63 Photos and videos

Francois retweeted

Jun 2

947

1,973

8,735

567,912

Francois retweeted

May 14

I think we are closer now to history on $GME than ever before

And I was there in 2024

I remember what it felt like

And nothing has even sniffed what I'm currently witnessing, not even April 2024

37

31

610

20,731

Francois retweeted

May 12

BAD NEWS EARLY, GOOD NEWS ON TIME.

There are two versions of a proxy statement.

The preliminary proxy (PRE 14A) is the draft. It files with the SEC for review. The SEC has roughly ten days to review it. If they don’t send a comment letter, the company is clear to file the definitive version.

The definitive proxy (DEF 14A) is what shareholders actually vote on. It does not go through a second review period. It’s effective immediately.

GameStop filed its PRE 14A at market close on May 11th.

The DEF 14A can file as early as May 21st.

The annual meeting is June 8th.

The definitive proxy files between May 21st and roughly May 26th.

That’s the window.

—

Every proxy opens with a letter to stockholders. It’s not a proposal or a voting item.

I’ve attached ours below.

150 words.

The comp gets one paragraph.

The 2.5 billion share authorization gets one sentence.

Acquiring companies is never mentioned.

The only forward-looking language is seven words: “when the right opportunity arises.”

That’s a placeholder. This letter was never meant to be finished.

—

Now think about what shareholders are walking into on June 8th with this letter as their only context.

The Comp Package

171.5 million shares in performance options.

Milestones up to $100 billion market cap.

The letter mentions the $20 billion floor.

It doesn’t mention the $100 billion ceiling. It doesn’t explain why those targets exist for $GME.

The Share Authorization

2.5 billion total authorized shares.

“When the right opportunity arises” is the entire explanation.

The Backdrop

A $55.5 billion bid for eBay just got publicly rejected as “neither credible nor attractive.”

Without additional context, every proposal fails.

Cohen built this meeting agenda.

He knows it’s insufficient.

You know it’s insufficient.

Which means the definitive letter is different.

—

The proposals won’t change. The SEC reviewed them. They have to stay consistent.

But the shareholder letter is not a proposal. It’s disclosure. Expanding disclosure between preliminary and definitive isn’t just permitted. It’s encouraged.

The preliminary letter is 150 words. The definitive letter could be 1,500. The proposals stay identical. The context changes everything.

—

Here is my prediction. Bookmark it.

The definitive proxy shareholder letter is where Cohen reveals the holding company.

‘We pursued the largest marketplace acquisition. We were rejected. Our stock is undervalued when the market sees a video game retailer.’

The solution isn’t to abandon the strategy.

The solution is to change what our stock represents.

A parent entity — with GameStop as its core subsidiary — building a diversified conglomerate.

The 2.5 billion shares are the authorized pool for that structure. The comp milestones to $100 billion aren’t for a retailer. They’re for the parent.

Delaware Section 251(g) allows a corporation to reorganize into a holding company without a shareholder vote. Google did this in 2015 when it became Alphabet. Each share converted 1:1. No dilution. No taxable event. The board executed it unilaterally.

The reorganization is 1:1 — no new shares needed.

But the moment the holdco exists, Cohen needs shares for everything that comes after.

The share authorization IS the holdco vote.

The comp approval IS the holdco vote.

Every proposal on June 8th is a piece of the same structure.

The letter is what connects them.

—

Cohen can’t walk into June 8th with a 150-word letter and ask for 2.5 billion shares on trust alone.

Not after $EBAY. Not with $100 billion milestones.

He built a meeting agenda where every item is incoherent without the reveal.

All three point at the same door. The shareholder letter opens it.

The DEF 14A files between May 21st and May 26th.

The letter expands.

The vision is disclosed.

June 8th.

BAD NEWS EARLY

GOOD NEWS ON TIME

32

101

584

135,360

Francois retweeted

Feb 26

Some Buffett quotes for the intellectually curious.

Quote 1, from when Buffett opened the 1995 shareholder meeting by asking shareholders to vote on authorizing the board to issue up to 1 million shares of preferred stock, he delivered an extended explanation:

“It’s an authorization. It’s not a command to issue shares. It’s not a directive. It simply gives the directors of the company the ability, in a situation where it makes sense for the company to issue preferred shares, to do so. Now, when we acquire businesses, sometimes the seller of the business wants cash, sometimes they would like common stock, and it’s certainly possible, as one potential seller did last year, that they want a convertible preferred stock. Now, from our standpoint, as long as the value of the consideration that we give equates, we really don’t care — aside from a question of tax basis we might obtain — but in other economic respects, we don’t care what form of consideration we use, because we will equate the value of cash, versus a straight preferred, versus a convertible preferred, versus common stock, whatever it may be. So, if the worry is that we will do something dumb in issuing the preferred stock, that’s a perfectly valid worry. But you should worry just as much that we’ll do something dumb in terms of using cash or common stock. I mean, if we’re going to do something unintelligent, we can do it with a variety of instruments.”

Quote 2, from when a shareholder directly asked whether the preferred stock authorization would dilute their holdings, Buffett responded:

“Only if we receive less in value than we give. That’s the key to it. I mean, if we issue $200 million worth of preferred and we receive a business that’s only worth $150 million, there’s no question you’re worse off than before. So are we, incidentally. But we’re all worse off. And that’s true if we give cash that’s worth more for a business than [the business is worth].”

