Obsessed with Digital Things Finance Business, Sometimes Sports. EVP @thewagency. Speaker: @HeroConf @SMX @ShopTalk Faculty @JohnsHopkins. Views = Mine

Joined September 2011

- Tweets 33,440

- Following 890

- Followers 2,899

- Likes 155,465

1,300 Photos and videos

Jun 12

The blatant dishonesty of our elected representatives is galling.

Let’s replace this with honest, real-world numbers. Elon’s net worth is ~$1.14T as of 5 pm ET today. A 5% tax on that would raise* ~$57B.

The best estimated cost for universal free college & trade school is ~$75B/year, which was provided by PWBM & Urban Institute- imperfectly priced in the demand side response & ignores the supply side reality. Nothing in any of those has modeled the interaction between surging demand plus institutions with no price discipline and a federal payer.

A more realistic scenario is a $150B first year price tag, slowly falling in real terms over the next 10 years as new supply (seats) comes online and people realize free degrees don’t have the same value but still have a significant time cost.

So: no, a 5% tax does not pay for this. It doesn’t come close.

Brad, a 5% tax on Elon's trillion net worth would literally pay for free college and trade school for every American.

And with the market's growth, he still would be worth over a trillion dollars!

You don't think that's worth it?

Community note

5% of $1.2T is $60b. 8m students in BA/BS programs on average pay over $20k/yr, or ~$160b/yr for BA/BS degrees only.

That tax could not cover even half of only US bachelor degree costs for just 1 year, excluding grad, ass., or trade degrees totaling another ~10m students.

nces.ed.gov/programs/coe/i…

bestcolleges.com/research/colle…

5

307

Jun 2

The 5th Amendment exists.

