Long / short trading with objective of beating $SPY in good times and protecting capital in bad. NOT financial advice. Subscribe for free at minervacap.us

Joined September 2023

- Tweets 8,099

- Following 231

- Followers 3,118

- Likes 6,129

3,472 Photos and videos

Pinned Tweet

May 14

Excited to reach 3,000 followers! Thanks to all of you for your support. ❤️

I've updated my pinned tweet to reflect my current trading process so that you can better understand my trade ideas. Let me know if you have any questions/comments!

x.com/MinervaCap/status/2055…

8

1,954

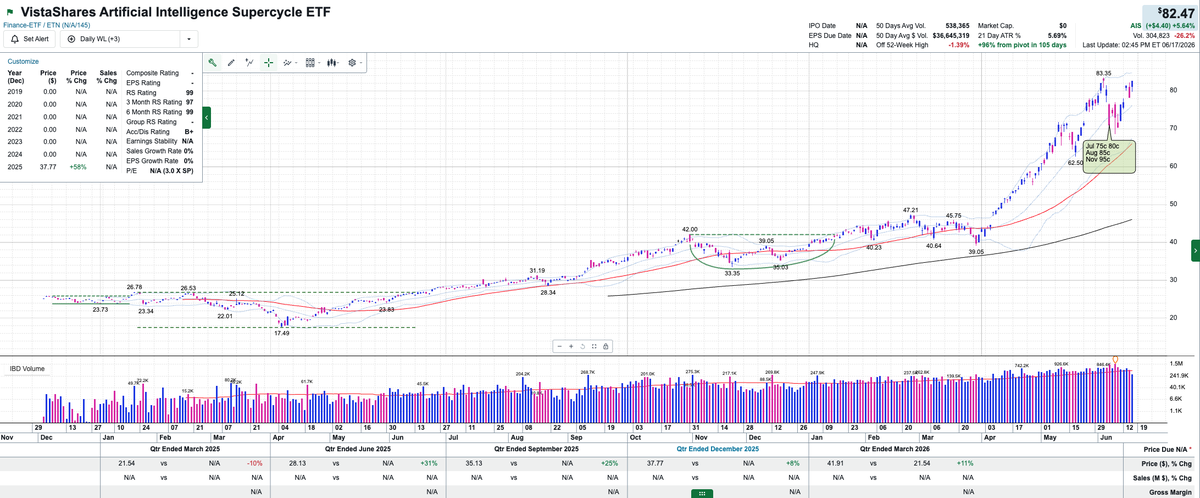

The AI trade (represented by the best-performing ETF $AIS) seems to like the new Fed Chair - about to break to new ATHs. Several of my calls bought during the dip doubled (limit orders to sell half went thru).

2

178

Minerva Capital retweeted

Fed dot plot was more hawkish BUT ...