Quote 3, from Buffett’s 2016 annual letter to Berkshire Hathaway shareholders:

“I followed the GEICO purchase by foolishly using Berkshire stock — a boatload of stock — to buy General Reinsurance in late 1998. After some early problems, General Re has become a fine insurance operation that we prize. It was, nevertheless, a terrible mistake on my part to issue 272,200 shares of Berkshire in buying General Re, an act that increased our outstanding shares by a whopping 21.8%. My error caused Berkshire shareholders to give far more than they received (a practice that — despite the Biblical endorsement — is far from blessed when you are buying businesses).

Early in 2000, I atoned for that folly by buying 76% (since grown to 90%) of MidAmerican Energy, a brilliantly-managed utility business… The MidAmerican cash purchase — I was learning — firmly launched us on our present course of (1) continuing to build our insurance operation; (2) energetically acquiring large and diversified non-insurance businesses and (3) largely making our deals from internally-generated cash. (Today, I would rather prep for a colonoscopy than issue Berkshire shares.)”

4

18

153

13,185

Francois retweeted

23 Jul 2022

reports of your death are greatly exaggerated

313

994

6,573

Francois retweeted

Mar 3

There are so many cool companies to invest in right now. Met a few ambitious ones today. Every sector, application, platform, utility - being reinvented. This is going to be a fun season ahead to invest...

71

97

1,098

41,685

Francois retweeted

Feb 27

WE LIVE! WHO'S WINNING THAT DIAMOND PACK FROM @GAMESTOP!?

x.com/i/broadcasts/1dGYljllE…

25

113

413

35,181

Francois retweeted

Feb 27

Tonight's @PowerPacks LIVE STREAM is sponsored by @GameStop! 🔥

We're giving away a $1000 Diamond Pack 💎 to celebrate Pokémon's 30th Anniversary, along with many other prizes! 🎁

Tune in at 2pm PT / 5pm ET / 10pm UK - Please share with your friends! Links in comments! 🔥

15

56

192

9,726

Francois retweeted

Feb 18

The Hollow Men

American capitalism is rotting from the head down. We have replaced the "Owner-Operator"—the risk-taker-with a new, parasitic class of corporate bureaucrat: The Risk-Free Insider.

By "Insider," I am not referring to a specific title. I am referring to the entire administrative state that has captured the modern corporation. This includes the Directors who exist solely to collect fees, the Executives who exist solely to collect bonuses, and the Managers who exist solely to hire consultants.

These are the hollow men of the boardroom. They are masters of PowerPoint. They wear the right suits. They say the right buzzwords about "governance" and "ESG." But they are mercenaries fighting a war with someone else’s ammunition.

In a functioning economy, authority is tied to liability. If you make a bad decision, you lose your own money. That fear of loss is the only thing that keeps a business honest. It forces you to cut waste, obsess over the customer, and stay late to fix what is broken.

Today, we have severed that link.

We have rigged the game so that heads, the Insider wins; tails, the shareholder loses.

If the stock goes up, the Insider collects a massive performance bonus. If the stock crashes due to their own incompetence, they are fired with a "Golden Parachute" worth tens of millions. They are gambling with the house’s money, and they never leave the table poorer than they arrived.

This looting starts in the boardroom.

We have normalized a "Country Club" culture where directors are selected based on social profiling rather than their ability to build a business. The modern board member is often a professional tourist—paid an average of $350,000 a year.

Let’s be brutally honest about what that number represents. The average director is paid nearly five times the GDP per capita of the United States. They earn more for attending four quarterly lunches than the vast majority of Americans earn in five years of hard labor.

And for what?

Most of these directors are "over-boarded," sitting on three or four boards simultaneously. They treat directorships as a gig economy for the elite. They fly in, rubber-stamp a compensation package they didn't read, and fly out. They collect checks from companies they do not understand, do not use, and certainly do not love.

They are not there to ask hard questions. They are there to be collegial. They are there to protect the other Insiders.

And what happens when these boards hire executives who also have no personal capital at risk?

We get the Delegation Economy.

When a Risk-Free Insider faces a crisis—bloated expenses, a broken supply chain, or a stale product—they do not roll up their sleeves. They hire a consultant. They pay a strategy firm millions of shareholder dollars to produce a 100-page deck telling them what they already know.

This is not management. It is intellectual money laundering.

They use shareholder capital to buy an insurance policy for their own careers. If the plan fails, they can blame the consultants. They delegate the work because they are terrified of the responsibility. They would rather preside over a slow, comfortable decline than risk a bold mistake.

While American Insiders are busy optimizing their severance packages, our global competitors are optimizing their products. They are not slowed down by bureaucracy. They are not waiting for a slide deck. They are outworking us.

If we continue to fill our C-suites with administrators instead of operators, we will lose our edge. We will see iconic American franchises hollowed out by fees, managed for the benefit of the Insiders, while the true owners—the shareholders—are left holding the bag.

The time for polite governance is over.

If we want to save the American economy from mediocrity, we must demand a return to the "Owner’s Mentality." We need leaders who treat shareholder capital with the same reverence they treat their own savings. The era of the Risk-Free Insider must end.