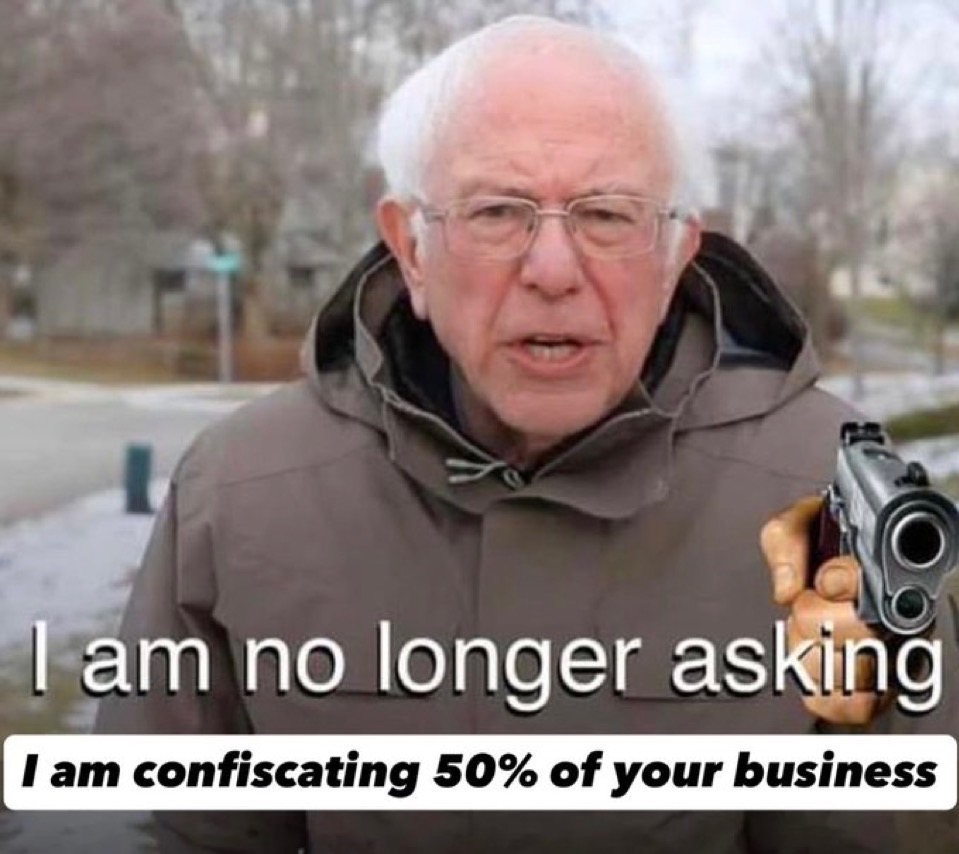

The real effect of this: it would destroy ~20% to ~45% of the value of every investment in your brokerage account, 401(k) or IRA. It would make the US government (in whatever form/fashion this bill decides) the controlling shareholders in the entire technology sector. And - most critically - it would relegate every entrepreneur who spends his/her life building something from an owner to a temporary custodian.

The fact that this was even entertained sickens me as someone who has come from relatively little. It's the most Anti-American idea I've ever heard.

@BernieSanders is not fit to be a sitting United States Senator. We're well past the point where his antics are those of a kooky old wanna-be socialist.

Jun 2

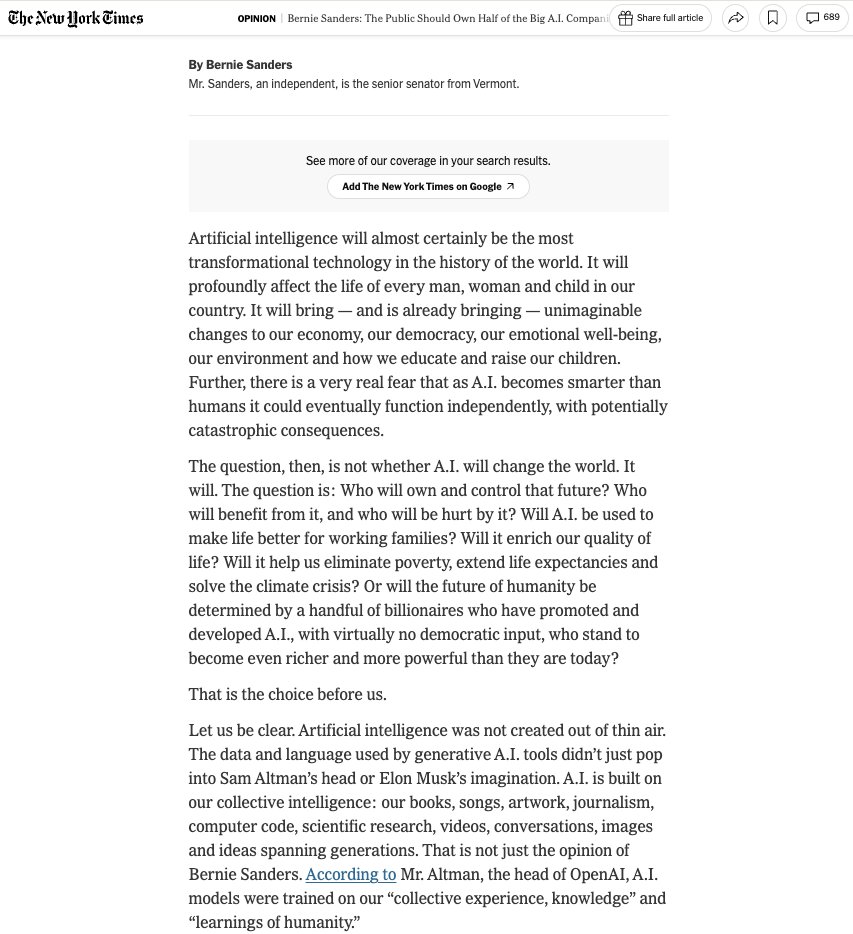

I will soon be introducing a bill to give the public a 50% ownership stake in the largest AI companies in America.

This would guarantee that the trillions created by AI are used to improve the lives of all of us — and block oligarch decisions that harm the American people.

