Joined April 2025

- Tweets 7,032

- Following 500

- Followers 1,344

- Likes 6,572

884 Photos and videos

Pinned Tweet

€100 FOR FREE with Trading212‼️

1) Register for an invest account using my link

2) Deposit a minimum of €1 before 10 days after registration and buy at least €1 of a stock you like

3) Collect your Free share worth up to €100

trading212.com/invite/4Dru0x…

Let’s help each other 💪🏻

3

3

79

Morning 🌅

Have a good Sunday 💪🏻

Someone of you did buy $SPCX ?

2

1

85

Luke Simple Dividends retweeted

Someone could explain me why $NOW down 25% in 9 days?😅

68

4

147

38,607

🚨 TRADE ALERT 🚨

I want to share this trade I’m still in.

Bought on the third touch of the daily level and let it run 🚀

🟢 I’m already up 41.2% 😬

SL on the most recent low at 0.7600

If you want me to see similar trades don’t forget to follow 🔥

2

3

99

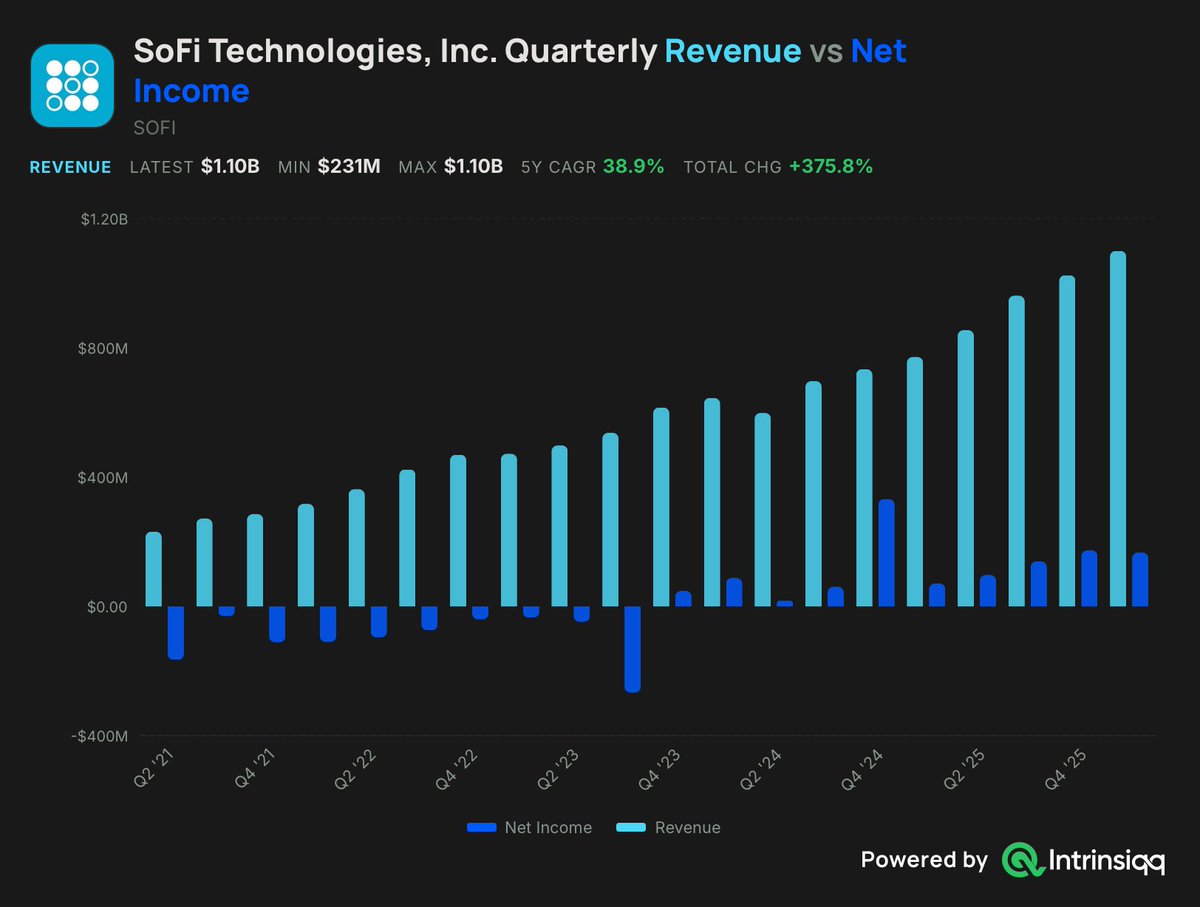

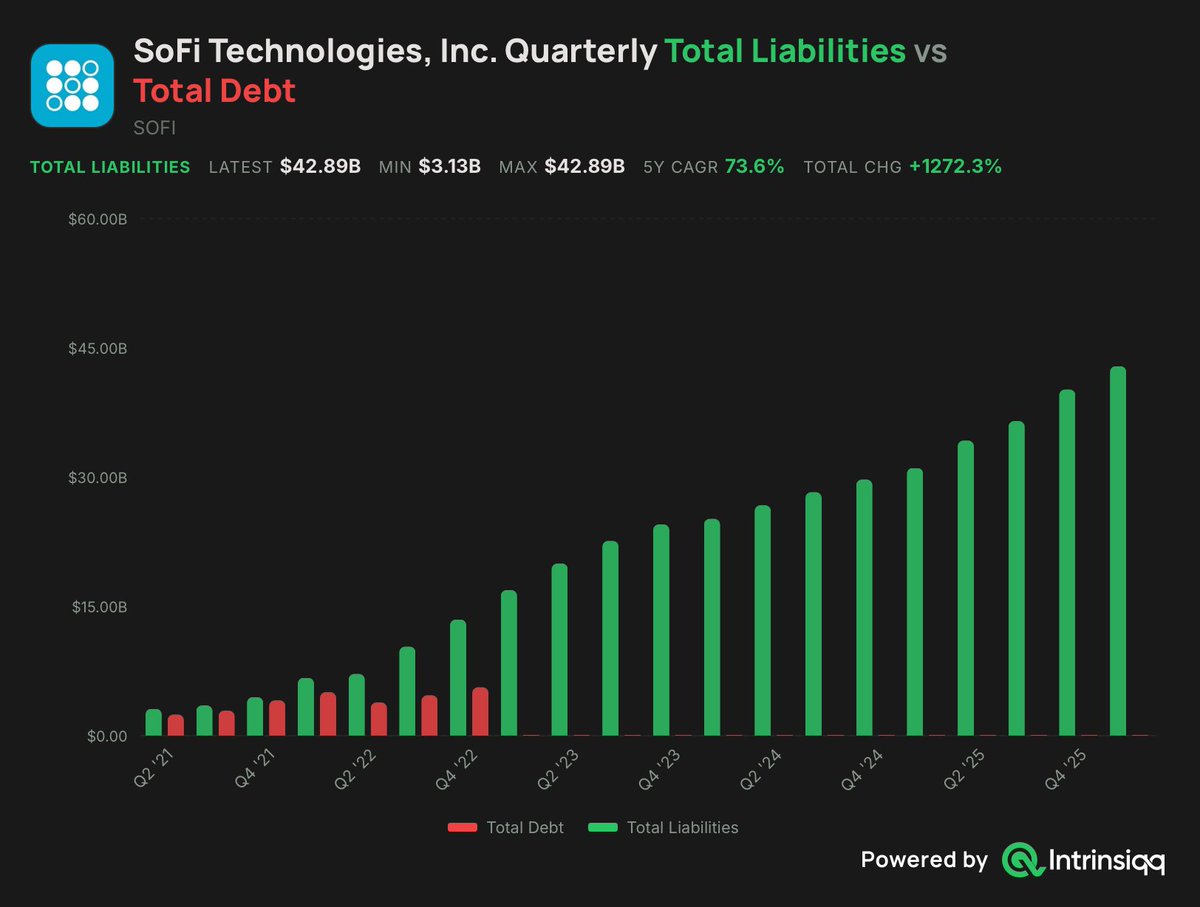

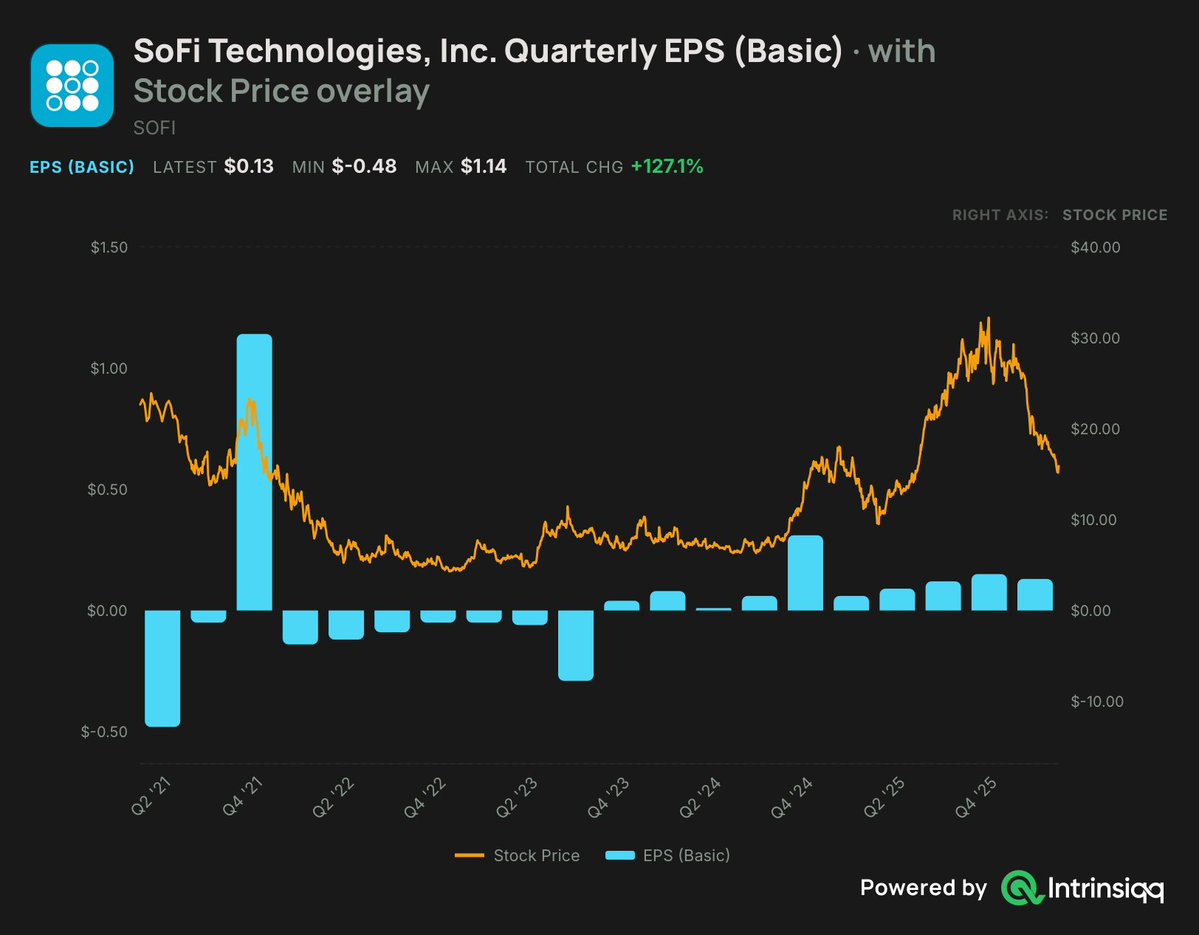

Do you think $SOFI is a BUY NOW?

During the last 5 Years:

Revenue: 376%

EPS: Turned positive

Price: -24.55% 🔴

I think something is wrong here🤔

20

2

76

5,996

🚨 THIS STOCK COULD 10X BY 2030 🚨

Adaptive Biotechnologies $ADPT

Here is my buy thesis and why it has multibagger potential over the next few years.