2,720

5,862

21,414

2,934,313

I wouldn't go so far as to say that I am asserting a claim because I am just reading from the Plan, but I understand what you mean.

when did we arrive at a cryptic agenda?

answering your last line: there is a lot of value in acquiring a shell company out of Chapter 11. if you want to IPO a private company then definitely speed-to-market; from not having to pay millions of dollars in financial audits and preparation to apply to the regulators for approval to go public. it is a fast-track way to be listed as a public company.

then there are massive tax advantages from the NOL's against future profits; we know this was something very important because it was disclosed in the 2023 10-K. just think about how much money $BBBYQ lost between September 2022 (when they couldn't get inventory for the holidays) to September 2023. on top of how terrible the old Board ran the company, they claimed a 600 million dollar plus loss on inefficient markets resulting in them being unable to effectively do their ATM raise (and exposing synthetic shares abuse by Cede in court records!).

but in my opinion, most important of all, the reason that RC saw value in the shell of the company was leverage. as long as the company wasn't going to die off in a Chapter 7 then a lot of bad behaviour could not be swept under the rug. keeping the asset alive was his leverage to hold entities accountable that got carried away with how far their hands reached into the cookie jar. that is the $BBBY story and it culminated with the third-party release.

that's why this Chapter 11 isn't like other ones. the primary goal isn't to rebrand and save a company or to shed some debt and have at it again as the old enterprise. the OldCo will be used for something because it has great tax benefits, sure. but saving the legacy business to relaunch was never the focus.

also just so you know,

"If it's RC doing this with the intention of reverse merging Teddy, I outright disagree with the value play compared to other opportunities he has with non-bankrupt companies."

you would not acquire a "non-bankrupt company" to perform a reverse merger. the public entity must be a "shell" in the sense of having no operations. why would you pay to acquire a public company only to have to gut it out to meet the rules for a reverse merger? don't confuse a reverse merger with being an acquired company. if the intent is to perform a reverse merger, the public entity *has to be* a shell.

24

52

359

11,294

Francois retweeted

23 Jan 2025

I wonder what he’s waiting for

627

264

5,519

517,731

welcome to the last day of the 12 Posts of $BBBYQ -mas, where the goal has been to review and simplify concepts from my research into $BBBY (old). I hope you’ve found the series as a good refresher of key concepts, new information to tie together important elements valuable and generally enjoyed the endeavour. though initially I had a really difficult time trying to condense what I wanted to share into “only” 12 posts, I was not expecting how much time and effort it would take to do it all! in the end, I hope you enjoyed it as much as I did. without further ado, lets get into the last post of the series..

no. 1!

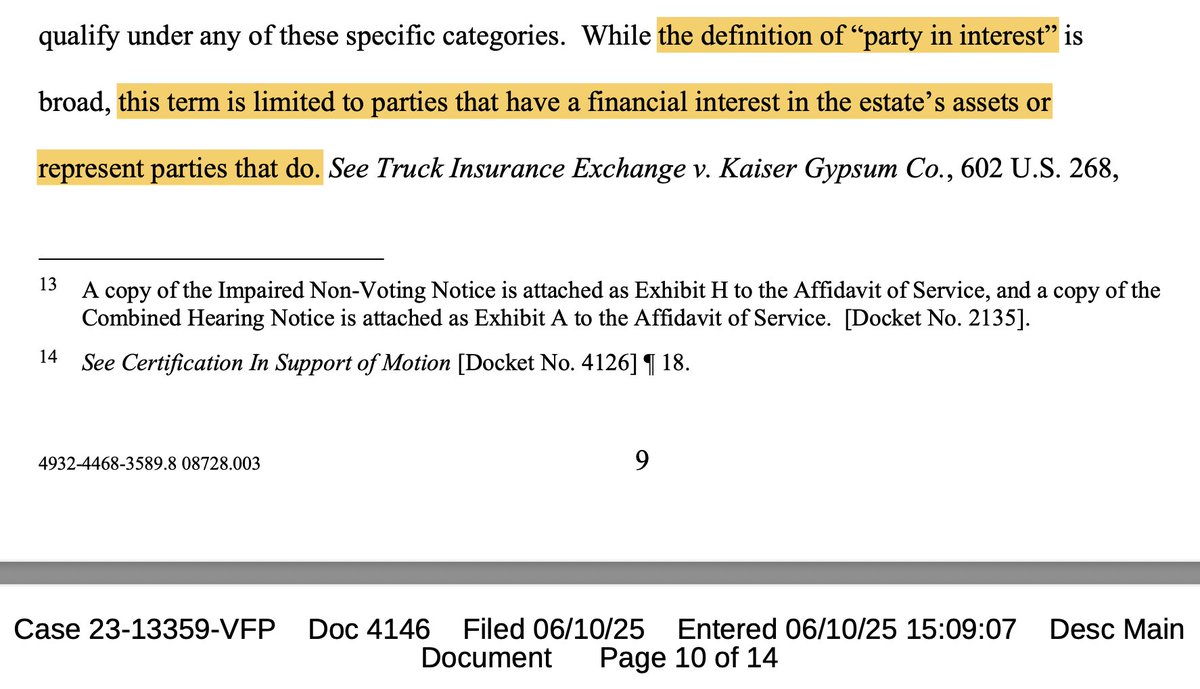

we’ve reviewed the Holder of Interests extensively, both as being a shareholder and their involvement in the third-party release. we also looked back on time-related limitations for an acquirer, their proxies and affiliates as it relates to the NOL.