2

136

Jun 1

If my goal was to destroy the US' global domination in finance, innovation & technology, I could not run a better playbook than @BernieSanders.

This is the most insane thing I've read in months. Nationalizing 50% of some of the largest companies in the world would immediately decimate millions of investors beneficiaries (including teachers, nurses, government workers, retirees).

These companies are owned by individuals. Bernie Sanders is proposing that half your NVIDIA shares or half your Alphabet shares or half your Microsoft shares go to the US government. That's the end state.

And if you say, "Well I don't own those in my retirement, I only own $VOO [or whatever ETF]" - guess what accounts for 40%-45% of that ETF's total holdings?

The fact that a sitting US Senator wrote this should shake every American to his/her core. There is nothing more anti-American than stealing from teachers, doctors, social workers, retirees & ordinary men and women so Sanders can give out [whatever] to his preferred constituencies.

2

7

322

May 29

Collin is exactly right.

It is actually cheaper for us to build maintain several tools in-house than it is to continue paying thousands per month in costs. Yes, that includes maintenance hosting updates.

We are finalizing development of one tool for under $10k all-in that will *upgrade* a $1,599/mo subscription. Hard to beat that from an investment standpoint.

May 29

We cut $2,200 a month off our software stack last quarter and didn't lose a single capability. Most of what we canceled were API wrappers charging us for data we already owned.

Strip away the marketing, and a lot of DTC SaaS tools are just a connection to an ad platform's API that reformats data you can already pull yourself.

Some of them run $2k /month and climb as you add clients. For too long, software has been operating at 80% gross margins with marginal cost of scale.

So I got relentless about our stack. Every quarter and before any renewal, we run it through three questions:

1. Are people on the team actually using this?

2. Is it expensive enough to deserve real scrutiny?

3. Are we paying for two tools that do the same job?

Anything that can't clear those gets cut.

There's a good chance a similar number is hiding in your stack. If you want a second set of eyes on what's actually worth keeping, I'd be happy to take a look.

2

5

377

May 29

Because of Griggs v. Duke Power Company.

SCOTUS ruled unanimously that under Title VII, any hiring screen producing “disparate impact” on a protected class must be demonstrably job-related and a business necessity…and the burden of proof sits on the employer, not the plaintiff.

Companies responded (predictably) by moving to less rigid hiring assessments & expanding the use of unstructured interviews, as those are legally safer despite being objectively less predictive.

In essence, companies traded more accurate, more consistent prediction of applicant success for fewer lawsuits.

If IQ is so useful why dont employers just give an IQ test for the interview and hire the highest scorers ?

4

382

May 26

Someone should tell @NYCMayor that NYCHA sits on the largest concentration of substandard housing in the City of New York, by every conditions metric available, including the agency's own internal queue of ~612,000 open repairs across its portfolio of ~2,500 buildings (245 per building). By the NYCHA's own physical needs estimates, ~$78B (yes, billion, with a "B") in repairs are needed across the portfolio right now.

The "worst" private landlord in NYC history carries 4,872 open HPD violations across 24 buildings (201 per building; landlord = Margaret Brunn)

So: the worst landlords in the City are better than the City itself.

May 26

NOW: Mamdani says his admin will transfer ownership from bad landlords to non-profits.

“For buildings that have suffered chronic neglect, we will work to transfer ownership to responsible stewards.

Stewards that include community land trusts, non-profits, or even the tenants themselves.”

1

1

7

263

May 26

Just the repairs needed per building (based on the NYCHA's own estimates) are staggering:

~$31.2M PER BUILDING in needed repairs

~$439,275 PER APARTMENT in needed repairs

~3.4 open work orders PER APARTMENT

No private landlord comes close. You don't have to like private landlords, but god damn.

1

64

May 23

This is a categorically insane statement.

At $400k/yr as a *salary*, you can live a wonderful life with relatively little stress. Save $8k/mo. After taxes, you’re living on $15k-20k/mo.

