Partner @Genventurecap investing in machine economy 🦊 Ex Chief Economist & CMO @Consensys 📈 Founder in Web3, roboadvice, data, and fintechblueprint.com

Joined May 2013

- Tweets 43,975

- Following 7,939

- Followers 24,028

- Likes 17,269

2,096 Photos and videos

Pinned Tweet

24 Mar 2025

Here are all my secrets

We cover crypto, AI, and the machine economy.

The weather changes but the stars point in the same direction.

Really enjoyed this conversation with @francescoswiss

24 Mar 2025

AI, Crypto & Web3: The Future of Intelligent Agent w/ @LexSokolin

00:07 - Who is Lex Sokolin

03:39 - The Economics of AI

05:16 - Why Crypto Struggles

07:51 - Web2 vs. Web3 AI

10:46 - DAOs in AI Frameworks

19:57 - The Rise of On-Chain AI Agents

30:35 - The Future of AI & Crypto

123

15

223

60,283

The next payments customer does not have a card in a leather wallet.

It has permissions, policy, credentials, and probably a spending limit set by someone in procurement.

Visa sees this. Stablecoins reshape settlement. AI agents reshape demand.

The prize is being the trust layer in between.

7

2

6

653

Investors top blasting into a speculative market won’t end well

It will feel good for a while

And then we will all throw up

6

4

564

This is called robot money

AI allocations rippling through the markets

Echoes in the rain

There’s a new phenomenon of small groups of people who are running these small little quant funds driven by AI models who are making fuck-you returns.

I’ve personally seen many who are 2x’ing capital in months. Many unsubstantiated rumors also claim SSI is a quant shop too.

Well known quant funds have all tested out LLMs for trading. Some claim it doesn’t work. Others, well.. what do we think Jane Street doing with their huge GPU cluster? On top of that, there’s a ton of people asking Claude / GPT what stocks to buy and/or “vibe code me a trading engine”. Applies to other financial instruments too: derivatives, futures, crypto, and on the less sophisticated side, prediction masks.

It begs the question: how does this change how we think about markets? how much retail volume is driven purely by the ripple effects of AI models? does this completely destroy efficient market hypotheses in favor of “correlated model hypothesis.” Early theories say

– Small studies including one by the Fed show destabilizing effects.

– We see amplified concentrated trades into the 20 known names in the market.

– Can leave trading vulnerable to GEO attacks like publishing specific articles to “poison” the models decision making.

Eventually any alpha generated by the model at a point of time *should* decay over time. New anti-AI trading strategies with custom post trains too. Remember, you need be able to afford the tokens to participate in this alpha. What does this mean for the future of wealth accumulation?

We live in a brave new world.

2

9

934

Banks do not need magical AI.

They need permissioned data, audit trails, model governance, compliance boundaries, and workflows that survive production.

A 90% accurate AI product in consumer software is useful.

A 90% accurate AI product in finance is a liability with a UI.

2

1

7

389

Every year someone announces the agent economy, allegedly

Today Mastercard shipped actual settlement rails for it — cards, accounts, stablecoins — and @Nevermined_ai is building the layer that decides what agents buy and at what price.

Being right early is indistinguishable from being wrong, until a card network shows up

Jun 10

1/6 @Mastercard just launched Agent Pay for Machines. New infrastructure built for AI agents to transact with each other, autonomously, at machine speed.

@Nevermined_ai is part of it 🧵

3

2

21

2,519

Lex Sokolin | Generative Ventures retweeted

AgoraGroup is proud to announce that Lex Sokolin, @LexSokolin, is joining the 2nd European edition of the Global Blockchain Congress.

Lex is an entrepreneur working on the next generation of financial services and economic growth. He is the Managing Partner and co-Founder of @genventurecap, a venture capital fund investing in the Machine Economy powered by Fintech, accelerated by AI, and settled on Web3.

We're beyond excited and looking forward to listening to what exclusive insights Lex is going to share on the GBC stage.

Be part of the blockchain revolution happening at the 2nd European GBC.

Register now: bit.ly/GBC-UK

#blockchain #London

1

5

234

holy shit Fable is powerful

We will all pick up the crumbs and be happy for it

1

2

216

For those of us building ZHCs, @levie shows what we need to move beyond vibes

Jun 10

This is a critical post to read if you’re building an applied AI company right now.