today I will present my case for why I believe that Ryan Cohen is the Holder of Interests.

we know that Interests are defined in the Plan as any equity security and we also know that at Confirmation, only one type of equity security existed; the common stock. therefore, I believe that a Holder of Interests can only be a Class 9 shareholder. in my opinion we see more evidence of this during the November 2022 bond exchange—the private individual investor and later, the several institutional ones retired their bonds to the Company in exchange for shares.

separately, we also know that RC has been listed as a co-debtor, creditor and party in interest in the Bed Bath Chapter 11 and no, this is not because of the litigation in the Section 16(b) case. that is a ridiculous claim that we have addressed many times.

adding another layer, any time that there has been a hearing involving the Class 9 common stock, RC has been named in the noticing list as a bypassed recipient—only when it involved common stock, until recently when it also now involves the omnibus objection of Claims. I believe there is no alternative explanation for his inclusion in the noticing list.

here is an admission by the plan man of what a party-in-interest means in this particular case from earlier this year:

yes I planned the 12 Posts series in a particular order and yes, it should all be clicking together and it all centres around someone being the Holder of Interests.

here is a clue from the Plan that has no alternative explanation:

if Interests can only refer to Class 9 equity, how can there be a Releasing Party, who is the Holder of Interests that is deemed to accept the Plan, when the treatment of Class 9 as written in the Plan deemed them to automatically reject the Plan?

it is because the Holder of Interests, a Class 9 shareholder, cannot vote against the third-party release that they are involved in because this would make the Plan unconfirmable and therefore, could not bind the participating parties to the third-party release itself.

I can’t overstate how important this is—how can the Plan state that there was a Holder of Interests deemed to accept the Plan? I believe that the only explanation is that RC is the Holder of Interests as a Class 9 shareholder. ..and guess what? you cannot give preferential treatment within a Class.

this would also explain the intriguing language from the third-party release that we discussed in a previous post: “..to finally resolve certain Claims among or against certain parties in interest in the Chapter 11 Cases,..”

we talked about the passage of time in that statement. who would meet that criteria? well, an activist shareholder from 2022 who held the Board accountable certainly would.

remember the Class Action lawsuit against RC taken over by Bratya and their attorney entering the Bed Bath Chapter 11 wanting not only any information relating to RC, but expanding their scope to any and all transactions involving any party in the entire Chapter 11? had they suspected he may be using a proxy or affiliate? what other explanation could there be?

I believe that there was a plan a, b and c. plan a: shareholder activism to revitalize the Company from the top-down, but the Board was not willing to move at the pace and in the direction that Ryan sought. plan b may have been an attempted bond conversion, which we know failed due to lacking participation from legacy bondholders.. which is a huge signal in itself since the bonds were already trading at a heavy discount at the time and converting them would have allowed the Company to improve its balance sheet and credit-worthiness for a turnaround while increasing the semi-annual payments to the holders and yet,.. they chose not to participate.

the biggest indication that the bond exchange was an effort of the affiliates was that it was written by Lazard. the affiliates themselves in my opinion knew that the bondholders were creating friction, which I believe led them to take their own bonds and privately exchange them for shares, as was disclosed by the Company on December 6, 2022.

..and lastly, plan c was to facilitate a takeover through the Chapter 11 when it became apparent the other two options were not going to be successful.

to further support the idea about the Holder of Interests:

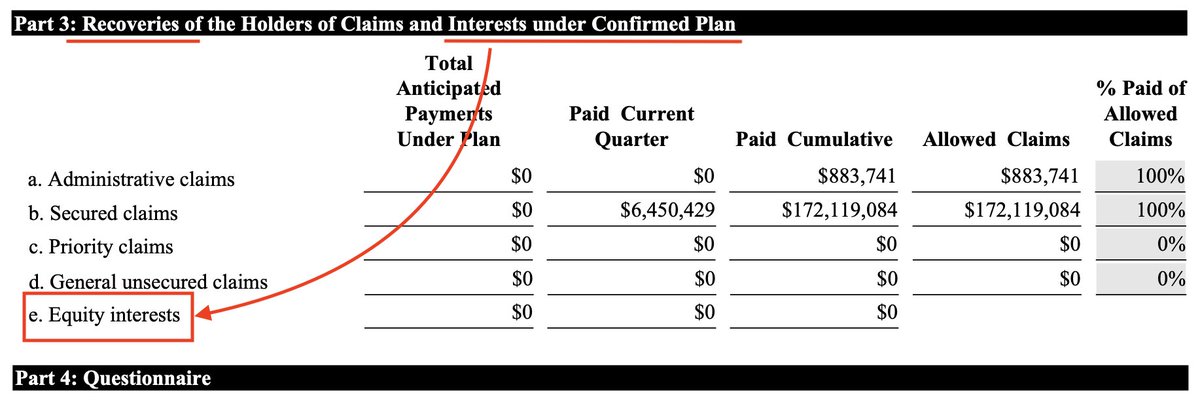

why are Interests and Equity interests listed in the Recovery section of the PCR? why are they there at all if "shares were cancelled"?

have you ever wondered why RC was listed bypassed recipient whenever Class 9 was discussed in Court? why is he mentioned at all and on top of that, not all of the time? I believe this again supports the theory that he is the Holder of Interests and can only be so as a Class 9 shareholder.

