Joined April 2017

- Tweets 5,262

- Following 113

- Followers 9,872

- Likes 29,251

771 Photos and videos

Just watched your macro YouTube post on BTC @PatrickEBoyle. As usual good content.

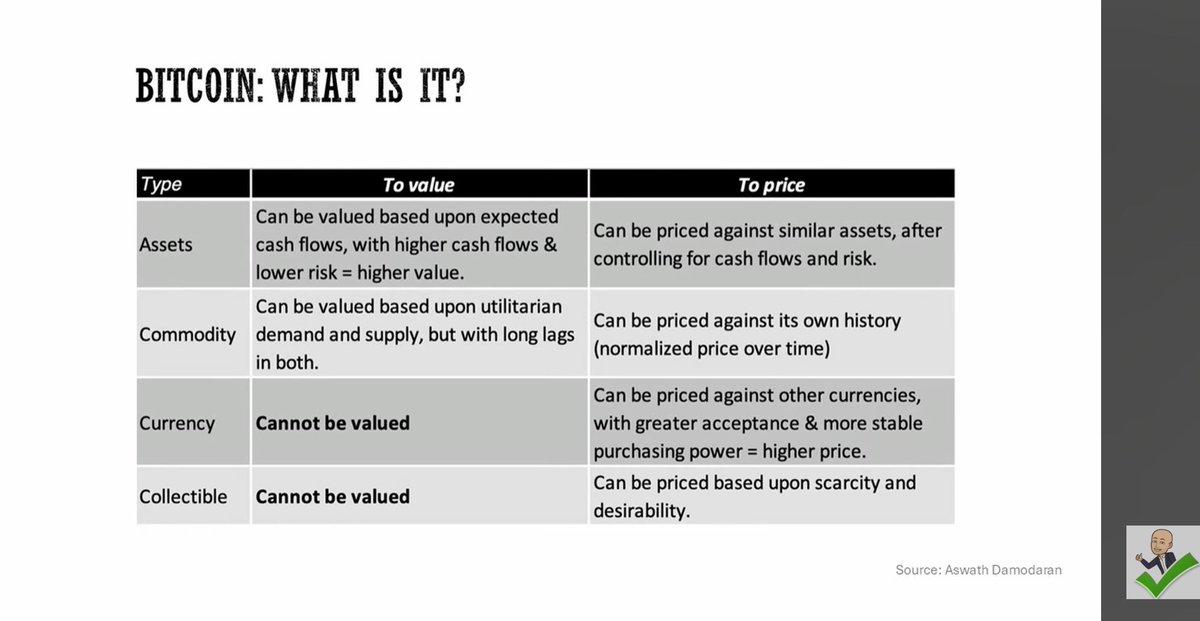

I, however, challenge this table in that currency can indeed be valued (an is) via the fundamentals of the respective economy. This is well established.

Anyway, I enjoy your podcasts.

1

512

8 Jun 2025

Fundamentals-based models offer comfort in approach rigor. This safety blanket is understandable.

But, the market is driven by narrative momentum on global themes. This tide lifts all boats, just in stages (1st/2nd order).

