Joined April 2018

- Tweets 10,553

- Following 3,764

- Followers 12,640

- Likes 20,927

1,205 Photos and videos

Pinned Tweet

The most comprehensive Tokenization & RWA standards report in 2026.

10 platforms. 6 compliance architectures.

Over 1 month of research.

Bookmark for your next flight.

Here's what the data actually shows 🧵

Mar 26

We mapped the full tokenization stack.

Standards, platforms, $620M in RWA collateral, and why T-bills are out, and gold is in.

Onchain allocators are rotating on macro.

A new report with @CredoraNetwork shows what’s actually happening in the RWA stack in 2026 🧵

19

6

92

19,997

RedStone has been a key oracle infra for Morpho's expansion since day 1.

And we will continue to power institutional markets as the platform scales.

By builders, for institutions.

Jun 11

🦋 Congrats to @Morpho on its $175M raise from @paradigm, @a16zcrypto, @RibbitCapital, @apolloglobal, and @vaneck_us.

$9.9B in deposits. Coinbase, Bitwise, and Société Générale already building on the protocol.

3

34

1,709

Canton just closed $355 million led by a16z crypto.

RedStone was the first oracle to launch on Canton in December 2025. Built natively for Daml - the smart contract layer Canton runs on.

The permissioned design means price data reaches only authorized parties, no public exposure - a hard requirement for regulated institutions on the network.

The integration covers the full data stack: live price feeds today, with liquidation intelligence and credit risk infrastructure as the logical next layer, with institutional onchain finance growing more complex.

If you're building on Canton - find us at @TokenizeThisNYC on June 23-25, where tokenized finance discussion will happen.

21

10

118

4,603

Shared my commentary with Decrypt: Kalshi's employer disclosure rule is a useful filter, not a solution.

Self-reported. Only verified when an investigation is triggered. And MNPI rarely travels through a clean employment line - it moves through contractors, advisors, friends, family.

Prediction markets are only accurate because informed participants trade on what they know. There's a meaningful difference between domain expertise and insider information. Broad checks risk removing the former while missing the latter.

New territory for a regulated venue - users should expect the same standards on how their identity and conflict data is stored and shared.

1

17

703

2

357

A Pole moved from Warsaw to Helsinki to study space.

Today his company is worth over €10B. Big congrats @rmodrzewski

ICEYE just raised more than €1B, led by General Atlantic, with Nokia and the Qatar Investment Authority joining. Here's how it came together.

In 2012, Rafał Modrzewski and Pekka Laurila started a research project at Aalto University. The conventional wisdom said radar satellites that can see through clouds and darkness had to be the size of a truck and cost hundreds of millions. They bet it could be done under 100kg.

They incorporated ICEYE in 2014. In January 2018 they launched the world's first SAR microsatellite. Most people in the industry didn't think it would work.

Today ICEYE operates the largest SAR satellite constellation on Earth.

Seven European governments now run sovereign systems built by the company, including Poland.

They're scaling from 50 to 100 satellites a year by 2028.

And the timing says everything about where deep tech is going. Days before SpaceX lists Friday in the largest IPO in history, Europe got its own space champion, started by a founders from Poland and Finland that pursued for years an idea nobody believed.

20

17

165

6,360

RedStone infrastructure has been powering Deel's expansion on Tempo.

Such players don't pick their infrastructure randomly; one needs to keep up to the highest standards.

We're powering the real economy onchain with the best partners.

Jun 9

.@deel just launched a stablecoin wallet for LATAM contractors.

In Argentina, 85% of contractors chose USD over pesos last year. Now those dollar balances can earn yield.

RedStone is the data layer that makes it possible.

8

4

36

1,533

The RWA transformation decade that is happening needs new set of rails to grow at scale safely.

RedStone Settle delivers a critical part of that stack.

It is a process.

Jun 2

Tokenization was supposed to make assets more liquid, but redemption windows of up to 180 days tell a different story.

Liquid Lane fixes the exit layer. RedStone Settle handles tokenized collateral once it's liquidated.

5

2

41

2,235

High signal conversation at RedStone & Coinbase RWA roundtable at @proofoftalk.

