Not investment advice. Personal opinions only. I may hold positions I discuss.

Joined July 2025

- Tweets 787

- Following 100

- Followers 1,381

- Likes 1,220

149 Photos and videos

Pinned Tweet

30 Dec 2025

Profiled several companies this year. More to come in 2026!

✅Tantalus (utility software & grid intelligence)

✅Greenland Resources (molybdenum junior minor)

✅Rumbu Holdings (funeral home roll-up)

✅Cybeats (SBOM & cyber compliance)

✅ALUULA (advanced composite materials)

✅Renoworks (vertical SaaS for home reno)

✅Freightos (digital freight infrastructure)

✅Kneat (enterprise validation for life sciences)

$GRID.TO $MOLY $RMB.V $CYBT.CN $AUUA.V $RW.V $CRGO $KSI.TO

Link to each write-up 👇

1

1

11

1,721

JB retweeted

May 25

We are approaching the end of the exploratory phase where you need to use as much AI as possible just to explore and see what's going on.

Companies are looking at real costs and ROI now, so we're in the next stage.

This will also prove that a lot of B2B SaaS is more protected than people think, because you do need the best reasoning models to extract value on top of them & right now the cost is high

May 21

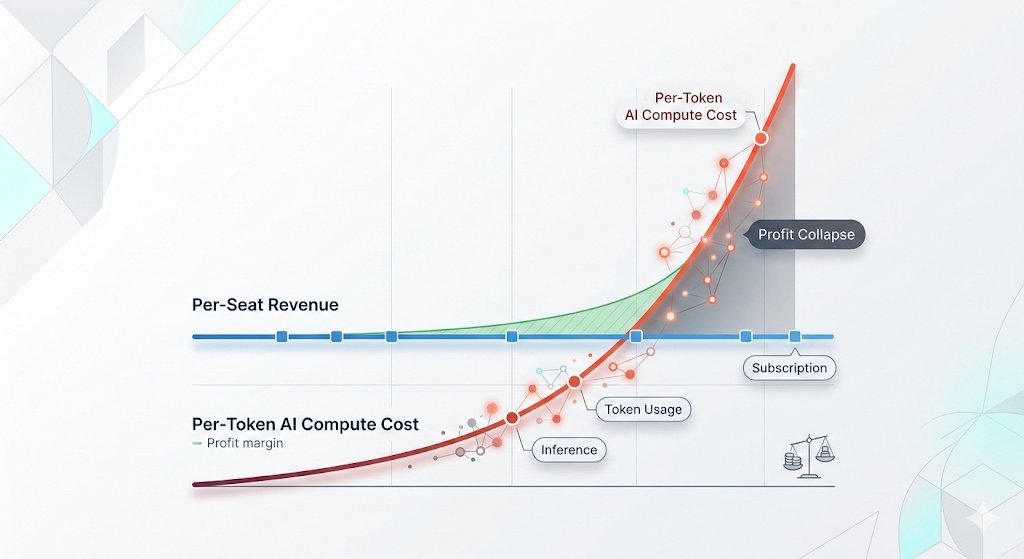

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

3

1

49

11,761

JB retweeted

May 22

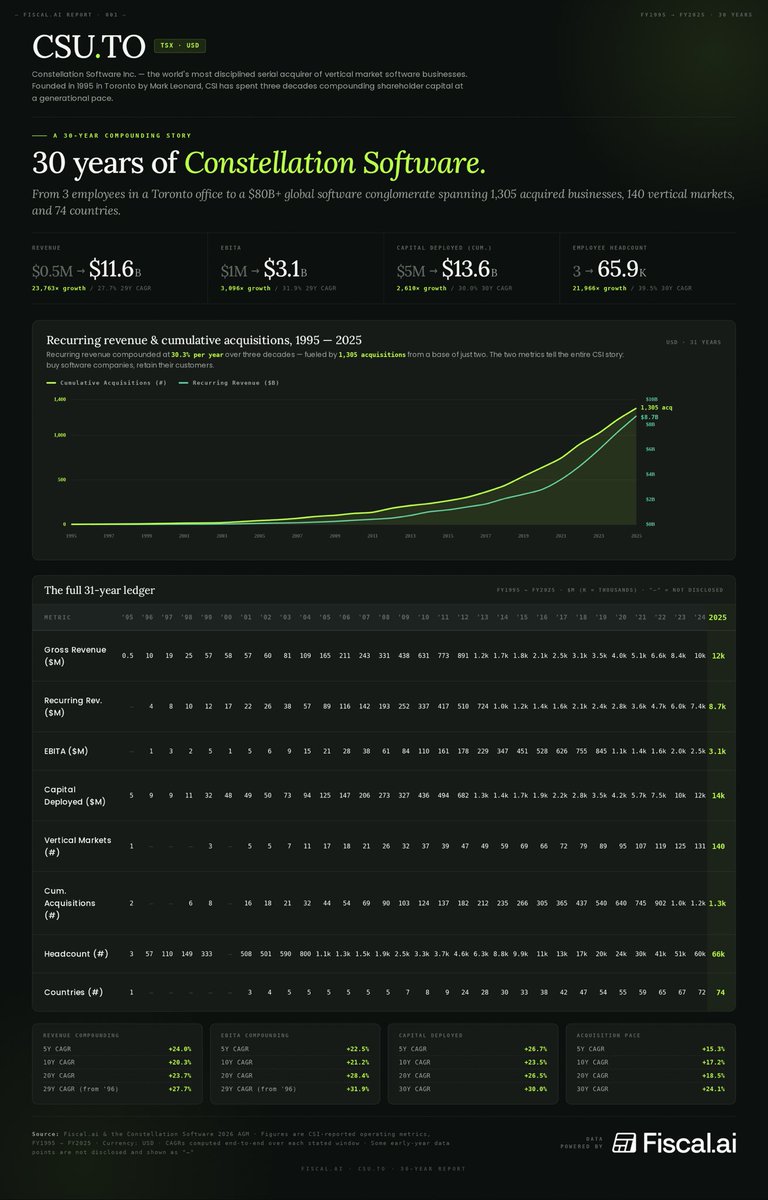

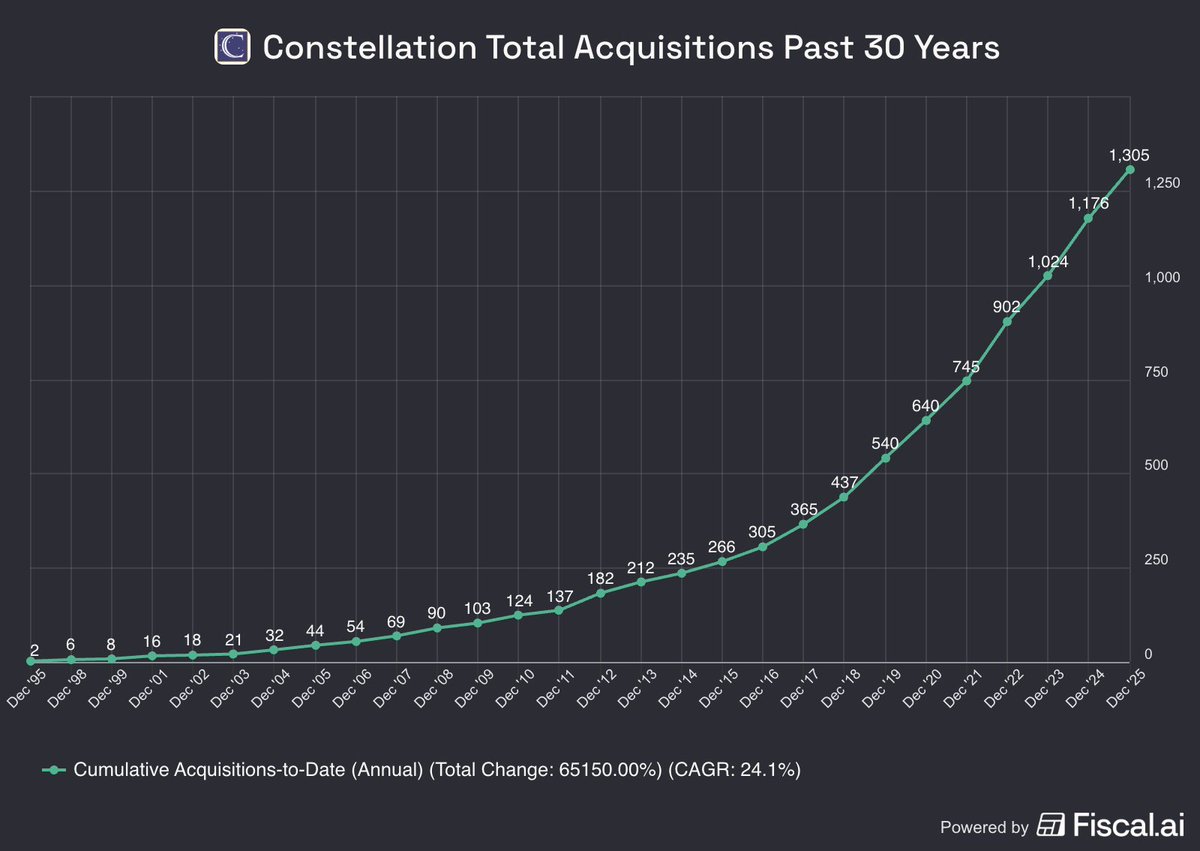

"Q2-to-date brings TTM capital deployed on acquisitions (and the equity investment in Asseco) to $2.835B, nearly double $1.50B in the previous TTM period." $CSU

2

3

74

9,331

JB retweeted

May 22

$CSU.to

"With Conduent, Q2-to-date brings TTM capital deployed to $2.835b, nearly double the $1.5b in the previous TTM period... Constellation's businss model is scaling and taking advantage of the dislocation in public software valuations." - RBC

3

10

82

6,410

JB retweeted

May 22

Record deployments this year for $CSU.to.

