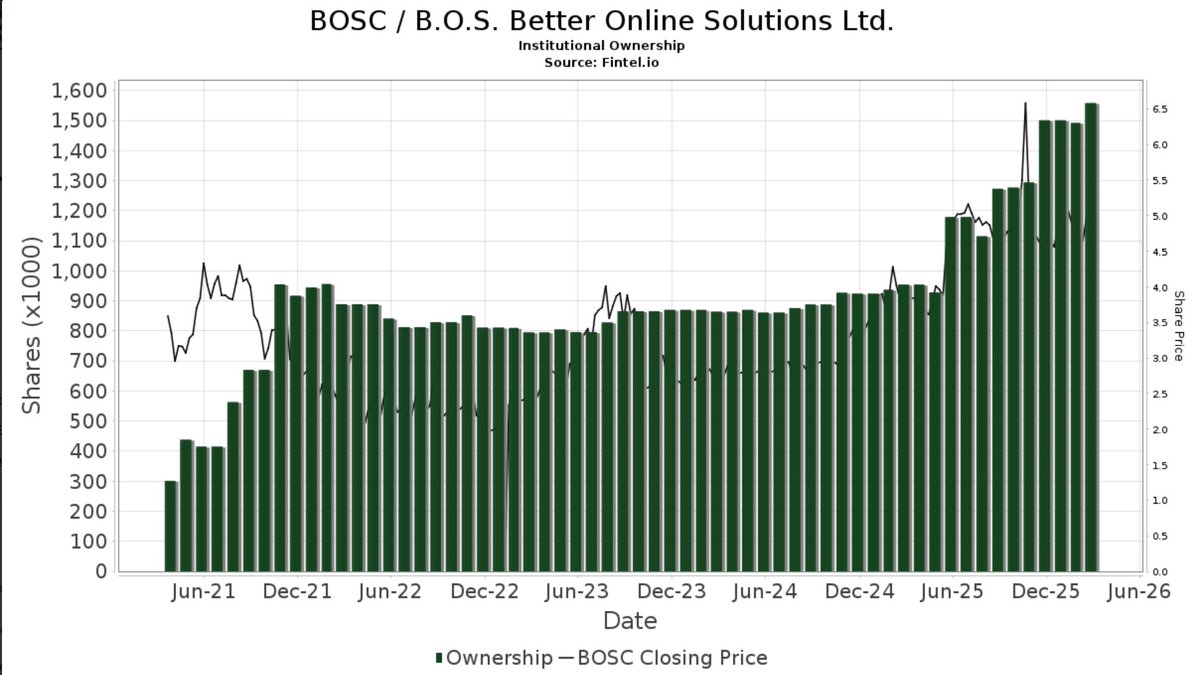

Another conservative guidance by $BOSC, which I expect to be raised throughout the year similar to this year. Also, they now have $11.8M in cash, which is well over 30% of the market cap alone.

Mar 31

BOS Reports Financial Results for the Fourth Quarter and Full Year 2025 $BOSC crweworld.com/article/news-p…

3

1

18

5,047

Kyle Adams retweeted

$SILC is the only short term solution to AI networking bottlenecks.

Until CPOs are ready and scale, the only way to improve global compute and reduce GPU idle times is to reduce data traffic.

That is what SmartNICs do, optimized hardware for latency including programmable semiconductors (FPGAs) directly connected to memory, GPUs or CPUs.

They take load of the network and those hardware for two reasons.

1. They are programmable and can be optimized for any kind of task, optimizing raw compute with exactly what we need, where we need it.

2. They are directly connected to hardware, removing transiting data in the network.

They can help for compute, data transmission, optimize workflows... anything the infra needs to operate at maximum compute.

As there’s no way to upgrade in-hardware bandwidth and latency today, the only method to improve compute further and reduce the actual networking bottleneck is to reduce the data transiting in the network.

That cannot be done by adding more GPUs or CPUs as it would lead to more data transiting and more idle time for those - counterproductive.

But it can be done with SmartNICs and FPGAs.

