Investor. Posts are not investment advice. Disclaimer: tinyurl.com/44vsnu79

Joined May 2022

- Tweets 92

- Following 74

- Followers 59

- Likes 696

15 Photos and videos

ft.com/content/521d1861-82c5…

Great Chris Hohn article in FT. Two quotes sum it up:

“For Hohn, the key metric for any company is pricing power… He is not dazzled by stratospheric revenue growth like other investors.”

“Chris likes buying global monopolies or duopolies.”

110

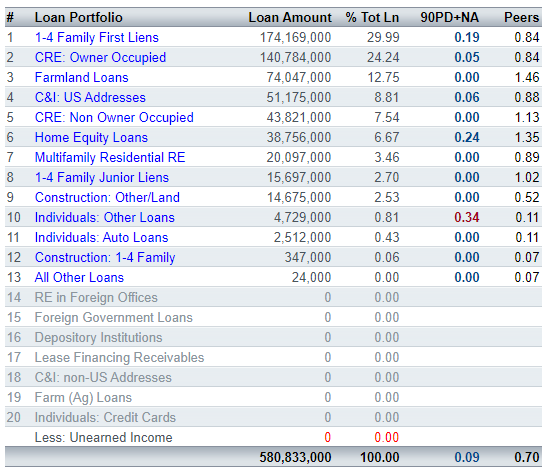

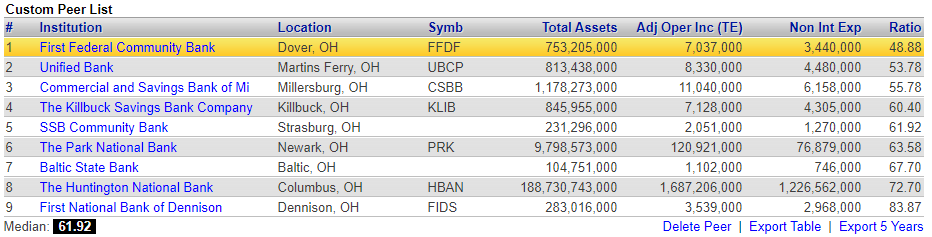

$BLHK Well-run, high-performing bank high growth potentially cheap valuation. Article below:

twentypunchinvestments.com/p…

2

236

MJS retweeted

Feb 28

An acquaintance worked at Berkshire HQ for a decade.

His stories are fascinating.

To protect his identify I’ll just say however focused and intelligent you think Buffett is, multiply it by 10.

22

35

1,089

377,380

Fairlight really summed up outperformance in four points. Go where competition is least, look at ALL available ideas in those areas, and find best relative value. And then insulate yourself from outside noise. Obviously easier said than done but well stated @Fairlight_Cap

2

152

Browning West publicly released their Letter to Board of Dominos Pizza Group PLC. Hopefully releasing letter publicly puts some pressure on $DOM.L management and board to increase share repurchases and stop pursuit of acquiring second brand.

prnewswire.co.uk/news-releas…

3

481

MJS retweeted

13 Jan 2025

You don't need a complicated and smart thesis to make money. The only thing that matters is that you are right. And it's (way) easier to be right on something simple. (2/5)

