Bitcoin and other cryptocurrency news relating to Kenya and East Africa, and to a lesser degree the rest of Sub-Saharan Africa.

Joined December 2013

- Tweets 24,428

- Following 5,757

- Followers 2,724

- Likes 0

394 Photos and videos

KenyaCoin retweeted

The Practical Engineer made a fascinating video on how washboards in dirt roads form. I was just wondering about this last week when traveling back from Silver City.

youtu.be/3YvwqMDDb3k?si=Ehs5…

1

98

Ethiopians (w/ agency) tried to warn him:

youtu.be/0YHvtrasAgw

3

4

17

5,019

KenyaCoin retweeted

Jun 1

Swahili is spoken by 200M people.

We worked on Sauti TTS to help change that.

Try our Swahili text-to-speech demo:

msingiai.com/products/sauti

Building speech AI for African languages.

15

57

181

6,040

KenyaCoin retweeted

Jun 1

There are many things not going right in our country.

But one thing we can celebrate is how Blessed we are.

Watch 🎥🇰🇪♥️

2

16

43

1,398

KenyaCoin retweeted

Our Lightning Developer Bootcamp in Bujumbura, Burundi 🇧🇮 is officially a wrap and what an incredible week it has been.

Over five days, participants journeyed from Bitcoin fundamentals, the history of money, cryptographic signatures, transactions, and the blockchain, all the way to building and testing real projects on the Lightning Network. Today, they pitched those projects to the room. Watching developers who started the week with questions end it with working ideas is exactly why we run these bootcamps.

A huge shoutout to our instructors, @heyolaniran and @advaxeir. You didn’t just teach, you inspired. The depth, clarity, and energy you brought to every session shaped the entire experience. Thank you both.

To our executing team, @_Satoshee and @Ladyyyy_lo, thank you for the countless behind the scenes efforts that made this bootcamp possible. These events only succeed because of people like you.

A special thank you to @belyi_nobel, @Barakana_GE, and the @bitdevsgtga team for inviting us to Burundi, welcoming us so warmly, and supporting the local ground planning. Your community’s passion for Bitcoin education is truly inspiring, and this definitely won’t be our last time here.

And to our sponsors and partners who continue to make this mission possible, @btrustteam, @HRF, @Tether_Africa, @afribitcoiners, @planb_network, and @freetechite, thank you. Your support is what transforms an idea into five days of hands on Bitcoin education across Africa.

The Lightning Network is growing across this continent. One city, one bootcamp, one developer at a time.

Next stop: Kisumu, Kenya 🇰🇪

3

12

41

3,371

May 31

Frontier Fintech Newsletter #121

A Mature Industry Searching for a Second Act

Mobile money’s revenue is deepening across the continent, but financial services remain a story rather than a line that moves the numbers; and the operators, telco and fintech alike, are still looking