History keeps replaying this way 🤷♂️

1

3

1,150

10 Apr 2025

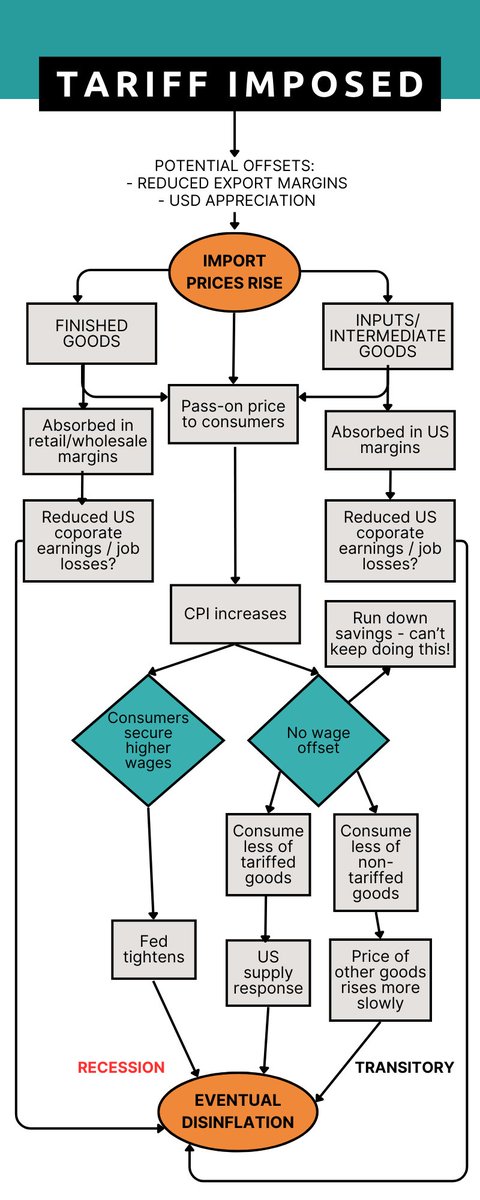

Any macro trading strategy right now with a thesis on a tariff roadmap has to be low conviction by default.

The only strategy I think has legs right now is technicals on volatility (daily price ranges, spot mean reversion, etc).

6

1,375

10 Apr 2025

After a market rout, anything not tariff escalation is a rally driver...remember "no news is good news"

