325 Photos and videos

Prof. Dollar retweeted

Jun 15

ずっと生で見たかったこれ🥹てか混ざりたかった😂

オレンジに染まるこのスタジアムを見た時負けた...と思ったけど彼らの応援はここがピークで、試合中は日本サポの声が響き渡っててずっと泣きそうだった🥹💙

33

168

4,128

367,981

Prof. Dollar retweeted

Jun 14

373

3,108

26,834

5,246,677

Prof. Dollar retweeted

Jun 14

187

1,296

11,900

1,423,812

Jun 13

🟠𝗢𝗥𝗔𝗡𝗝𝗘 𝗙𝗘𝗩𝗘𝗥 - a cinematic look at the enduring passion for Dutch football. Featuring reflections on the team's historical legacy, this production explores the intense anticipation and national fervor that surrounds the squad.

youtube.com/watch?v=_XHEYhVu…

#FIFAWorldCup

233

Prof. Dollar retweeted

Jun 12

$qure $clpt

Uhhh guys, FDA just gave the playbook, they just told us directly what they think about natural history for HD here.. This is the FDA speaking here. This was June 5, 2026, Lauren Holder also spoke. 2 hd people spoke. Why do you think the FDA specifically requested Lauren to be there and speak?? -) Not sure what else the new FDA can say, they basically just specifically called out HD and natural history..

Look who was one of the main hosts and also spoke

Teresa Buracchio- the same Teresa that said

“FDA official confirms plausible mechanism principles not exclusive to bespoke gene therapies”

Michelle Campbell FDA 35.48 to 36.38 woah….

Look what she says about HD..

FDA again 1:36 - 1:39- big time big time, FDA calls out HD and natural history.

“Natural history is going to be paramount and fundamental to how we really think about the understanding of the disease!”

“Whether it’s ALS, Huntington’s, or a neurodegenerative disease, The truth is the same, time matters.” @laurencurehd spoke from 1:28

youtu.be/A7FSfQINBVE

fiercebiotech.com/biotech/fd…

@peter_mantas @Tim_Corr @DesertDweller93 @Prof_Dollar @biggercapital @Christina4HD

8

14

90

28,002

Prof. Dollar retweeted

Jun 10

I went through every single patent $QURE owns and I'm convinced this will be a behemoth. Post below.

4

7

94

14,983

Prof. Dollar retweeted

Jun 7

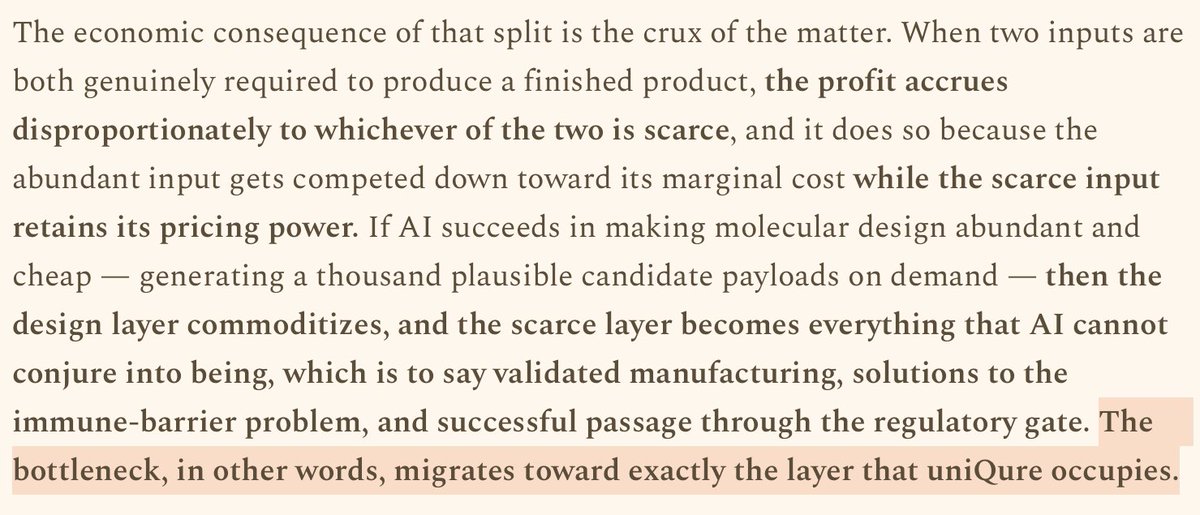

Remember I mentioned owning $twst as a bottleneck play? Well here’s the equally compelling case for $qure.

Think about what the AI drug discovery landscape looks like in 2028.