If this was ever listed on the Nasdaq.... (it never will be thankfully)

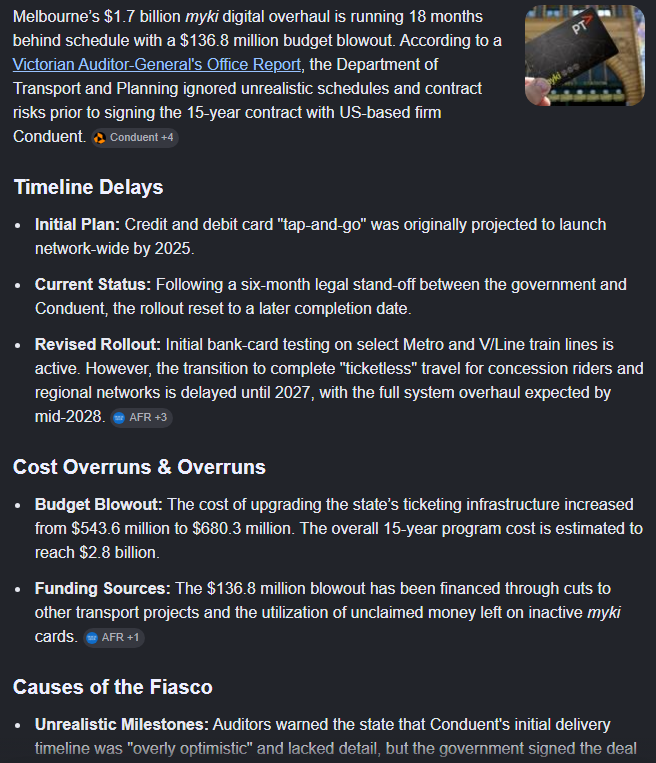

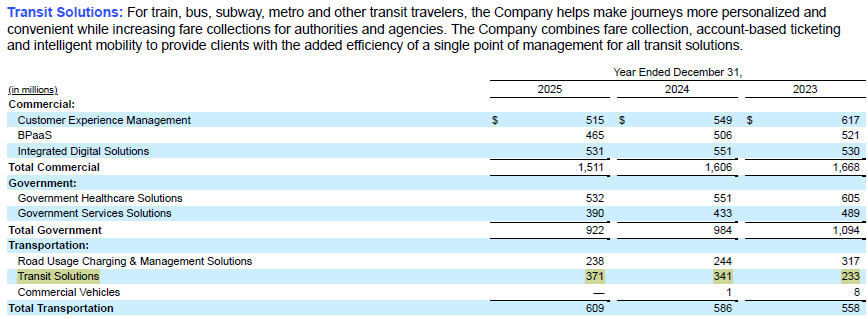

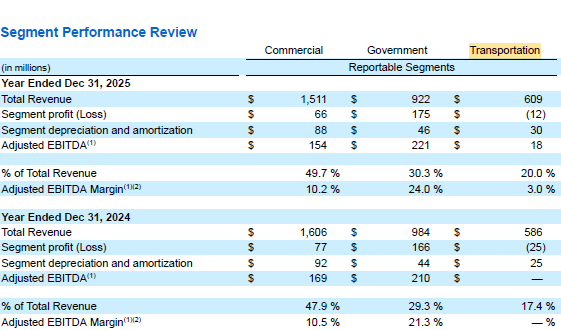

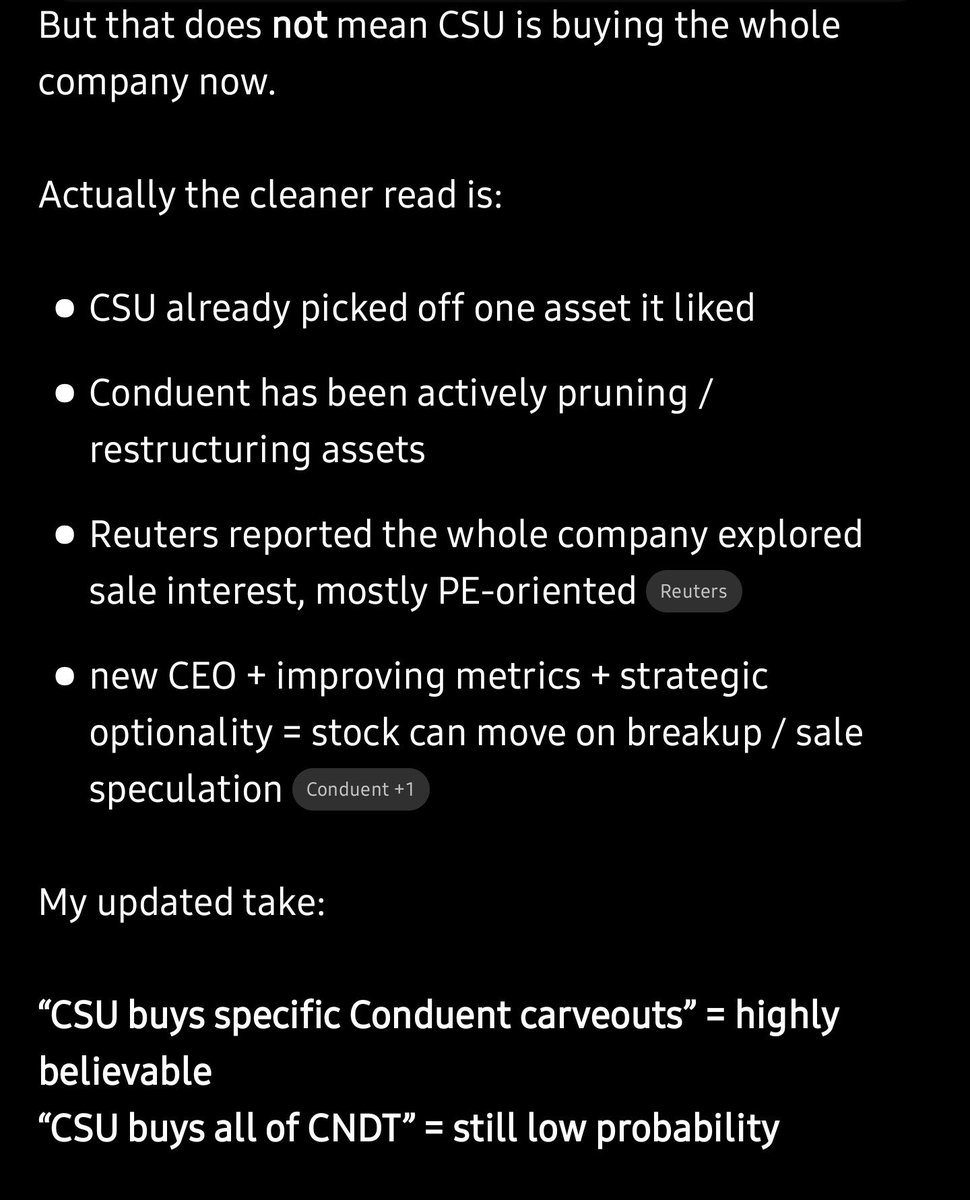

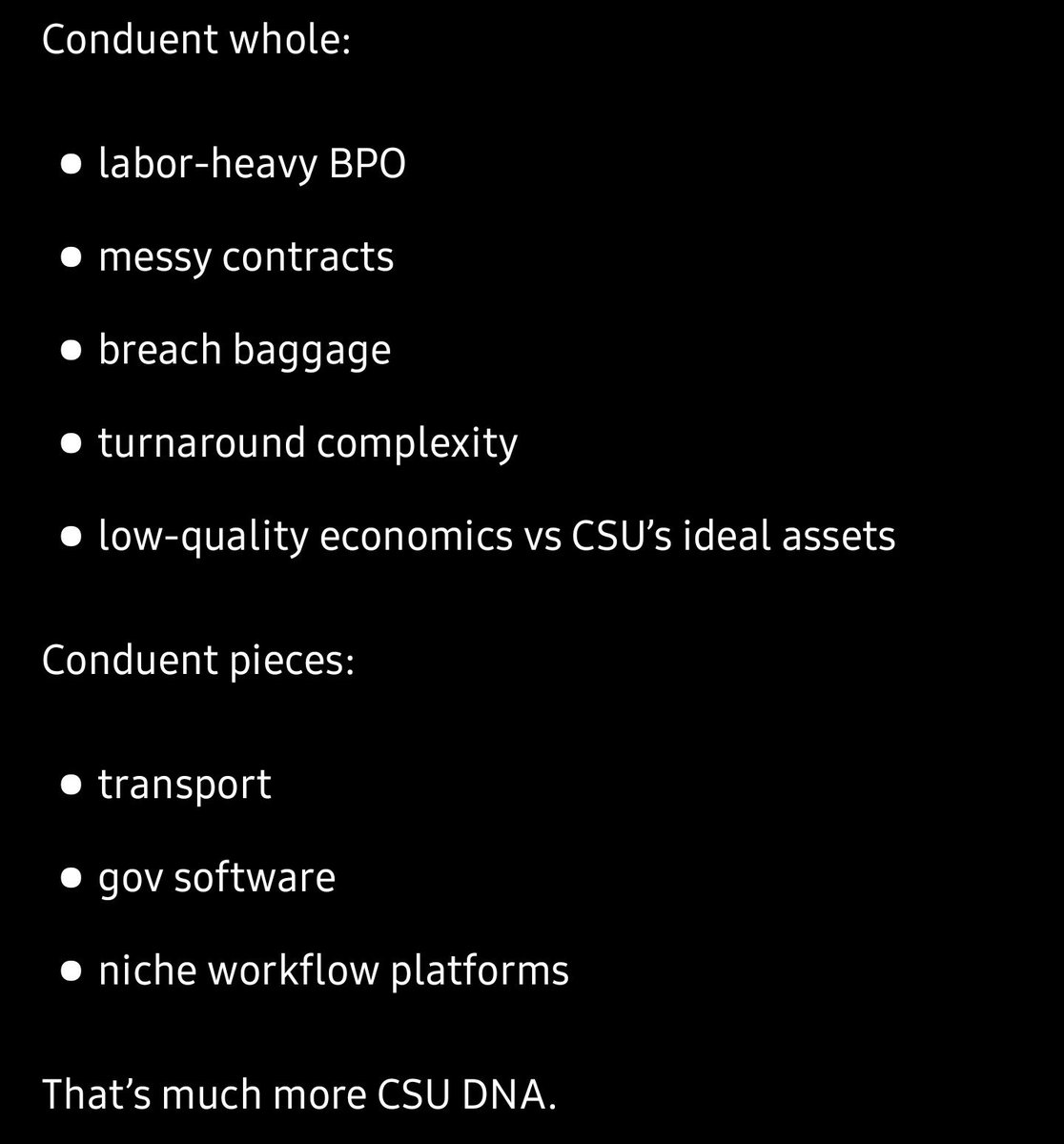

$CSU.TO carves-out transportation assets - again - from $CNDT for $164M

They might be buying the "Transit Solutions" segment that generated $371M in revenue in 2025, implying a ~0,4x Sales multiple

CNDT is a forced seller due to an total disaster in the implementation of $1 billion transport contract in Melbourne 🇦🇺