3

1,250

Market Interest retweeted

1 Apr 2025

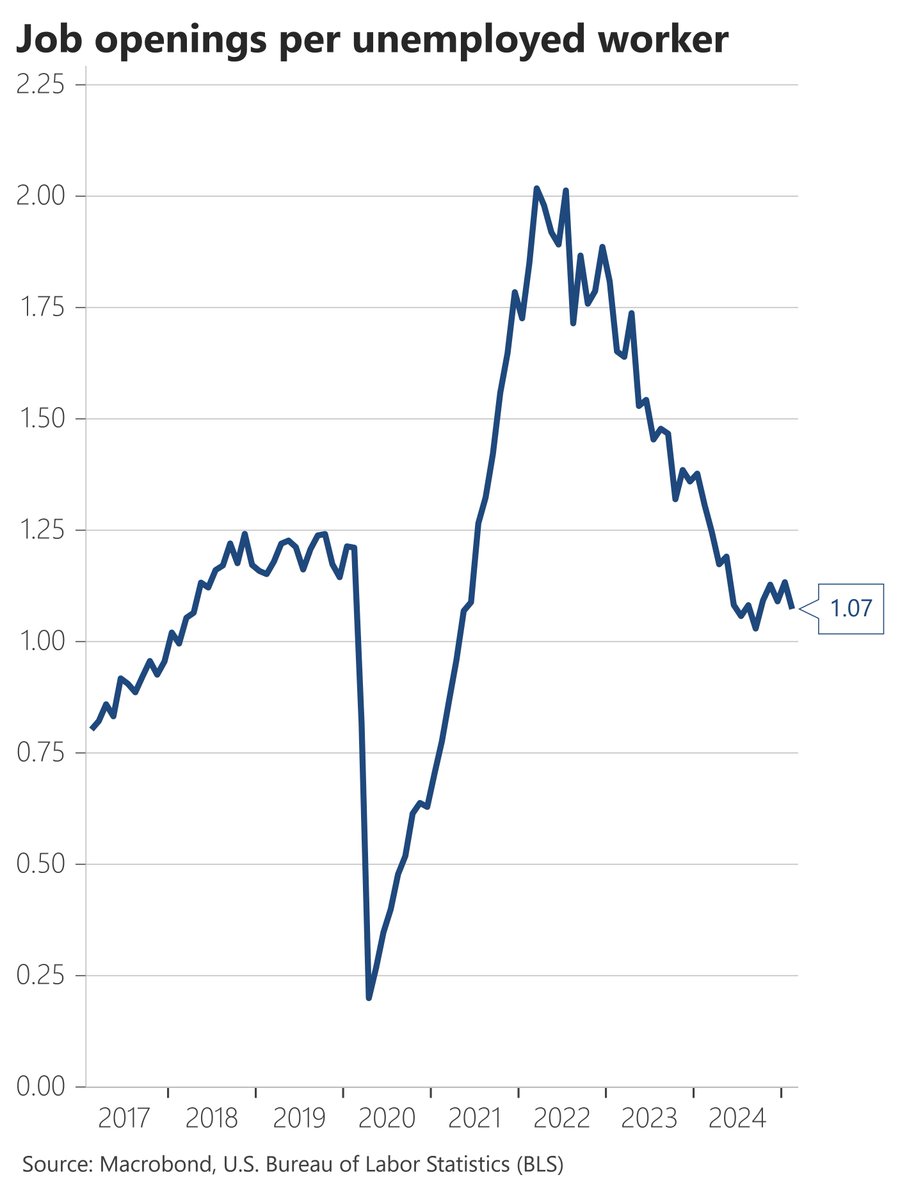

No sign of any hiring reacceleration in the JOLTS series for February.

Job openings continue to grind lower. There were 1.07 openings for every worker counted as unemployed in February, little changed from the recent trend.

Hiring and firing held steady. Quits edged down.

22

147

644

77,128

1 Apr 2025

It's consistent with 2018/19 tariff impact on US inflation in the window before Covid. Those arguing for structurally higher inflation stop halfway through the cause and effect flow, imho.

Also, I think we can discount the wage adjustment path; Covid-nomics was the exception.

31 Mar 2025

many people are saying this is the best summary of tariffs in the world...

1

3

1,185

1 Apr 2025

Good debate here; let me add my two pennies worth:

China is still emerging relative to DM economies. That means there's potential for structural growth to be either higher or maintain a stable run-rate vs DM growth that's on a downward trajectory absent aggressive innovation.

1 Apr 2025

China, despite dominating export markets and being the world's biggest external saver, still racks up roughly $4.5trn (that's dollars, by the way) of new debt every year.

That's 16% of the size of the US economy, every year.

This doesn't scream healthy.

1/

1

885

30 Mar 2025

Very fair points here by Jens.

My take (adding to the below) is that looking at the 2018/19 trade war, I think we can reasonably expect inflation to underperform the upside worry (by markets), and can also expect global mnfg recession 2.0.

The rest of macro is Fed-related.

