FintechPolicy.org serves as a hub for collating and analyzing global regulatory developments in financial technology. LinkedIn: bit.ly/2q7V6Vh

Joined April 2018

- Tweets 909

- Following 213

- Followers 447

- Likes 480

57 Photos and videos

FintechPolicy.org retweeted

19 Jun 2023

Digital Euro bill leaked - Will Europe have a Central Bank Digital Currency? 👀

What is it?

👀 A draft law for the Digital Euro, a Central Bank Digital Currency for the EU, has been leaked. It would be illegal to pay interest on the new digital Euro or charge for using or moving it. It is designed to replicate cash and work offline, like withdrawing bank notes at an ATM. Shops would have to accept the Euro and would not be programmable. There are doubts about whether the bill could pass through the Parliament, but the Commission would publicize a draft.

My analysis 👇

🤔 This is the start of the debate, not the end. A draft bill that hasn't made it near the floor is far from something passable. The imperative has shifted from worries about private companies like Facebook threatening the role of the Euro. The concern is G7 vs. BRICS currencies; notably, China has a CBDC. I wouldn't expect a Digital Euro to be live and available to consumers this decade.

🤔 The temptation with digital is to create traceable money. The criticism of CBDCs is that the privacy and anonymity of cash would be lost. This bill attempts to address that by assuring it will be private, but like taking money to a branch, banks would play an essential role in identifying where the cash came from.

🤔 We need a cash-like thing for the digital economy. Digital money that works offline is valuable. We have physical money that can work offline, which allows the vulnerable and unbanked to operate in society. The future will have more digital and not less, so having something to replicate that function of money for the marginalized is useful. A nation-state is as good as anyone at providing digital cash since they already do it with physical cash.

🤔 Do G7 countries need a CBDC? China's CBDC is an alternative to the big tech payment rails from Tencent and Alipay. China's policy objective is to ensure it can manage and plan the economy centrally and is less concerned about individual privacy. That's not an objective the G7 shares, nor is it required. There are already multiple payment rails in the West. Adding another could be useful, however.

🤔 Not having programmability ruins the best feature of digital cash. Smart money would unleash innovation, but perhaps there's a way to achieve policy objectives and enable innovation without a CBDC? The UK is researching providing APIs to the central bank payment infrastructure to provide a "CBDC" in a sense. This would bring the benefits equivalent to "FedNow access" for banks and private sector payments companies. In turn, these companies could provide true digital cash for consumers via these APIs. You could call that a CBDC, but it looks a lot more like APIs for others to distribute digital cash within guardrails created by the central bank. It wouldn't require a Blockchain, it could be private, but it's also very early research.

2

7

22

7,558

FintechPolicy.org retweeted

20 Jun 2023

Detailed conversation with acting Comptroller Mike Hsu on 3rd party risk management, MDIs and the banking crisis with @ChrisBrummerDr

podcasts.apple.com/us/podcas…

1

5

10

2,754

FintechPolicy.org retweeted

20 Jun 2023

A #UnifiedLedger – a new type of financial market infrastructure – can harness the benefits of tokenisation by combining #CBDC, #TokenisedDeposits and #TokenisedAssets in shared programmable platforms. #BISAnnualEconReport