In December, they projected 2.5% core PCE for 2026, and median FFR of 3.4%

"Real FFR" (w/ core PCE): 0.9%

March

Core PCE: 2.7%

Median FFR: 3.4%

Real FFR: 0.7%

June

Core PCE: 3.3%

Median FFR: 3.8%

Real FFR: 0.5%

Policy getting easier 🤔

4

5

14

2,221

Minerva Capital retweeted

19h

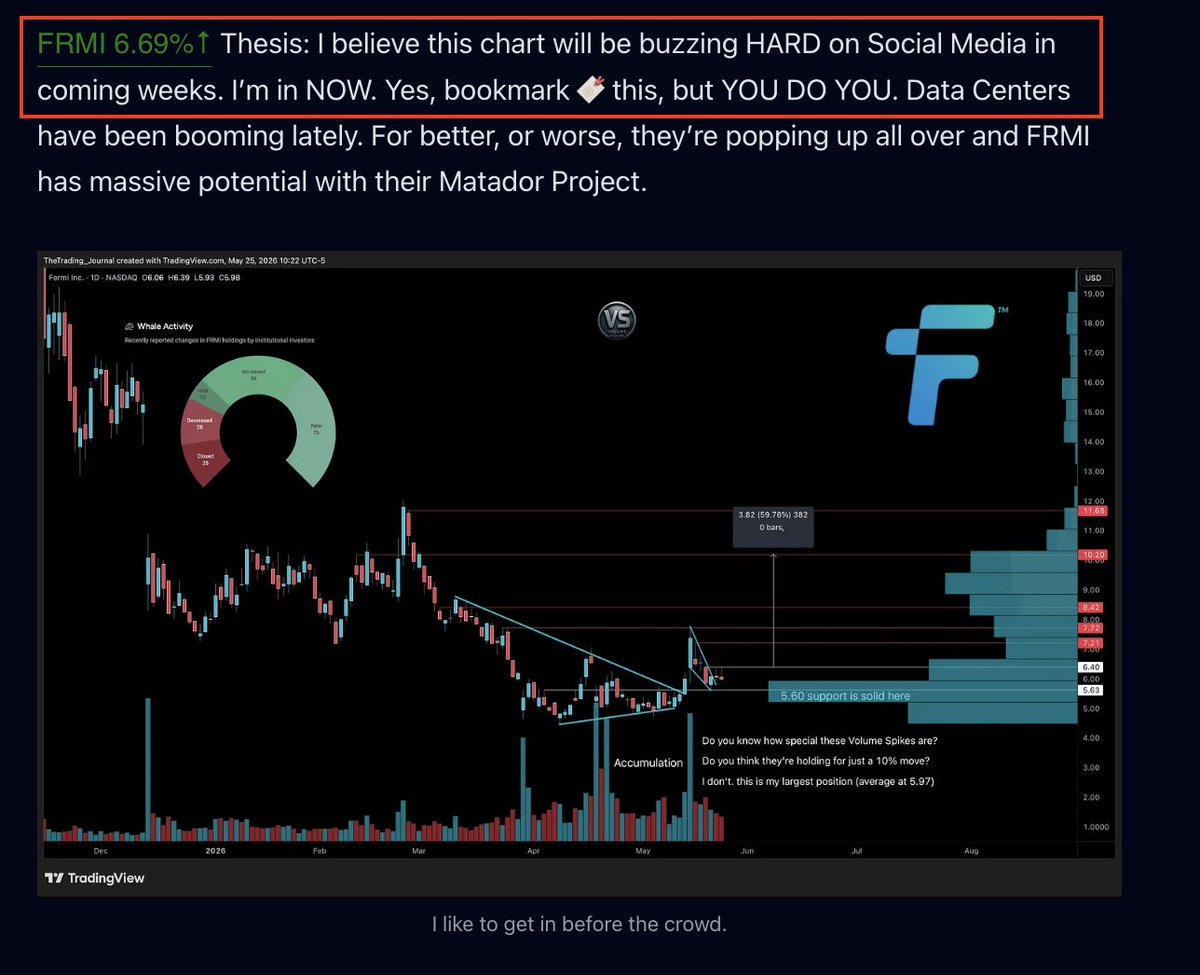

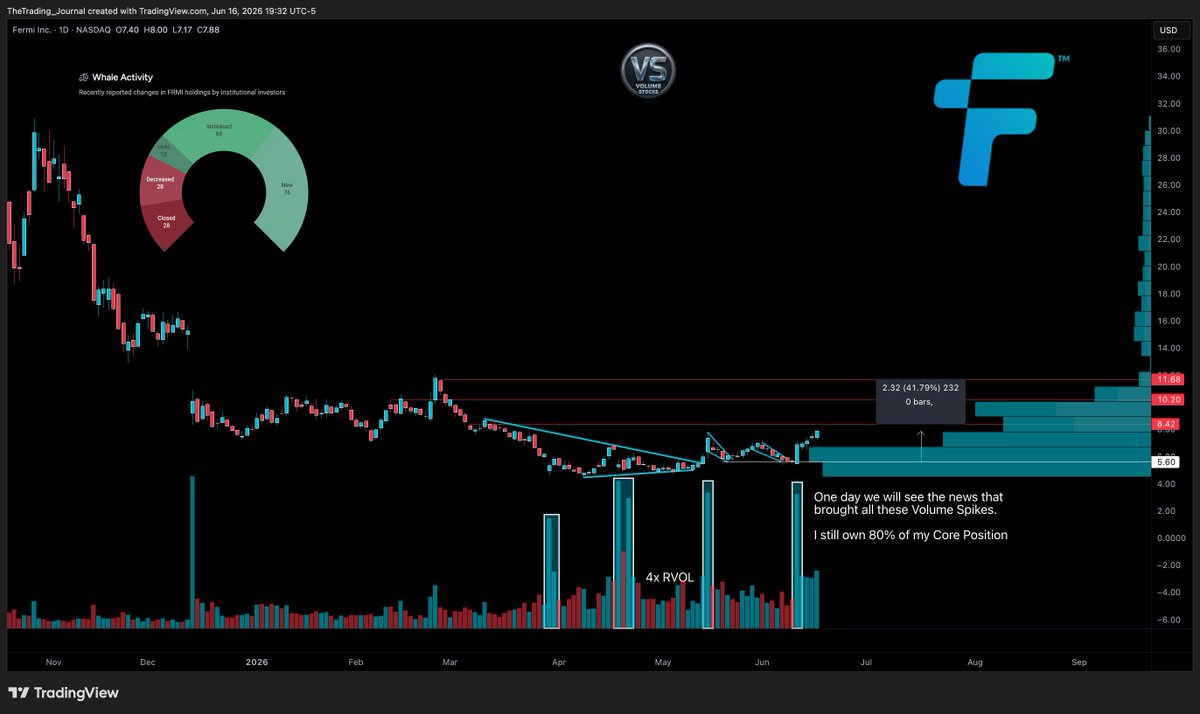

$FRMI "Project Matador"

This is making a push in pre.

⦿ Fermi is positioning itself as one of the few players that could actually deliver gigawatts of clean, firm power on a hyperscaler timeline.

Here is some more context. Trump's name is all over this document.

nrc.gov/docs/ML2516/ML25169A…

There's a lot to like here.

I've loved the accumulation.

Historic Regulatory Milestone:

⦿ They hold the only active Combined Operating License Application (COLA) for large light-water reactors in the United States in more than 15 years.

⦿ The NRC has accepted parts of their application and placed them in a fast-track environmental review pilot program.

⦿ Massive Scale & Timing: Project Matador aims for 4 AP1000 reactors (roughly 4.4 GW nuclear) as part of a larger 11–17 GW private power campus for AI/hyperscalers.

⦿ This is one of the most ambitious nuclear data center projects in the country right now.

Partnerships with top-tier players

⦿ like Hyundai E&C and Doosan Enerbility (proven nuclear builders).

⦿ Significant financing commitments already secured.

Non-nuclear power infrastructure (gas, etc.) is already under construction, with first power targeted for 2026.

⦿ Heavy political branding (Trump name) alignment with current administration priorities on energy dominance and AI infrastructure.

⦿ Market Tailwinds: Explosive AI data center demand means behind-the-meter nuclear power is extremely valuable.

1

1

9

1,541

Minerva Capital retweeted

Jun 15

Energy could be a "source of real underperformance" in the months ahead.

@MarkNewtonCMT of @Fundstrat tells @RemyBlaireNews healthcare and financials are his top picks, with $NKE "starting to finally show some evidence of rallying."