By 45-50, you have a wonderful nest egg of $4M-$8M. You’ve lived a life better than 99% of the world on your way to it. And, since Meta does love to give out options & incentive units, they likely have another $1M-$2M in stock, which is just the cherry on top of the rich life sundae.

For 99% of the population, that is a better life than what they’ll ever experience. And, the best part of the deal is that this high W2 salary provides them optionality for anything else. If they want to build a side project? No problem. If they want to angel invest or advise startups? They have the resources & a resume tailor-made for it. If they want to travel, enjoy life, raise a family? Can do.

The notion that every job is a jail sentence simply must go. The reality is that 98% of the population is better off working for someone else.

May 21

This might be a hot take but I know someone at meta who makes $400k a year and is quite literally capped at that number for life - likely will never get a promotion strong enough to change that.

9-5 until they’re what, 50?

This is not living. No matter the salary.

72

48

1,799

808,188

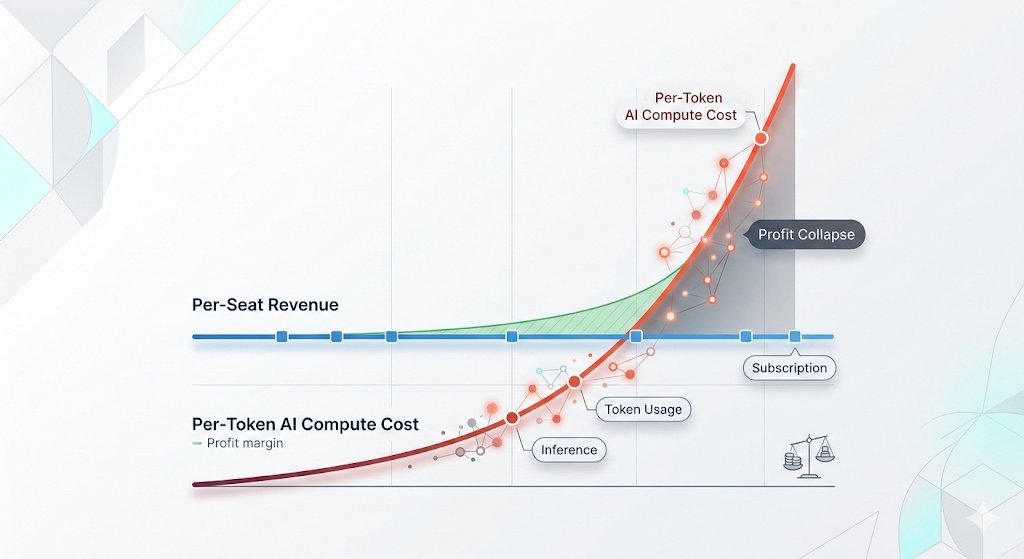

May 22

The Microsoft and Uber stories are being misread by most people because the reading skips the part where neither company actually scaled back.

MSFT is migrating 100k engineers from Claude Code to Copilot (which they own capture every prompt bit of user feedback to improve their own product). That's a different thing vs. cost capitulation - it's MSFT electing to build internally, where they can use frontier capacity at cost vs. at cost-plus-markup AND make that investment do double work (improve Copilot save $$$).

Uber's CTO said the company was "back to the drawing board." That doesn't entail that they're no longer using the tools - it means they're rebuilding their forecasts/models/FinOps around consumption they underestimated by an order of magnitude. Engineers spending $2k/mo on tokens aren't doing it for fun; they're doing it because the productivity differential justifies it.

Both examples point to the same conclusion (and it isn't the one being reported). It's "this got valuable enough that usage exceeded projections in a fraction of the time" aka Jevons paradox showing up in real time - not the end of the subsidy era.

The market structure emerging from this is bifurcation, which is what is missed in the entire conversation.

On one end: Frontier inference (reasoning, long context, agentic workflows) is consolidating rents at the top. Demand at that tier is supply-constrained, not price-sensitive.

