Joined September 2021

- Tweets 350

- Following 592

- Followers 1,216

- Likes 5,202

16 Photos and videos

Jun 13

Ep 2 -= Sat Kartar Life Ltd

WEe continue looking at all the listed players within the listed Ayurvedic ecosystem

Sat Kartar stands out from all other manufacturers and vendors of medicnes ( allopathy and ayurvedic) as it is pure play D2C brand in the listed space

Exciting model but untested on scale

The more and more we look at other models , the more we realise how operationally effecient and Superior Jeena Sikho really is.

@TrinetraAsset #investing

1

1

11

1,734

Priyam shah retweeted

Jun 12

Never give up

Jun 12

> you’ll never start a rocket company

> you’ll never build your own engines

> you’ll never be able to use off-the-shelf parts

> you’ll never survive three launch failures

> you’ll never reach orbit

> you’ll never win NASA’s trust

> you’ll never launch cargo to the ISS

> you’ll never compete with Boeing

> you’ll never compete with Lockheed

> you’ll never make rockets reusable

> you’ll never land a rocket vertically

> you’ll never land one on a drone ship

> you’ll never reuse a booster

> you’ll never fly the same booster 10 times

> you’ll never fly the same booster 20 times

> you’ll never fly the same booster 30 times

> you’ll never recover and reuse the fairing

> you’ll never lower launch costs

> you’ll never launch every month

> you’ll never launch every week

> you’ll never launch multiple times a week

> you’ll never carry astronauts

> you’ll never replace Roscosmos

> you’ll never fly civilians to orbit

> you’ll never manufacture satellites at scale

> you’ll never build the biggest constellation ever

> you’ll never make satellite internet work

> you’ll never make satellite internet fast

> you’ll never make satellite internet affordable

> you’ll never serve rural customers

> you’ll never serve aircraft and ships

> you’ll never build a methane rocket engine

> you’ll never make full-flow staged combustion work

> you’ll never build the most powerful rocket ever

> you’ll never build a rocket bigger than Saturn V

> you’ll never build it out of stainless steel

> you’ll never launch Starship

> you’ll never separate Super Heavy and Starship

> you’ll never relight Raptor in space

> you’ll never bring Super Heavy back

> you’ll never catch a booster with Mechazilla tower arms

> you’ll never launch 85% of mass to orbit worldwide

> you’ll never change the economics of space

> you’ll never force the entire industry to copy you

> you’ll never win

> you’ll never IPO

Congratulations to @elonmusk and the SpaceX team. You did what countless people said was impossible, and you did it time and time again.

Today is your day. You deserve this. May it be a glorious one.

308

2,498

25,529

971,337

Jun 6

The TAM Based story telling that folks are skeptical about Jeena Sikho can is not too much of a concern ;

Having visited ~ 4 Hospitals/ Day Care centers in Mumbai and Surat - The demand is very real

A - Five Lakh Seventy Thousand people walked through Clinics and Day Care centers ( OPD Patients) through FY 26

The demand is real , visible and not manufactured - If there wasnt an underlying belief in Ayurveda or usage of Ayurvedic products - This pace of growth wouldn t have been possible .

You can fool one person all the time, but not all people all the time .

B - The Unit economics can be questioned on paper but you need to visit a hospital to understand why this is the case

They look nothing like a allopathy hospital - No OTs, Cath Labs, ICUs, radiology machines - nothing

The rents are low as almost all are on the outskirts of cities.

C - I still believe, the way JSL operates unit economics are very similar to how a Hotel runs , and not a hospital

The model has evereything that a well run Hotel needs

Low Opex, high occupancy , High Average Length of Stay ( ALOS )

Its actually quite opposite to a allopathy hospital as any reputable hospital would try to shorten their ALOS - reason being Day 1 or 2 has surgery post which any additional days of stay tends to taper off the ARPOB

D - Insurance tie ups validate their workings

Why has IRDAI mandated that AYUSH treatments be covered by all insurers

Why is every single insurer , including GIPSA ( Government insurers) on board and on the panel for JSL

E - Mental model to think aboout JSL is that it operates on the intersection on health and wellness - leveraging the fact that Ayurveda has always existed in India

But has only existed with the abscence of a national end to end integrated chain . JSL is simple institutionalising what has already existed

Ayurvedic doctors have always been there . Medicines have always been there - JSL Has branded them and formalised the chain

E - Yes treatment efficacy for some causes like Cancer is questionable but that is a miniscule percentage of revenue

Everything that Ayurveda propogates is ultimately wellness and a way of life.

Theyve never said its a magical 8 day treatment - Its a way of life that needs to be followed

F - Yes the key man risk is real and always be there.