The key takeaway: Kelp hack slowed things down, but has not changed the expansion direction.

Running such an event at Louvre Palace is just a pleasure. Thanks @SmartestBeta 🤝

10

1

63

1,722

Midday in Warsaw, afternoon in Paris 🇫🇷

Kicking off @proofoftalk - who should I meet here?

5

2

56

2,080

ElevenLabs Summit in Warsaw with opening speech by president @NawrockiKn 🇵🇱

Couldn’t imagine more majestic venue than the Grand Theater - adequate place to showcase the success of @mati, Piotr and the team.

The new wave of Poland-based scaleups is coming.

5

7

172

4,695

Gnosis Pay got hacked.

Users should watch out as the investigation is ongoing.

Not the best June kick off...

Jun 1

A bug related to the @gnosispay delay module has been discovered. We are investigating & will share updates as soon as possible.

If you are able to withdraw funds from the Gnosis Pay card to your wallet, we strongly recommend that you do that.

Affected users will be reimbursed.

3

1

19

4,360

Coming to Paris tomorrow for @proofoftalk 🇫🇷

Hope there’s still some of it left after the post CL riots…

If you’re coming and want to talk about future of tokenized finance, hit me up!

15

35

921

TokenizeThis around the corner.

Make sure to get your ticket 🤌

May 30

Tokenized equities are no longer a concept.

Join us at @TokenizeThisNYC, June 25.