Victoria Auditor-General's Office issued an embarrasing audit in March 2026, basically blaming CNDT (overly optimistic delivery schedule; lack of colaboration; performance issues... you name it)

Now the adults will take charge

1

2

36

9,505

JB retweeted

May 21

$CSU feasting on this carcus for the second time?!

From 2023:

csisoftware.com/constellatio…

May 21

Big acquisition for $CSU.TO! marketscreener.com/news/cond…

2

4

71

19,957

JB retweeted

May 19

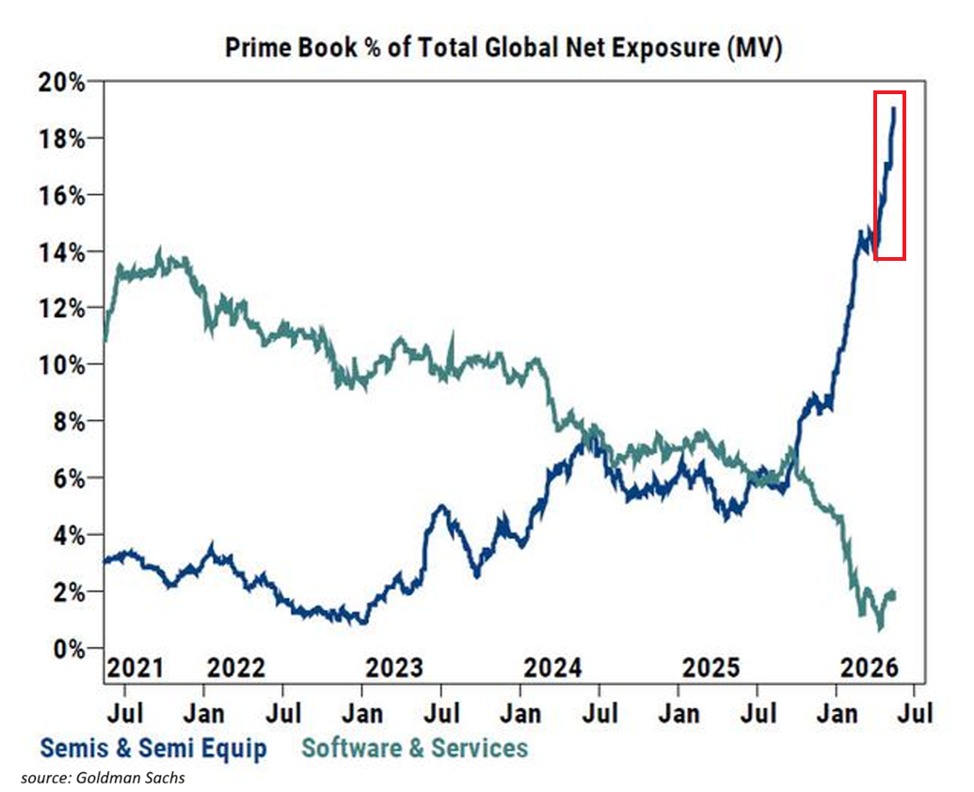

Software sold off on AI replacement fears. That fear turbocharged the semi rally. Next move funds rotate semi profits into oversold software names to outperform. Markets always overshoot.

Rinse and repeat

Hedge funds are all-in on semiconductor stocks:

Semiconductor and semiconductor equipment stocks now account for 19% of total global hedge fund market exposure, the highest on record.

This percentage has more than DOUBLED since the start of 2026.

By comparison, semiconductor stocks represented less than 2% of global hedge fund exposure during the 2022 bear market.

This comes as the Semiconductor index, $SOX, has rallied 405% over this period.

To put this into perspective, software and services stocks now account for ~2% of hedge fund portfolios.

This metric has declined -10 percentage points over the last 4 years.

Hedge funds are extremely bullish on chip stocks.