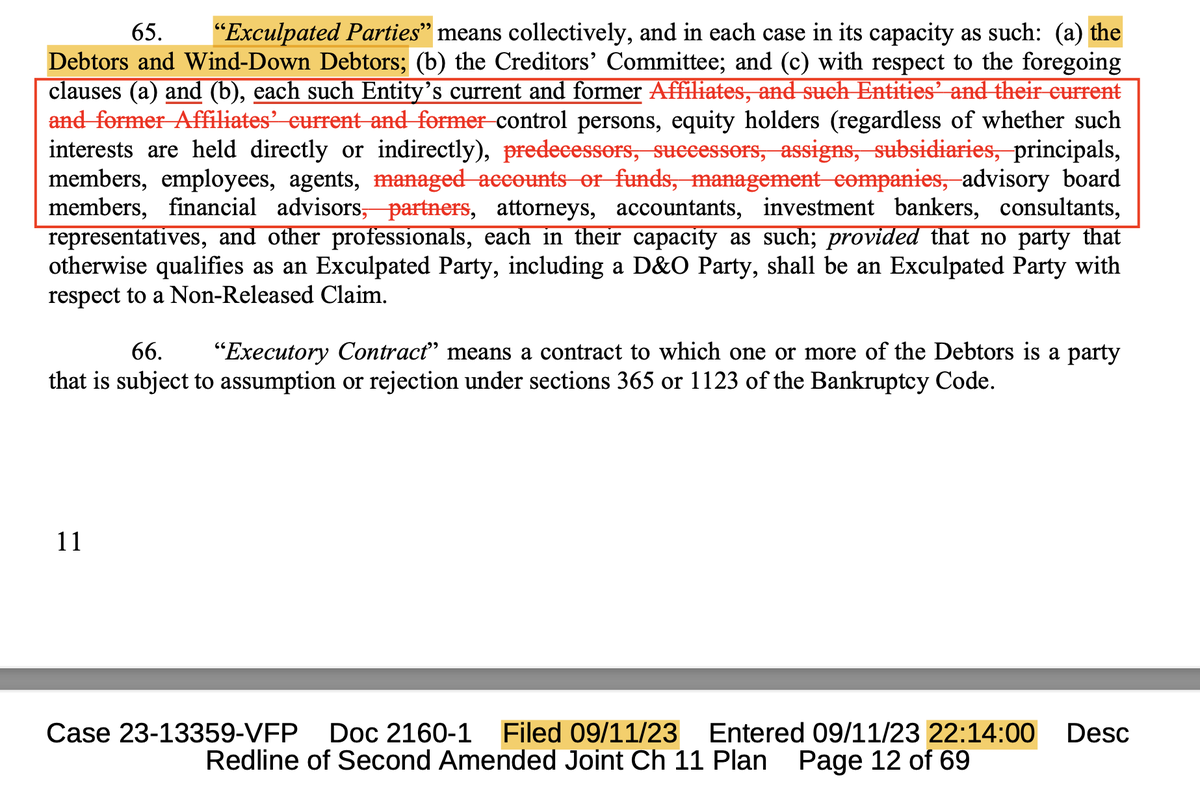

earlier I mentioned the Class Action and the request brought forward by Bratya. to appease them (and not disclose all transactional matters) the Plan was amended to state that RC is not a Released Party. what is funny is now that we understand the third-party release we know that if RC is the Holder of Interests, he is participating in the third-party release as a Relasing party.

however, as defined in the Plan by not being a Released Party he would no longer qualify for the Exculpation provisions in the Plan and wouldn’t you know it, look what was amended right after satisfying Bratya with listing RC as a Released Party, the Exculpation section of the Plan is amended:

isn’t that something? what other reason would there be for this if not to make adjustments because of the newly-changed legal status of RC? it is the only logical explanation.

not only that, but in the same revision we see legal language amended that as of the day before the Confirmation Hearing, everything may not be completed by the Effective Date:

“..through and until the date upon which all remaining property of the Debtors' Estates vested in the Wind-Down Debtors has been liquidated and distributed in accordance with the terms of the Plan,..”

what are the odds?

unless,.. RC is the Holder of Interests, who agreed to the third-party release in exchange for "substantial consideration" with multiple parties, which included the contributions to reach agreement for the Asset Sale Transaction.

to conclude: I believe that RC held the Board accountable for tremendous value-destruction to shareholders. I believe that he is the Holder of Interests, negotiated settlements through the third-party release and acquired the shell of the Company he set out to change in 2022 through the Asset Sale Transaction. when this NewCo emerges, I believe that it will distribute non-voting securities to comply with the new value exception of the absolute priority rule and that this is a viable mechanism of recovery for Class 9 shareholders.

the end!

..and that wraps up the 12 Posts series. I hope that you found value in reading it and enjoyed it as much as I did writing it. I have no idea when anything will happen and what timeline the recovery is following, but while everyone waits I hope you benefitted from a review of the critical points from the Plan that allow for meaningful recovery and a roadmap for how things may unfold.

I would like to wish everyone a wonderful holiday season filled with good health, love and happiness.

À bientôt!

welcome to the 12 Posts of $BBBYQ -mas. my goal is to try to review and simplify concepts from my research into $BBBY (old).

no. 2!