29 Mar 2025

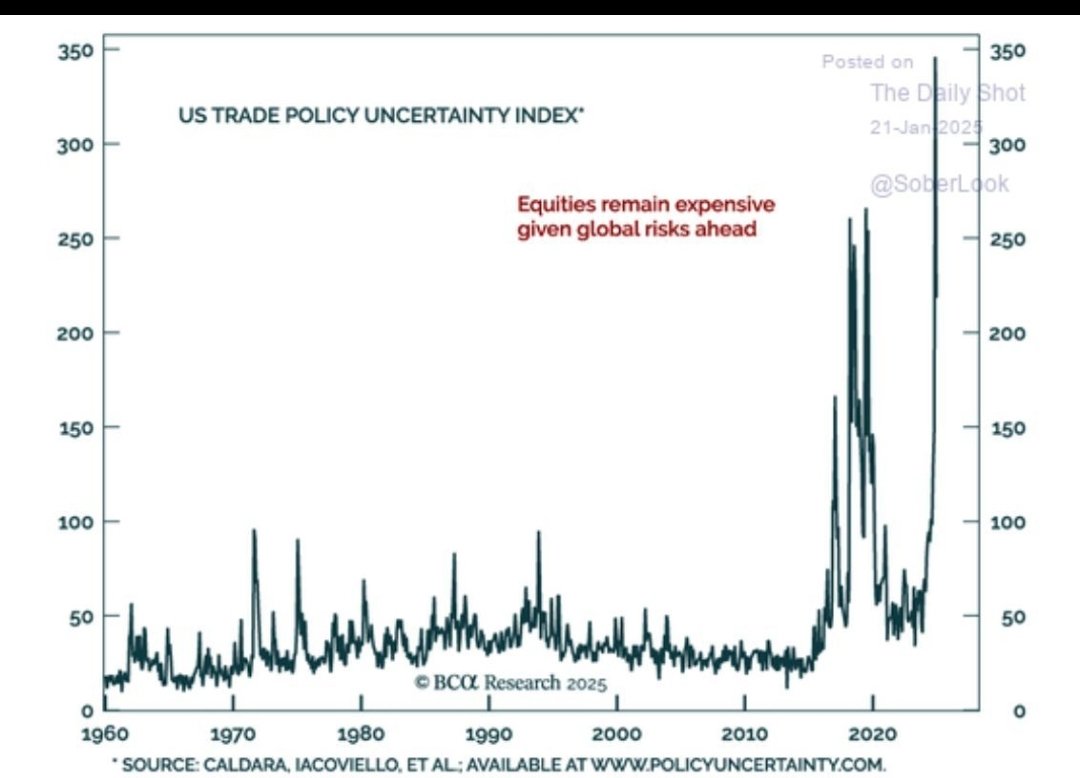

It is hard to predict US tariff policy, but I will say the following:

It is pretty clear that final decisions about April 2 have not been made yet, even with a only few days left to the deadline.

This means that, whatever is announced on April 2, is unlikely to be any final, complete and internally consistent solution.

It is highly likely that whatever is announced (on so-called reciprocal tariffs) will be adjusted and negotiated in coming weeks and months. Meaning that uncertainty will linger.

Further, even if reciprocal tariffs will eventually settle in a steady state of sorts, there are still pending tariffs at the sectoral and country level on many many fronts (pharma tariffs, lumber tariffs, semiconductor tariffs, copper tariffs, agricultural tariffs, China tariffs, Venezuela tariffs)

All told, it is hard too see that we will get resolution on April 2. April 2 may be the biggest day for tariff announcements, among others. But it will hardly resolve the uncertainty.

And the uncertainty will continue to feed into confidence, or lack there-off. And the uncertainty itself will matter for businesses engaged in trade (imports and exports), many of which are in a form a paralysis with respect to hiring and capex. And this is just one transmission mechanism. The other is financial conditions. The US equity market is already dramatically underperforming, and over time, the negative wealth effect will map into consumption, as households will have to normalize their savings rate if their balance sheets are not boosted by asset returns.

And finally this:

Normally, when analyzing economic policy, you can do a mapping from economic pain into a policy response. But here we have a different causality, with economic pain generated directly from the policy itself, and it is not obvious when the pain will be so severe that there will be a policy response. This is a quite unique situation.

I will leave it at that. A pretty important week ahead...