1️⃣ BUY THESIS

Adaptive's economic engine is clonoSEQ-an FDA-cleared measurable residual disease (MRD) test for blood cancers (like leukemia and multiple myeloma).

It is rapidly becoming the gold standard in oncology.

— Massive Growth:

The MRD segment is on fire, up 53% YoY in early 2026, and now accounts for 95% of total revenue.

— Deep Moat:

The test is highly integrated into Electronic Medical Records (EMRs), making it incredibly sticky for healthcare providers.

— Derisked Pipeline:

Unlike speculative, pre-revenue biotechs, $ADPT has a proven commercial product that is already generating hundreds of millions.

2️⃣ WHY IT’S A 10X BY 2030:

To pull off a 10X return, a company needs a massive Total Addressable Market (TAM) and serious operating leverage.

Here is how $ADPT gets there:

— Flipping the Profitability Switch:

The company is targeting positive adjusted EBITDA in 2025 and positive Free Cash Flow by the end of 2026. Once a commercial-stage biotech scales past its cash burn, valuation multiples tend to expand violently.

— TAM Expansion:

Right now, clonoSEQ dominates specific blood cancers. Expanding into broader oncology and immune-medicine applications opens up a multi-billion dollar market.

— Operating Leverage:

As revenue (currently growing at ~35% overall) outpaces operating expenses, the bottom line will swell. If they maintain their high double-digit growth rate through the decade, a 10X valuation shift is entirely plausible.