Best of brands in India are first built on personal brands and institutionalised over time

There can be endless debates on the clinical efficacy of treatments and the fact that they may not work - Think about JSL as a category creator.

2

5

36

11,219

Jun 2

Some super explicit Guidance On Jeena Sikho Concall right Now;

Our aim is to grow PAT 4x to 5X in the next 5 years

And it is doable.

2

1

29

3,171

May 14

A 45 minute video taking you through the Jeena sikho business

We like the business and are in awe of the execution that has happened and also what yet has to take place

You may ot may not be a believer in Ayurveda but cannot deny that massive tailwinds exist here

If an Industry has gone from 2.5 billion to 45 billion USD ( AYUSH prooduct sales), something special has already taken place and the demand is real

3

14

72

8,009

May 12

Pace of Growth

Why do we say, that Good times never last

They did not last, even for the King of Good Times

Investing across small or midcaps have crated this narrative that multibaggers are easy to disover, hold and nurture and see through

Some potential investors we talk to @TrinetraAsset , whether we are discussiong our model portfolios or individual stock research - tell us they expect multibaggers 5 years out

We find it funny because the future is uncretain , unpredictable and definitely not on an excel sheet

Intrinsic value, a concept washed down your throat by professors and finance magazine peddlers is a broken word.

Intrinsic value of a stock today for FY 30 or FY 35 is basically your abiliity to chart out all the cash that the business will at will generate over the next 5 to 10 years, use a discount rate and get it back to its Present value

The only problem , is neither the promoter knows the shape of his company 10 years out , neither the merchant bankers who bought the issue and defintely not you.

Our view on looking at companies is to follow earnings , intead of predicting them

Continue investing in companies which exhibit and deliver high pace of earnings growth and exit those who dont. ( earnings momentum, not price momentum - I will one day take a seperate session on why Technical analysis is a dastardly and stupid thing to do )

Instead of considering investing outcomes as certainities , we consider them as variables, say in a Bayes probability theorem

Probaility of a ( Multibagger Stock A ) =

Prior Knowledge of the event ( Stock A )

New evidence that either adds to or refutes Prior knowledge

The fact that , in the last 10 years only 150 odd cos out of the 4500 companies were able to cross from the 1000 cr to 5000 cr market cap says, that our starting probability itself is 5% tops and not what people assume.

Not to be a pessimist here, we look for asymmetrical returns but not through single bets and single mindedness .

Look out for companies doing better than others, and continue backing them as long as they continue outperforming ( in numbers)

Markets mimic life very well - The world only cares about winners.

If Indias richest man, circa 2008 and bankrupt today - couldnt map his own cash flows - Aap or hum toh kya hi he.

hashtag#investing

2

11

1,126

May 11

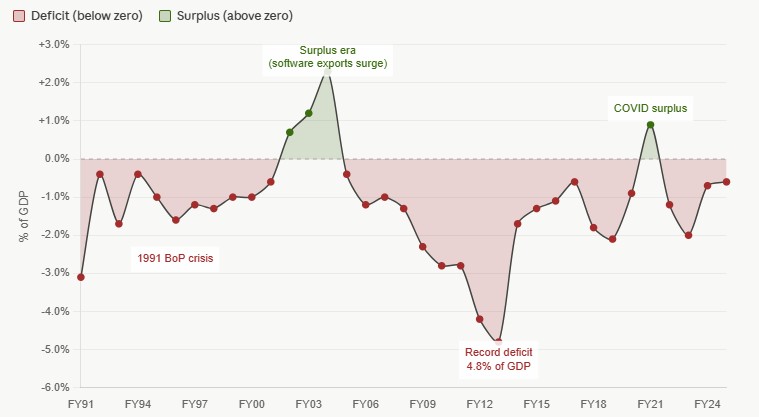

Not as bad as it sounds

We have more or less been running a current account deficit since forever.

I would split CAD into controllables and uncontrollables

A current account statement is like a P/L statement that then flows into The Balance Sheet

Put simply - A current account has 4 variables

A - (Good exports - Good imports) - Uncontrollable

The imports are primarily crude and Gold - And exports from India will never match up in the forseeable deficit

We ran a negative Deficit of 87 Billion USD in Q2 FY 26

B - ( Serevices exports - Services Imports ) - Controllable

Our services , namely IT services exports and the GCC wave has kept this tab in surplus since 2 decades now - This nicely negatesd the impact that our Goods deficit has

As long as talent pool doesnt shrink and we continue to have a cost arbitrage with the west, this will continue to do well

C - Primary Income - ( Income earned by Indians owning assets abroad - Income paid to foreigners on Indian Assets ) - Uncontrollable

Here the income earned is NOT remittances but say dividends on our reserves, a majority of which are hel;d through T Bills, dividends received by Indian cos have a subsidiary abroad'

Income paid to foreigners include everything from dividends paid to bond holders to all the OFS that MNC cos do in India at obscene valuations and promptly remit the money home

D - Secondary Income ( Incoming transfers - Outgoing transfers) - Controllable

Thank god to our India Loving diaspora abroad, we have a very healthy inward remittance that offsets a lot of pain

So the Current account is largely - A B C D = which has largely been negative

Whatb do you do when you incur a loss on the P/L ?