3

1,150

19 Mar 2025

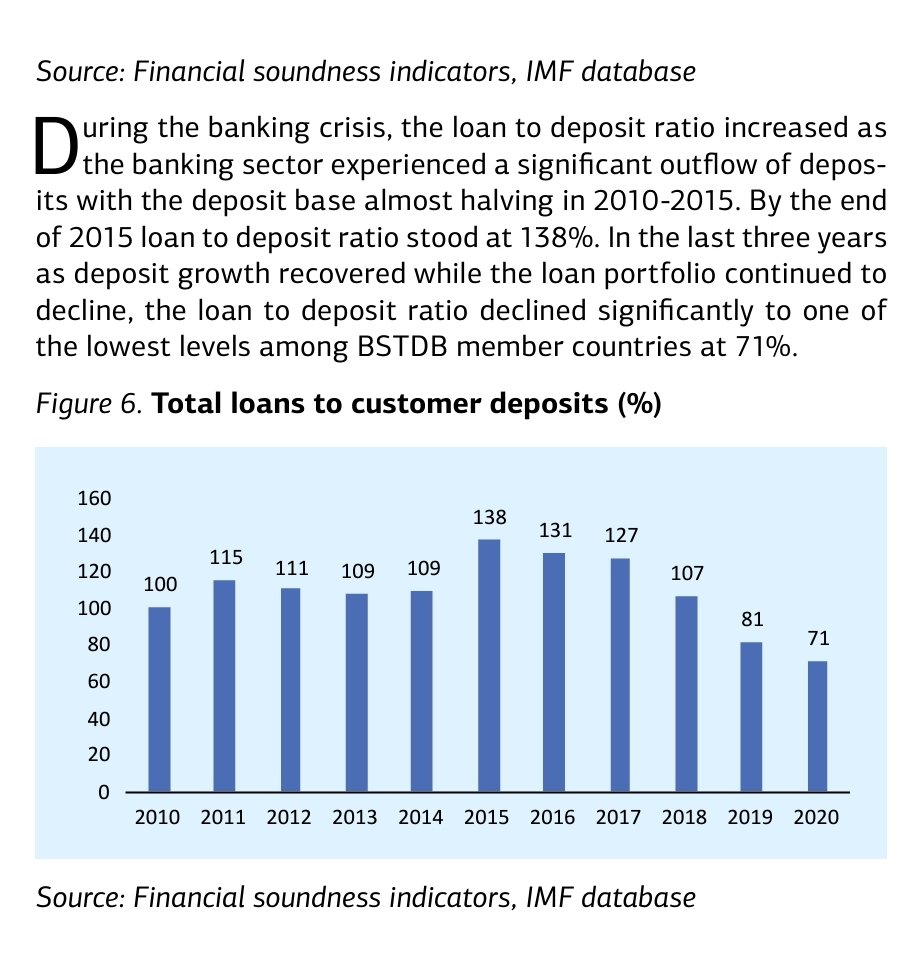

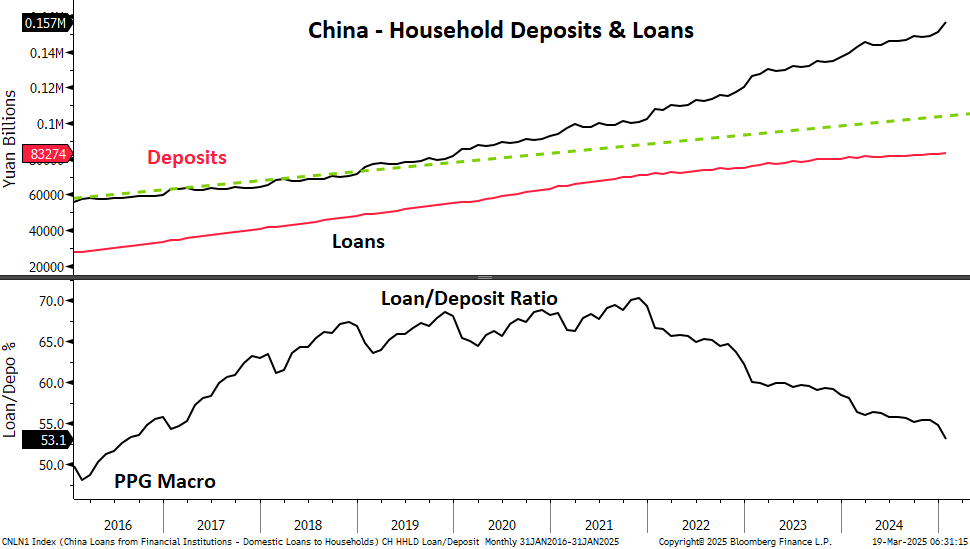

Good point on loan to deposit ratios. The screenshot below is a reminder of what it looked like into and out of the Greece crisis, arguably the diametrical opposite consumer dynamic vs. China.

It would be useful to see recent global stats on this.

The problem is that wealthier Chinese have most of their money in real estate and have suffered big losses.

In turn, they become more conservative with their savings.

Low rates are not boosting borrowing. They are increasing savings.

1

3

1,276

19 Mar 2025

...and historically, deep rate cuts are a result of bad news (forced hands). In the last ~20yrs, I don't remember many (if any) examples of CBs cutting a decent amount purely on soft landing dynamics.

It's typically been a few cuts, pause, then exogenous drivers of deeper cuts.

19 Mar 2025

Central banks can cut because of good news or bad news. The window for ‘good’ cuts is closing due to new inflation risks. (And it's not clear the "dots" show this plot turn).

“Probably for the next six months, I would expect the Fed to be watching and not doing very much."