Dozens of companies have identified validated CNS targets using AI. They have the molecules and the biology.

However, they don’t have the regulated delivery, the regulatory infrastructure,

the regulated manufacturing, regulated safety data or the patient database required for trials.

$QURE becomes the delivery partner of choice for CNS gene therapy. Why? Because they’re the only option with:

1) Years of validated human CNS safety data;

2) Global regulatory pathway;

3) Deep access to the world’s largest HD natural history dataset;

4) Established GMP manufacturing infrastructure;

5) Surgical CNS delivery network across US and Europe;

6) Systemic BBB-crossing capsid delivery in development;

7) MSH3 patent covering somatic repeat expansion across 15 diseases

8) IP on HTT1a and MSH3 AAV/RNAi constructs filed years before the field converged on this biology where basically every AI program targeting repeat expansion disorders will need to license

AI finds the targets but $qure gets them into the brain.

The bottleneck in the AI drug discovery era isn’t the molecule, it will be the delivery and they’ve spent a decade plus solving exactly that.

Oh btw this is on top of 130 and 260 being blockbuster drugs.

Jun 6

I believe this next wave of Bio is going to be bigger than anyone can imagine.

Multiple $10T companies. Maybe even a 100 Trillion dollar company.

9

11

95

17,134

Prof. Dollar retweeted

Jun 6

126

413

4,460

161,489

Prof. Dollar retweeted

Jun 7

Thanks for having us, Times Square! 🧡

#OranjeIsTakingOver #FIFAWorldCup

18

50

405

28,849

Prof. Dollar retweeted

Jun 7

Oranje is taking over New York City. 🌆

#OranjeIsTakingOver #FIFAWorldCup

10

29

319

17,172

Prof. Dollar retweeted

Jun 6

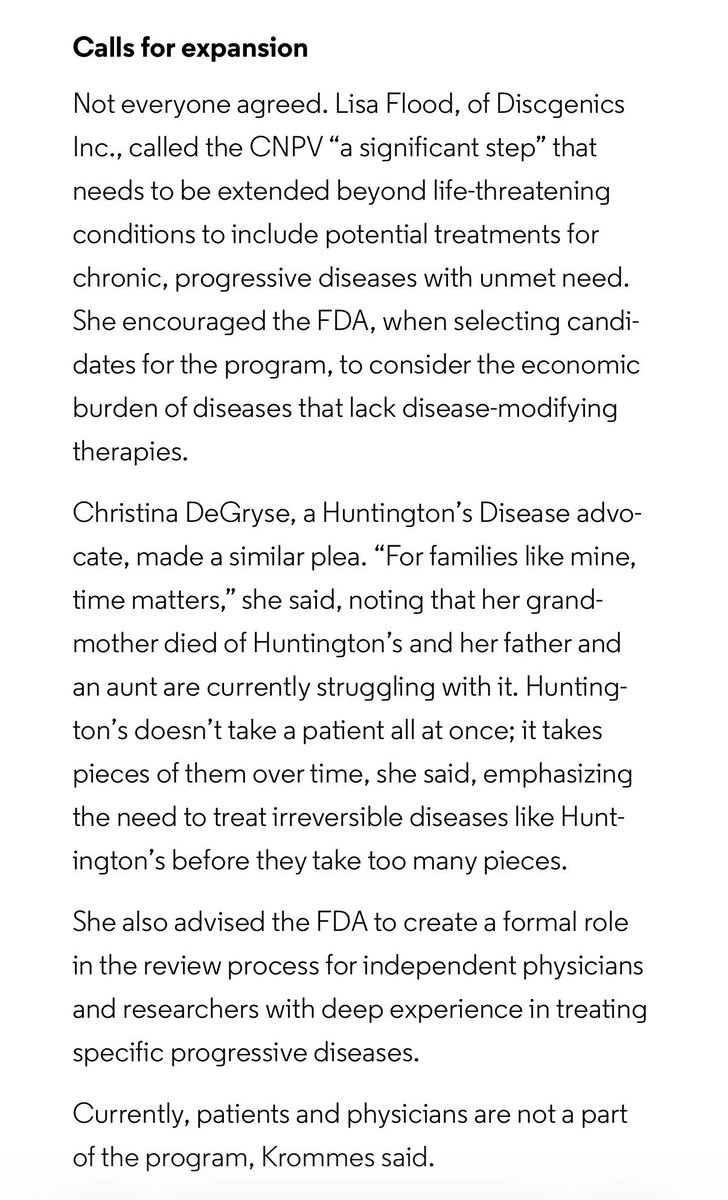

We called for faster access to promising therapies and for clinicians who treat Huntington’s disease to have a formal role in regulatory review.