9

33

8,008

Jun 17

2

301

Jun 16

1

357

Jun 16

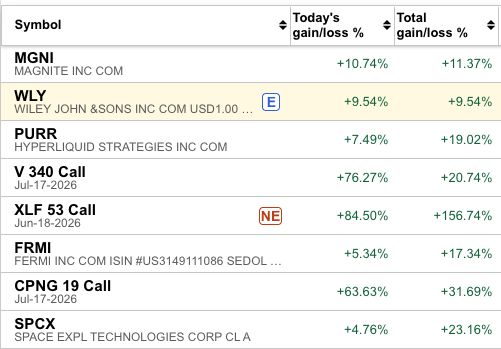

$WLY crashed on good results. I went long on VWAP reclaim vs LOD. NFA

x.com/Finsee_main/status/206…

Jun 16

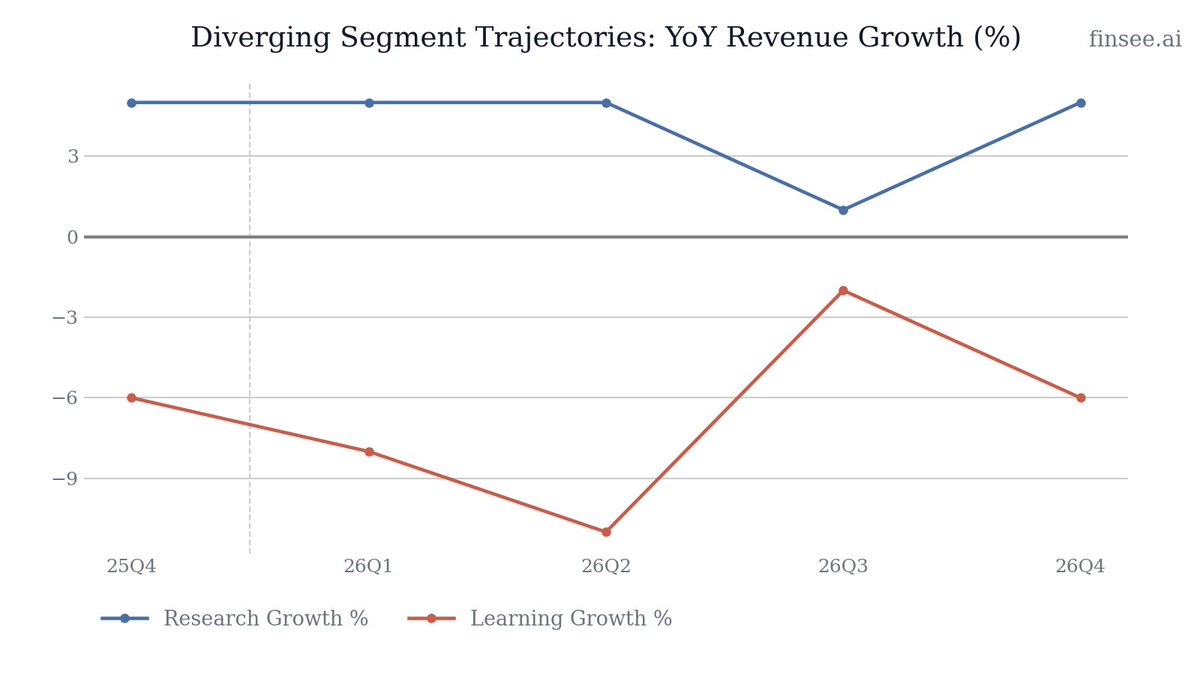

$WLY Q4 2026 earnings: Record Margins and AI Momentum Eclipse Learning Segment Drag

Wiley capped off a strong FY26 with massive profitability improvements, driving Free Cash Flow up 55% to $195M. While total revenue was flat due to an ongoing contraction in the Learning segment, the core Research business delivered stable 5% growth. AI revenue hit $49M, and aggressive cost cuts expanded Adjusted EBITDA margin by 480 bps in Q4 to a robust 33.2%. Management enters FY27 with high confidence, predicting further margin expansion and EPS growth, bolstered by the Emerald Publishing acquisition, despite acknowledging short-term cash flow dilution from the deal.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐏𝐫𝐨𝐟𝐢𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐁𝐫𝐞𝐚𝐤𝐭𝐡𝐫𝐨𝐮𝐠𝐡 — Restructuring and the technology transformation are yielding massive operating leverage. Q4 Corporate Expenses dropped 21%, pushing the consolidated Adjusted EBITDA margin up to an impressive 33.2% from 28.4% a year ago.

• 𝐀𝐈 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐢𝐬 𝐒𝐜𝐚𝐥𝐢𝐧𝐠 — Total AI revenue reached $49M ( 23%), with lifetime revenue crossing $110M. Wiley is successfully transitioning from one-off LLM training licenses to recurring corporate AI subscriptions.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐋𝐞𝐚𝐫𝐧𝐢𝐧𝐠 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐂𝐡𝐫𝐨𝐧𝐢𝐜 𝐋𝐚𝐠𝐠𝐚𝐫𝐝 — The Learning business shrunk another 6% in Q4 and 7% for the full year. Macro headwinds, soft retail channels, and falling computer science enrollments show no signs of reversing.

• 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐃𝐢𝐥𝐮𝐭𝐢𝐨𝐧 𝐟𝐫𝐨𝐦 𝐀𝐜𝐪𝐮𝐢𝐬𝐢𝐭𝐢𝐨𝐧 — The Emerald Publishing acquisition, while strategic for content scale, will dilute FY27 Free Cash Flow by $15M and push CapEx higher ($80M vs $65M in FY26).