3

1,008

12 Mar 2025

What was the explanation offered? Cheers

1

1,060

7 Mar 2025

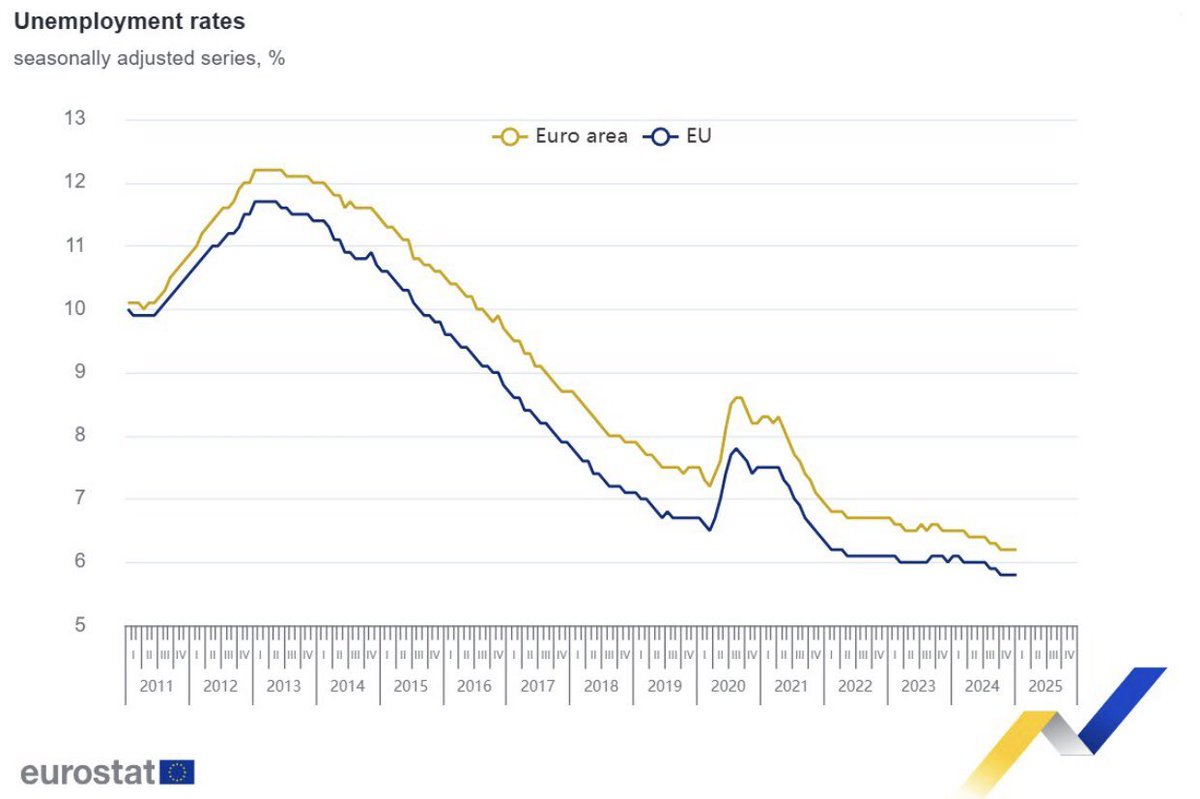

For what it's worth, structural unemployment rates differ by country, as with potential GDP and other measures. For example, a recession for China is low [positive] GDP growth, whereas for most countries, it's actual negative % changes.

7 Mar 2025

6% unemployment rate would be considered recessionary level in the US

1

667

28 Feb 2025

This measure already exists; final sales to domestic purchasers.

Separately, outside of nationalisation, moving large sections of the private sector under a government umbrella is highly unlikely.

A more accurate measure of GDP would exclude government spending.

Otherwise, you can scale GDP artificially high by spending money on things that don’t make people’s lives better.

For example, you could shift everyone who is building cars to working at the DMV. That would result in no cars and a much worse standard of living, but GDP would appear to be the same!

Community note

The United States already reports a measure of GDP excluding government spending, called "Value Added by Private Industries (VAPI)". It currently accounts for 88.7% of US GDP and has steadily risen as a share of GDP since 2009, under both Obama and Biden as well as Trump:

fred.stlouisfed.org/series/VAPI

fred.stlouisfed.org/series/VAPGDPPI

4

716

25 Feb 2025

Ah, the "eventually hypothesis" that markets almost never buy and require Fed intervention to cap downside.