On the other: Commodity inference (the GPT-4-class workloads that defined the category 18 months ago) is collapsing toward marginal cost. Equivalent-capability pricing is now ~1/600th of what it was 6 years ago. Those 2 curves moving in opposite directions are the entire pricing landscape. They have almost nothing to do with each other. Treating this as a single number is an analytical error that's leading to most of the bad takes.

The implication for procurement is straightforward: the cost differential between running frontier on everything vs. routing intelligently across frontier commodity tiers is now 100x to 500x on equivalent workloads. That delta is the rent (and likely, the most valuable infrastructure business that has yet to be built). Whoever builds it will capture more durable margin than either the layer above or the layer below. The labs know this, which is why they're racing to wrap routing into their own platforms. Most enterprise buyers haven't bothered to figure it out (they're too busy building stuff for their business to think about how to optimize the cost of doing it), which is why their spend looks categorically insane.

The Uber analogy gets reached for a lot in this conversation. It doesn't hold. Uber subsidized rides on the way to a clean rent-extraction end state (i.e. own the network, raise prices, let the unit economics work).

AI labs can't run that playbook, because the terminal state is multiple breakthroughs away and the "extraction" time for a frontier model is 12-18 months. Fortunately for them, their strategic capital is patient in ways venture money isn't, and their end state is bifurcated, not unitary. The right-sizing pressure people are looking for isn't going to land at the model layer. It's going to land at the application layer, on every company that raised on the assumption that commodity inference would stay subsidized long enough to build a moat. That subsidy is ending, but the labs aren't the ones who have to absorb the cost; it's their customers' customers who will end up holding the bag.

The question that follows naturally is: how do the labs absorb training costs that increase 10x per generation if commodity inference falls to zero.

It has an answer the labs say out loud and most analysts ignore. They don't absorb it through token margin. They absorb it through a combination of (1) enterprise bundle contracts, (2) (eventually) through agentic outcome pricing & (3) ultimately through strategic capital treating training CapEx as optionality on capability scaling as opposed to cost-of-goods. The right comparable for an AI lab is late-stage pharma. Both have decade-long burn, binary terminal values & a capital base sized to the option vs the current P&L. That model survives commodity compression in a way SaaS economics can't. It also fails differently when it fails, which is the part the writedown discourse hasn't started pricing in yet.

The "subsidy era ending" framing sounds good, but it's analytically wrong. The subsidy era didn't end. The undifferentiated consumption era is ending.

May 21

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

3

6

1,749

Sam retweeted

May 19

The disclosure included 3,600 trades in 3 months

That’s around 40 trades a day

Many of them are $1,000 - $15,000 a trade

1,000 of different stocks were traded

Does anyone really think he’s managing the account?

May 19

“The President doesn’t sit at the Oval Office on his computer on a Robinhood account buying and selling stocks. That’s absurd.” @VP 🤣🤣

15

9

89

35,909

May 19

If the argument here is that ringing up stuff that customers selected from the store you work in = "making the company money"....I think we need to take a step back.

You didn't design or build the store

You didn't vet/source the goods sold

You didn't pay for the inventory

You didn't pay the OpEx (electricity isn't free!)

You didn't advertise/market the store

You took no risk.

Also: if you "make" the company $2,000 in gross, for most retail that's ~$200 net. Your $71 "made" is actually ~$100 to the company (FICA, fringe, compliance). So, you got ~25% of the net value you "created".

That's pretty fair, wouldn't you say?

May 18

No I work in retail where I can quite literally see how much money I’m making the company. I’ll do anywhere between $600 and $2000 in a 5hr shift while only making $71. It’s more radicalizing to see the dramatic extent at which your surplus labor is being extracted

Community note

Retail net profit margins ($'s of profit / $ of sales) average 5.6%. On $200-$2000 of sales, that means the net profit for the business was $33-112 (after all expenses). If the poster is making $71, they are capturing 39-68% of the value (after all costs outside their labor.

pages.stern.nyu.edu/~adamodar/New_…

1

4

1,065

May 19

The structural advantage in any system with multiplicative dynamics is (almost) always lower variance at acceptable mean, not higher mean at any variance.