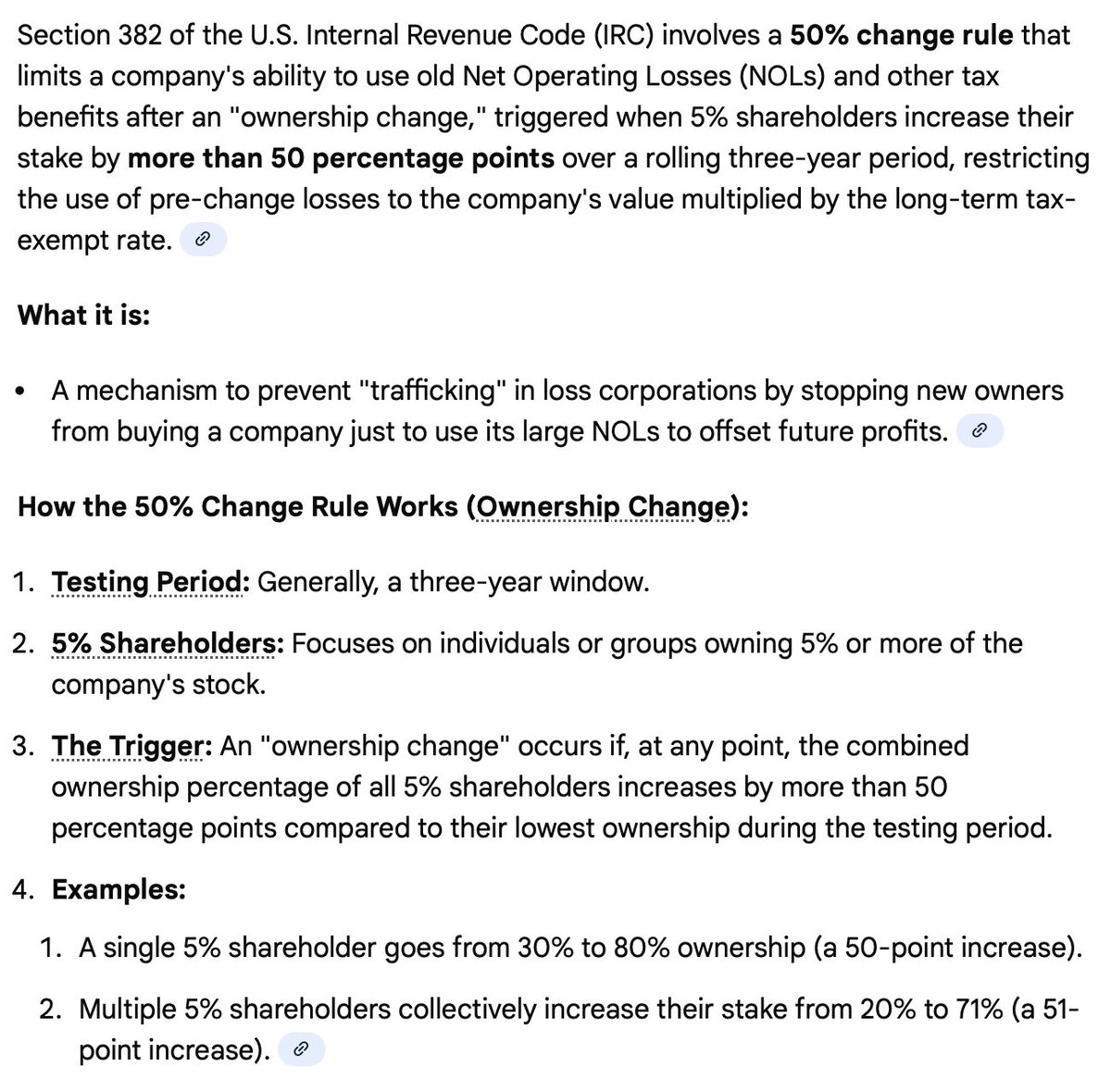

yesterday we introduced the concept of the NOL and why the Company considered it an important asset, going as far as to confirm that there would be a change in control resulting from the Chapter 11. if you consider yesterday’s post as a look at the NOL as it related to a Company, today’s will go over limitations of the NOL as it relates to investors. a reporting investor who meets the criteria can trigger an ownership change of a Company:

remember back to when the Company filed for Chapter 11 and the NOL Order was immediately filed at the beginning? yes, this is one of the reasons.