15

9

136

31,409

JB retweeted

May 17

When a university student realized AI won't displace all software leaders. Software is more than code. $CSU.to

9

20

171

45,588

JB retweeted

May 13

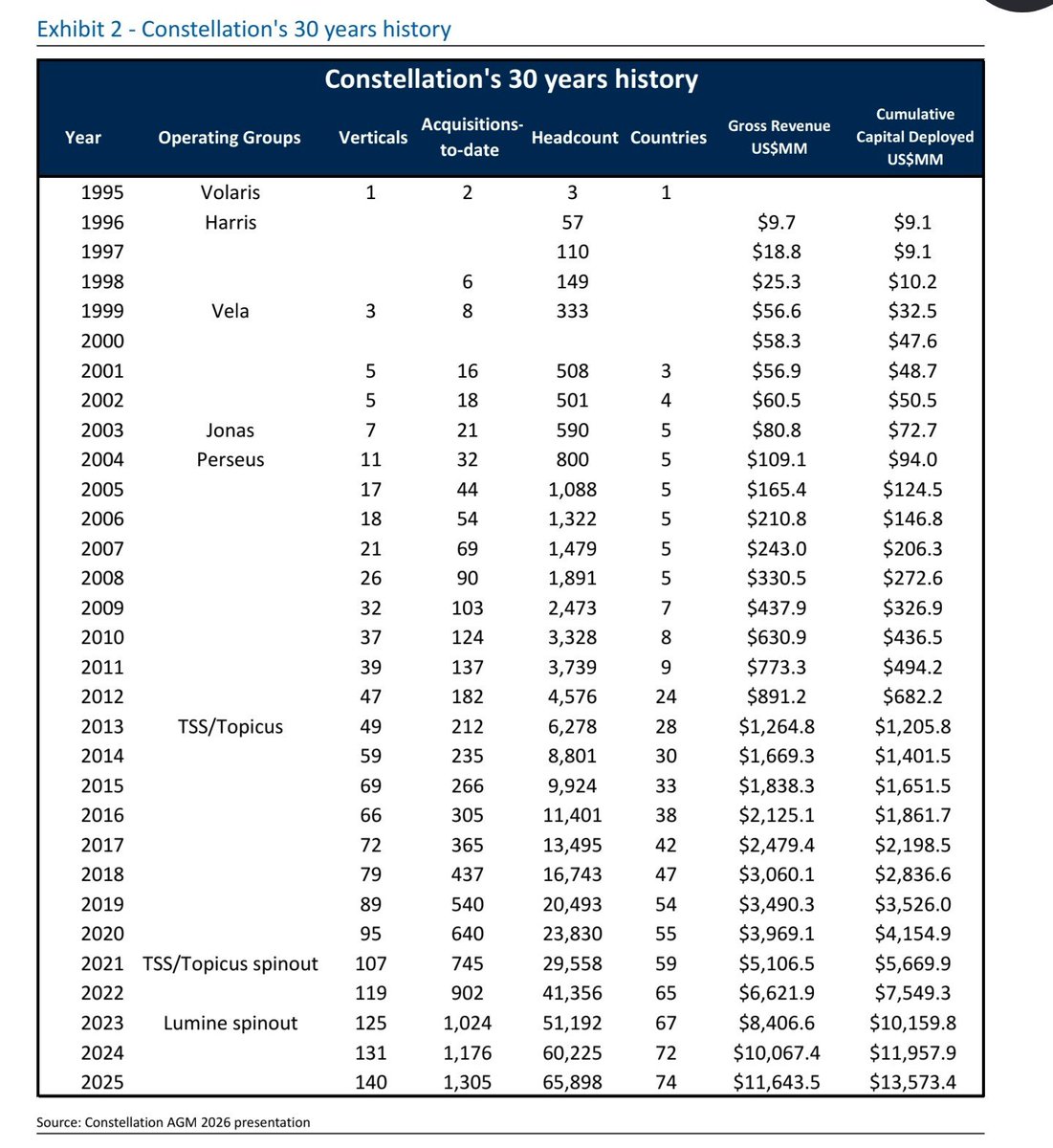

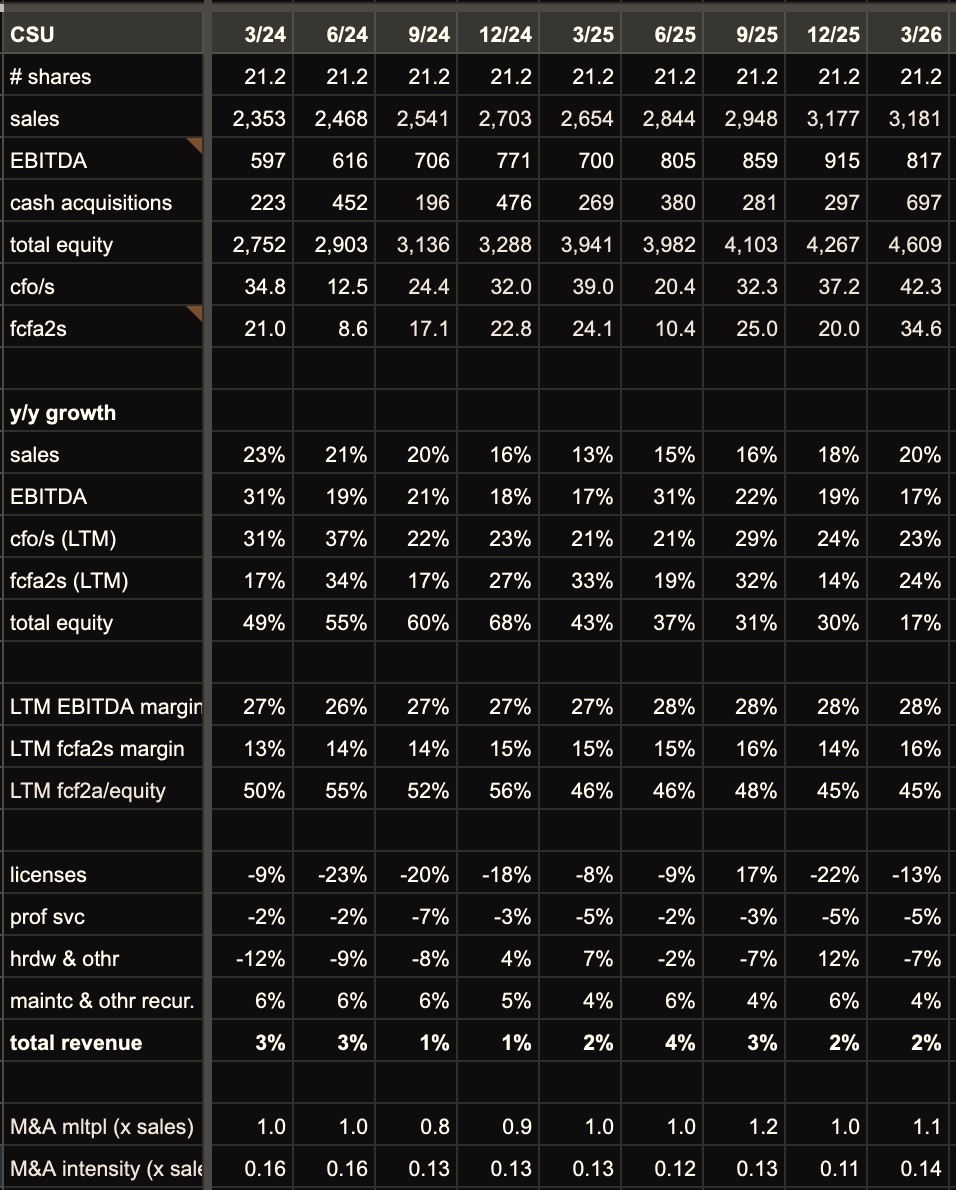

Constellation Software (CSU) Q1’26 deep dive 👇

$CSU $CSU.TO

IMPORTANT FRAMING (because CSU consolidates TOI LMN)

CSU consolidates 100% of both Topicus and Lumine (control via super voting). So CSU’s reported revenue / opex / cash / M&A includes TOI LMN fully, and economics are then split via NCI (and FCFA2S deducts NCI).

1) Growth: strong headline; “maintenance organic” is the clean signal

Revenue grew 20% YoY to $3,181m. Organic growth was 6% (or 2% FX-adjusted).

Cleanest read is maintenance & other recurring:

Maintenance 22% YoY and 9% organic (FX-adjusted 4%).

Licenses were -9% organic and hardware slightly negative organically, so don’t over-read those.

2) M&A: remember LMN TOI are inside CSU’s numbers

Total consideration for acquisitions in Q1 was $809m (cash at close $697m):

- Synchronoss (inside Lumine): total consideration $309m (contributed $22m revenue and ~$(2)m net loss in the partial quarter)