1

59

May 12

The more I look at consumer behavior, the more convinced I become that the sum of our vices remains constant - the only thing that changes is the underlying distribution.

1

2

142

May 11

I've been saying this for 2 years. Interest stacks / LALs for niche-y products make mathematical sense.

Instead of asking the algorithm to surface patterns across an audience of ~270M people, you compress the search space to 10M people. End result? (1) Better prior (if real buyers are ~0.5% of the broad audience better targeting increases density to 5%, you've raised the probability of a conversion by 10x before learning); (2) faster signal acquisition (Meta needs ~50 conversions/week/ad set to exit learning. Higher buyer density = more stable customer acquisition = less wasted spend faster learning exit.

This is particularly true with LALs, because they do something IS can't: they cluster in Meta's latent feature space capture unique, non-intuitive buyer/prospect signatures that no IS could possibly surface.

End of the day: broad can be great if you have a product in a known category with massive TAM (i.e. buyer density in the general population is sufficiently high that the costs of segmentation are higher than the benefits). But if you have a product that targets a niche buyer (or if you have multiple buyer segments), LALs/IS can make a lot of mathematical sense.

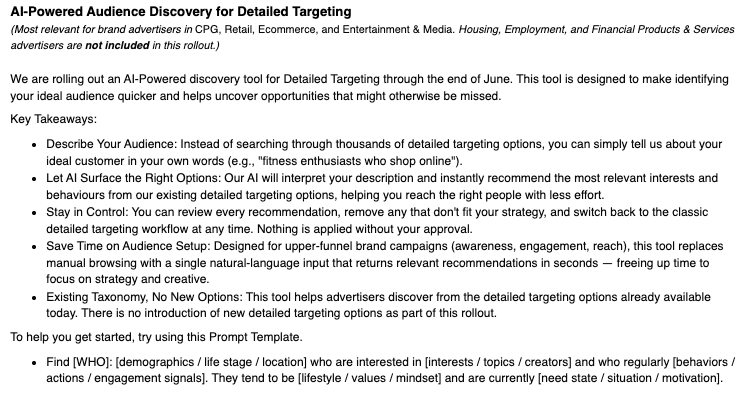

May 11

Could Interest targeting on Meta be making a comeback?

This new update in June will allow advertisers to describe their target audience instead of searching through thousands of Meta's interest options.

Meta will use AI to surface the right options, reminiscent of TikTok Ads Manager's "recommended interests" feature.

This runs counter to the popular narratives right now: "media buying will be dead soon" "Meta is simplifying the ads experience" etc

The number of complex ad product rollouts has accelerated in the last 12 months: this, incremental attribution, expansion of Value Rules, Profit Optimization, lead quality optimization...

Optionality in the media buying workflow is getting MORE, not LESS complex

1

5

872

May 8

Remind me who Beyoncé, LeBron, MJ, Taylor Swift & Oprah “extracted”

If you genuinely believe that “billionaires are inherently extractive” then I’m curious at what level that stops.

Is it $500M? Because that person is ~7 years away from being a billionaire, assuming decent returns & no colossal mistakes.

What about $250M? Only 15 years away.

Is the SMB owner throwing off ~$5M a year, living on $500k and optimizing taxes to invest $2.5M a year in equities and some real estate (exactly what has been preached by people on all sides of the political spectrum - save more than you spend! Be fiscally responsible. Invest in your future) inherently extractive? Because the person that does that for 30-40 years, and generates 1 standard deviation above median returns, is either at or damn close to “billionaire” status.

There’s a reason virtually every study of billionaires admits they undercount precisely this “silent” segment. I personally know multiple people who did exactly this. They aren’t flashy. You’d think they were well-off, but never guess they were closer to 10-figures.

Are they inherently extractive?