@HunterAllen4 I know you would like this one😉

5

2

25

3,404

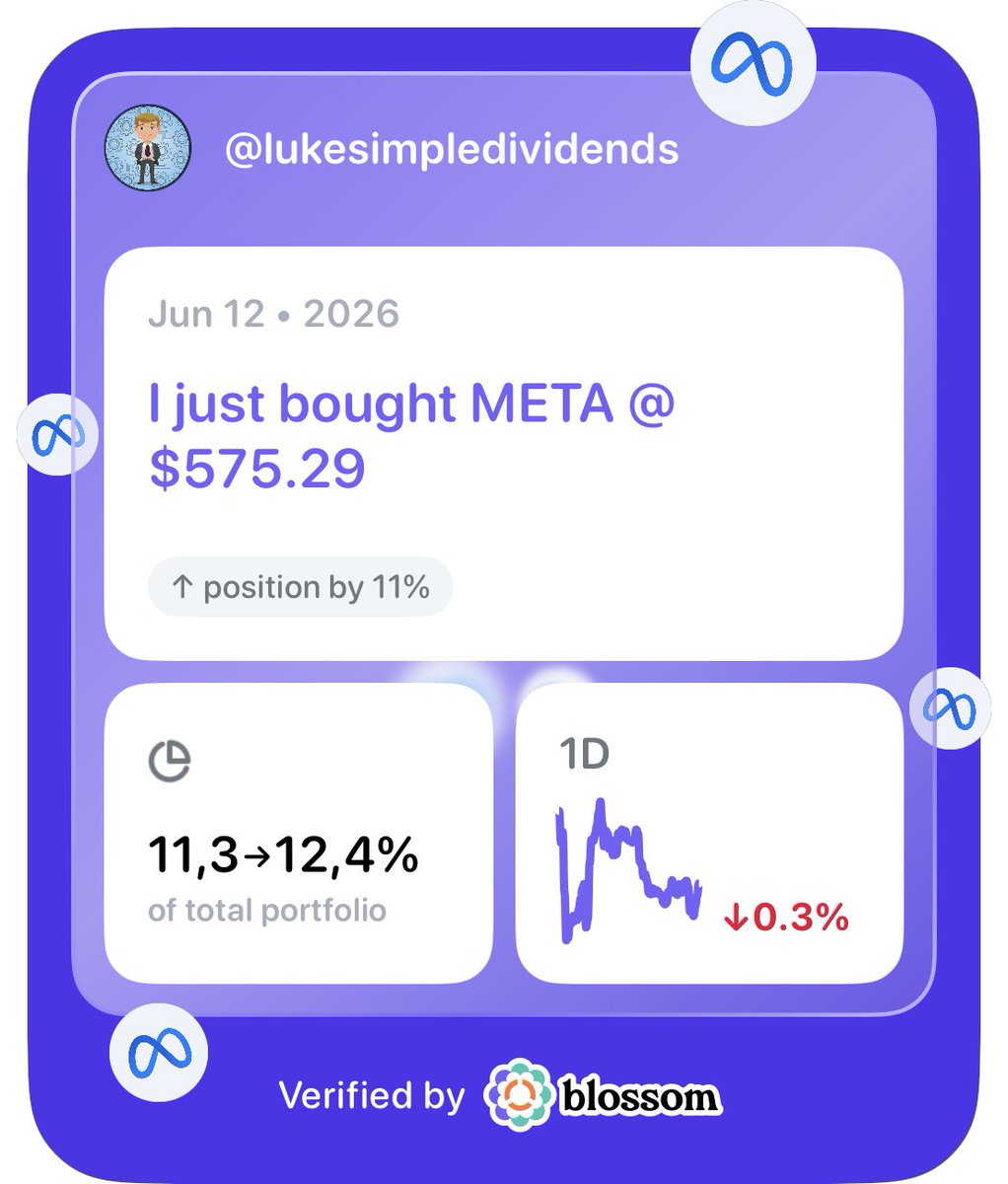

🚨 $META STOCK ANALYSIS 🚨

Out stock analysis in my Substack page!