5

4

34

28,184

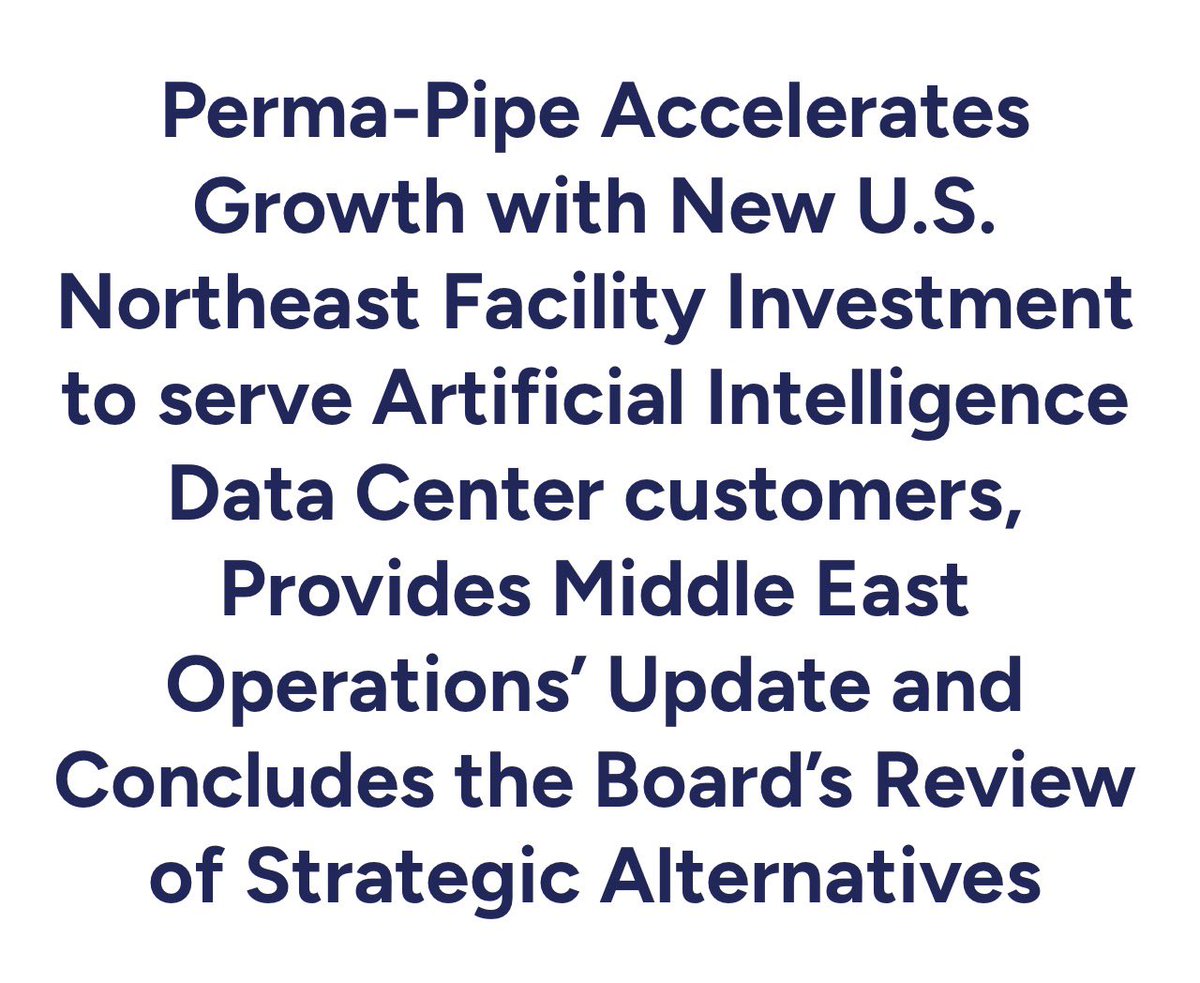

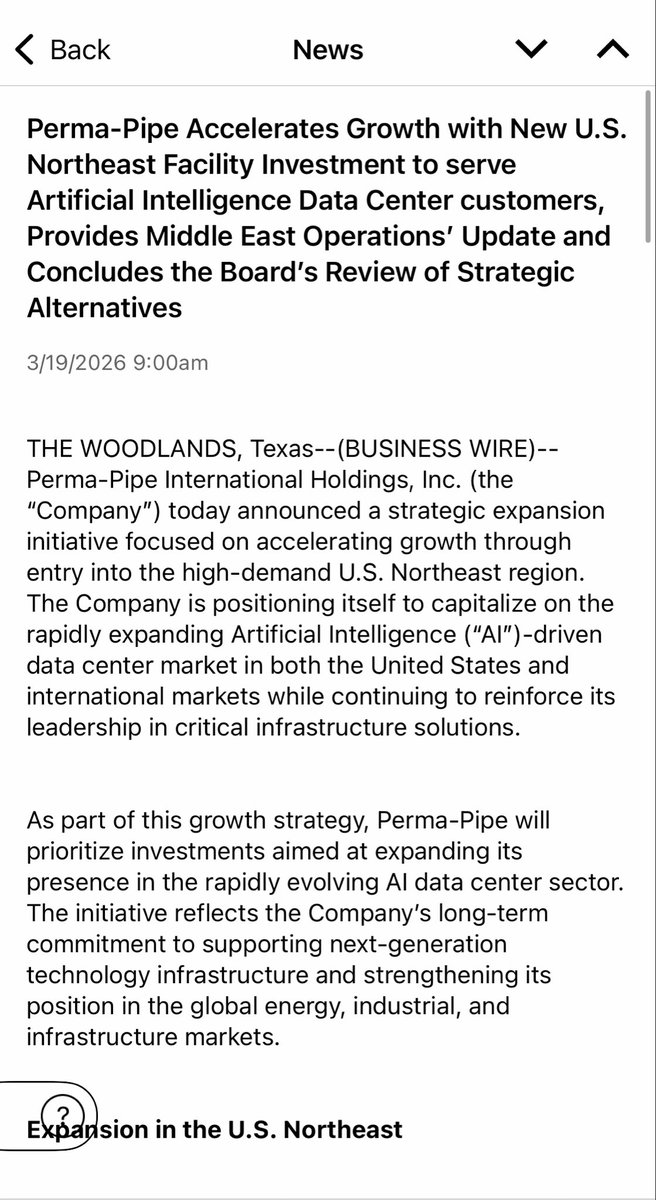

Mar 19

$PPIH 🚀 🚀 🚀

“We are excited to announce the expansion of our operations with a new facility in the Northeast, set to become operational in the second quarter of 2026. This facility will primarily focus on serving the rapidly growing AI-driven data center market, as well as the District Heating and Cooling sector. This strategic move supports our commitment to organic growth and strengthens our position as a global leader in the technology infrastructure ecosystem. Our primary focus will be on capitalizing on the significant potential in these key markets, both domestically and internationally. Furthermore, we are currently seeking to secure a new global banking agreement to provide enhanced liquidity, flexible financing options and expanded access to capital to support further investments in our growth.”

Perma-Pipe also reaffirmed its strong operational position across the Middle East and North Africa region.

“Perma-Pipe remains fully committed to its operations throughout the MENA region. Despite ongoing regional conflicts our business operations have not been impacted. We have implemented comprehensive business continuity plans designed to mitigate potential risks and aim to ensure uninterrupted service to our customers and maintain operational stability and safety across all of our facilities,” Saleh Sagr added.

4

4

37

5,679

Kyle Adams retweeted

Mar 19

Huge news out today for $PPIH 🔥

· Perma-Pipe Accelerates Growth with New U.S. Northeast Facility Investment to serve Artificial Intelligence Data Center customers

@KyleAdamsStocks

1

3

12

5,245

Mar 19

Nice little announcement from $BOSC today.

Will be interesting to see how India grows over the next year.

Mar 19

$BOSC BOS Expands India Presence with New Sales Partnership Agreement

stocktitan.net/news/BOSC/bos…

1

2

9

4,338

Kyle Adams retweeted

Mar 18

Great post from @ManthanTweets1

I think this explains the bulk of $TMDX sell off today. Overall healthcare sector took a hit, so this is magnified by $TMDX.

Last year the same thing happened, people freaked out due to increasing regulations.

The more regulated this market becomes, the better $TMDX does as it makes it harder for others to compete with the company’s already established OCS and NOP programs.

As mentioned by management multiple times recently, $TMDX is working hard to become an OPO and join forces with OPTN. This will only expand the company’s TAM.