bit.ly/3NCpfrm

20

136

336

98,111

FintechPolicy.org retweeted

21 Apr 2023

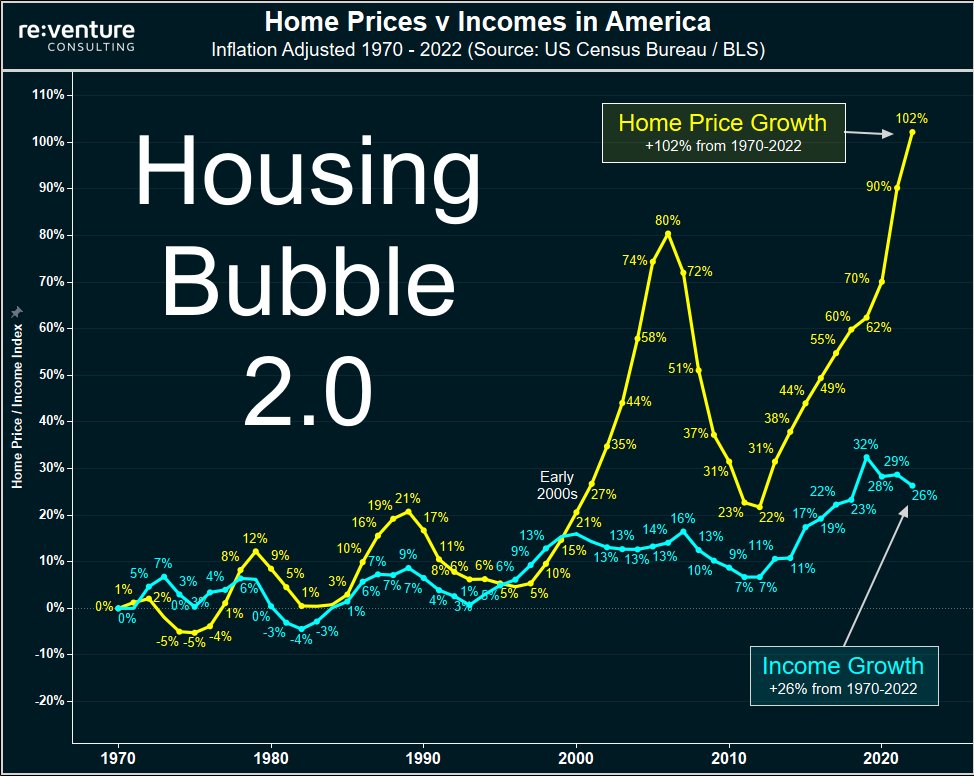

The fundamental problem in today's Housing Market is simple:

Home Prices are growing way faster than Incomes.

Real Home Prices up 102% since 1970.

Real Incomes only up 26%.

Something changed starting in early 2000s.

348

1,572

6,188

1,552,778

FintechPolicy.org retweeted

3 Aug 2022

PWG report identified right risks on #stablecoins but disagreement on how to handle still in Congress and unclear on timeline — @USTreasury Under Sec. Liang responding to always insightful @ChrisBrummerDr during @PhilFedResearch #FinTech conference.

6

21

FintechPolicy.org retweeted

#SaveTheDate! Due to international interest and schedules, DC #FintechWeek2022 will be moving up a week to coincide with the #IMF and the #WorldBank meetings. We expect our most influential in-person event to date! Looking forward to seeing you on Oct 11 12

ALT Save the Date! Fintech Week 2022 October 11 and 12.

5

6

FintechPolicy.org retweeted

27 Jul 2022

Maybe worth noting that when the CEA looked for historical parallels to current inflation, they found that the best match was 1946-48 1/

27 Jul 2022

Given all the discussion this week, I thought it'd be interesting to look back at the one example we have of a two-quarter contraction in G.D.P. that was *not* labeled a recession by NBER: Q2 and Q3, 1947.

9

55

230

FintechPolicy.org retweeted

28 Jul 2022

Thanks to European Parliament Vice President @EvaKaili and @kerstpe for hopping on my podcast to provide an insider's look on the back story for MICA--and breaking down what it means for the world's crypto policy. @Europarl_EN podcasts.apple.com/us/podcas…

3

8

24

FintechPolicy.org retweeted

27 Jul 2022

🔥🔥Financial Regulation, Corporate Governance, and the Hidden Costs of #Clearinghouses is featured today on @HarvardCorpGov! @OhioStateLJ

Particular appropriate timing given today’s @CFTC meeting on Governance Requirements for Derivatives Clearing Organizations #CFTC #finreg

Posted: Financial Regulation, Corporate Governance, and the Hidden Costs of Clearinghouses, corpgov.law.harvard.edu/2022… #corpgov #Clearinghouses #FinReg

3

15

FintechPolicy.org retweeted

14 Jul 2022

Several Chinese cities get ready to airdrop digital yuans.

Shenzhen, with 18 million residents, had 2.6 million people signing up so far. buff.ly/3OctqqK

14

24

82

FintechPolicy.org retweeted

14 Jul 2022

For the dozen people who asked the price. $0. (It’s why we do it—to deliver a world class experience for founders, regulators, the public, for free). But space will be super limited this year! We’ll announce a registration process in the future.

12 Jul 2022

DC Fintech Week returns in person, October 17-19, 2022. With lots of hard work—and goodwill from friends around the world—it's become the country's premier forum on financial technology and policy. Look forward to seeing everyone in Washington this fall.

dcfintechweek.org

1

5

24

FintechPolicy.org retweeted

12 Jul 2022

DC Fintech Week returns in person, October 17-19, 2022. With lots of hard work—and goodwill from friends around the world—it's become the country's premier forum on financial technology and policy. Look forward to seeing everyone in Washington this fall.

dcfintechweek.org

3

3

20

FintechPolicy.org retweeted

10 Jul 2022

"It feels like the ground is moving beneath the feet of everyone in financial services. Slowly, then suddenly.