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. Management is executing flawlessly on the variables they can control: costs, margins, and AI integration. The structural profitability improvements heavily outweigh the top-line drag from the legacy Learning business.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢🟢 𝐀𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐯𝐞 𝐌𝐚𝐫𝐠𝐢𝐧 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐲 𝐏𝐚𝐲𝐬 𝐎𝐟𝐟

Accelerating margin expansion is the defining story of FY26. Full-year Adjusted EBITDA margin climbed 220 bps to 26.2%, and Q4 alone saw a 480 bps jump to 33.2%. This wasn't accidental—it was driven by a 21% reduction in Q4 unallocated Corporate Expenses, fueled by a multi-year technology transformation and strict restructuring discipline. FY27 guidance suggests this trend is stable, targeting 26.5% to 27.5% margins.

🟢 𝐀𝐈 𝐓𝐫𝐚𝐧𝐬𝐢𝐭𝐢𝐨𝐧 𝐟𝐫𝐨𝐦 𝐋𝐮𝐦𝐩𝐲 𝐭𝐨 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠

AI revenue grew 23% to $49M in FY26. More importantly, management noted that 'recurring revenue is rapidly scaling'. Landmark partnerships with IQVIA and OpenEvidence in healthcare, alongside new corporate customer signings, are shifting Wiley's AI model from unpredictable Wave 1 LLM training deals to high-margin, predictable Wave 2 subscription knowledge feeds.

🔴 𝐋𝐞𝐚𝐫𝐧𝐢𝐧𝐠 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐑𝐞𝐦𝐚𝐢𝐧𝐬 𝐚 𝐒𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐚𝐥 𝐃𝐫𝐚𝐠

The Learning segment continues to bleed, posting a 6% revenue decline in Q4 and 7% for the full year. Management blames 'macro headwinds and retail channel softness,' but the consistent downward trajectory suggests deeper structural issues, such as changing academic enrollment patterns and intense competitive pressures. This segment limits overall company top-line growth.

🟢 𝐄𝐦𝐞𝐫𝐚𝐥𝐝 𝐏𝐮𝐛𝐥𝐢𝐬𝐡𝐢𝐧𝐠 𝐀𝐜𝐪𝐮𝐢𝐬𝐢𝐭𝐢𝐨𝐧 𝐀𝐝𝐝𝐬 𝐒𝐜𝐚𝐥𝐞, 𝐇𝐢𝐭𝐬 𝐍𝐞𝐚𝐫-𝐓𝐞𝐫𝐦 𝐂𝐚𝐬𝐡 [NEW]

Wiley acquired Emerald Publishing to increase its scale in Research and bolster its proprietary content advantage for the AI economy. Emerald will add $78M to FY27 revenue and $0.10 to EPS, but it comes at a cost: it will be dilutive to Free Cash Flow by $15M in year one. It is not expected to be FCF accretive until FY28.

🔴 𝐂𝐚𝐬𝐡 𝐂𝐨𝐥𝐥𝐞𝐜𝐭𝐢𝐨𝐧 𝐓𝐢𝐦𝐢𝐧𝐠 𝐈𝐬𝐬𝐮𝐞𝐬 [NEW]

Despite a massive 55% jump in Free Cash Flow to $195M, management explicitly flagged that FCF was 'moderated by late renewal signings impacting the timing of cash collection.' While likely a temporary working capital shift, any delay in institutional renewals in the core Research business requires close monitoring in Q1 FY27.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰: $195 million

Accelerating. Up 55% YoY from $126M. This was driven by higher cash earnings and a reduction in CapEx ($65M vs $77M in FY25), validating the company's capital-light, partner-driven AI strategy.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐑𝐞𝐭𝐮𝐫𝐧𝐬: $174 million

Accelerating. Wiley returned a record amount to shareholders, up from $137M in the prior year. This includes $100M in share repurchases (up from $60M) and a dividend increase marking the 32nd consecutive year of dividend growth.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟕 𝐎𝐫𝐠𝐚𝐧𝐢𝐜 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐆𝐫𝐨𝐰𝐭𝐡: Low-to-mid single digits

Accelerating slightly. With FY26 organic revenue coming in flat to 1%, guidance for low-to-mid single digits implies an acceleration, driven by core Research growth and an expected moderation of declines in the Learning segment.

