That's the power of Intel inside.

Joined October 2023

- Tweets 2,147

- Following 227

- Followers 1,940

- Likes 5,237

128 Photos and videos

Pinned Tweet

2026 Intel Watchlist

H1

• CES: Panther Lake momentum (18A)

• Clearwater Forest launch (18A EMIB 3.5D)

• EMIB/EMIB-T design wins / customer callouts

• Direct Connect: “a new node after 18A-P”

• External 18A-P tape-out announcement

• More partnership/investment signals

H2

• 14A major external customer signal

• Ohio investment acceleration / Oregon D1X Mod 4 construction update

• Rack-scale AI GPU solution: Jaguar Shores progress/launch signal

• Intel×UMC 12nm platform milestones design wins

• 18A yields stabilize 18A-P ramp

• Nova Lake / Diamond Rapids launches

• IFS financials: op loss burn-down

6

27

223

32,908

Obviously, it’s because of the significant 18A ramp up from Q2 and the start for shipping of Wildcat Lake, which can truly replace Raptor Lake as OEM loves that part so much.

In contrast, AMD will continue to focus on server CPU and keep prioritizing capacity for it.

Jun 12

MSI Chairman Warns Memory & GPU Shortages Will Drag Into 2026, But Says CPU Supply Will Get Better By Q3 wccftech.com/msi-warns-memor…

wccftech.com/msi-warns-memor…

1

2

50

6,583

SpaceX is building the infrastructure of the future

1,205

3,965

30,458

43,768,623

That’s a luxurious problem, implying massive demands ahead.

I bet when Intel raise the capital for the fab buildout, the stock price will skyrocket despite the dilution.

Jun 11

SemiAnalysis says $INTC currently does not have enough money for major CapEx spending.

They need to raise capital through dilution 👀 a 4% to 5% dilution would raise ~$25B

They need to build new fabs and they simply don’t have the funds right now!!! 😱😱😱

2

1

50

6,574

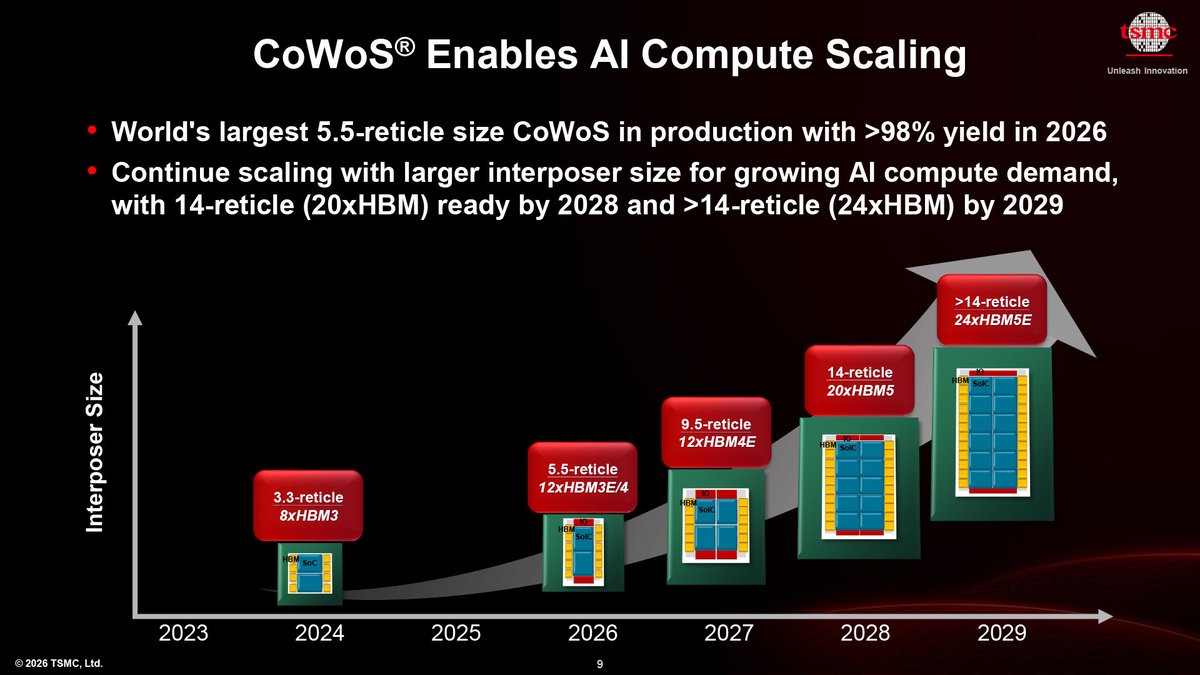

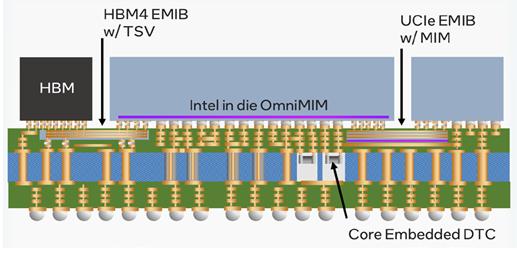

TSMC is aiming 14x reticle for CoWoS-L in 2028, Intel is 12x.