You draw from your reserves

What do you do do when reserves are depleting ( Like we had in 1991? )

You do a QIP - Only caveat is here the institution would be the World Bank

None of this of course is going to happen to us. We have healthy reserves and many monetary measures to offset this

Only problem is that GOI is trying to control the uncontrollables

Wont work

In India, if you tell someone to not do something - They will definitely do it.

We need some bold economic policy decisions, rationalisation of taxes and a need to tone down the freebies .

#investing

1

7

632

Apr 1

Hospital scuttlebutt

We were in Delhi and Faridabad a whike back to visit some of the newer hospitals of Yatharth Hospitals, a listed entity that is expanding fast within the NCR region

Public data suggests that the hospital industry is entering into a new capex cycle

Almost every single hospital chain has announced major capex with the likes and size of even *Max* hospitals announcing their intention of doubling their bed size over the next 4/5 years

When one of the largest players in the industry announces capex at this scale, it means that the industry as a whole has entered into a capex mode.

We crunched some data on when the last time the hospital industry went into a capex mode as whole – 2015 to 2019

-Hospital bed counts almost increased by 70 to 100% for multiple hospital chains during that period ( 2015 to 2019)

-The period had low/ no returns for hospital stocks

We believe that while we are in a hospital supercycle as of today similar to that we saw in 2015/2019 – but we are unlikely to see the same low/no return cycle.

There are *distinct* differences between the both cycles

A – Conventional capex in the 2015 to 2019 cycle was greenfield and brownfield.

In simple terms ;

*Greenfield* capex cycle means purchase of land, construction of building and the entire facility – Has a 5 to 6 year payback period.

*Brownfield* capex is construction of a new facility either on or near your existing hospital/ Land parcel. – Has a 2 to 3 year payback period.

This time the capex cycle has one distinct difference -

A - A lot of the new capacity that is being added in few hospital chains is through *acquisitions* .

There are 500 multiple defunct hospital assets available for sale if you just look at *SARFAESI* website

These hospitals went defunct due to lack talent/ Branding.

The new play within the sector is to acquire hospitals either through NCLT/ SARFAESI in a good location, spend a minimal amount on capex, re brand them and voila you have a running asset in a few months

These Hospitals are take less than 6 months to breakeven and thus add to the topline very fast.

B – Unlike the last cycle, when a lot of these new assets were created through debt, the new playbook is acquiring these new assets through money raised via QIP/ Prefential issues.

While this leads to equity dilution , there is no debt burden so ROE expands immediately on breakeven unlike the last cycle where it took years for the new capacity to be ROE positive for shareholders

Our view on *Yatharth*

-Went from 1000 to 2800 beds – almost all through acquisitions led by QIPs and IPO proceeds

-Plans to follow similar playbook to reach 6000 beds in 3 to 4 years

-Major focus on oncology which is the highest ARPOB ( Average revenue per occupied bed )

-The mental model with such business models is to stay with them to as long as growth persists

@TrinetraAsset

5

24

2,983

Priyam shah retweeted

Feb 25

Grateful to present at TIA 20:20 at IIT Madras, sharing my thesis on #Azad Eng 650 passionate investors. Powerful conversations.

Honoured to share the stage with Mr. G. Maran, Mr. Sunil Shah, Mr. Naresh Katariya, & Mr. Shyam Sekhar sir & many more.