May 25

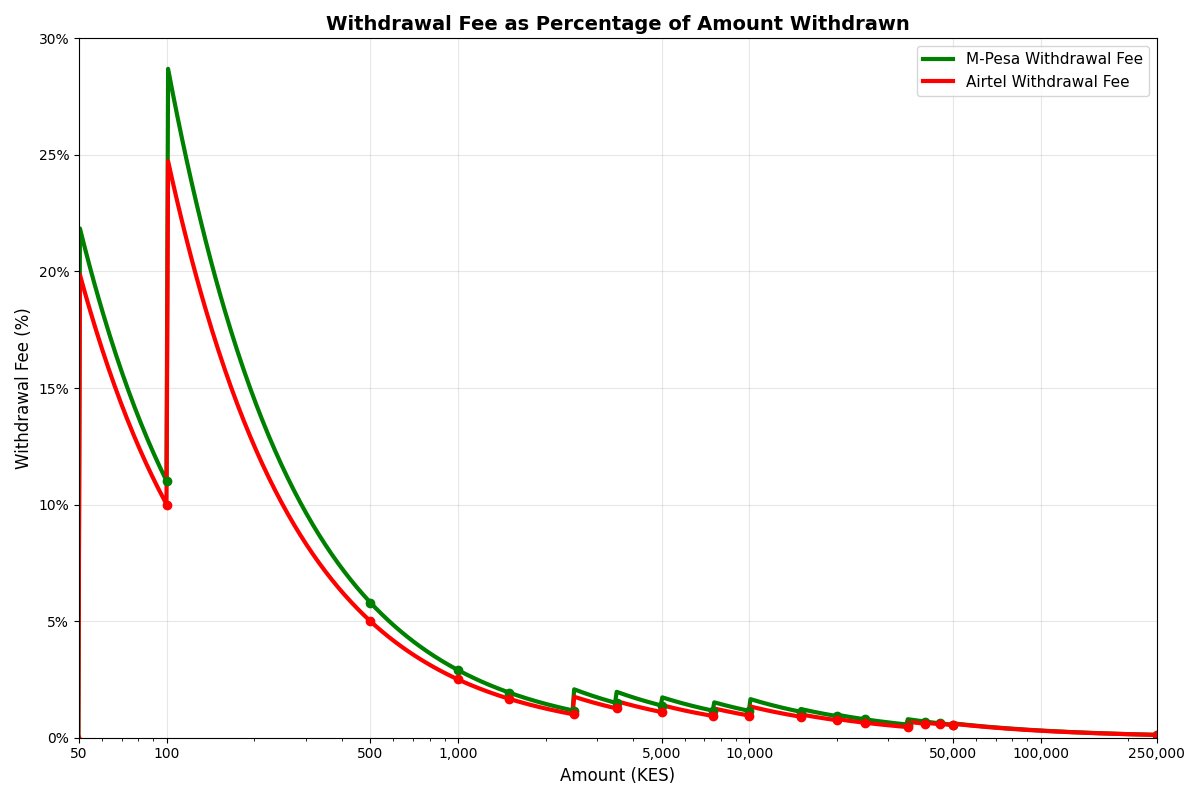

Airtel MoMo earns 0.728% on every dollar it processes. M-Pesa earns 0.438%. MTN MoMo, 0.396%.

You'd read Airtel's higher take rate as the stronger business. It's closer to the opposite.

In mobile money, withdrawal fees are the high-margin line. A customer tolerates a fee on a once-a-month cash-out that they'd never accept on every merchant payment. So a high blended take rate is the signature of a book still dominated by expensive basic transactions, a business monetising the turnstile rather than the loop.

This is the trap at the centre of the whole industry. A telco mobile money business is most profitable precisely when it is least mature. The one earning the fattest spread is the one still doing the most cash conversion. But the direction of travel for all three is away from exactly that, toward ecosystems where money circulates and the cash-out moment becomes rare.

So maturity is self-cannibalising. As an operator deepens, it trades its most profitable activity for thinner merchant flows. M-Pesa's take rate has fallen from 93bp to 60bp, not weakness, but the arithmetic of a turnstile becoming a loop.

And the second act that was meant to rescue the margin never arrived. Lending was supposed to re-rate a payments business into something richer. Yet M-Pesa books financial services at under 6% of revenue after $11bn through Fuliza. It's a rounding error at MTN. Airtel won't disclose it.

This is why the market values @CapitecBankSA at $1,154 per user and MTN MoMo at $109. One is a full-stack bank. The others are fee-on-transfer rails priced accordingly.

Mobile money is approaching its twentieth year; old enough to be infrastructure rather than innovation. And infrastructure that grows only with the population it serves is infrastructure waiting to be repriced or routed around.

