Natural Resources analyst and Head of Research @ VSA Capital.

Joined November 2010

- Tweets 739

- Following 787

- Followers 383

- Likes 809

36 Photos and videos

Oliver O'Donnell, CFA retweeted

17 Oct 2024

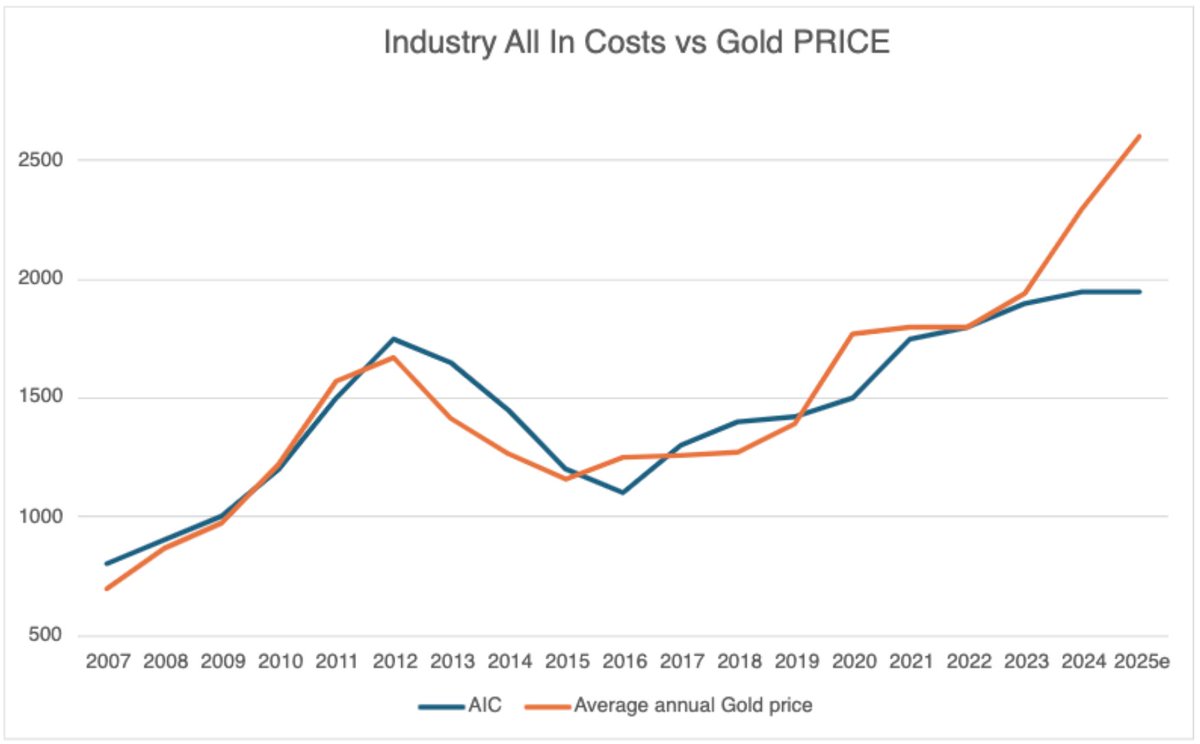

So here is the gold mining industry's AIC - (total costs i.e AISC growth capex, G&A, M&A, dividends etc.) vs the gold price. As you can see its been a horrible business, slipping in and out of marginally positive and negative free cash flow over the past 15 years. And suddenly...Boom! Massive positive margin expansion. I'm not sure anyone is really getting this outside the sector specialists. In theory the industry can now, for the first time in living memory, finance reserve replacement and a much higher return of capital to shareholders from FCF.

31

110

412

80,517

Oliver O'Donnell, CFA retweeted

10 Jul 2024

If you missed it first time, click original post for full video of @DoubleOD2 talking to @AdrianOBrien of @MidnightSunMine

24 Jun 2024

.@VSACapital's @DoubleOD2 talks to @AdrianOBrien of @MidnightSunMine a Canadian #exploration company, focused on its #flagship Solwezi Project in the heart of the #Zambia-Congo #Copper Belt, the 2nd largest copper producing region in the #world. youtu.be/7pPt5eWX8e4