Thank you team @TIA_Investors

16

12

170

30,857

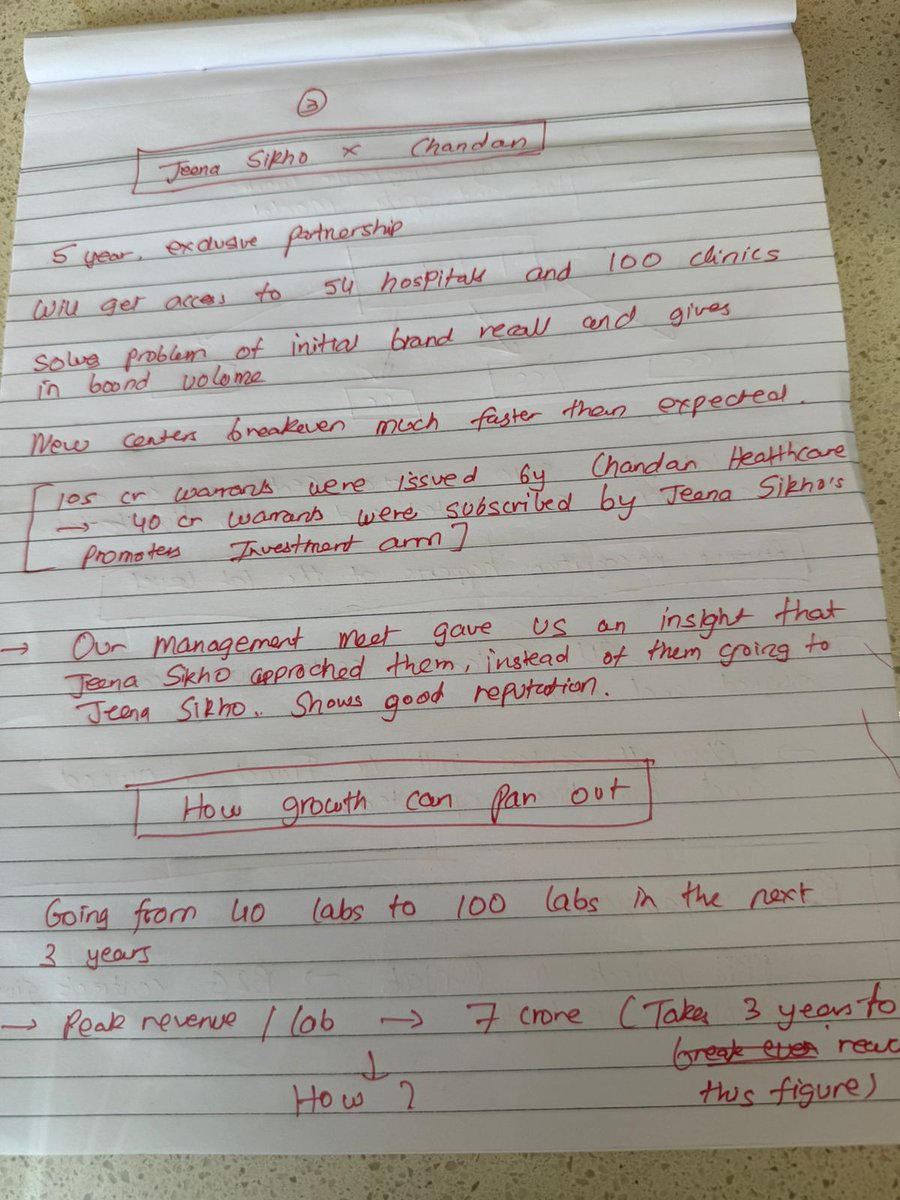

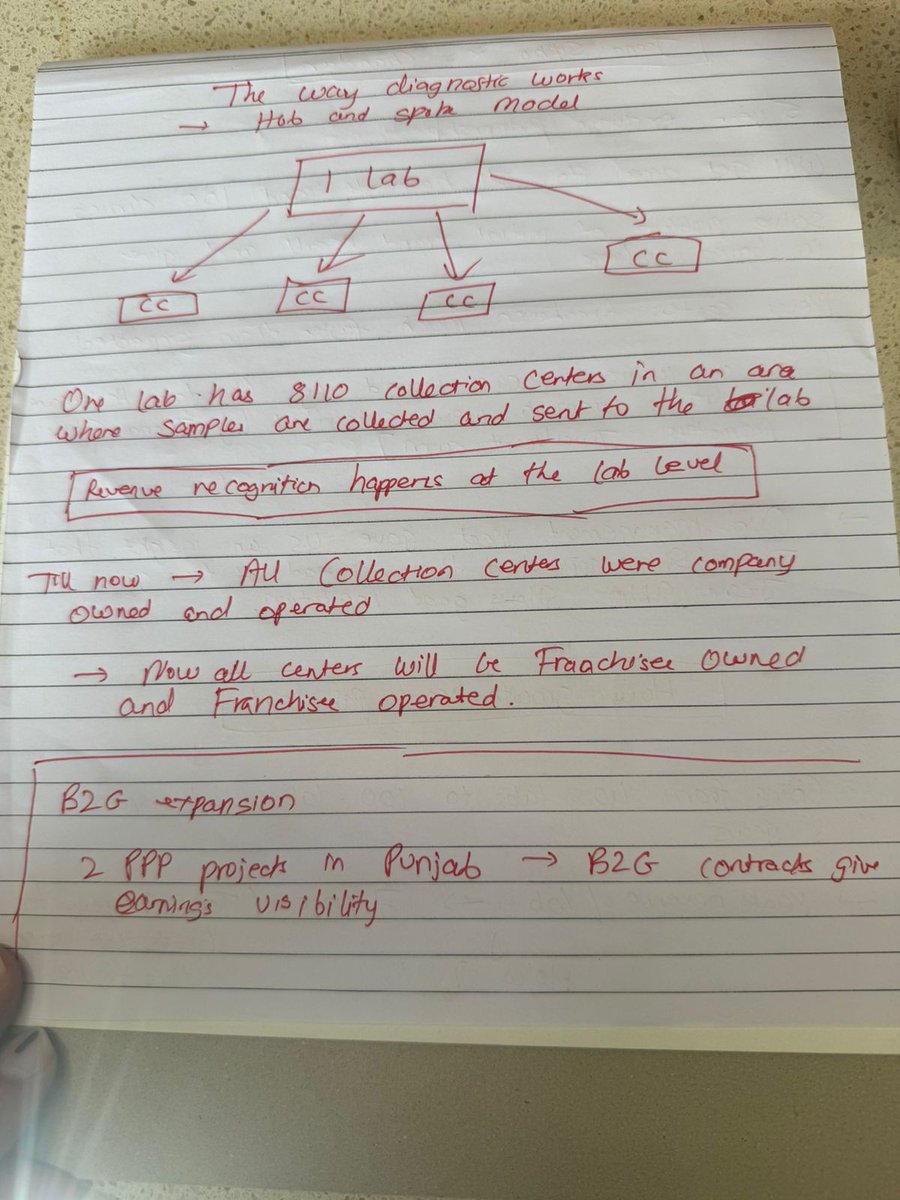

Feb 12

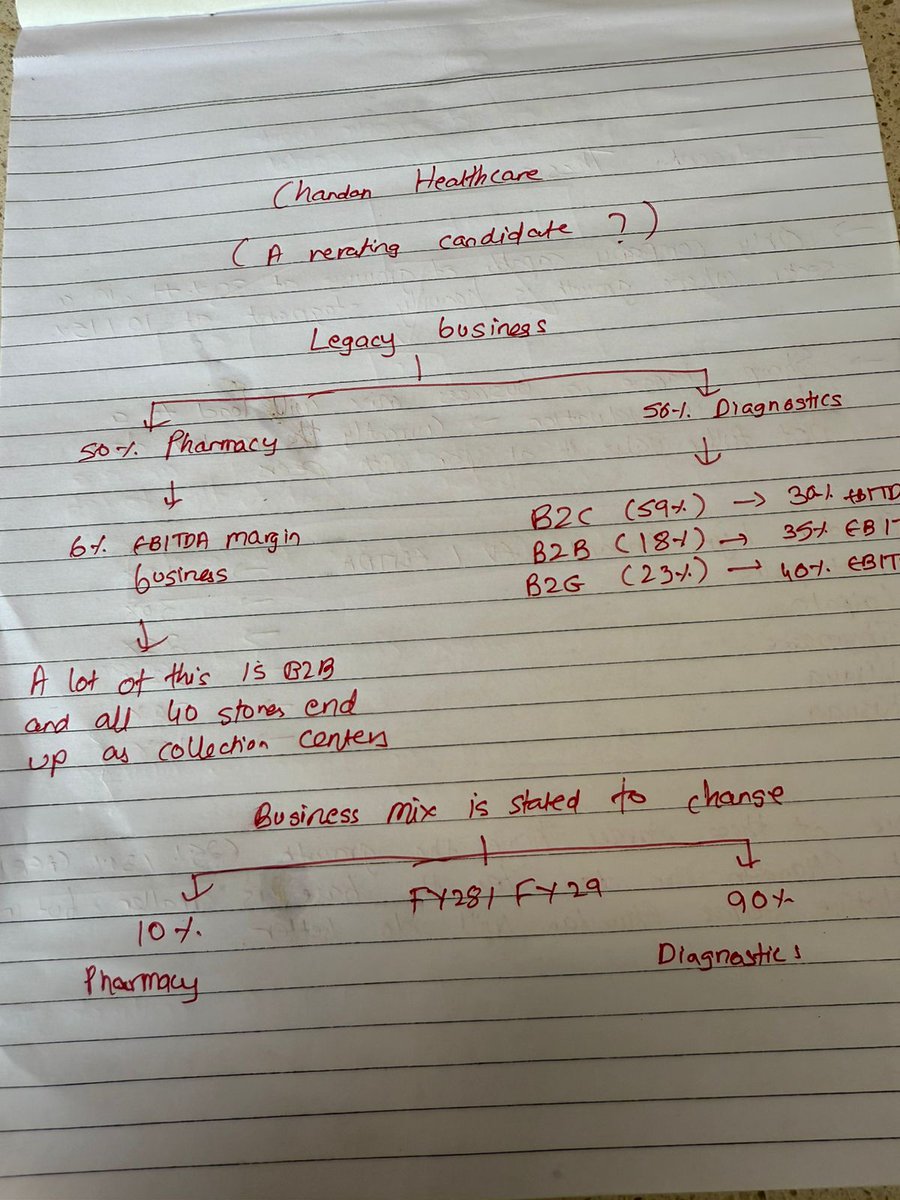

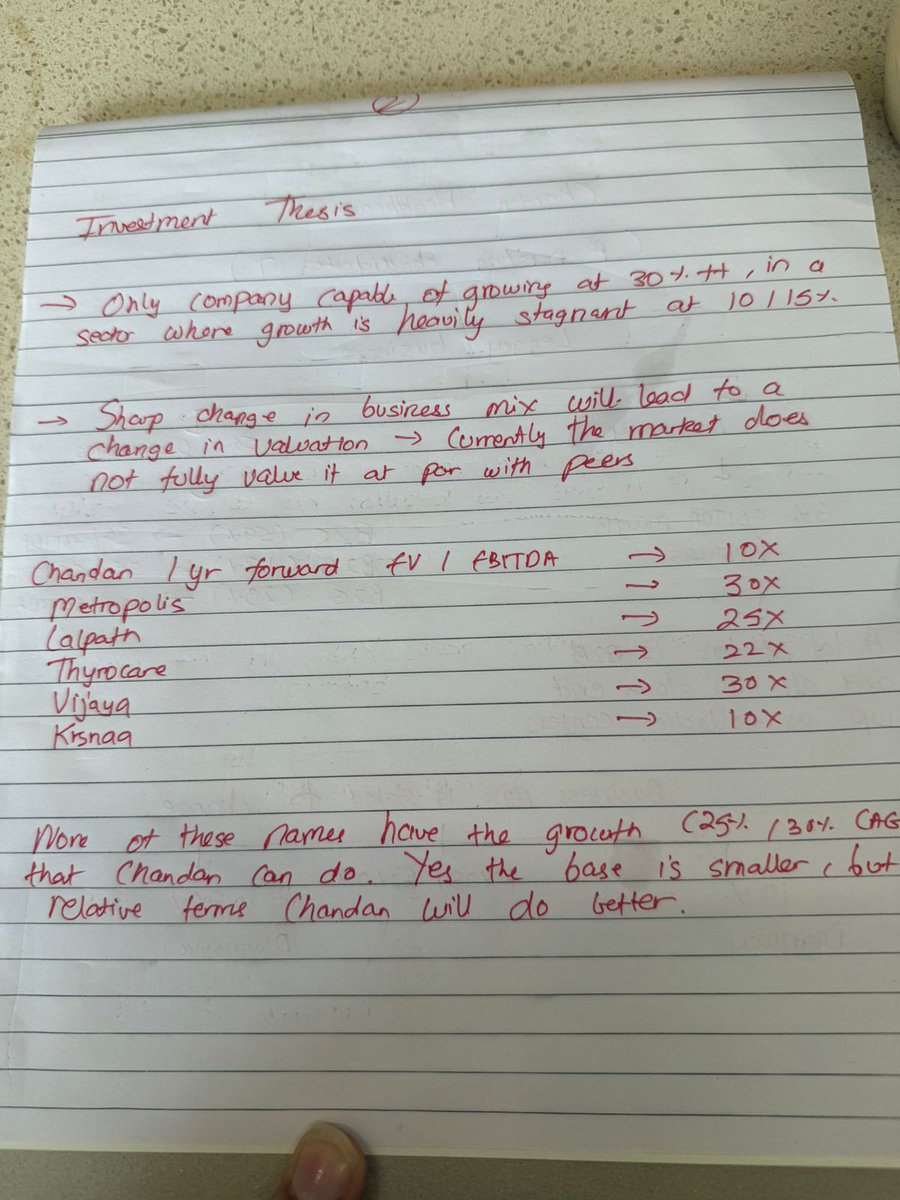

Our Thesis and notes on Chandan Healthcare

If execution is on point for the next few years, we feel the rate of change in this business is going to be phenomenally high in this business

Notes attached in the comment section

1

7

35

5,844

Feb 6

We shot a long form video taking you through our thesis of Unihealth Hospitals

Our original thesis - docsend.com/view/x4rnvuutdvm…

The video is a conversation with the management on the business, future outlook and what lies ahead.