“An application earns its place in the untrainable corner by doing unglamorous work: arranging a company's private reality so a model can act on it, handing the model the tools to act, working with the customer to change the reality of its workforce. A company that brings the translation is tough to copy – and the translation never ends. Integration and maintenance run as long as the relationship does, won by teams that put domain-specialized engineers and tools next to the customer.”

There’s still an insanely large gulf between model capabilities and what it takes to apply them to specific corporate workflows. Some of that is technology that needs to be built, a lot is access to (and formatting of) the right data to work with, and a ton more is on the change management and specific implementation work (FDEs, etc.) it takes to make AI work in any specific corporate setting.

2 things can be very true at once: frontier models and labs will continue to grow an incredible amount, and there will be a vast ecosystem of software and services companies that emerge to bring the power of these models to real enterprises. This makes room for new infrastructure provides, applied AI companies in every vertical, new versions of system integrators, and more players.

Incredibly exciting time on all fronts.

1

8

1,254

Lex Sokolin | Generative Ventures retweeted

Jun 9

We're going to see an entirely new class of financial products emerge for consumers that strengthen the position of neobanks as the middle layer between trad banking and onchain finance.

One example is @olivetreeyield from our current batch. They're bringing differentiated yield to crypto through insurance backed annuities. While most crypto yield comes from staking, lending, vaults and treasury products, Olive Tree unlocks insurance balance sheets as a new source of principal protected yield (e.g 5.5%)

This gives consumers access to more predictable, returns while helping fintechs and neobanks offer financial products that are differentiated from the competition.

Over time, this market will likely become winner take most, with neobanks competing not just on UX, but on the strongest suite of savings, yield, credit, and investment products for their customers.

22

7

136

15,405

More of us discovering robot money

Jun 9

At NIV, we've been seeing tremendous growth clustering around the intersection of AI, Stablecoins, DeFi, and Fintech. This has led us to believe that agentic finance, defined broadly, will be one of the biggest trends of the next decade.

Indeed, we believe that 1) AI agents are on the cusp of becoming true economic actors, able to discover, negotiate, and transact, 2) there will be billions of such agents within 5-10 years, engaging in trillions of dollars in annual transactions, 3) these agents will need new financial systems, markets, infrastructure, and tools, which will unlock applications and experiences that are hard to imagine today, and create tremendous value.

This is one of our main areas of focus, so if you're working in this space, please get in touch.

Full Deck Here: lnkd.in/emSGsGDK

2

1

11

1,054

If SpaceX falters, others hesitate to follow. Risk capital floods into AI startups, overshadowing potential mega-IPOs and casting doubt on market sentiment. #SpaceX #AI #MarketTrends