1

1

18

576

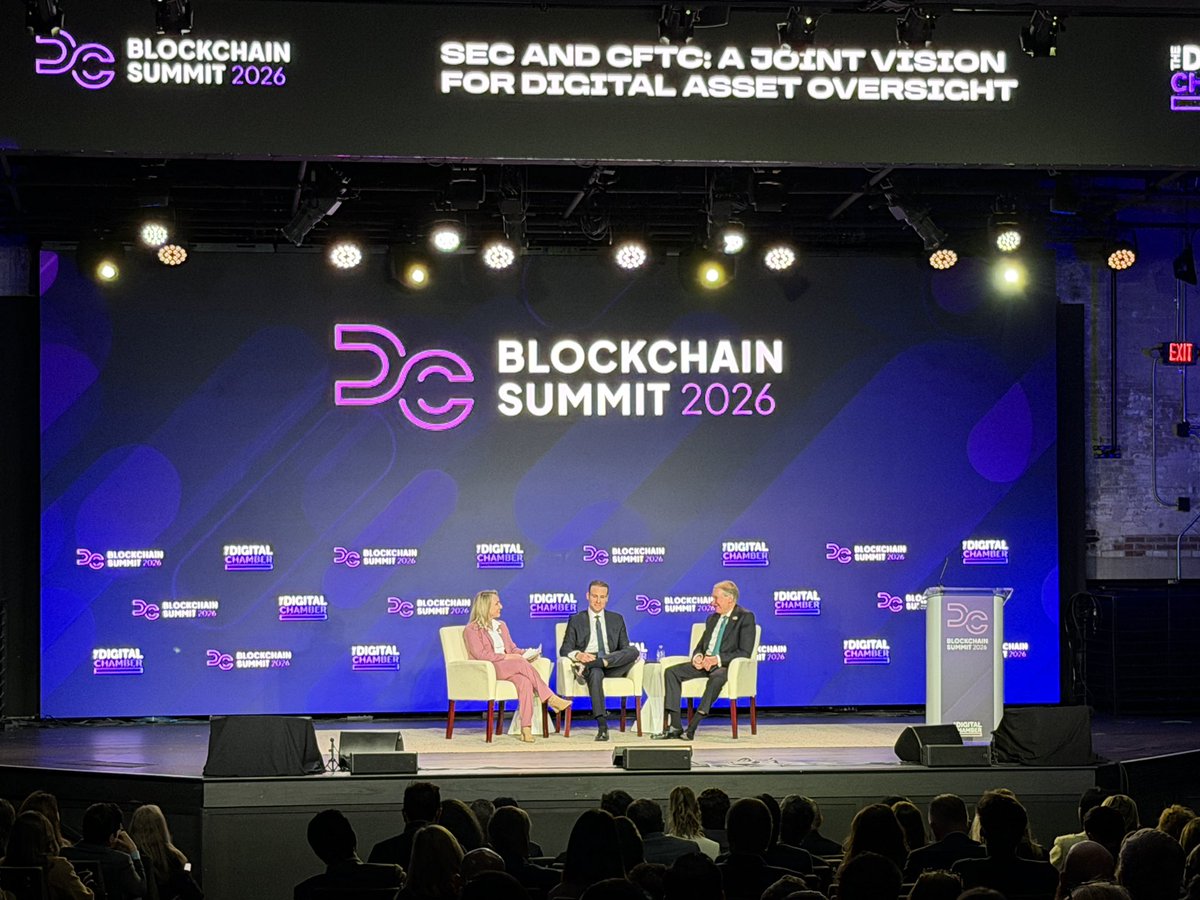

Big day. CFTC Approves First Regulated Bitcoin Perpetual Contract in U.S.

Everyone in Washington at @DigitalChamber's DC Blockchain Summit could sense it's coming.

And that's only just another step.

A historic moment for crypto industry.

Chairman Paul Atkins SEC and Chairman Michael Selig CFTC discussing the joint MoU and plans to work closely together.

2026 will be big.

6

1

22

776

RedStone continues to support the tokenization revolution.

One protocol at a time.

May 28

VBILL is now live on @eulerfinance.

Tokenized U.S. Treasuries can now be used within the Euler ecosystem as onchain collateral.

This marks another step in bringing institutional-grade assets into DeFi.

13

2

34

1,281

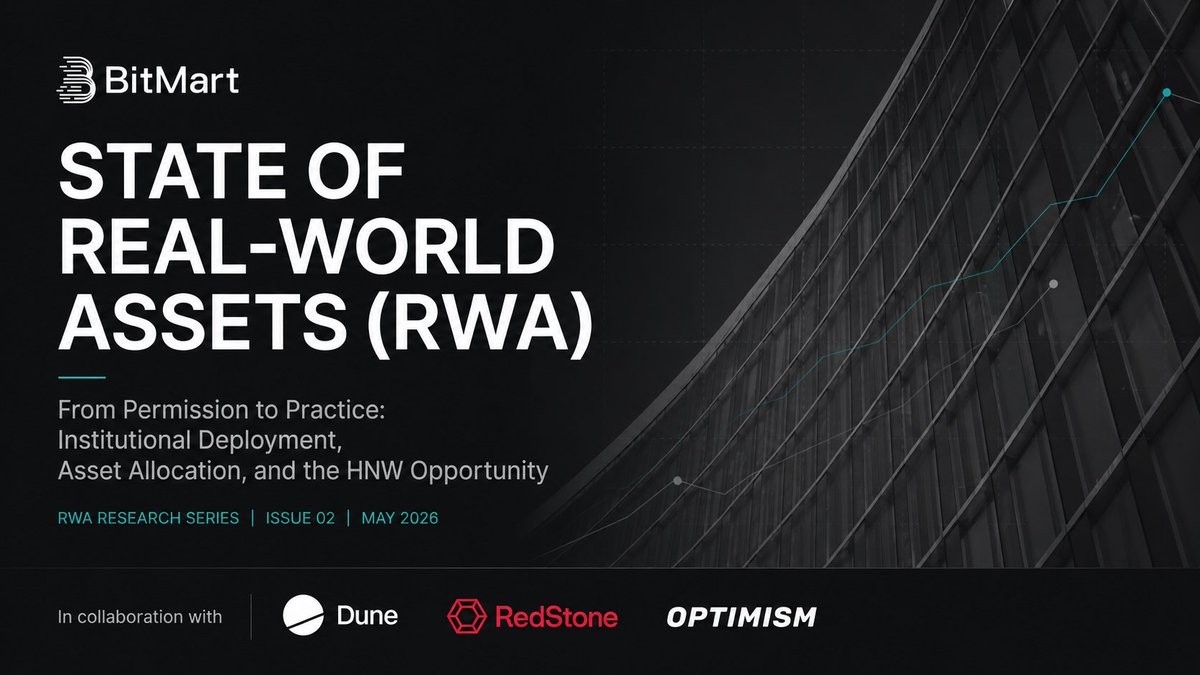

A solid piece of research on the RWA market.