Disc - Invested, biased.

5

28

3,448

Priyam shah retweeted

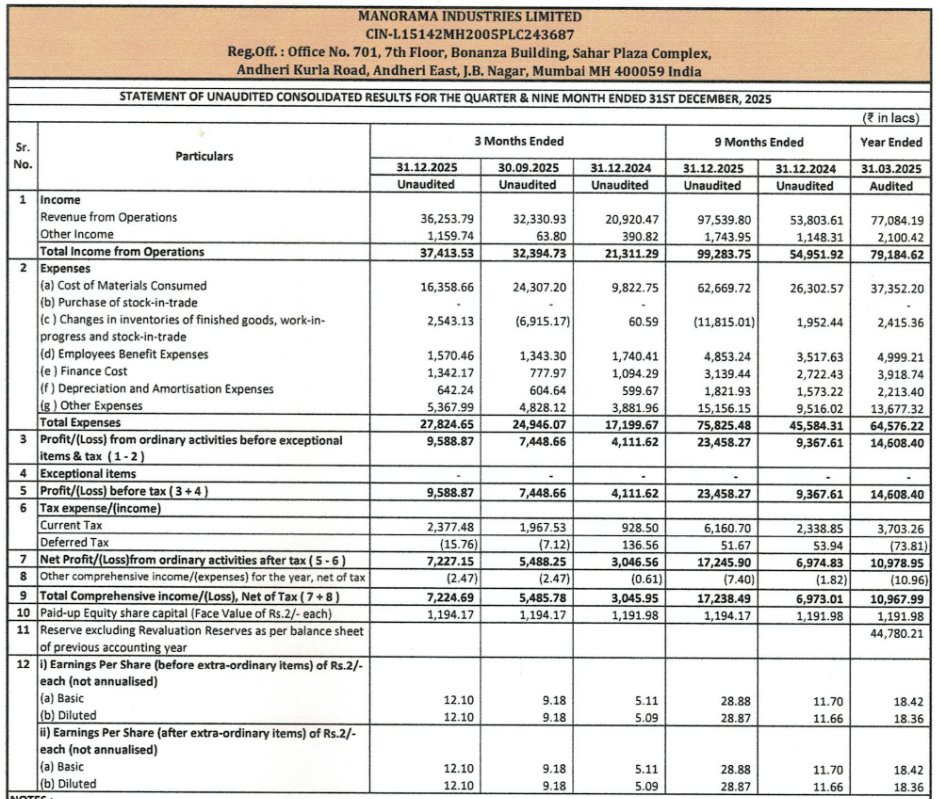

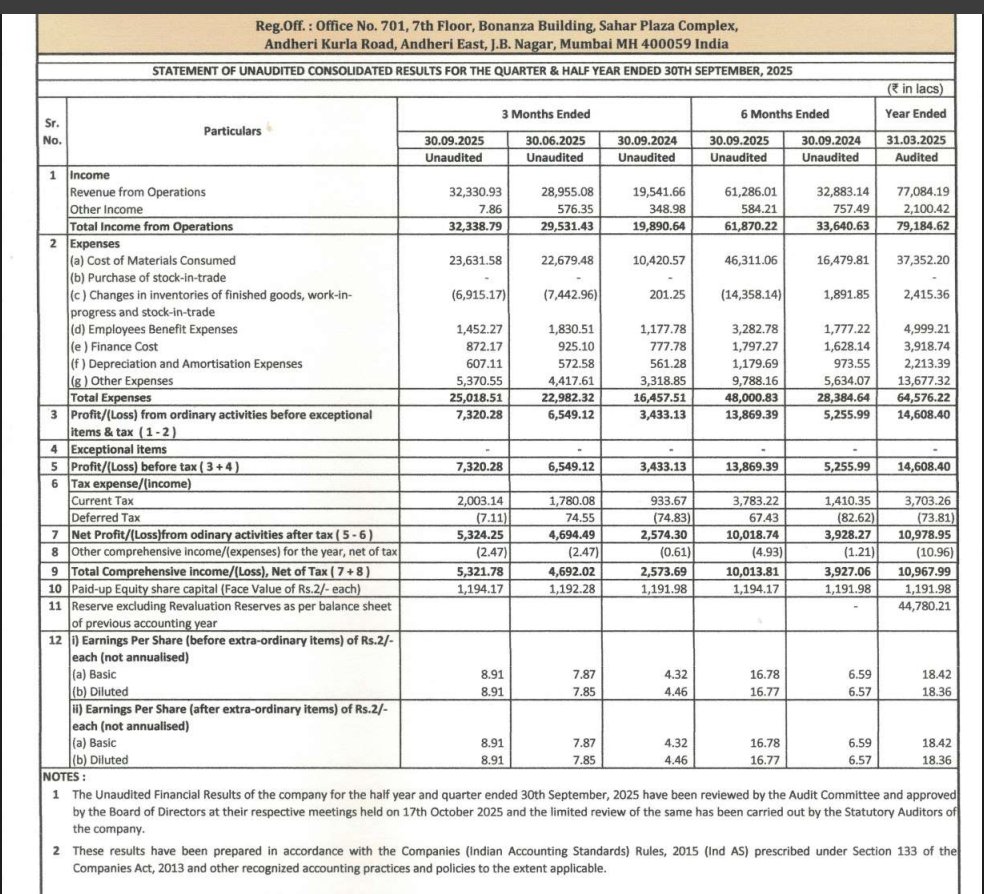

Jan 28

#ManoramaInd has achieved an all-time high PAT of 72cr, in line with FY24 EBITDA. We see PAT scaling to 230–250crs in FY26 and progressing toward 1,000crs thereafter. The ongoing capacity expansion from 40k MT to 52.5k MT is set to significantly boost financials.

RoCE: 50%

17 Oct 2025

#ManoramaInd

The company reported a PAT of ₹53.2 Cr.

I believe FY2026 could see PAT exceeding ₹200 Cr, with this quarter alone likely reflecting strong growth.

Looking ahead, I see the potential for Manorama Industries to achieve ₹1,000 Cr in PAT by FY2030.

3

9

47

5,123

Jan 13

As we highlighted earlier, Only High ROCE ratios without meaningful topline growth is useless

A bubble chart that compares a cross section of ROCE ratios and last 3 year topline growth

No prizes for guessing which stocks did well and which were laggards.

Our core investment thesis over the years is to back companies in sunrise industries with a high pace of growth

Never fails and the results speak for themselves.

2

9

783

Jan 13

The BIG 4

In IT Services

We start the earnings season

With the usual set of laggard results that are dressed up as High ROE Coffee Can names that provide nothing else other than an anchoring bias

Anything that cannot earnings > 10% is a perfect retirement stock

ROCE and ROE numbers do not matter without growth

A 10 year sales growth of 10 % , after accounting for a ~ 50% currency depreciationis absymal

Glory days for IT services are over and nothing bad about owning TCS but it will continue to be a 8 to 10% cagr stock where serious money cannot be made or lost either

A bar too low for an active investor

A company where the CFF ~ Cash flow from operating activities , which means all the money Is either bring paid out as dividend and/or structured as buybacks

Essentially making these cos piggy banks and not growth machines

