What matters. When it matters.

Joined June 2023

- Tweets 457

- Following 88

- Followers 50

- Likes 14

71 Photos and videos

Pinned Tweet

$SPCX is now worth more than $AMZN and $MSFT.

Think about that for a moment.

The market isn't valuing SpaceX based on what it is today. It's valuing what it could become.

Starlink becoming a global communications backbone.

Launch services remaining the dominant gateway to space.

Defense and national security contracts expanding.

AI becoming deeply integrated into its ecosystem.

And eventually, space infrastructure evolving into an entirely new economic frontier.

That's why investors are willing to assign a valuation that would have sounded absurd just a few years ago.

But there's another side to this story.

Space remains one of the most capital-intensive, technically complex and heavily regulated industries on the planet. Every step toward that future carries enormous execution risk.

The bulls see the next trillion-dollar platform.

The skeptics see a future that is already being priced as if success is guaranteed.

If SpaceX executes on even a fraction of its long-term vision, today's valuation may look cheap.

If it executes on all of it, investors may one day look back at $3T and wonder why they thought it was expensive.

That's the bet the market is making.

#SpaceX #AI #Markets

88

let the magic begin

Disney’s #Hexed is only in theaters November 25

48

As it happened - moments which blew the drivers' championship wide open 🏆👀

#F1 #BarcelonaGP

54

Jun 13

GHOST CAR! 👻 It was mighty tight between Russell and Hamilton ⚔️

Lewis was so close to taking his first pole for Ferrari 🤏

#F1 #BarcelonaGP

1

108

Jun 13

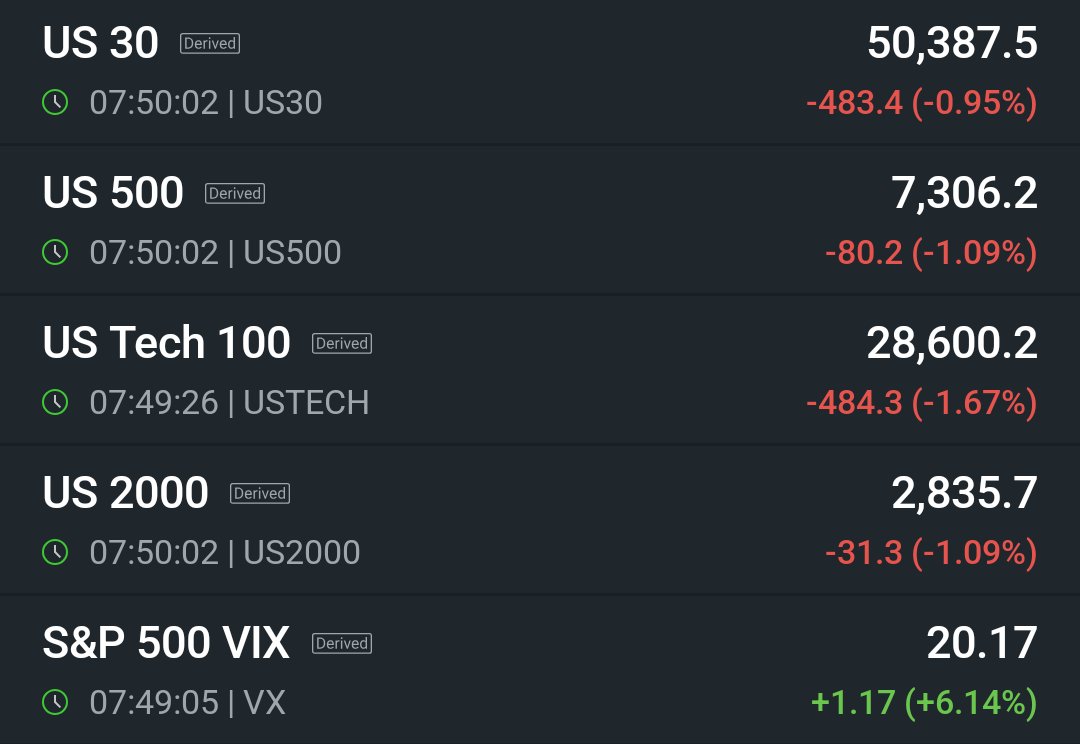

The next 72 hours could shape the direction of global markets for the rest of the summer.