2

2

850

25 Feb 2025

This communication duality is one thing CBs have managed to keep constant in the last 20yrs, along with inflation targeting.

25 Feb 2025

Classic joined-up thinking from that lot in Frankfurt...within 4hrs of each other...

*ECB RATES DEFINITELY STILL RESTRICTIVE: STOURNARAS TO POLITICO

*ECB'S SCHNABEL: CAN'T SAY WITH CONFIDENCE POLICY IS RESTRICTIVE

2

639

25 Feb 2025

Just wondering if 1) tech dominance and 2) AI themes would naturally result in the below distributions?

25 Feb 2025

2

922

25 Feb 2025

Why does long bitcoin feel like an intrinsic short vol position?

697

25 Feb 2025

Over recent years, #gold has rallied with:

1) rising real yields

2) falling real yields

2) strong dollar

3) rising geopolitical tension

4) easing geopolitical tension

4) because of momentum

That's the pin-the-tail-on-the-donkey for gold, where narrative turnover is high. 🤷♂️

5

594

24 Feb 2025

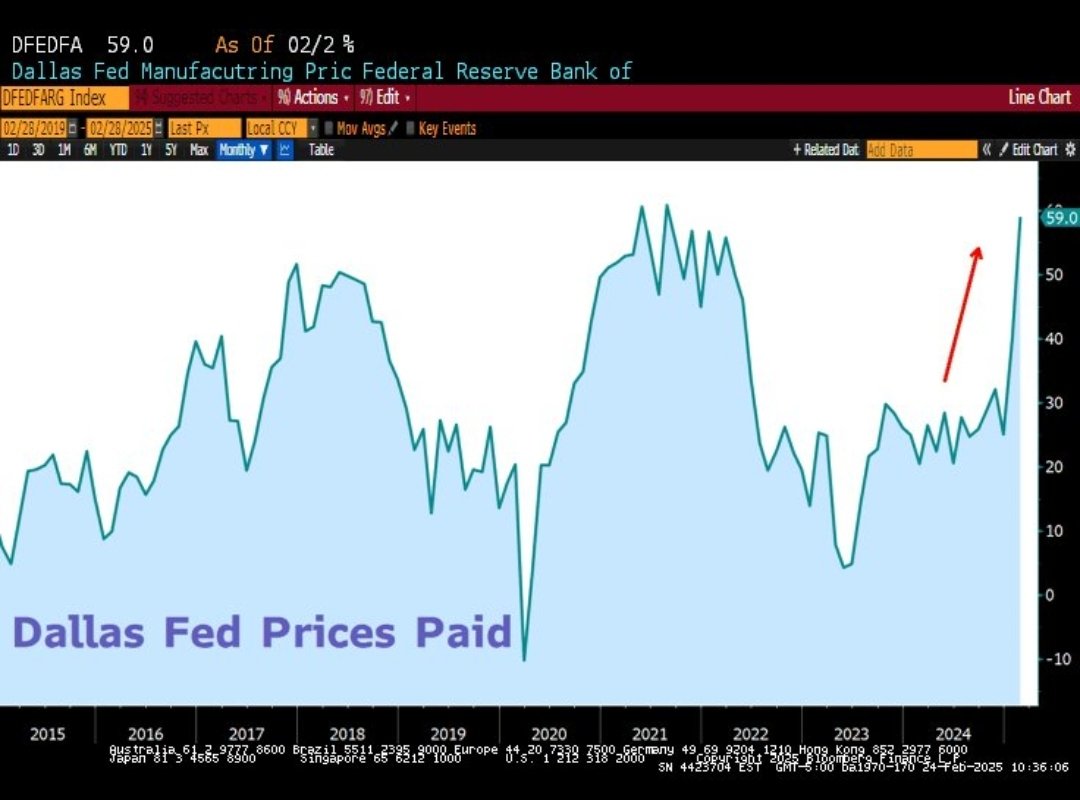

For me, this reading is at odds with macro momentum and the overall Fed backdrop. Such spikes are consistent with a supply-side shock (I can't imagine a demand-pull shock outside of helicopter money).

What's driving this?

H/t @Convertbond

1

502