That said, I believe Intel will soon revise up its EMIB-T target as it’s easier to scale up the size, and, the target was set a year ago.

There are 2 key challenges for EMIB:

First, as the EMIB reticle size enlarges, the CTE mismatch between the top dies and the substrate will cause serious warpage.

Second, EMIB-T substrates include a lot more passive devices, such as eDTC, eMIM, and IVR, and require higher precision and more time for bridge die bonding which will make it harder to manufacture, and that’s the key reason the substrate yield is still low.

That’s CoPoS.

TSMC is aiming 14x reticle in 2028 for CoWoS-L.

1

8

77

10,074

That’s very true. Dave Zinsner said they are running the fab at 100% utilization.

Jun 10

Interesting stat that foundry utilization rates are back to, wait for it, 2021 levels. Only difference in this cycle is Intel is back to over 90%.

19

2,420

Some people say assembly yield is irrelevant, substrate yield is the key.

Of course assembly yield is extremely relevant when it comes to costs.

Customers let you place their “good dies” on “good substrates,” so assembly yield directly impacts their final product cost.

Substrate yield matters when it comes to throughput, but compared to top dies, it’s not the main cost driver. That’s why, from a cost perspective, assembly yield is far more important than substrate yield.

Jun 8

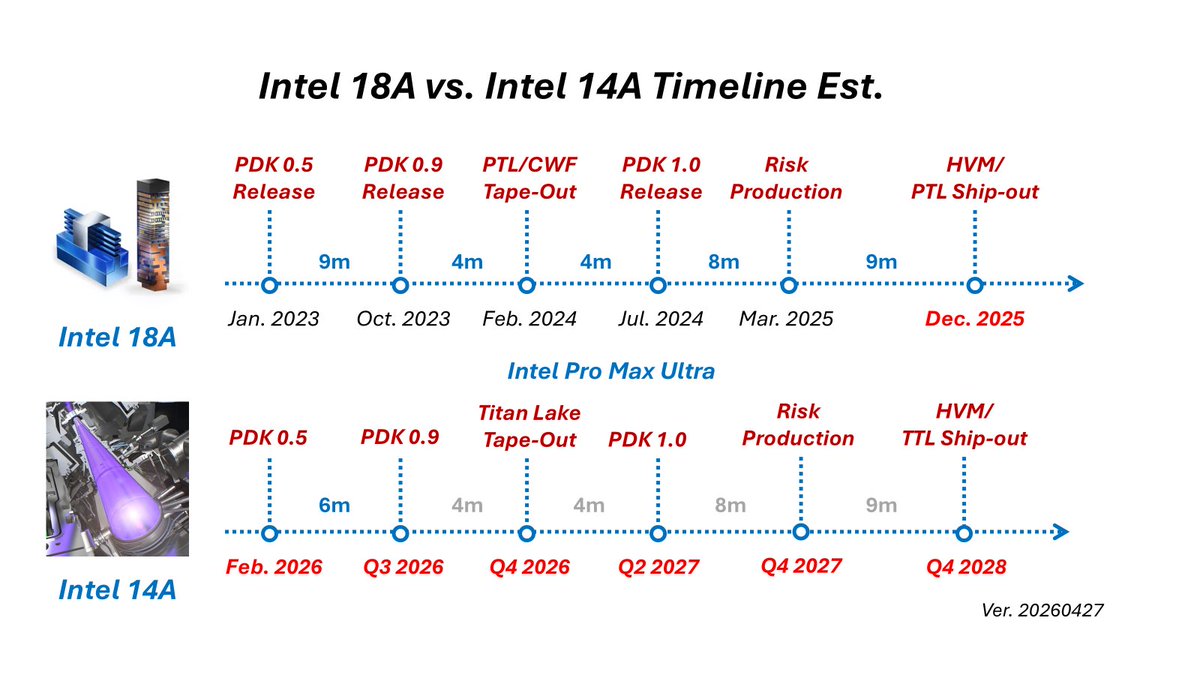

Intel (INTC) Note Takeaways:

•Big Raise for Foundry Capacity

◦Intel 3: 80% (mainly Ireland) by end-2028 (vs end-2026)

◦18A: 100% (Arizona) by end-2028 (vs end-2026)

◦14A: Strong ramp in Oregon

•Capacity Drivers:

◦Robust server CPU demand

◦18A yields improving to ~80%, EMIB to 90-95% in recent weeks

◦Major U.S. fabless on pipeline

◦Major smartphone maker to start with 18A-P (tablets/PCs) committed to 14A capacity

◦TeraFab project late-2028

•18A Capacity Shift:

Pathfinder Lake volume wafer capacity → Clearwater Forest (CWF) starts 3Q26, with full volume 1Q27 (expected to be ~1/3 of total 18A wafers)

•Financial Matrix:

◦IFS to turn profitable in 2H27

◦DCAI revenue 39% YoY in 2026E / 30% in 2027E

•Nvidia Collaboration: Likely includes x86 CPUs

→ PC (RTX Nova Lake in 2027)

→ Server CPUs (Intel x86 IP foundry) in late 2028

•TP Raised to $135

1

24

3,511

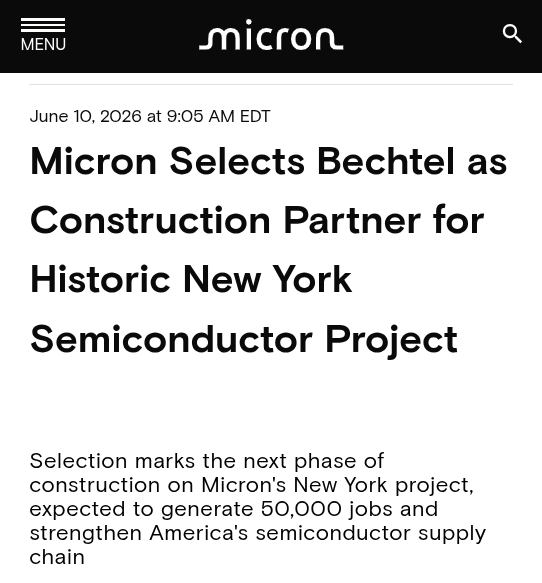

Bechtel hadn’t built semiconductor fabs for a very long time before Project Cardinal (Intel Ohio). Their last major fab project was likely for Motorola or IBM.

That’s why I believe it is Intel who gave Micron the confidence that Bechtel can deliver a large-scale fab today.

Jun 10

Bechtel lands the Micron NY contract—it will be the nation’s largest semiconductor manufacturing facility. They're also building Intel's Ohio fab.