𝐅𝐘𝟐𝟕 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀 𝐌𝐚𝐫𝐠𝐢𝐧: 26.5% to 27.5%

Stable to Accelerating. Improving from 26.2% in FY26. This indicates that management expects ongoing efficiency gains and restructuring savings to outpace new growth investments and the integration costs of Emerald Publishing.

𝐅𝐘𝟐𝟕 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐏𝐒: $4.60 to $5.05

Stable growth. The midpoint of $4.825 implies roughly 15.1% YoY growth, maintaining the exact same growth rate achieved in FY26 ( 15% to $4.19). This is driven by higher expected operating income and lower share count.

𝐅𝐘𝟐𝟕 𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰: $205 million

Decelerating growth. Up only ~5% from FY26's $195M, a sharp deceleration from the 55% growth seen this year. The slowdown is explicitly attributed to $15M in year-1 dilution from the Emerald acquisition, higher CapEx ($80M vs $65M), restructuring costs, and higher cash taxes.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐋𝐞𝐚𝐫𝐧𝐢𝐧𝐠 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐄𝐧𝐝-𝐆𝐚𝐦𝐞

Given the chronic declines and macro headwinds in the Learning segment, is there a point where management considers divesting this business entirely to focus as a pure-play Research and AI data provider?

𝐄𝐦𝐞𝐫𝐚𝐥𝐝 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐢𝐨𝐧 𝐑𝐢𝐬𝐤𝐬

The Emerald Publishing acquisition is dilutive to Free Cash Flow by $15M in FY27. What are the specific integration milestones required to flip this to FCF accretive by FY28, and how much restructuring is involved?

𝐋𝐚𝐭𝐞 𝐑𝐞𝐧𝐞𝐰𝐚𝐥 𝐒𝐢𝐠𝐧𝐢𝐧𝐠𝐬

You cited late renewal signings as a drag on cash collections in Q4. Was this driven by specific geographies, resistance to price increases, or administrative delays, and has the backlog cleared in Q1?

𝐀𝐈 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐌𝐢𝐱

Of the $49M in AI revenue delivered in FY26, what exact percentage is now tied to recurring corporate subscriptions versus one-time LLM training licenses, and what is the target mix for FY27?

1

1

537

Jun 16

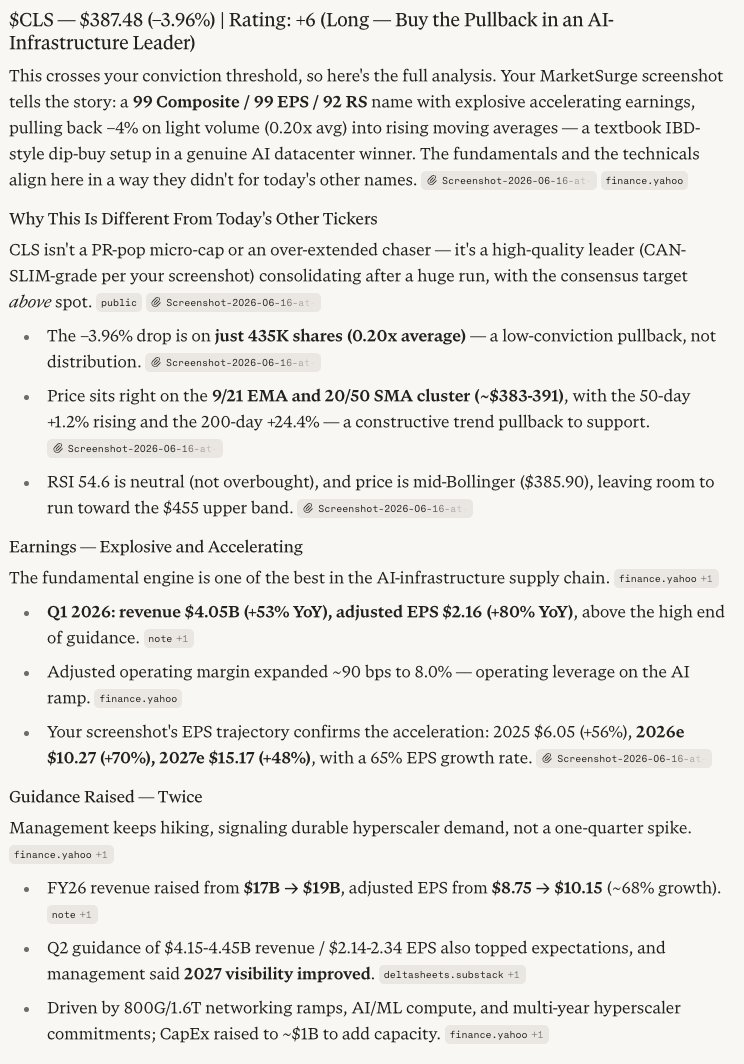

Picked up $CLS shares and July $400/450 call spreads on this checkback to the 50DMA. NFA