Oftentimes, the market focuses on the “noise”, things that “could” affect $TMDX but ultimately end up helping. The company has proved from time to time again, that no competitor is anywhere near.

They just posted their best quarter ever, and Q1 26 looks even better. Europe will double the TAM. Collaboration with OPTN will be a massive catalyst. Theres just so much to look forward to.

$TMDX sold off probably due to latest guidelines released today for OPOs to follow in DCD cases. Most of these were in place after last year NYC article and hearing/HRSA action when OPOs were asked to implement immediate measures. At that time, Immediate and long term measures were planned. This one is long term measure and it will improve DCD process and Waleed was in full support of it. Just 2 days back, Waleed said they are in confidential conversation with CMS/OPTN about being integrated in some fashion to help modernize system. I assume that is about NOPConnect. Just read the transcript of oppenheimer conference this week. I believe this will increase TMDX dominance than anything else as following this protocol will take more time and OCS has significant time advantage than any competitor when it comes to avoiding ischemic damage. This is repeat of last year when post hearing & NYC article narrative was spread and stock sold off to 100$ that time. NOW - DCD adoption for Jan and Feb is at historic level and March is trending at same level.

Q1 currently pointing to 180m Rev.

aopo.org/donation-perspectiv…

4

2

43

9,485

Mar 16

$BOSC should do very well, especially since Israeli defense spending about to go through the roof.

4

3

28

7,026

Mar 15

$TMDX 🚀

I’ll buy more if it continues to dip :)

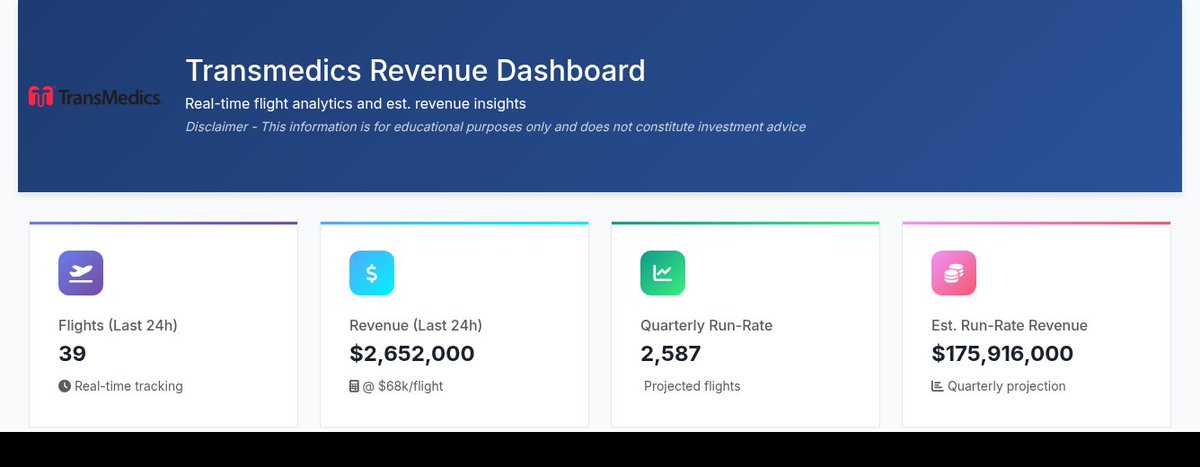

$TMDX did 39 flights and grossed an $2,652,000 (est) in the last 24 hours.

They are on track to do 2,587 flights and gross $175,916,000 (est) this quarter.

Link - singularityresearchfund.com/…

Disclaimer: This information is for educational purposes only and does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and you should not treat any of the content as such.

2

36

6,034

Mar 12

$BKTI guidance seems ultra conservative, and likely doing this to beat and raise throughout the year like they did in 2025.

Overall, strong Q4, but 2026 EPS / revenue guidance seems low. Will be interesting to learn more on their 2030 vision in the investor conference next month.

The company expects gross margins above 50% in 2026, which is crazy to see since they were in the low teens just a few years ago.

$BKTI BK Technologies Reports Fourth Quarter and Full Year 2025 Results Above Guidance accessnewswire.com/newsroom/…

5

2

22

6,319