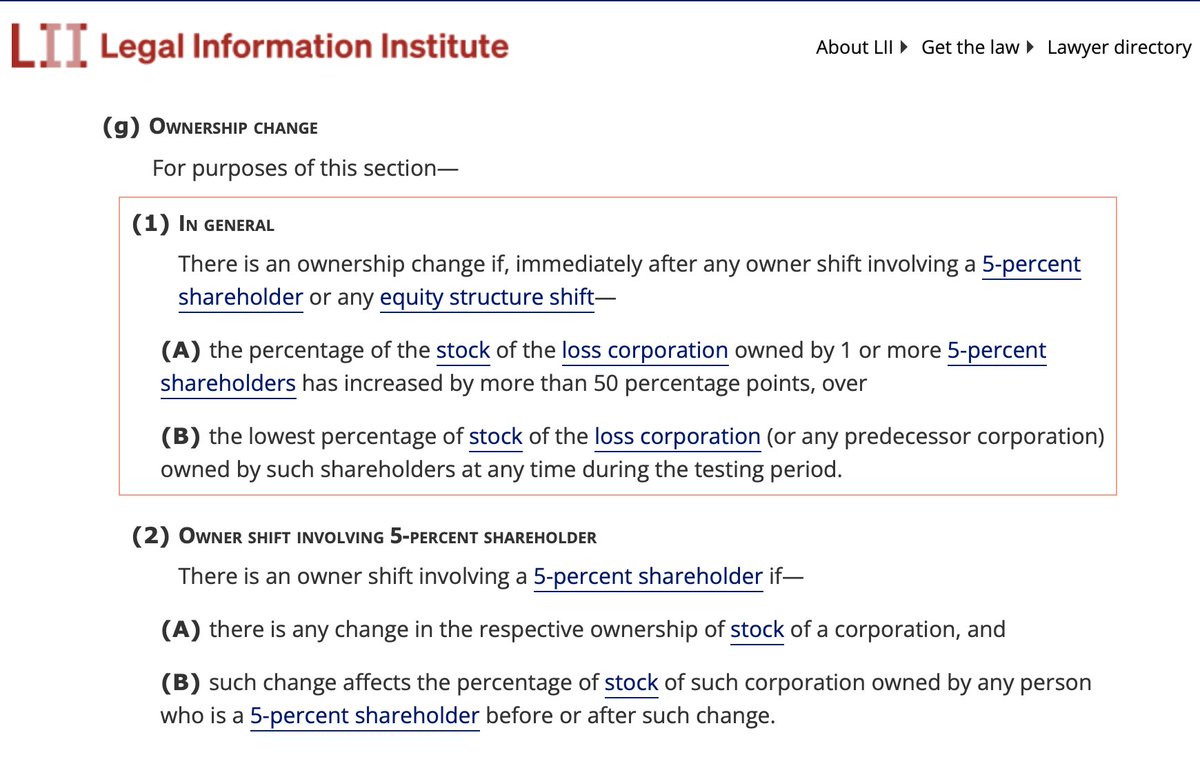

I briefly touched on this in my last video post, “Part 4/3”. there is a second limitation to protect “tax harvesting” inside of Section 382 and it involves a 50% change rule that is triggered when any 5% shareholder increases their stake by more than 50 percentage points over a rolling three-year period. it is often referred to as a “lookback period” or a “rollforward analysis”.

to no one’s surprise at this point of course we find evidence of this very thing happening in the Deloitte fee statement:

remember all those hours spent on a tax restructuring? I really can’t stress enough how significant this is, it is a really huge clue. Deloitte confirms that they were performing exactly this analysis.