2

2

433

Oliver O'Donnell, CFA retweeted

4 Jul 2024

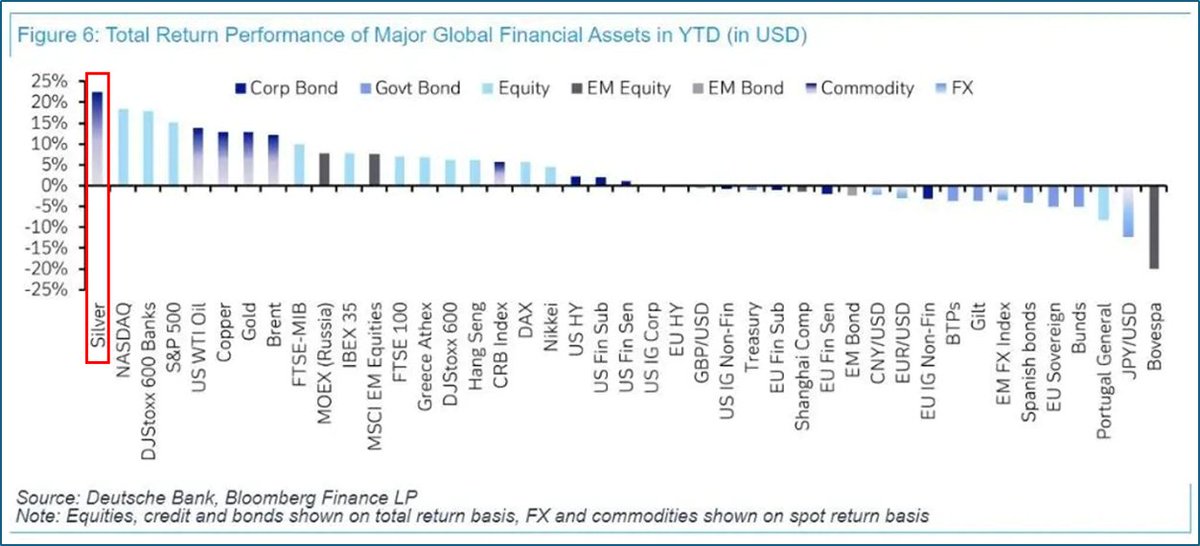

#Silver: Best performing asset in first half 2024

39

299

987

180,758

5 Jun 2024

Always great to hear from @alex_langer and Greg Liller! Exciting timing with rising metal prices

5 Jun 2024

.@VSACapital's @DoubleOD2 talks to Greg Liller & @alex_langer about @SierraMadreSM La Guitarra #mine in #Mexico @FMSilverCorp #fundraise #silver #gold #mining #investing #drilling #resources #fasttrack #restart #production #exciting #news youtu.be/w-PSJksovgY

7

211

Oliver O'Donnell, CFA retweeted

12 Jun 2023

Click here to see the full interview with @DoubleOD2 and @tdlamb #CEO of @MyriadUranium #uranium #Niger bit.ly/43VDkpc

4

11

969

21 Jul 2022

Looks like @TVLithium in the right place according to @Tesla

Lithium Refining Is a ‘License to Print Money,’ Musk Says bloomberg.com/news/articles/…

21 Jul 2022

Setting you up nicely for a cooler day, @DoubleOD2 and @PaulRenken covering news from

@AlkemyCapital @TVLithium

@CaledoniaMining

@shanta_gold

@GreatlandGold

bit.ly/3RRSNBm

#morningminer #Mining #investing

2

Oliver O'Donnell, CFA retweeted

17 May 2022

The @KusasaProject is focused on breaking the cycle of poverty, addressing the issue at its roots by the establishment of an independent primary school serving disadvantaged children.

Watch a video of VSA's recent visit to Kusasa Centre here:

bit.ly/3PtBoxq

1

1

12 Apr 2022

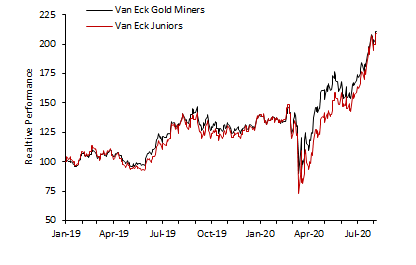

This is an exciting chart showing a significant opportunity in equities, good for my PM coverage universe of small cap gold and silver @PrimeMiningCorp @CaracalGoldplc @GSilver_co @SierraMadreSM @corp_apollo @tectonic_gold

1

1

Oliver O'Donnell, CFA retweeted

3 Nov 2021

We would like to welcome @SierraMadreSM to 121 Mining Investment London on 17-18 November for 121 investor meetings.

If you would also like to join us or to apply for a free investor pass – click here: hubs.la/H0-wJNb0

#121Online #Mining #Investment

2

2

26 Aug 2021

Bump for @aim_irr today, looks like now the BCN discount to the offer price has closed the rotation is beginning. Sensed some frustration after IRR hadn’t initially moved but this may change momentum

3

16 Jul 2021

A great pick from @PaulRenken who initiated on @MillennialLi in January 2017, now being taken out by @GanfengOfficial as their campaign for lithium domination continues

1

1

1

Oliver O'Donnell, CFA retweeted

17 May 2021

@VSACapital is excited to be working with Tungsten West on its IPO ahead of production restart. @AmonkMonkey spoke to @METhompson72 at the mine site.

VSA Capital welcomes qualifying HNW investors to participate in the IPO.

Info : ipo@vsacapital.com or youtu.be/lhkmIRfn11g

2

Oliver O'Donnell, CFA retweeted

16 May 2021

#tungsten #tin #tungstenwest

Tungsten West announces our intention to list on AIM as covered by The Sunday Times today.