Go check it💪🏻

open.substack.com/pub/lukesi…

3

6

557

Luke Simple Dividends retweeted

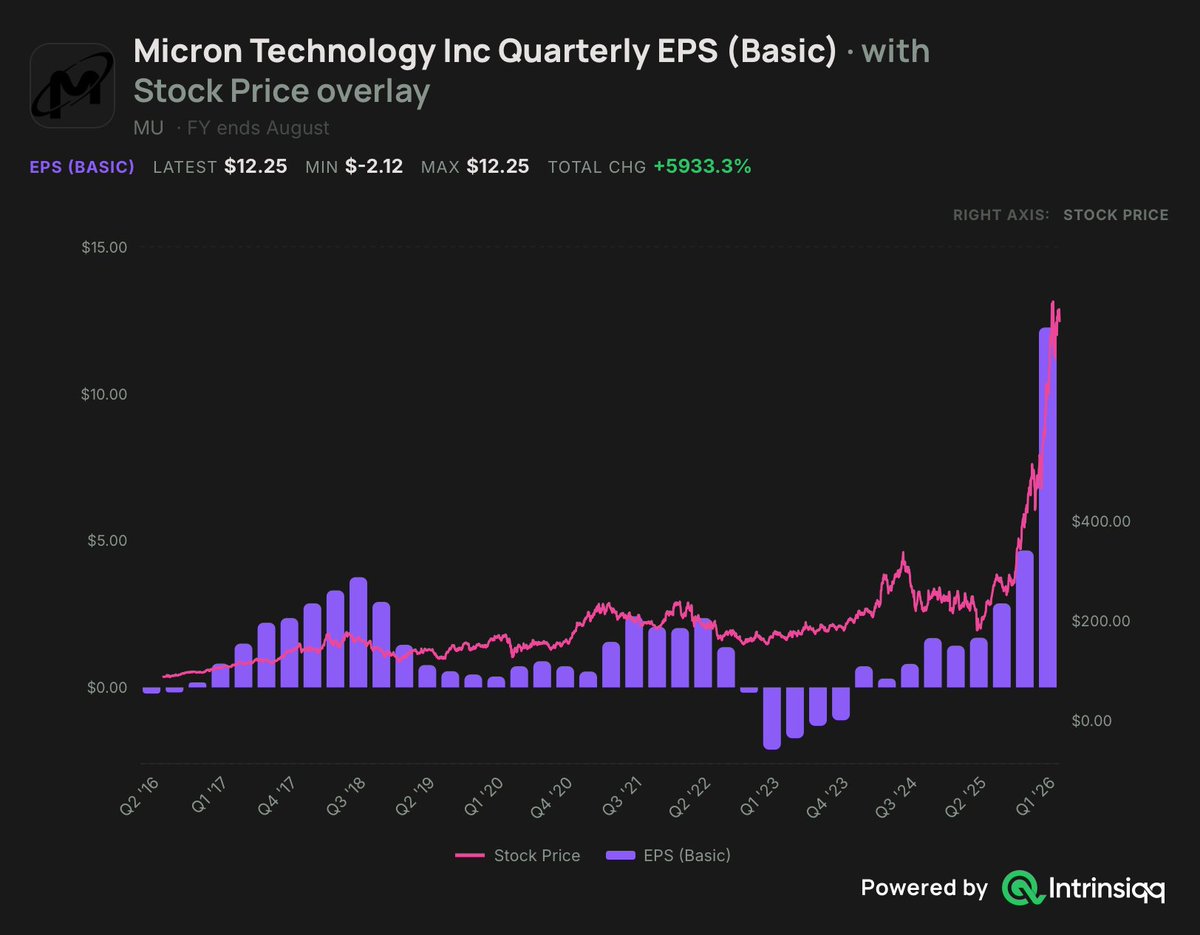