🇯🇵 Monday: The Bank of Japan is expected to deliver its highest interest rate in decades, a move that could further unwind global carry trades and tighten liquidity.

🇺🇸 Tuesday-Wednesday: The Federal Reserve meets with inflation running at 4.2%, more than double its target, while markets have almost completely priced out rate cuts.

🛢️ Meanwhile, President Trump has signaled progress toward an Iran agreement, a development that could ease energy prices and alter the inflation outlook just as central banks reassess policy.

For markets, the question is no longer just rates.

It's whether falling geopolitical risk can offset tightening financial conditions.

Oil, the dollar, bonds, gold and equities may all be forced to pick a direction this week.

#Markets #Fed #BOJ #Inflation #Oil

1

49

Jun 10

US inflation is back above 4%.

The market wasn't surprised by a hotter CPI print.

Oil prices have been climbing for weeks, geopolitical tensions have returned, and inflation was already showing signs of firming in previous reports.

What matters now is how markets reprice interest rates.

If inflation continues to move away from the Fed's target, expectations for lower rates could be pushed further out. That would likely keep Treasury yields elevated and provide support for the US Dollar.

For gold, the picture becomes more complicated.

Gold thrives on inflation fears, but it also competes with a stronger dollar and higher yields. If rates stay higher for longer, holding non-yielding assets becomes less attractive.

The headline is inflation.

The real story is whether higher inflation reignites the dollar and yields trade or whether investors focus on preserving purchasing power through hard assets.

#Inflation $SPX #GOLD #DXY

1

47

Jun 10

38

Jun 5

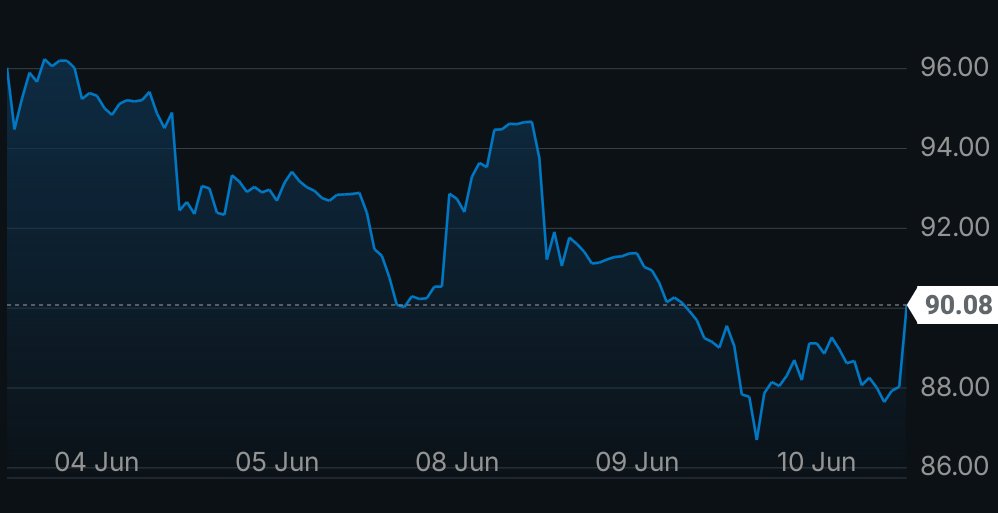

𝗚𝗼𝗹𝗱, 𝗦𝗶𝗹𝘃𝗲𝗿 & 𝗧𝗵𝗲 𝗔𝗜 𝗕𝗼𝗼𝗺: 𝗪𝗵𝗲𝗿𝗲 𝗗𝗼𝗲𝘀 𝗦𝗺𝗮𝗿𝘁 𝗠𝗼𝗻𝗲𝘆 𝗚𝗼 𝗡𝗲𝘅𝘁?

For most of 2025 and early 2026, precious metals looked unstoppable.

Gold printed new all-time highs almost every week.

Silver outperformed nearly every major asset class.

Then everything changed.

ME conflict initially pushed investors toward safe havens. Gold surged, silver followed, and crude oil exploded higher.

But as the conflict dragged on, markets shifted focus.

Higher oil prices fueled inflation fears, stronger economic data pushed Treasury yields higher, and the U.S. dollar regained strength.

The result?

Gold fell from above $5,200 to nearly $4,300.