Embedded finance fundamentally shifted how banking gets distributed. DeFi will change how it gets manufactured and distributed"

#fintech #DeFi

10 Jul 2022

Fintech 🧠 Food - July 10 2022

📣 Manufacturing vs Distribution in Finance

💸 4 Fintech Companies

👀 FTX bails out Crypto

👀 Robinhood memestock report findings

📚 State of web3 by Chainalysis

sytaylor.substack.com/p/-jul…

1

2

8

Financial engineering to be put on trial in bankruptcy courts | Financial Times ft.com/content/e07656a5-6103…

1

4

FintechPolicy.org retweeted

24 Jun 2022

And while we're on required reading

The @ChrisBrummerDr testimony on the Future of Digital Assets Regulation is ESSENTIAL reading

chrisbrummer.medium.com/cong…

2

3

7

FintechPolicy.org retweeted

18 Jun 2022

LATEST: Bitcoin falls below $20,000 for the first time since December 2020 ⬇️ trib.al/11u4zU4

48

106

322

FintechPolicy.org retweeted

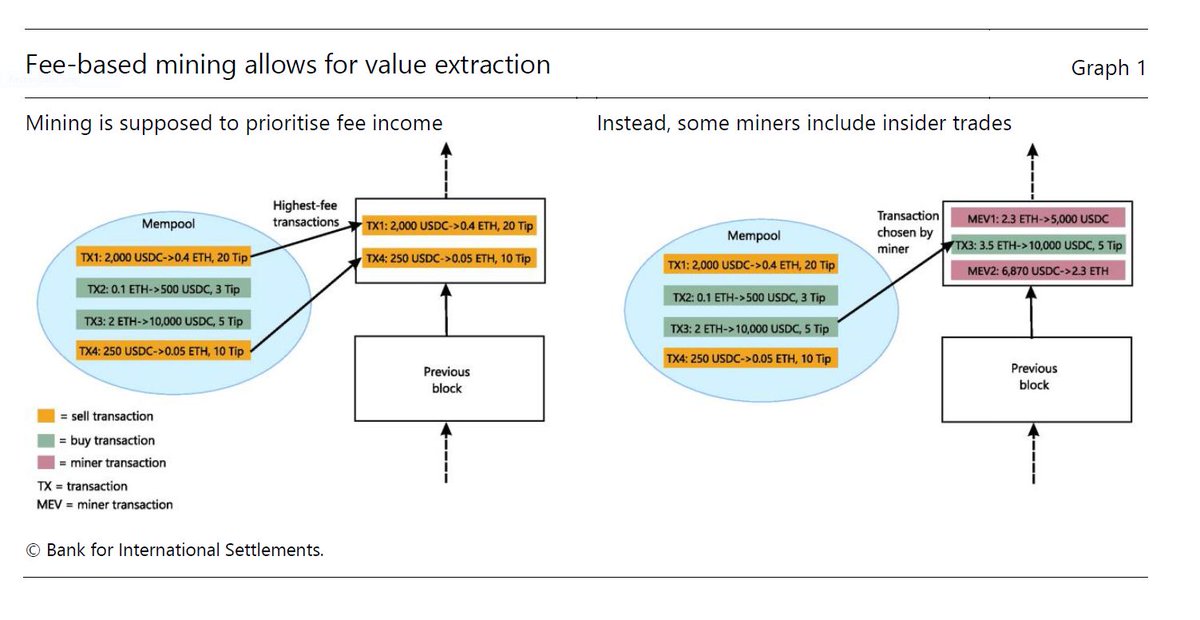

16 Jun 2022

Incredibly vindicating to see the @BIS @RaphAuer @Jon__Frost use my framing of miners as intermediaries in this BIS Bulletin.

16 Jun 2022

#Cryptocurrencies such as #ETH rely on #miners to update the #blockchain. These intermediaries can include, exclude and order transactions at will, allowing for market manipulation in #DeFi #BISBulletin bit.ly/3zGqyyY

2

9

43

FintechPolicy.org retweeted

7 Jun 2022

Excited to join @ChrisBrummerDr again on the #FintechBeat podcast! We discussed my book, There's Nothing Micro About a Billion Women and the main challenges keeping us from fully economically empowering women (as well as the solutions), and more! #financialinclusion

🎙️🎧 New ep of the #FintechBeat podcast: cms.megaphone.fm/channel/fin…

@MEIskenderian, the CEO of Women’s World Banking, talks about her new book and the opportunities and challenges facing women entrepreneurs in developing countries.

1

4

FintechPolicy.org retweeted

Join @rff tomorrow, June 8 from 9 - 10:30 am EST, for "Decarbonization Policy and International Competitiveness". IIEL professor @J_A_Hillman will be joining to break down recent developments in decarbonization and industrial competitiveness

RSVP here rff.org/events/rff-live/deca…

2

1

FintechPolicy.org retweeted

7 Jun 2022

okay, so here are my quick thoughts on the Lummis bill:

22

225

769