Direction stays the same, but specifics and metrics change constantly.

The decade of RWA growth continues.

May 20

BitMart's State of #RWA Issue 02 is out 🚀

"From Permission to Practice" - we break down how $24.6B in onchain RWA TVL got here, where it's going, and what's still holding institutions back.

Co-authored with @Dune @redstone_defi, and @Optimism

Full report: bit.ly/BitMart-RWA02

5

2

33

1,801

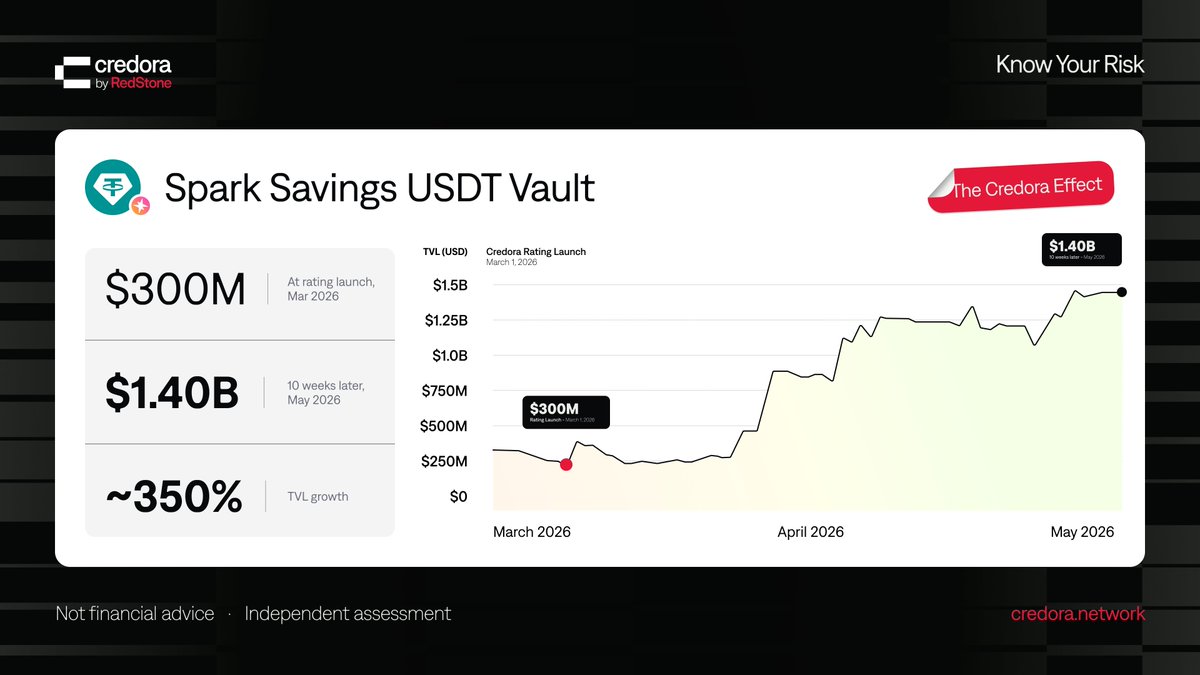

For five years, institutional allocators have been looking at DeFi from the same angle. The yields are interesting. The infrastructure is impressive.

But we cannot defend a position to our risk committee without an independently documented probability of loss.

Spark Savings USDT just ran that experiment cleanly. Same vault, same mechanics, same protocol. The key variable that changed on March 1, 2026 was that Credora published an independently quantified probability of loss. Ten weeks later, TVL went from $300M to $1.40B.

The April 17 stress test made the mechanism legible. The rsETH hack. Institutions needed to know, in real time, whether their Spark position was in scope. The Credora rating document was downloaded 69 times in a single day. Spark held and attracted capital. Comparable unrated vaults on the same protocol lost TVL.