Silver dropped from above $80 to around $70.

Meanwhile, the S&P 500 and Nasdaq continued climbing on the back of AI, data centers, semiconductors, and software.

𝗪𝗵𝗮𝘁 𝗔𝗰𝘁𝘂𝗮𝗹𝗹𝘆 𝗖𝗵𝗮𝗻𝗴𝗲𝗱?

The bull case for gold was built on four pillars:

• Central bank buying

• ETF inflows

• Geopolitical uncertainty

• Weakness in the U.S. dollar

Three of those pillars weakened simultaneously.

ETF demand slowed sharply.

Central bank purchases remain positive but are no longer accelerating.

The dollar stabilized as investors priced in higher-for-longer interest rates.

Gold didn't suddenly become a bad asset.

It simply became expensive enough that buyers became selective.

---

𝗦𝗶𝗹𝘃𝗲𝗿 𝗜𝘀 𝗔 𝗗𝗶𝗳𝗳𝗲𝗿𝗲𝗻𝘁 𝗦𝘁𝗼𝗿𝘆

Unlike gold, silver is both a precious metal and an industrial metal.

That distinction matters.

The AI boom is not just software.

It requires:

Data centers

Power infrastructure

Electronics

Networking equipment

Advanced manufacturing

Silver remains deeply embedded across many of those supply chains.

Even though solar manufacturers are reducing silver usage per panel, long-term industrial demand remains supported by electrification, AI infrastructure and electronics growth. Supply deficits are also expected to persist.

This makes silver potentially more volatile than gold, but also potentially more rewarding during expansionary economic cycles.

---

𝗧𝗵𝗲 𝗥𝗲𝗮𝗹 𝗖𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗶𝗼𝗻: 𝗚𝗼𝗹𝗱 𝘃𝘀 𝗔𝗜 𝗦𝘁𝗼𝗰𝗸𝘀

This is where investors face a difficult choice.

Why hold gold when AI stocks are compounding revenue at extraordinary rates?

The answer is simple:

Gold is not competing with Nvidia.

Gold is competing with uncertainty.

When investors fear recession, currency debasement, debt problems, or geopolitical shocks, gold becomes insurance.

When investors are optimistic about growth and innovation, capital flows toward equities.

Today, markets are rewarding growth.

That doesn't mean gold is dead.

It means the market is currently paying a premium for future earnings instead of protection.

---

𝗪𝗵𝗮𝘁 𝗟𝗼𝗻𝗴-𝗧𝗲𝗿𝗺 𝗛𝗼𝗹𝗱𝗲𝗿𝘀 𝗦𝗵𝗼𝘂𝗹𝗱 𝗗𝗼

If you already own gold:

Don't panic because of a 15-20% correction.

Gold remains supported by central-bank demand, reserve diversification and long-term geopolitical uncertainty.

If you own silver:

Expect volatility.

Silver behaves like a hybrid of gold and technology-related industrial demand.

The swings will likely remain larger than gold's.

---

𝗪𝗵𝗮𝘁 𝗡𝗲𝘄 𝗜𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀 𝗦𝗵𝗼𝘂𝗹𝗱 𝗗𝗼

A portfolio doesn't need to be all-in on either PMs or AI.

A balanced allocation make more sense.

Conservative Investor

70% equities

20% gold

10% silver

Balanced Investor

80% equities

15% gold

5% silver

Growth Investor

90% equities

5% gold

5% silver

The objective is not maximizing returns.

The objective is surviving multiple market regimes.

---

𝗣𝘂𝗹𝘀𝗲𝟮𝟰 𝗧𝗮𝗸𝗲

The easy money in PMs may already be behind us.

The easy money in AI may also be behind us.

The next decade will likely reward investors who own both productivity and protection.

AI offers growth.

Gold offers resilience.

Silver sits somewhere in the middle.

#Gold #Silver #AI #Investing #Markets #Nasdaq #SP500 #Commodities

What matters. When it matters.