2

2

32

4,293

Intel Pro Max Ultra retweeted

=>

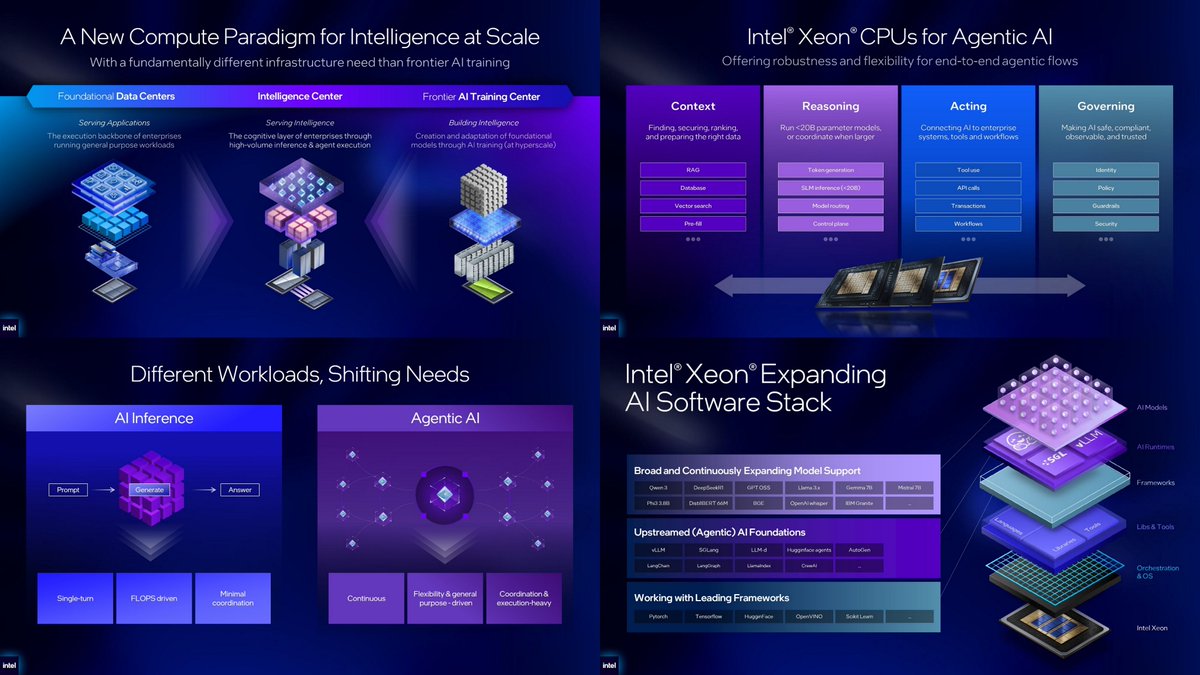

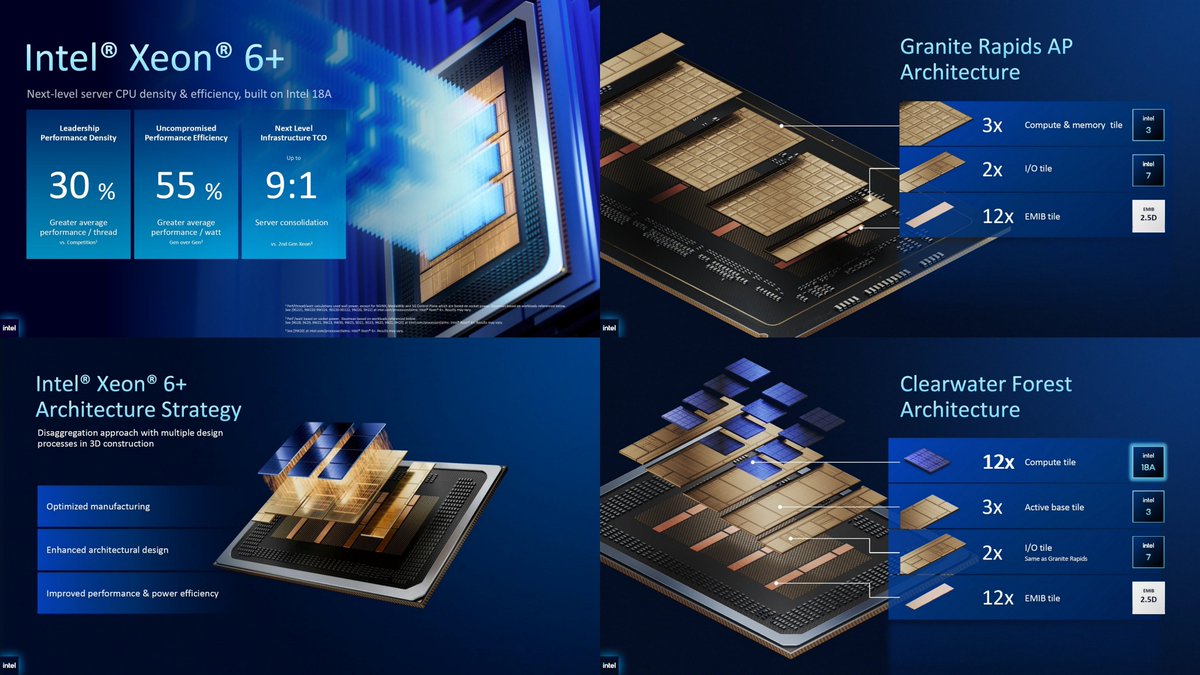

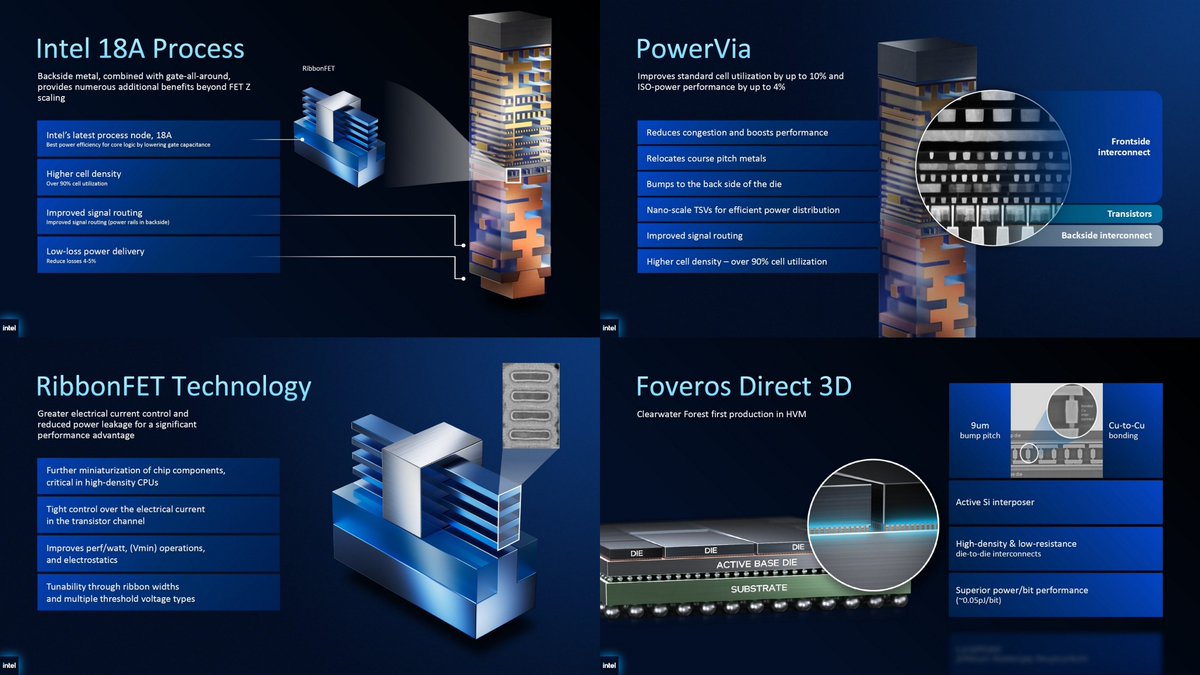