1

6

81

11,139

MJS retweeted

17 Sep 2024

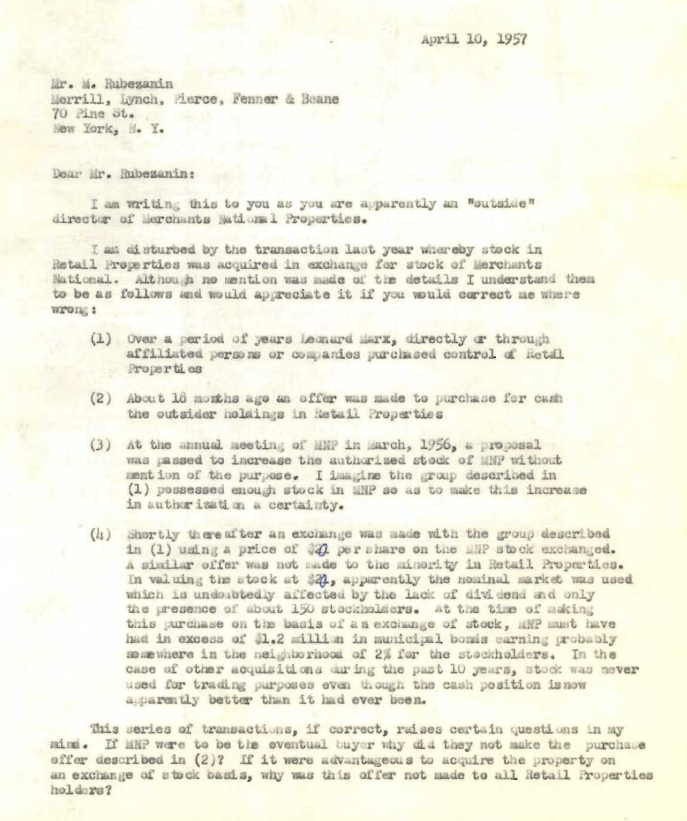

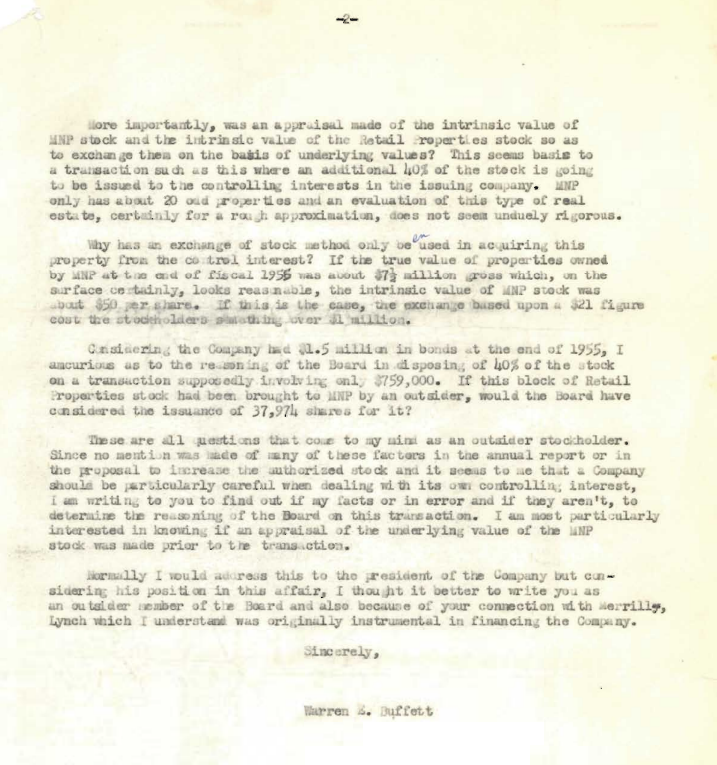

One of the companies I wanted to write about in Buffett's Early Investments (pre-order here: amzn.to/3TvSHSc) was Merchants' National Properties. I couldn't find the right documents so I picked something else. But I did come across this letter from Warren Buffett to an outside director (the document is almost 70 years old, so it's in bad shape). Buffett is questioning an "outside director" (his quotations clearly indicating his skepticism on the director's independence) for exchanging MNP stock at a low valuation to management members who owned Retail Properties, enriching themselves at the expense of minority shareholders.

Young Buffett was far more confrontational with management and boards in the earliest part of his career than is commonly believed.

Buffett sold this stock to Walter Schloss at $14 a share in 1963. Schloss talked about it in this interview (grahamanddoddsville.net/word…) with Jim Grant, when it was worth $553, about an 11% CAGR at the time (not including the additional return from dividends). Buffett sold MNP and a handful of other stocks to Schloss to repay Schloss for selling him his Dempster Mill stock when Warren was in the midst of taking control of that company in 1960. MNP is still publicly traded today over-the-counter.

6

26

155

37,908

MJS retweeted

2 May 2024

Long term returns almost always come down to how shrewdly capital is reinvested.

It helps to have a genius doing it.

2

36

4,842

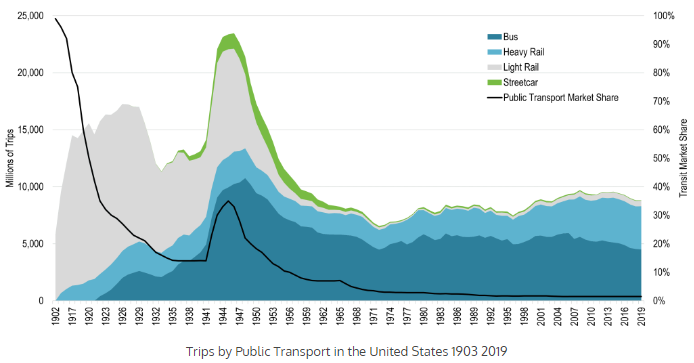

Link to article on Buffett's 1950's Union Street Railway investment $BRK $BRK.A $BRK.B: twentypunchinvestments.com/p…

1

1

274