191

Jun 5

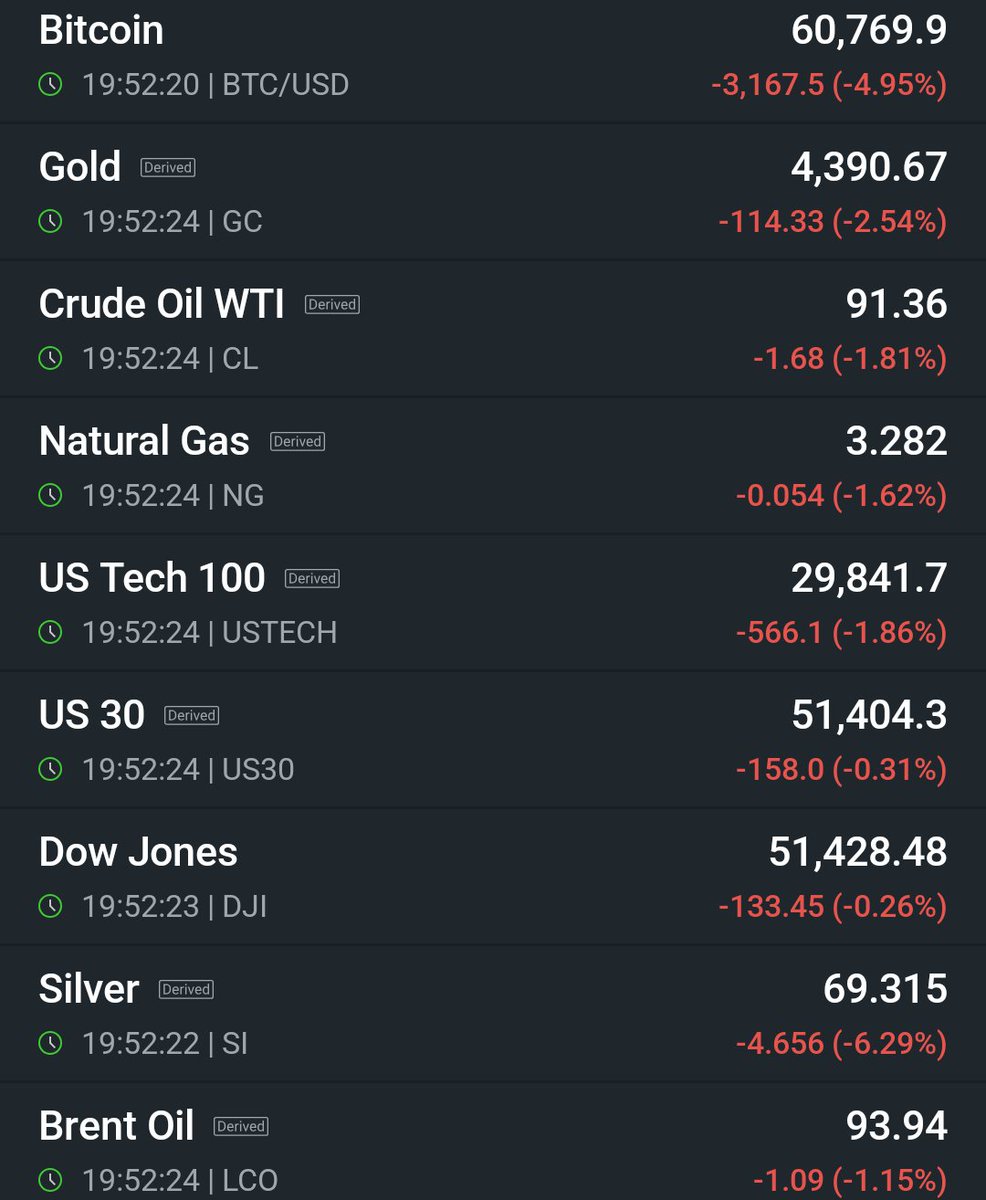

🔴 Bitcoin -4.9%

🔴 Silver -6.3%

🔴 Gold -2.5%

🔴 Crude Oil -1.8%

🔴 Nasdaq 100 -1.9%

Risk assets are down.

Safe havens are down.

Commodities are down.

Days like this are less about fundamentals and more about positioning, leverage, and liquidity.

The market is sending a simple message: cash is king until conviction returns.

#Markets #Macro #Bitcoin #Gold #Silver #Oil #Nasdaq #Investing #Pulse24

85

May 25

84

May 23

1

107

May 23

A crucial moment in the Sprint! 🤯

This is the view from Antonelli's onboard of the earlier moment at Turn 10 💨

#F1Sprint #CanadianGP

1

318

May 23

117