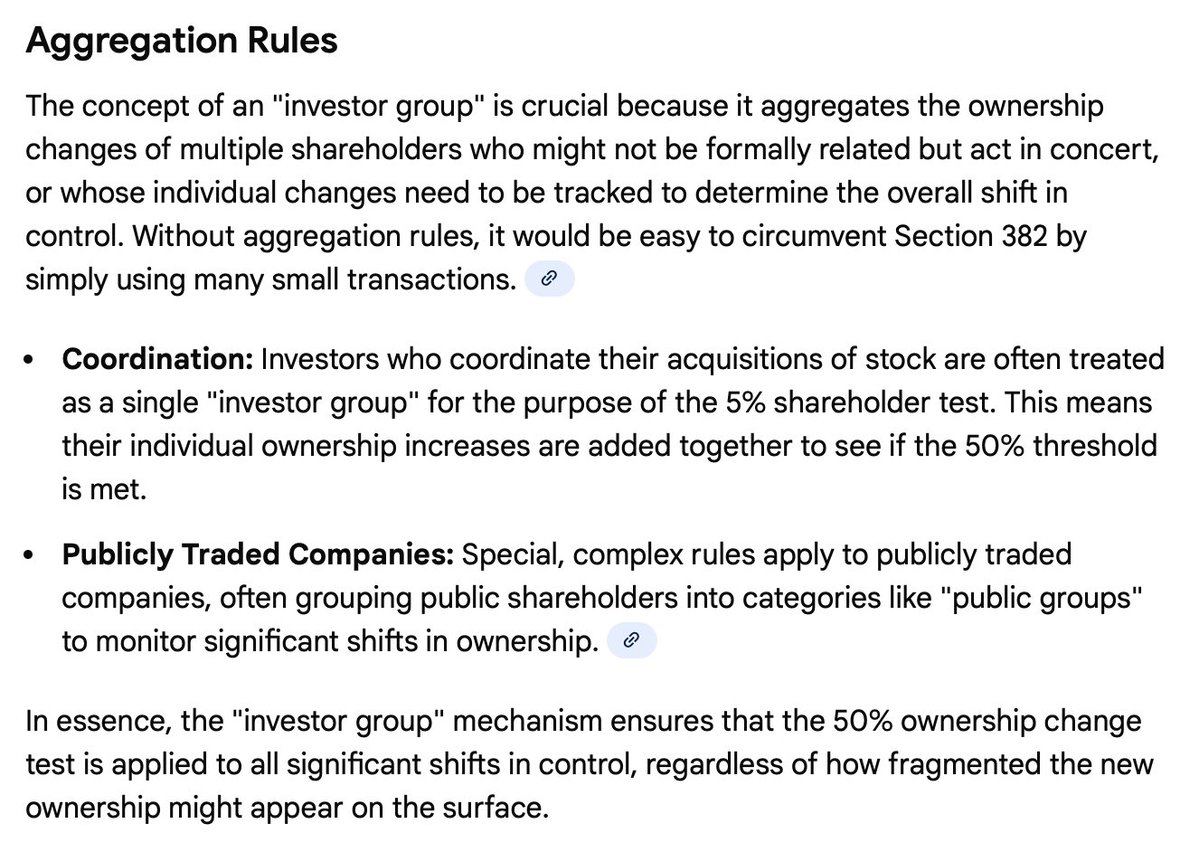

now here is where it gets interesting because this rule is not limited only to a 5% shareholder but it also envelops anyone who would qualify as a proxy or an affiliate with them:

over time we have seen many mentions of proxies and affiliates; from the Lazard Dealer Manager Agreement, to the credit bid definition inside the FILO Credit Agreement, the HBC equity raise, just to name a few. these protections and extensions to affiliates have been present for a very long time, with the Lazard DMA predating even the FILO Loan on August 10, 2022.

so.. if the percentage by value owned by one or more 5% shareholders increases by more than 50 percentage points over the lowest percentage ownership of such shareholders in a three–year period, a change in control is triggered and “yer NOL’s are gone, bro”.

this is really important to understand. for a Company who claims that the NOL is a valuable asset to them in the context of a Chapter 11, this would be something they would be paying very close attention to.

put simply it is designed to prevent companies from being bought just for their tax breaks.

the 50% rule says:

• if the ownership of the company changes by more than 50% over a rolling three-year period, the company's ability to use their NOL’s is severely limited.

• the IRS puts a cap on how much of the "old" losses can be used each year after the "new" owners take over.

it is not really up for debate that the NOL was a valuable asset. now we’ve explored both a two-year and three-year limitation to prevent taking advantage of special tax breaks available only inside of Chapter 11. the possibilities should be dwindling.

tomorrow we will do the math.. until then!

107

148

724

159,160

*Limit ONE item per customer. Exclusions include: Stolen items of any kind, unless it’s Half-Life 3. Your cousin’s mixtape. Your ex’s espresso machine. Dirty clothes of any kind including but not limited to socks, underwear, t-shirts, pants, shorts, and underwear (seriously, don’t bring us your dirty underwear). Illicit drugs and alcohol. Nuclear bombs. Computers (such as desktops, laptops, notebooks, all-in-ones, minis, workstations, e-readers, tablets, thin clients, smart displays, virtual reality headsets with built-in processor, interactive flat panel displays with built-in processor) excluding certain MacBooks GameStop normally accepts in trade. The Mayan Calendar. Copper wire, alternators, transmissions, and other vehicle parts. Half-Life 3 (unless it’s stolen—then sure). Broken games. Cribs. Fraudulent gift cards. Greg. Televisions. Car seats. Italian plumbers, mushroom people, and giant fire-breathing tortoises. Bones. Full-size planes, trains, and automobiles. Torn up Mark Sanchez trading cards. Life-size cardboard cutouts of your celebrity crushes. Sonic The Hedgehog 2006. Mercury, arsenic, anthrax, any other sort of poison. Small scale servers. Any UAVs, ray-guns, or noob-toobs. Jewelry. Macaroni art of ANY kind. Counterfeit currency. Cursed items. The 2007 hit “Bee Movie”. Hazardous waste or material, chemicals, liquids. Siblings, and other close relatives. Ashes of your loved ones. Recently unburied copies of E.T. The Video Game. Vacuums filled with ghosts. Stone wheels. Cherries, Nuka-Cola, sweet rolls, star drops, Jill Sandwiches, pork buns, or any other food item. Dead or alive animals (Taxidermy items are valid for trade). Sexual and explicit items. Social security cards. Expired drivers licenses. Guns, unless it’s the Halo 3 Battle Rifle. That Zune you only used once. Any historical artifacts such as the riches of El Dorado, The Ark of the Covenant, and the Scion. Small electronic equipment (portable digital music players, VCRs, DVD players, DVRs, digital converter boxes, cable or satellite receivers, projectors including those with DVD player capability). Items resembling body parts. Liquids. That one gift from Aunt Helen (don’t worry, we won’t tell). Whatever the heck a Bandicoot is. Bones. Living animals (yes, that includes your ant farm). Any Books of the Dead. Halos. Rethink your life choices if you’re still reading this. But also thank you for reading this. Computers peripherals intended for use with a computer and weighing less than 100 pounds (monitors, keyboards/keypads, mice/pointing devices, external hard drives (excluding those normally accepted in trade), facsimile machines, document scanners, printers, 3D printers, label printers, digital picture frames). Church organs. Your dying gardenias. Bonfires. Full-size planes, trains, and automobiles. Any recently resurrected dinosaurs. The entire 2002 Cleveland Cavaliers roster. Projectors including those with DVD player capability. The Hammer of Dawn. Suss individuals. Items MUST fit in our 20x20x20 measuring box. Terms and conditions of promotion are subject to change. GameStop employees have the discretion to reject any item.

191

212

2,899

495,393