2

227

Jun 15

379

BG2 w/ Gavin Baker. The SpaceX IPO, Fable 5 / Mythos, AI Capex Update & Market Check. 🚀💰 @BG2Pod @altcap @GavinSBaker @_clarktang

49

66

777

9,270,896

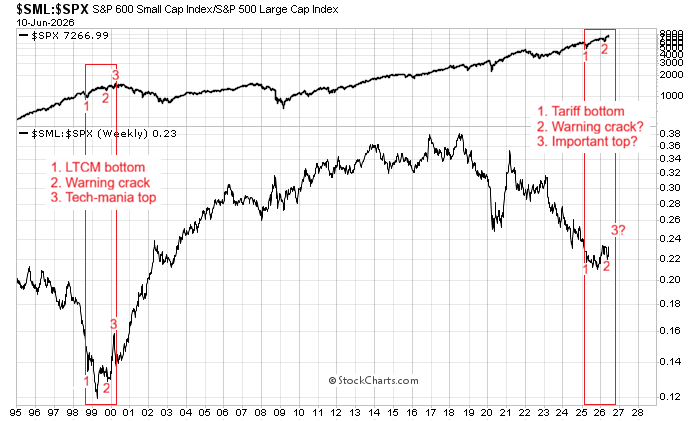

Jun 11

$IWM held today's gap-up so far unlike $SPY and shows a much better structure (above the 21EMA on the daily) unburdened by the large-caps issuing equity and spending huge amounts of capital: $MAGS -1%

x.com/mark_ungewitter/status…

Small-cap should outperform sharply from here, if post-LTCM analog continues. Big if, of course.

1

2

934

Jun 12

$IWM now at all-time highs and impressive vs large-cap indices. Facing resistance at this trendline but third time's the charm?

1

1

315

Jun 15

$MAGS one of strongest out of the major ETFs as rate pressures abate. Sentiment is negative on megacaps due to their huge spending plans. Bounced off the Iran war low AVWAP / DeMark Buy signal. I took the July 70 calls. NFA

192

Minerva Capital retweeted

Jun 11

🏛️ Alex Sacerdote | A Tech Investing Masterclass

Alex Sacerdote, founder of Whale Rock Capital, is one of the most successful technology investors we track.

Over time, a portfolio built around his top positions has delivered exceptional results, outperforming most hedge funds and significantly outpacing the Nasdaq.

That's why this interview is a must-watch for anyone serious about becoming a better investor.

📊 The goal isn't to copy every trade blindly.

It's to understand how elite investors identify winners, build conviction, and stay invested through volatility.

📈 You don't need to become the next Alex Sacerdote.

You just need to learn how to invest alongside him. 🤝

Save this post. You will not regret.

x.com/patrick_oshag/status/2…

My conversation with Alex Sacerdote, founder of Whale Rock Capital Management.

Alex runs more than $17B and has been one of the best performing tech investors for years, though he keeps a low public profile.

As you'll hear, he is singular in how he thinks about investing through technology cycles.

For over 25 years, he has built his entire investment framework around a single idea, the S-curve.

We discuss:

- The AI L-Curve

- When to buy into an S-curve and when to sell out

- The de-commoditization of data center hardware

- Why he went net short software

- His two models for tech adoption

- Finding alpha

Enjoy!

Timestamps

0:00 Intro

9:55 AI's L-Curve

19:31 Whale Rock's S-Curve Playbook

26:14 Spotting Inflection Points

32:02 Finding AI Winners

40:04 AI vs Software

48:13 The Hardware Renaissance

58:04 Why Investors Miss AI

1:05:18 Whale Rock's Research Machine

6

38

6,112