- “Additional acquisitions”: total consideration $500m = cash $388m holdbacks $91m contingent $21m

Cash flow bridge (to reconcile optics):

Cash paid at close was $697m, and then there was another ~$69m of post-acq settlement / holdback payments → “cash used in acquisitions” shows up as $766m.

CSU also acquired $77m of cash with the businesses.

Standalone CSU deployment (“ex TOI LMN” lens):

Topicus did €22.5m of total consideration in Q1 (~$25–26m), so standalone CSU consideration is roughly:

$809m – $309m – ~$26m ≈ ~$473m in Q1’26 (similar to Q4’25). TTM standalone consideration is ~ ~$1.5b → CSU is still chugging along on acquisitions.

Bonus: post-quarter pipeline

Subsequent to Mar 31, CSU completed / committed to $786m of acquisitions (cash $627m deferred $159m).

3) Operating leverage: roughly steady (Q1 staff is seasonally optically heavy)

Expenses grew 21% vs revenue 20% (expense ratio 75% → 76%).

Staff grew 19% YoY. CSU reminds Q1 staff % is seasonally higher due to payroll taxes tied to annual bonus payments in March.

Lumine had acquisition-related costs this quarter (not quantified at CSU level), so some staff-line noise is possible.

4) Below EBIT: lots of noise (don’t anchor on EPS without context)

- FX swung hard: $45m gain vs -$32m loss last year.