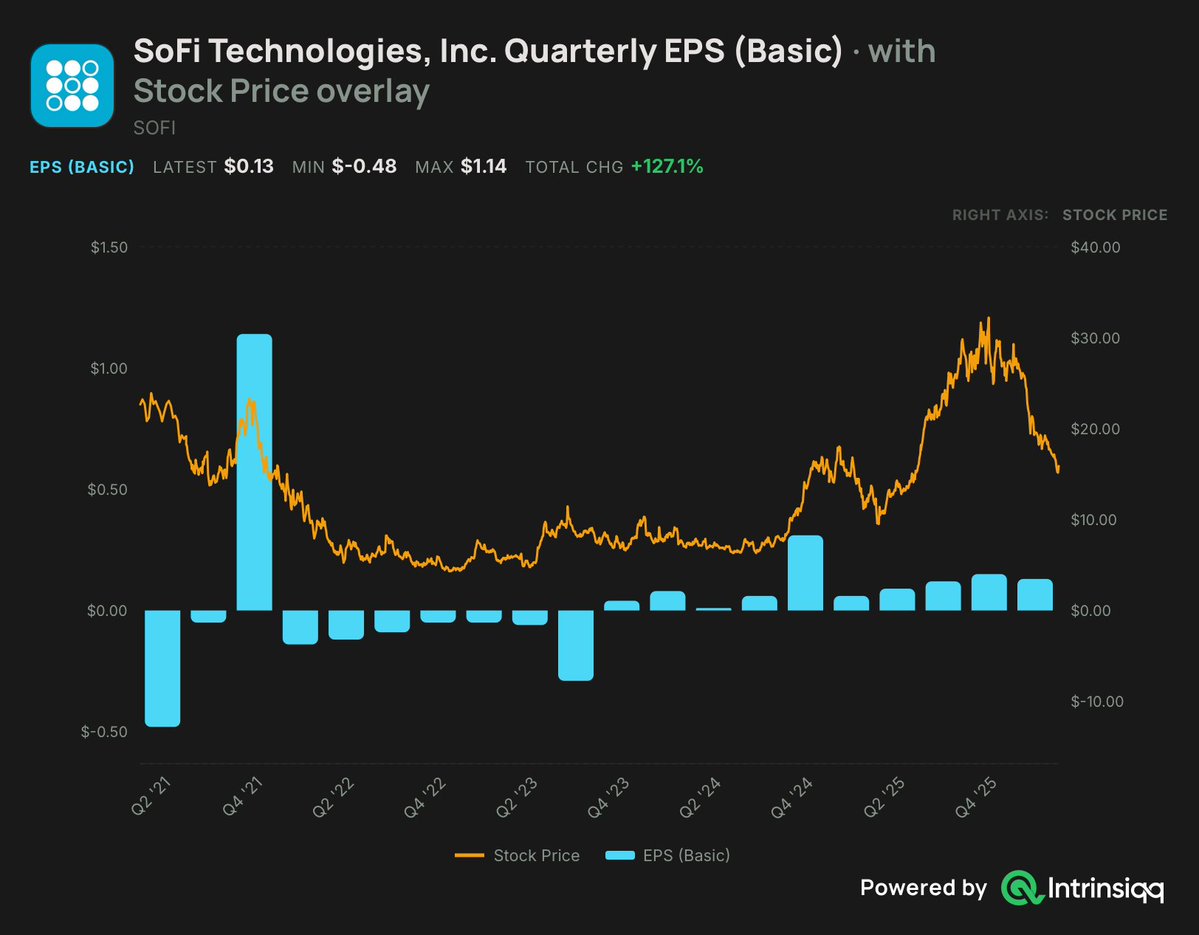

Day 3 of posting $SOFI until hits $50

(Fair value🫢)