1

7

519

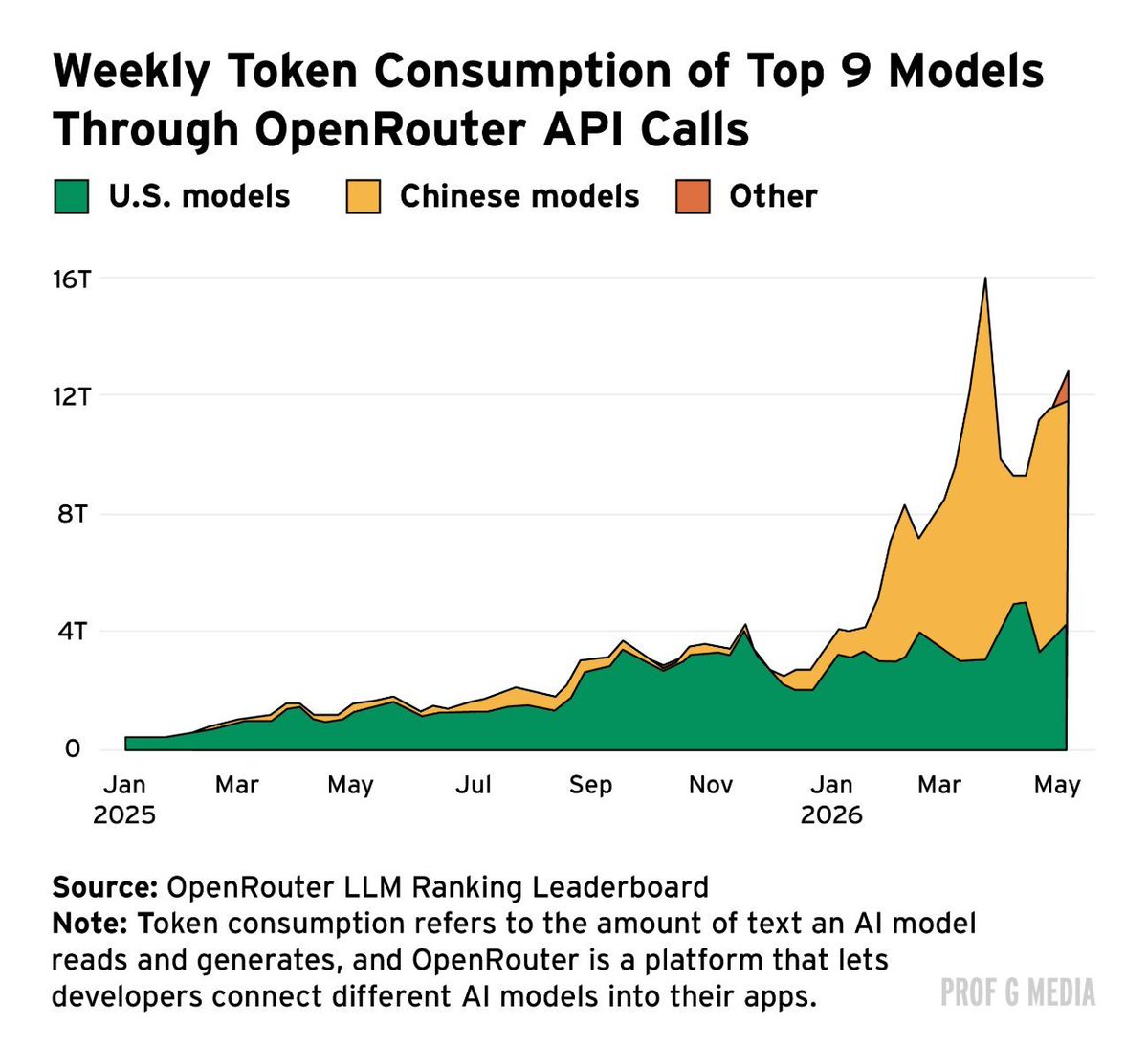

Open source will win

It won’t hurt a bit

Jun 7

This is a pretty striking shift toward Chinese models by American AI startups since the start of the year. substack.com/@profgmarkets/p…

1

7

1,739

Fintech doesn't have an AI problem.

It has a customer reality problem.

The same person exists as a payment account, a card profile, a loan application, a KYC file, a fraud signal, a support ticket, a brokerage balance, a rewards user, and a marketing segment.

Then we ask AI to “personalize the experience.”

Personalize what?

If the system does not understand the customer as one economic actor, the agent is just navigating a pile of product silos.

This is the part of AI fintech that feels under-discussed.

The winning layer is not just the chatbot, the copilot, or the workflow automation.

It is the shared customer model underneath them.

A truth layer across products, transactions, risk, compliance, support, and intent.

Once that exists, the product can change shape.

Payments become context.

Credit becomes dynamic.

Advice becomes situational.

Support becomes proactive.

Compliance becomes part of the flow, not a checkpoint at the edge.

This matters for banks, but also for wallets, brokerages, lenders, neobanks, payroll platforms, SMB finance tools, and embedded finance.

Fintech was built by unbundling the bank.

AI may force the bundle to come back as software.

Not as one app.

But as one model of the customer.

Smart builders are paying attention.

5

10

638

After getting used to Claude I am finding retail ChatGPT almost entirely unusable

I don’t see how they can come back

8

1

12

2,031

Agents do not need another chatbot wrapper.

They need:

- money movement

- identity

- permissions

- audit trails

- settlement

- risk limits

That is why the “agentic economy” becomes a finance story so quickly.

Once software can act, it needs accounts.

Once it has accounts, it needs controls.

Once it has controls, you are back in the world of banking, capital markets, insurance, and payments.

Except this time the customer may be a machine.

10

4

35

3,537

Lex Sokolin | Generative Ventures retweeted

Web3 brought us decentralized finance with platforms like Coinbase and Ethereum. Now, we're entering Web4 – the agentic economy. AI isn't just replacing search; it's reshaping payments, capital markets, banking, and insurance. #Web3 #AI #FutureOfFinance

8

4

15

1,821

Lex Sokolin | Generative Ventures retweeted

Jun 5

We continue to ship features that move us closer to the agentic economy future.

Right now working on analytics product across the industry where agentic treasury management can make a difference.

Strong overlap with agentic investment committee

First draft and always improving. Will be up on the main site soon.

2

6

42

1,290