8

10

82

Oliver O'Donnell, CFA retweeted

27 Apr 2021

Following the major announcement of the new business plan @AmonkMonkey of @VSACapital spoke to the Chairman of @PensanaRE, Paul Atherley, to discuss the outlook for the company and #RareEarths

bit.ly/3dVtnkh

#EnergyTransition

#mining

4

7

Oliver O'Donnell, CFA retweeted

25 Mar 2021

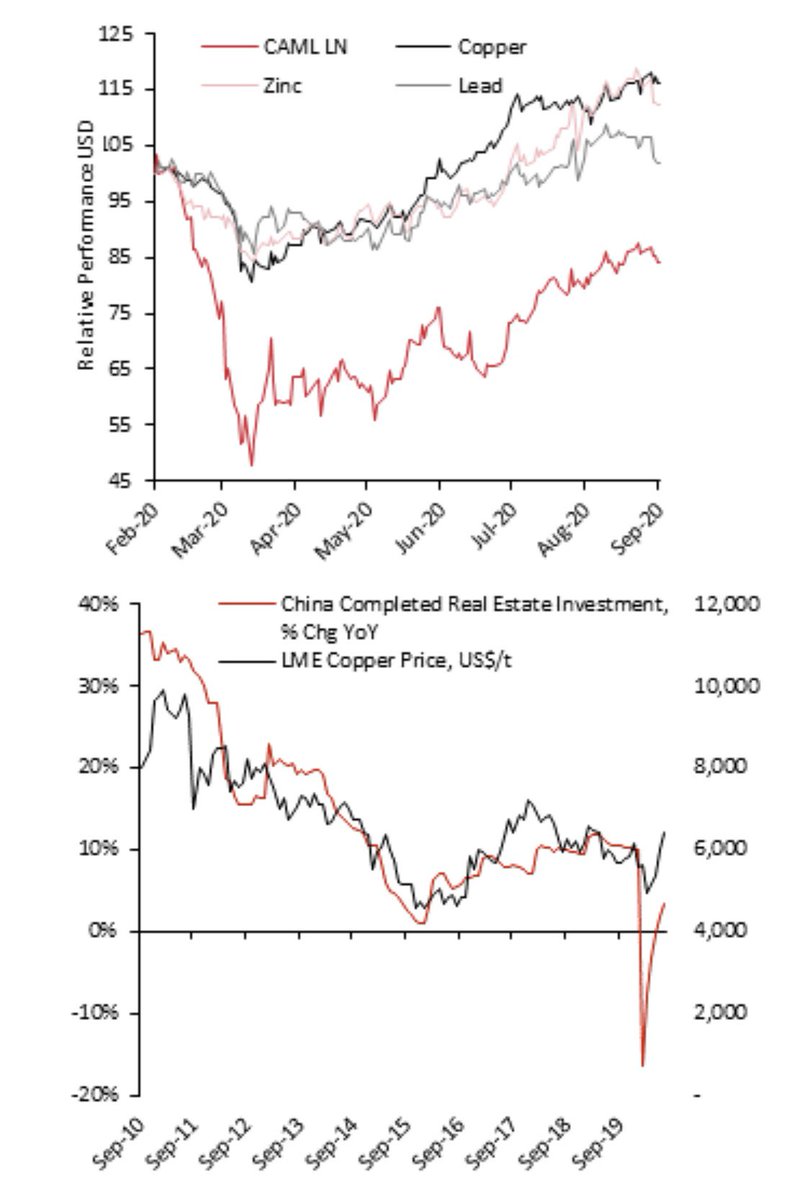

The Morning Miner and today with special guest from @CamlMetals CEO Nigel Robinson discussing his views on metal markets #copper, a different type of mining cycle, battery metals and ESG bit.ly/31ut4WN @AmonkMonkey @PaulRenken

3

2

23 Mar 2021

Was a great event to be a part of!

23 Mar 2021

Earlier this week @VSACapital held a webinar for investors to discuss @AlloyFerro and @VisionBlueRes, Sir Mick Davis summarized the opportunity perfectly but do watch the full video on our Youtube Channel bit.ly/2QwhVT0 #mining #vanadium #vfbs #energytransition

1

Oliver O'Donnell, CFA retweeted

22 Mar 2021

Fantastic to see the start of trading for @samarkandglobal on the @AquisStockEx. An exciting first for all involved, congratulations! #technology #disruption #investing

2

1

19 Mar 2021

Thanks @AmonkMonkey !

19 Mar 2021

well done Ollie O'Donnell @VSACapital being ranked 2nd in Resources

2

Oliver O'Donnell, CFA retweeted

19 Mar 2021

Following the landmark deal with @VisionBlueRes, @AmonkMonkey spoke with Nick Bridgen, CEO of @AlloyFerro on the deal, the Balasausqandiq project and the vanadium price outlook bit.ly/3eRXJFf #mining #vanadium #vfbs #energytransition

1

7

12

19 Mar 2021

Strong start for @PrimeMiningCorp, clear why expanded acreage and first drill hole at Guadalupe East shows resources will grow along strike and at depth

19 Mar 2021

First assays from @PrimeMiningCorp and surface results show scale potential, raise for @TridentPlc, @AlloyFerro moves higher again and Caerus IPO bit.ly/2P3ltvc @PaulRenken @AmonkMonkey #mining #investing #mexico #gold

1