Rational thinking brings you nowhere in a clown world.

Joined May 2013

- Tweets 23,327

- Following 39

- Followers 631

- Likes 16,678

486 Photos and videos

Impact Valor retweeted

Jun 15

Hes 17-1, not bad or humiliating tbh, just a great warrior who lost today

1

1

22

7,659

Impact Valor retweeted

Jun 12

Is the exit liquidity being disobedient!

12

18

709

26,599

Impact Valor retweeted

Jun 10

No, real yields fall as the Fed will not hike rates nearly enough to keep pace with rising inflation. That is what traders don't understand. But they will learn a lesson the hard way.

10

5

74

8,423

Impact Valor retweeted

Jun 7

bro crashed the whole market and is now trolling

6

2

252

15,087

Impact Valor retweeted

Jun 8

Is that how many years you expect to get for securities fraud?

90

19

692

48,816

Impact Valor retweeted

I know it's difficult for some of you.

Reading is hard.

Sentences longer than six words can be frightening. Metaphors arrive unannounced and suddenly half of Twitter is hiding under the desk screaming "LLM!" like medieval villagers spotting a telescope.

"That's not a sector rotation. That is a gravitational, once-in-a-generation event."

"Sounds like an LLM."

No, it sounds like English.

The fact that a sentence contains more than two syllables and wasn't written in the style of a sports betting advertisement does not mean a machine wrote it.

It means somebody finished secondary school.

What fascinates me is that this has become the universal refuge of the intellectually bankrupt.

Can't answer the point?

LLM.

Don't understand the analogy?

LLM.

Encounter a word that doesn't normally appear between "bro" and a laughing emoji?

Definitely LLM.

By that standard, every book in a library was written by artificial intelligence and Shakespeare was clearly running GPT-Elizabethan.

The tragedy isn't that you think it sounds like an LLM.

The tragedy is that you've spent so long reading Twitter that ordinary literacy now appears supernatural.

A man points at the moon and you become suspicious of the finger because it contains punctuation.

I pitty you.

Sorry you are that.

3

1

11

635

Impact Valor retweeted

This is a charming little theory, mostly because it mistakes a spreadsheet coincidence for a capital-flow model.

“AI market cap increased by $19 trillion” does not mean $19 trillion of cash was transferred into AI stocks. Market capitalisation is not a bank account. It is last price multiplied by shares outstanding. When Nvidia rises, nobody needs to gather the full increase in market cap from BTC holders in a wheelbarrow and deliver it to Nasdaq.

That is the first error.

The second is calling BTC “the most liquid risk asset on earth.” No. It is a risk asset, certainly. Liquid compared with many speculative tokens, yes. But compared with Treasuries, major FX, S&P futures, large-cap equities, or actual institutional funding markets, this is adorable.

The third error is assuming that BTC is being “drained” to fund AI IPOs. That requires evidence of a flow channel: BTC sales, fiat conversion, capital migration, allocation into AI primary issuance, and enough scale to explain the price move. Otherwise it is just a bedtime story for people who discovered correlation and mistook it for causation.

The fourth error is confusing public-market revaluation with IPO funding. AI market cap expansion is mostly repricing of existing listed firms, not fresh capital formation equal to the headline number. A stock going up does not mean the economy found new cash equal to the market-cap increase. It means the marginal buyer repriced future expectations.

BTC is falling because marginal demand is weakening relative to marginal supply. ETF flows, leveraged positions, miner economics, treasury-company pressure, derivatives liquidations, liquidity withdrawal, and declining speculative appetite are all actual mechanisms. “AI got big” is not a mechanism. It is a slogan wearing a calculator.

The phrase “13x the size of Bitcoin” is not analysis either. It merely compares two market capitalisations as though size alone explains capital movement. By that logic, every large asset class should constantly drain every smaller one. Strangely, reality declines the invitation.

If BTC were truly the superior reserve asset its promoters claim, AI investment would not drain it. Capital would use BTC as collateral, settlement, treasury reserve, or transactional infrastructure. Instead, when productive opportunities appear elsewhere, capital leaves the speculative shrine and goes looking for cash flows.

That is the part being avoided.

AI equities at least claim earnings, infrastructure demand, productivity effects, enterprise adoption, and future revenue. Whether overvalued or not, there is a business model underneath the froth. BTC offers the hope that someone later pays more for the same inert object.

So no, BTC is not crashing because AI created “$19 trillion” and sucked the money out through a golden straw.