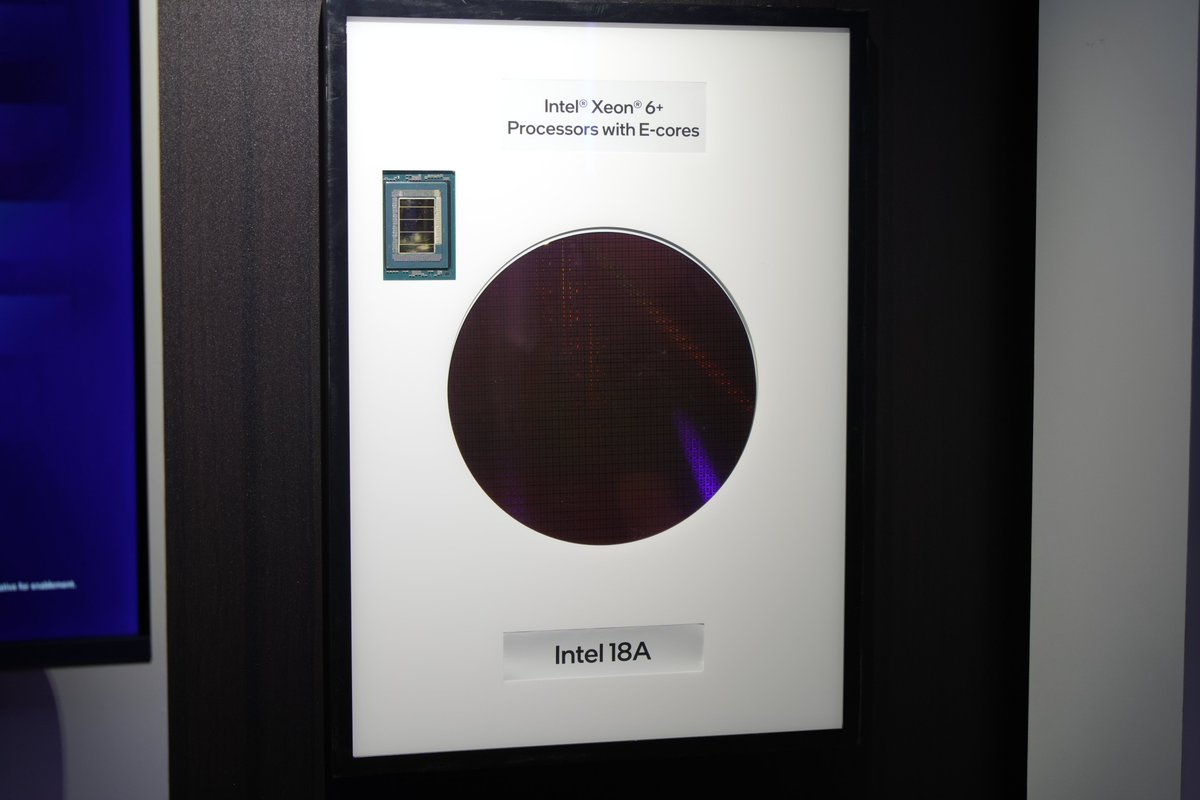

Intel Data Center Business Strategy, Kevork Kechichian, EVP and GM, DCG, Computex 2026, Jun 3, 2026 (117 pp) intel.com/content/www/us/en/…