EPS Price chart

8

3

77

6,543

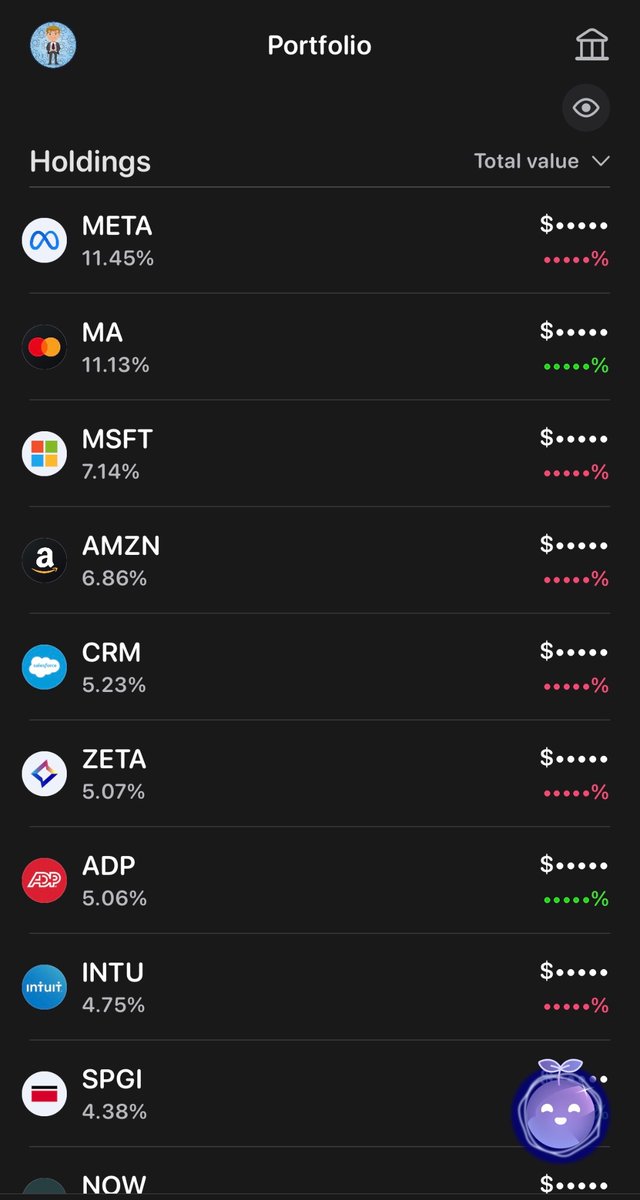

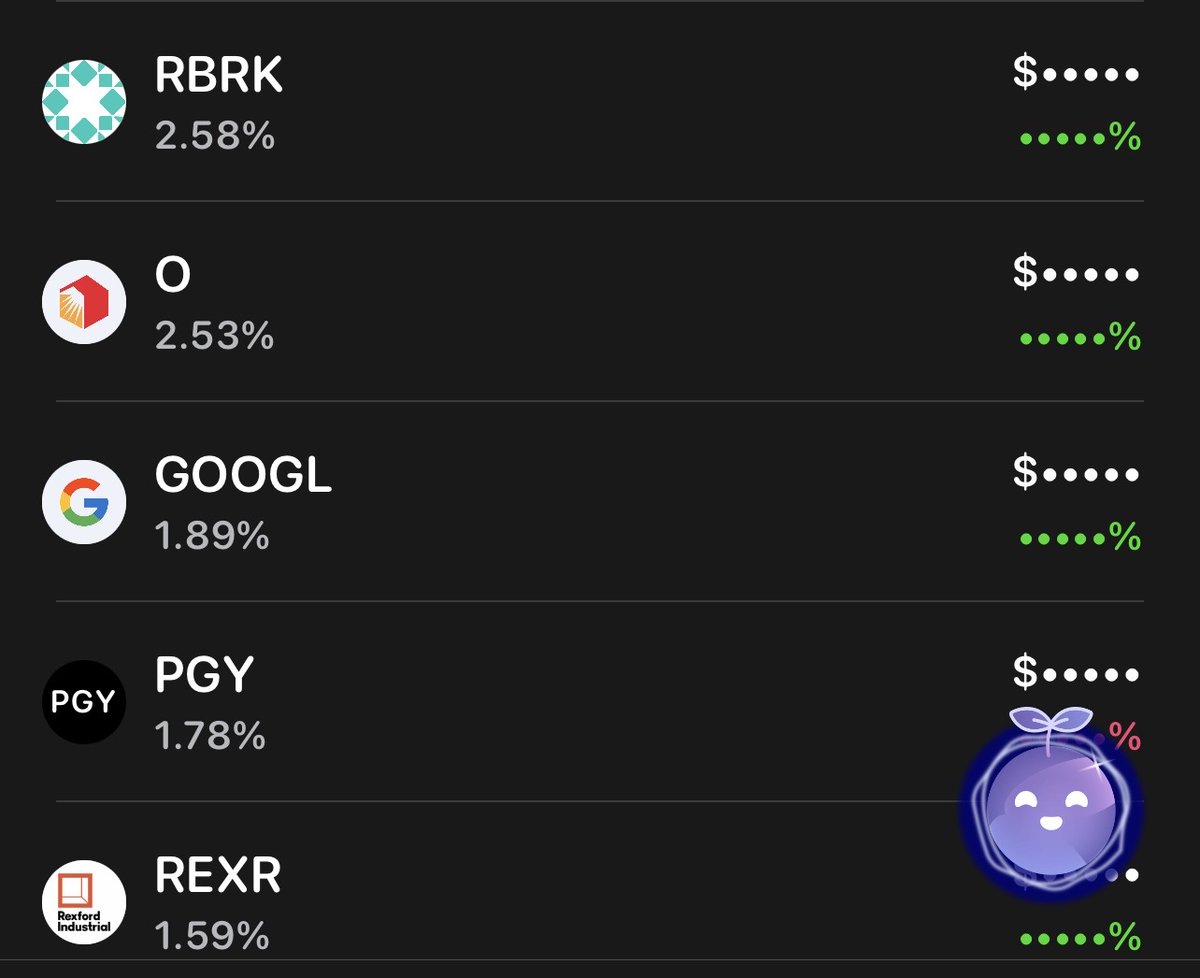

🚨 ROAD TO 100K DAILY UPDATE 🚨

Tot Value: $35,208

Luke Portfolio: ⬆️ 0.15%

S&P500: ⬆️ 0.54%

Nasdaq: ⬆️ 0.59%

Aggregated: ⬆️ 0.08%

🟢 Best performers:

$CELH 2.75%

$ACN 1.65%

$VICI 1.53%

🔴 Worst performers:

$RBRK -4.56%

$ZTS -2.25%

$PGY -2.10%

BUYS:

$META $MSFT $CELH

FOLLOW TO DON’T MISS NEW BUYS 🔥

💰 Track my Full portfolio and live trades in the link in BIO

$META $MA $MSFT $AMZN $CRM $ZETA $ADP $INTU $SPGI $NOW $ACN $VICI $CELH $UNH $NVO $RBRK $O $GOOGL $PGY $REXR $ELF $ZTS $TSM

5

1

6

138