Full analysis (Link in Comments)👇

1

65

KenyaCoin retweeted

Bankers Association pushes back against Finance Bill 2026, warns levies could cripple digital payments

eastleighvoice.co.ke/busines…

15

9

247

KenyaCoin retweeted

May 27

US To Set Up Quarantine Facility In Kenya For Americans Exposed To Ebola zerohedge.com/medical/us-set…

37

44

148

55,354

KenyaCoin retweeted

May 25

What do you do when your research could break the internet's cryptography?

Google: "prove it without showing it"

2

17

142

4,824

KenyaCoin retweeted

May 25

Walter Rodney was wrong.

Africans are poor because too many African countries make it hard to start businesses, get permits, access reliable electricity, trade freely, protect property, enforce contracts, attract investment, and keep the rewards of hard work.

Singapore is richer than Britain, its former colonizer.

Switzerland, which never built a colonial empire, is richer than Spain and Portugal, two of the greatest imperial powers in history.

695

1,275

7,978

920,051

KenyaCoin retweeted

Huge milestone for BitDevs Mauritius 🇲🇺 .

We’re now officially listed among the global BitDevs cities pioneered by BitDevs NYC.

Proud to represent Mauritius in this growing network of Bitcoin developers and researchers.

Big thanks to @btrustteam for the support.

1

7

19

462

Made in Africa: Kurt and the Open-Source Bitcoin Miner That Anyone Can Make

opensats.org/blog/developer-…

3

16

41

2,805

KenyaCoin retweeted

May 25

As a Zambian I stayed Four months in Kenya, and not once did I touch fiat.

From paying bills and buying everyday goods, I’ve lived entirely on Bitcoin.

Bitcoin isn’t just theory it’s real, practical, and working here.

And with @tando_me , it’s been seamless and reliable.

16

30

105

5,718

May 25

Should be of interest to those receiving payment in PayPal.

May 13

I built RemoteFlow — USD straight to M-Pesa. No blocks. Fair rate. Minutes.

RemoteFlow converts your USD earnings and sends them straight to your M-Pesa.

remoteflow.cc

#Kenya #MPesa #Freelancing

@engeniusam , @Moruri_c , @blackie_360

1

2

35

May 25

M-Pesa & Cash App are mostly A2A ledger entries — fast internal accounting, not true P2P settlement.

Bitcoin Lightning is different: real B2B/B2C settlement on an open network.

These apps are great stepping stones. The endgame: a circular bitcoin economy where value moves P2P

1

76

KenyaCoin retweeted

May 13

I built RemoteFlow — USD straight to M-Pesa. No blocks. Fair rate. Minutes.

RemoteFlow converts your USD earnings and sends them straight to your M-Pesa.

remoteflow.cc

#Kenya #MPesa #Freelancing

@engeniusam , @Moruri_c , @blackie_360

5

6

231

KenyaCoin retweeted

May 24

so this evening , i ported kenya-locations to TS/Kotlin/Swift libs while maintaining the data sources as simple json files ,

built to cover any sort of informal location addressing in 🇰🇪 projects i've done so far.

more to come ✨

→ github.com/davidamunga/kenya…

3

26

61

1,450

⚡ THE WAIT IS OVER ⚡

We are pleased to announce that Lightning trading is now live on the Hodl Hodl Mainnet, powered by our strategic integrations with @arkade_os and @satora_io

This milestone represents a significant advancement in our mission to deliver the most efficient Bitcoin-native peer-to-peer trading experience.

Our platform now offers substantially improved transaction speeds and settlement efficiency, enabling users to execute trades with greater speed and reduced friction.

Hodl Hodl users can now benefit from the speed and scalability that Lightning technology provides while maintaining the security and transparency inherent to our platform.

This is a major leap forward for Bitcoin-native P2P trading.

NOTE: Lightning Network trading is currently in BETA. During this initial phase, trading activity is subject to transaction limits ranging from $5 USD to $50 USD (approximately 700 to 70,000 SATs)

Welcome to Lightning on Hodl Hodl. ⚡

ALT Lightning trades on Hodl Hodl

9

39

120

22,267