Xeon 6 - Product Presentation, Jun 3, PDF (66 pp) x.com/ogawa_tter/status/2061…

COMPUTEX 2026, Keynote, Jun 2 youtube.com/live/1h_zY377urU

=>

"Intel Puts Agentic AI to Work with Xeon 6 , Networking, and AI Systems", Jun 1, 2026 newsroom.intel.com/data-cent…

Intel Xeon 6 - Product Presentation, Jun 1, PPTX (66 pp) intel.com/content/www/us/en/…

COMPUTEX 2026, Keynote, Jun 2 youtube.com/live/1h_zY377urU…

Press newsroom.intel.com/artificia…

1

3

12

3,050

They do.

MTK is the first Intel Foundry customer, using Intel 16 produced in Ireland Fab 14/24 for Wi-Fi digital dies and STB SoC.

Soon, MTK will use more advanced nodes and more capacity from Intel, mark my words.

Jun 8

As Jukan wrote here, this is a packaging order win, not a fab production win

Mediatek isn't using IFS front end

2

4

52

4,558

Some takeaways from the server and PC OEMs recently:

🗄️Server

1. For general purpose servers and certain AI server, like NVL-8, CPU attach opportunities, customers still appear to prefer Intel Xeon.

2. Server CPU procurement is no longer a lead-time issue. It is allocation and price renegotiation. OEMs can seldom order CPUs nowadays, the hyperscalers / customers will negotiate with Intel / AMD directly.

3. Intel appears to be facing more severe CPU supply tightness than AMD, with server CPUs being the most constrained.

4. A special server or dense-compute design using large numbers of Lunar Lake, with Memory on Package, appears to be a potential workaround for server CPU and DRAM supply constraints.

💻PC

1. Rising CPU and DRAM prices are creating cost pressure for OEMs, but OEMs also seem able to pass these costs on to end customers.

2. High-end new notebook programs appear to be primarily based on Intel CPUs (or Intel CPU has more designs and SKU optionality), with OEMs citing Intel’s advantages in power efficiency and battery life versus AMD.

3. Intel 18A notebook design activity appears broad, spanning both high-end and lower-price segments. The presence of Wildcat Lake-based notebooks priced around US$699 suggests that 18A is not merely a premium showcase platform.

4. There were also no obvious delivery issues observed in Intel 18A CPU. This is a positive signal for Intel’s 18A client ramp, although actual shipment volume will still need to be verified over time.

3

8

62

17,439

IT’S A REAL MONOPOLY.

ASML should be treasured and supported. It is arguably the greatest company in Europe.

6

1,003

Clearly, Intel 3 is going to be the bottleneck for intel’s future growth: Panther, Nova, Razer Lake need it; Granite, Clearwater, Diamond Rapids need it. Fab 34 alone (plus F24) is not enough to fulfill those explosive server and client demands.

So I believe Fab 38 in Israel will be used for additional intel 3 ramp in the near future. F38.1 space is now ready for tool move-in.

6

7

92

6,756

Intel Pro Max Ultra retweeted

Jun 2

Just in and exclusive to @culpium

Intel is Struggling to Supply Laptop Chips Built Around its New 18A Node culpium.com/p/intel-is-strug…