@BioWorld coverage:

1

9

50

1,461

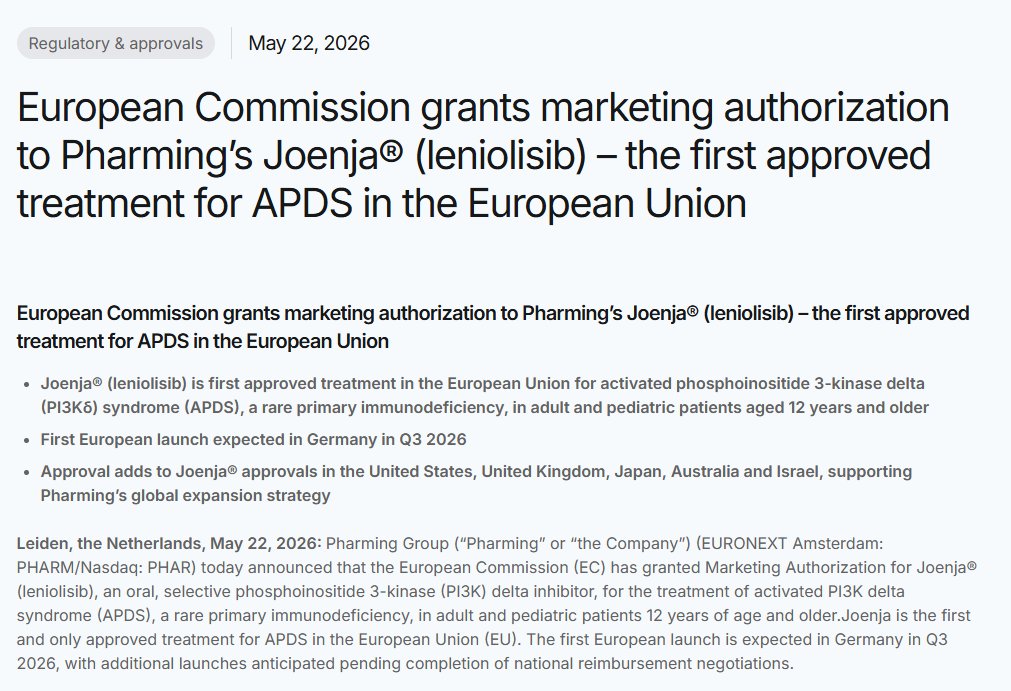

Jun 4

$PHAR Pharming announces U.S. FDA acceptance of sNDA resubmission for #Joenja® (leniolisib) to treat children aged 4 to 11 years with #APDS

Source: pharming.com/our-news/pharmi…

5

237

Prof. Dollar retweeted

Jun 2

I am so honored and excited to be presenting at this upcoming virtual research update!

"Progress in ALS and rare neurodegenerative disease research depends on the type of collaboration that efficiently delivers results.

On June 5, @CPathInstitute's Critical Path for Rare Neurodegenerative Diseases consortium will convene partners from the @US_FDA, @NIH, the @FNIH_Org, and the lived experience community for a half-day virtual update on the work being done to accelerate therapy development for patients who cannot wait."

Register now: f.mtr.cool/vqyzjrerlc

#CPath #ActforALS #DrugDevelopment #DataSharing #GlobalHealth #Collaboration #RareDisease

7

37

4,264

May 30

$QURE “I don’t think we need a cure,” neuroscientist said. “If you can slow it down by 50 percent and pick people up early on, you’ve probably done it.”

#AMT130 reported ~75%.

He gets it.

Patients gets it.

Only question left:

Does the FDA get it?

theinitiativemagazine.com/en… $CLPT

1

9

55

2,359

Prof. Dollar retweeted

May 28

$qure $clpt

Toronto star about amt 130

“There’s never a competition over which disease is the worst,” says Harding, whose work mapping the structure of huntingtin earned her the 2024 Nancy S. Wexler Young Investigator Prize. “But most neurologists agree that Huntington’s is one of the most devastating.”

Gene therapy offers a possible workaround by targeting the genetic instructions upstream instead.

“It opens up the opportunity to drug the undruggable,” says Harding. “We could be in for an explosion of therapies, of new ways we can treat diseases.”

thestar.com/code-switching-h…

1

7

46

10,346

May 22

$PHAR EMA grants marketing authorization to #Pharming ’s #Joenja (leniolisib), the first approved treatment for #APDS in the EU. Launch expected in Germany in Q3 2026. Press: pharming.com/our-news/europe…

3

325