BTC is falling because its marginal buyer is weakening, its leveraged structure is fragile, its institutional wrappers are procyclical, and its economic utility has not matched the narrative sold around it.

A market cap comparison is not economics. It is numerology with better lighting.

8

14

110

13,325

Impact Valor retweeted

Jun 5

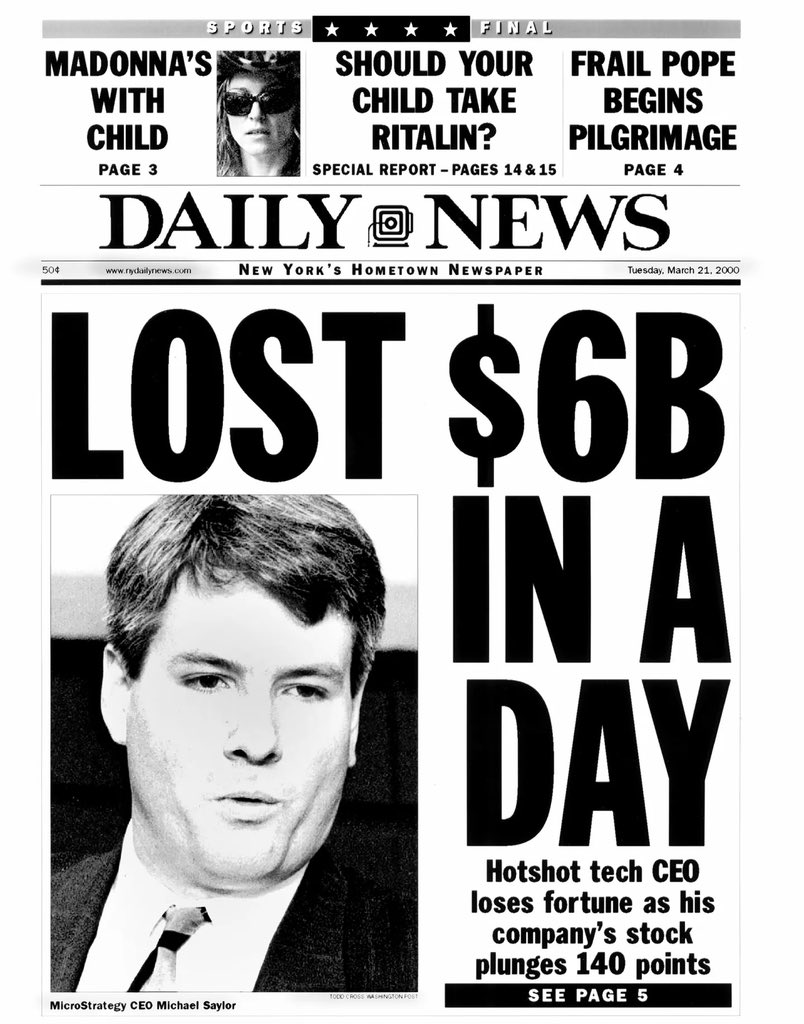

Bitcoin isn't crashing below $60k because Saylor sold 32 BTC.

It's crashing because $19 trillion of new AI market cap got created in 12 months... 13x the size of Bitcoin.

The most liquid risk asset on earth is being drained to fund the biggest IPO cycle since 2000.

314

433

4,697

836,540

Impact Valor retweeted

Too bad it wasn’t the femoral artery

1

1

510

Impact Valor retweeted

Shame he didn't shoot his penis off, keep him from polluting the genetic pool.

4

2

384

21,238

Impact Valor retweeted

Jun 3

There’s no way I’d invest in this dude after watching him crash out.

1

3

38

2,407

Impact Valor retweeted

Jun 3

LOL, Build a whole platform and ecosystem then blame users for things fallen apart is diabolical. Use a peer-reviewed, academic approach to find a solution same as you built the blockchain.

5

1

20

8,696

Impact Valor retweeted

Jun 3

1

15

1,615

Impact Valor retweeted

Jun 3

I got scammed by a guy who works for Charles, and IOG protected him.

Charles deserves everything coming to him. It’s over. Pathetic excuse of a man. Fucking pathetic.

2

3

84

7,075

Impact Valor retweeted

Trying to absolve himself of responsibility to avoid blame and potentially prosecution

1

4

107

5,623

Impact Valor retweeted

Jun 3

He's acting like he didn't personally dump over a billion dollars worth of tokens lmao

1

3

296

8,138