5

6

35

104,086

Intel Pro Max Ultra retweeted

Jun 2

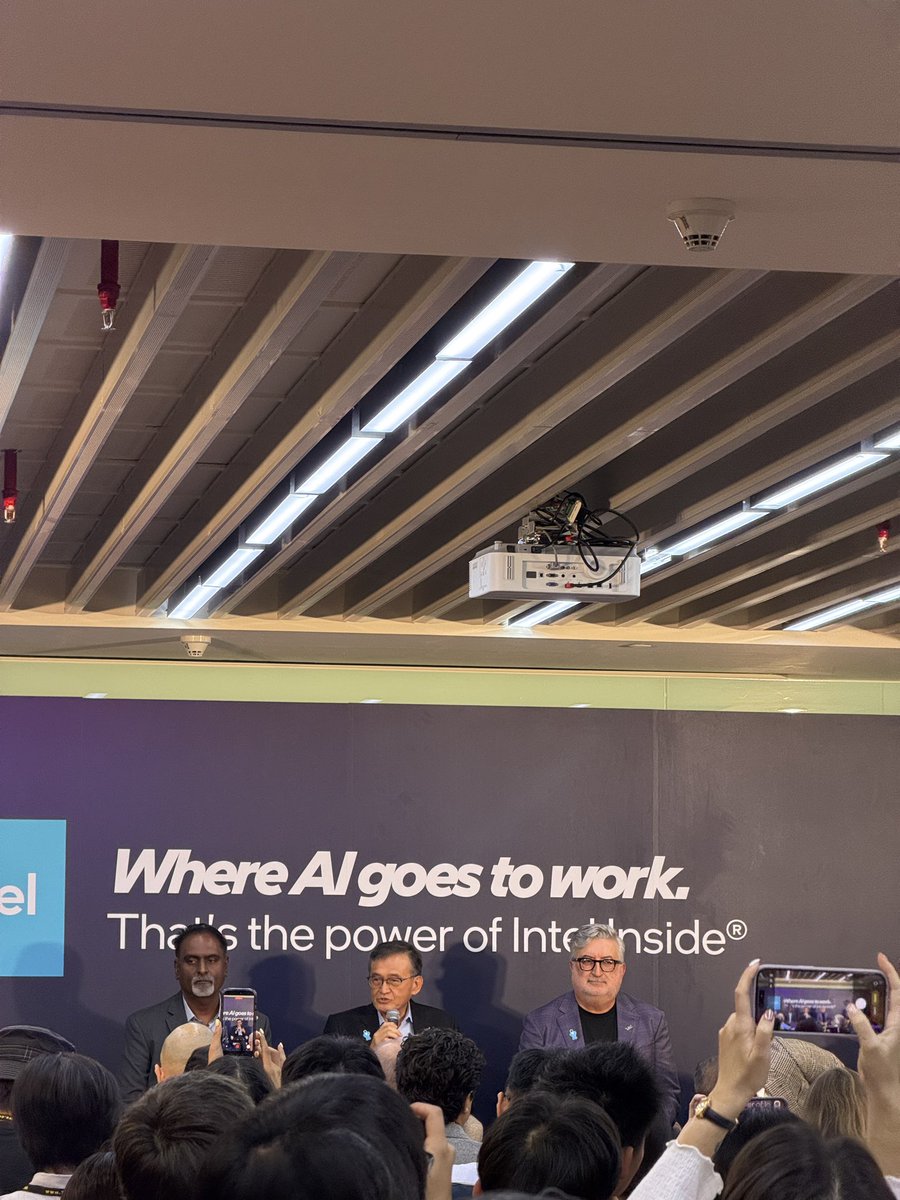

It's the @intel Computex keynote!

@LipBuTan1 to the stage

6

16

149

16,340

Intel Pro Max Ultra retweeted

Jun 2

"Tremendous progress in 14A" - LBT

2

10

146

23,457

MediaTek at Goldman Sachs Taiwan Day:

“The next-generation program is adopting only EMIB-T, with tape-out targeted for 4Q26 and mass production by 4Q27.”

This is significantly different from what Taiwanese media had reported — that the next-generation program would use both CoWoS and EMIB-T in parallel.

$INTC

18

49

392

123,446

Samsung Foundry Breaks Into China’s Largest Automaker BYD With Automotive Chips

Samsung Electronics’ foundry division has been found to be in talks with China’s top electric vehicle maker BYD and other local automakers over a series of contracts for autonomous driving systems on chip (SoC). As SMIC, China’s largest foundry, shows a wide technology gap versus Samsung Electronics, local automakers are approaching Samsung’s foundry about chip production.

According to the semiconductor industry on the 1st, Samsung Electronics has been confirmed to be in discussions with BYD and other major automakers over orders for 2nm (nanometer, one billionth of a meter) and 4nm process production. If the orders go through, local automakers far larger than the Chinese EV maker NIO, which currently uses Samsung’s 5nm process to make autonomous driving chips, would join the client roster.

An industry official said, “The core area Samsung’s foundry is now most focused on in the Chinese market is automotive electronics,” adding, “It is actively pursuing technical discussions with major Chinese automakers to produce next generation automotive SoCs on Samsung’s foundry’s leading edge processes.”

Behind the courtship that Chinese automakers are sending Samsung Electronics lies a structural limitation in China’s foundry ecosystem. SMIC, the largest foundry in China, currently implements a 7nm class process. But the dominant assessment is that it has a stark technology gap versus Samsung Electronics and TSMC when it comes to the fine process capabilities needed for next generation autonomous driving chips.

In particular, SMIC’s leading edge 7nm production line is fully booked with volume from a handful of strategic customers such as Huawei. Most of SMIC’s remaining production lines are skewed toward older processes of 14nm and above, making it difficult to meet the demands of Chinese automakers.