- IRGA liability revaluation swung from a $94m charge last year to a -$76m gain this year (non-cash).

Important nuance: the IRGA liability fell mainly because Topicus’ listed stakes (Asseco Sygnity) were lower, offset by Topicus’ trailing maintenance/recurring growth net profits.

- Asseco now shows up via equity-method income (~$10–11m this quarter, lagged).

- Finance costs were higher due to higher average debt outstanding.

5) Cash: CFO 9%;

my FCFAA math

My FCFAA variant: start from CFO, subtract interest/leases/capex, add acquired cash, deduct post-acq settlement cash.

In Q1’26:

CFO 897

less interest / leases / capex: 111

cash obtained from businesses: 77

– post-acq settlement payments: 69

FCFAA: ~795m in Q1 (up ~11% YoY)

On TTM basis (my calc):

OCF: 2,807m

less interest / leases / capex: 377m

FCF: 2,430m

cash obtained from businesses: 239m

– post-acq settlement payments: 339m

FCFAA: ~2,330m TTM

(Note: this includes 100% of Topicus Lumine, so be careful with valuation.)

6) Balance sheet / dry powder

Cash ~$3.01bn and total debt ~$3.99bn → net debt ~$0.98bn (ex leases).

Lease obligations are ~0.44bn → “incl leases” net debt ~1.44bn (~0.4x net debt / TTM EBITDA).

CSI Facility is $1.085bn and was undrawn at quarter-end (only ~$13m letters of credit).

Net-net: good organic (especially maintenance), steady M&A machine, and strong Q1 cash generation.

5

36

7,574

JB retweeted

May 13

If you owned this business privately and removed the stock price movements, you'd be very, very happy with it's continued results.

$CSU

6

5

144

14,165

JB retweeted

May 12

$CSU.to went on an acquisition tear:

Q1 2025: $133m

Q4 2025: $571m

Q1 2026: $809m

In 2025 they acquired $1.58b

Including Q1 subsequent commitments they have already surpassed all of 2025 deployment

...And this ignores PEMS deployment.

🔥

11

24

241

35,213

JB retweeted

Apr 17

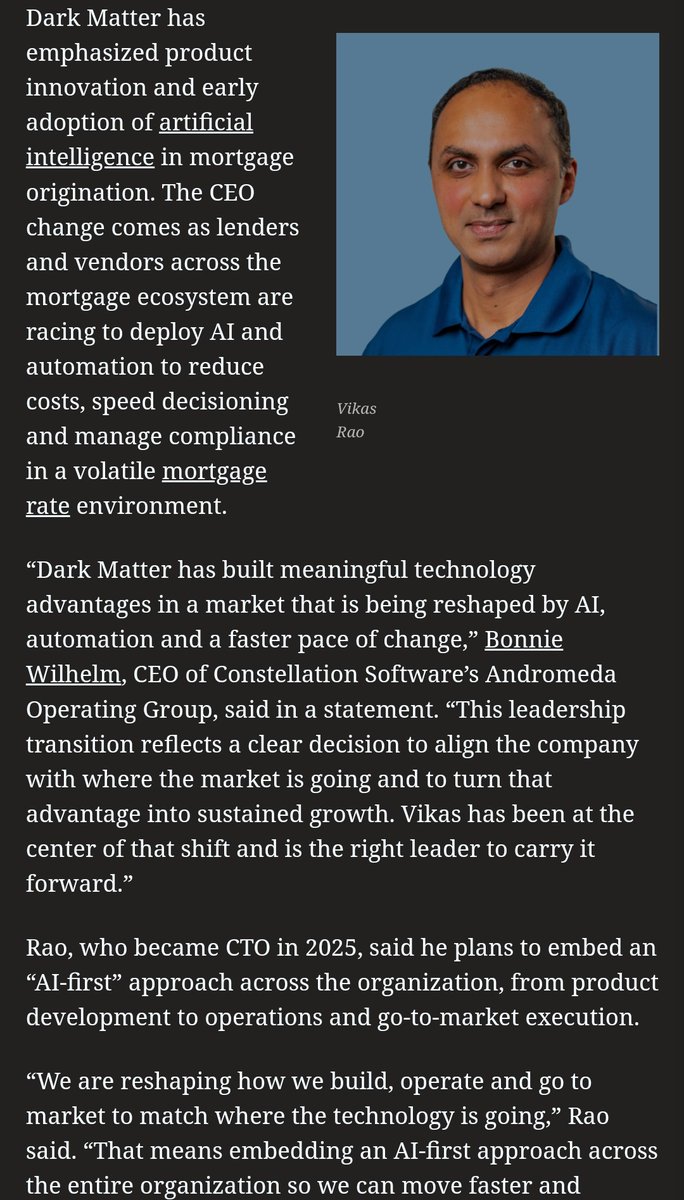

$CSU business unit Dark Matter Technologies, a mortgage software provider, is making organizational changes—cutting 5% of workforce & promoting its CTO to CEO to accelerate its AI strategy & growth. They are an early adopter of AI in mortgage origination.

1

7

54

21,599