May 8

The elite rage at @AOC for saying something obviously true - billionaires are inherently extractive - is amazing. It’s the Epstein class at work. Snowflakes all of them.

2

6

306

May 8

The path that produced the billionaire is the same path that produced the millionaire next door, the same path that produced the comfortable retirement of every disciplined saver you know (like the school teacher who saves for 40 years and leaves $3M to her kids).

AOC’s argument doesn’t actually target billionaires - it targets the mechanism that produces wealth at every level, applied at a threshold that seems rhetorically & politically convenient. That threshold won’t stay where she put it, because the moral framing doesn’t have a stopping point. Today, it’s billionaires. Tomorrow, it’s centi-millionaires. Then it’s “potential billionaires” (I.e. anyone with the capacity to earn & invest substantial money ($2.5M a year) over a sufficiently long time horizon).

The doctor with 3 offices & a net worth of $20M is wealthy beyond what most Americans will ever see. So is BigLaw lawyer with $30M saved after 30 years of practice. So is SMB owner with $50M. Every one of them is a ‘billionaire in waiting’ - the only question is investment returns & time. Every one of them becomes a target once the precedent is set that majority preference can override individual wealth accumulation.

The honest version of this debate isn’t ‘should billionaires exist.’ It’s ‘should disciplined wealth accumulation be permitted at all.’

If the answer to the above question is yes, then the billionaires are legitimate by extension. If the answer is no, then we’re not arguing about billionaires - we’re arguing about whether the savings account, the IRA, the family business & the patient stock portfolio should exist as a path to anything meaningful. The only differences between the disciplined saver and the billionaire are: (1) how much they invest, (2) where they choose to invest their capital and (3) how long they’ve been doing it.

If we’re going to debate this, let’s have an honest debate @AOC

@RobertMSterling figured you might have a thought about this.

May 7

AOC: “There’s a certain level of wealth and accumulation that is unearned. You can’t earn a billion dollars. You just can’t earn that. You can get market power, you can break rules, you can abuse labor laws, you can pay people less than what they’re worth, but you can’t earn that”

1

2

337

May 7

For those who don't know about Congressman Khanna:

He's a sitting member of Congress & one of the ~600 most powerful people in the world - including other heads of state, members of the US Congress, CEOs, POTUS/VPOTUS, Cabinet Members, etc.

His net worth is far in excess of $100M (one of ~29,000 people world wide with a 9-figure net worth - or Top-0.0004% of the population). That seems pretty wealthy.

He is - definitionally - one of the "wealthy & powerful"

The wealthy & powerful know that if I succeed they have major issues.

They have seen me fight against the Epstein class, for a billionaire tax, against aid to Israel, & against the war in Iran.

So they have taken to launching ad hominem attacks on me.

I welcome their hatred.

2

131

May 7

Let’s address some things here:

1. ~$65M of this is one-time comp to make Nichol whole for the loss of his unvested Chipotle stock.

2. When you compare steady-state FTE:CEO pay, you end up with a ~$25M:$40k ratio, or 625:1. The S&P 500 average is 285:1. The delta there is explained by relative size/complexity (Starbucks is a top ~25% F500 company, so CEO comp should be higher than the mean).

3. Any residual difference is bundled pricing of (a) base comp for the role, (b) lock-in premium against poaching, (c) insurance against unplanned transition cost & (d) signaling premium that affects succession candidate quality.

But let’s make the bigger point: the CEO of Starbucks’ pay should not be compared to the median worker. You wouldn’t compare LeBron’s comp to be median stadium usher. The relevant question is whether Nicholas is paid fairly relative to the other CEOs capable of executing a turnaround of a $120B company. Given his record at Chipotle ( 700% gain), I’d argue Nichols’ steady-state comp is fair or even below market.

May 6

The Starbucks CEO made $97 million in 2024.

The median Starbucks barista made $14,674.

That's a 6,666/1 ratio.

a barista would have to have started working 4,643 years before Jesus was born to earn what the CEO made in a single year.

1

369