The only distant optionality is the AI data center

The theme is more exciting than TCS’s role in it.

AI data centers are a different ball game compared to vanilla data centers

Data centers that are going to run AI Inference models need much more conpute power and infrastructure

Between Reliance, Adani and TCS now ~ almost 5 GW of AI data centers will come through in the next 5 years

That is almost a ~ 3 lakh crore of private capex that primarily will be classifie as

GPUs - ~ 50%

Land, Building and EPC - ~ 15% . In Inda land in most of these cases will ne alloted so that might drive down cost .

Liquid cooling systems - 15% ~ which has to be locally sourced in India

Electrical Infrastructure - 20% ~ which again will be locally sourced

So net net, A rough TAM of 120,000 crores for AI data centers alone in India over the next few years

How and where this money moves will be key to find out where value will be made.

We happen to be meeting a micro cap data center epc company this week - More on thise insights later

2

2

13

2,420

29 Dec 2025

Timex - OFS - A point to worry ? Not all

Major points covered

Business direction

Pace of Growth

3 key triggers working out for them

Multiple Optionalities in the near Future

2

4

31

3,865

Priyam shah retweeted

25 Dec 2025

Koushik Mohan, Lead Analyst, Ashika Group, will be speaking at TIA 20-20 Ideas Summit 2026 !

@mohan_koushik1

Link to Register :

docs.google.com/forms/d/e/1F…

7

9

66

22,902

Priyam shah retweeted

9 Nov 2025

Trinetra Asset Managers made bold prediction about HBL couple of months ago. Of course, company has delivered even more aggressively.

Report is available on Telegram channel, posted on Aug 11th, if you are looking for a detailed note.

8 Nov 2025

#HBL Eng

Revenue: 1,222.9cr vs 520.96cr

PAT: 387.27cr vs 87.26cr

Did anyone expect numbers like these? Absolutely mind-blowing!

At this pace, 2,000cr PAT looks just around the corner.

Last year’s topline is turning into this year’s bottom line what a transformation!

5

9

112

22,525