This is not about whether ratings are perfect. Every institutional credit market has spent decades arguing about that. What the Spark data shows is more specific: when capital has to choose between a vault where the risk is on record and one where it is not, it picks the one with the independent verification. Especially under stress, when those decisions have to be taken for billions of dollars.

Two markets are starting to separate inside DeFi. The rated one, where institutional allocation flows when conditions get noisy. And the unrated one, where allocators have to defend why they did not already exit.

Credora is what made that distinction possible onchain. An independent rating, methodology you can read, probability of loss you can cite in a risk memo. The Spark data is a great showcase. That is what institutional capital has been actually waiting for.

7

3

31

1,198

And to browse through rated strategies check out app.credora.network/

1

225

Bloomberg does not cover Polish companies every week.

But for Żabka story is one of the most underrated business case studies in our region, and the incoming CEO just put the ambition on the table.

Build the 7-Eleven of Europe.

Some numbers first.

-> 12,339 stores at end of 2025. PLN 27.2bn revenue ( 14.1% YoY). Net profit up 78.3% to over PLN 1bn. Almost a third of Poland's population lives within 300 meters of a Żabka (no joke, they are everywhere). The company opened 1,394 new locations in 2025 alone.

-> Origin: 1998, Poznań. Mariusz Świtalski, the guy who had already built Poland's largest wholesale network (Elektromis), bet on the country's tradition of small neighborhood shopping and launched a modern version of it. Seven stores in Poznań. By 2001, 100 stores. By October 2005, 1,700.

Then came the private equity baton pass:

2007: Penta Investments

2011: Mid Europa Partners

2017: CVC Capital Partners (just over €1bn)

That 2017 deal is where it gets interesting. Right after closing, CVC and the management team flew to Japan to study Seven & i Holdings firsthand. They came back and re-engineered the company around it. Franchise-first model. Dense urban footprint. Hot food. Mobile app. Autonomous Nano stores. Private label. A tech stack closer to a fintech than a corner shop.

October 2024: IPO on Warsaw Stock Exchange. PLN 6.45bn raised. ~$5bn market cap at debut. Biggest Polish listing since Allegro in 2020. Fourth largest European IPO of 2024.

The 2025 results show the model is working:

Revenue: PLN 27.2bn ( 14.1%)

Net profit: PLN 1.06bn ( 78%)

Adjusted EBITDA margin (Q4): 14.4%

12,339 Żabka stores in Poland

173 Froo stores in Romania ( 188% YoY in year two)

Stated goal: double end-customer sales between 2023 and 2028

Romania is the proof of concept for the European ambition. Żabka entered in May 2024 by acquiring local distributor DRIM Daniel Distribuție FMCG, rebranded the network as Froo, and is already seeing customer traffic per store approaching Polish levels. Estimated market capacity in Romania: ~4,000 locations.

Now the ambition. Tomasz Blicharski, currently Chief Strategy Officer, takes over as CEO on 1 January 2027. He told Bloomberg the long-term goal is to be the convenience leader in Europe. The thesis is sharp: Europe is structurally fragmented, the global players including 7-Eleven do not run unified pan-European operations, and there is no European convenience champion.

There is a gap, and Żabka is the only operator with the franchise machinery, technology, density and balance sheet to fill it.

The optionality is what makes this very perspective:

East vs West is still open.

East = faster consumer growth, lower entry barriers, smaller TAM.

West = larger economies, harder competition, supplier rebuild.

Nano (autonomous stores) gives a low-capex wedge into harder markets.

The digital ecosystem (Maczfit prepared meals, Dietly D2C marketplace, Jush! and Delio eGrocery) extends the surface area to attack each new geography.

A Polish company born in Poznań, ~€1bn buyout in 2017, now a $5bn public company openly chasing 7-Eleven for the European convenience crown.

There are plenty of promising and innovative businesses out of Poland, I'll try to cover some of them this year 🇵🇱

11

9

151

22,315

Read more:

Poland’s leading convenience store chain will prioritize European expansion under its incoming chief executive officer bloomberg.com/news/articles/…

5

1,425