The reason Chinese companies have requested collaboration with Samsung Electronics reflects this reality. To achieve full autonomous driving, AI chips made on 4nm and even 2nm processes are required. Because autonomous driving chips must process large volumes of data inside the vehicle in real time, compute performance, power efficiency, and thermal management are all important.

Above all, because autonomous driving chips directly affect driving range and safety, automakers have no choice but to select a foundry with strong fine process competitiveness. For this reason, Chinese automakers have acknowledged SMIC’s slow pace of process innovation and pivoted toward entrusting chip production to Samsung Electronics’ foundry. Samsung Electronics’ 4nm process has now entered a mature stage where yields are stabilizing, and its most advanced 2nm process applying gate all around (GAA) technology has had its mass production capability recognized to the point that Tesla has entrusted it with manufacturing its next generation AI chip (AI6).

An industry official said, “With SMIC still showing limitations in the most advanced processes, Samsung Electronics is the most realistic alternative Chinese companies can choose aside from TSMC.” He added, “The fact that Samsung Electronics holds its own automotive chip design and mass production experience, such as ‘Exynos Auto,’ through its System LSI division is also a factor raising the trust of Chinese companies.”

The industry expects that, following Chinese automakers, Chinese big tech companies will eventually knock on the door of Samsung Electronics’ foundry as well. This is because Chinese big tech players such as Alibaba, Tencent, ByteDance, and Baidu are now staking everything on developing their own AI semiconductors and securing data center chips.

Because these companies are included on the list targeted by the US government’s semiconductor export controls against China, it would be difficult for them to place large orders with Samsung Electronics’ foundry right away. But the landscape could change depending on shifts in US China relations or any easing of export restrictions. The industry judges that Chinese AI chip developers that have collaborated with Samsung Electronics in the past, such as Baidu, are strong potential customers.

An industry official said, “Chinese companies showing interest in Samsung’s foundry is a move to find a leading edge process alternative rather than a choice to evade sanctions,” adding, “If they secure trust in automotive chips, the scope of cooperation could later widen to AI chips and high performance computing chips.”

9

38

355

59,733

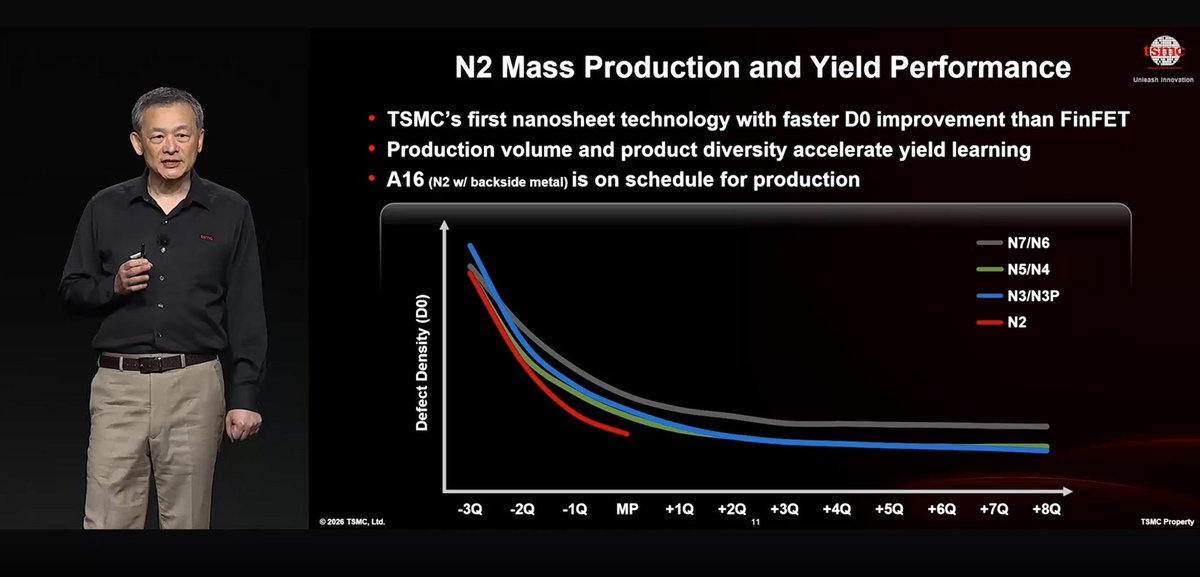

Morgan Stanley has absolutely no clue about the industry.

Intel mentioned multiple times their original 2026 year-end yield target was to reach “industry acceptance level”, which means D0 = 0.1. And they accelerated it to mid-year, indicating they are achieving that anytime now.

Morgan Stanley estimates Intel 18A yield at 50%.

It also notes that Apple is currently the only customer that has “signed a contract.”

$INTC

4

4

55

8,815