my pronouns protect you, and your pronouns protect me

Joined February 2021

- Tweets 7,886

- Following 163

- Followers 109

- Likes 12,617

402 Photos and videos

Ruf&R retweeted

Feb 18

Nashville teacher allegedly threatened with termination for refusing to read LGBTQ book to first graders.

foxnews.com/media/nashville-…

39

136

269

18,175

Anything you’d like to say about this @MetroSchools @freddieoconnell

10 Nov 2024

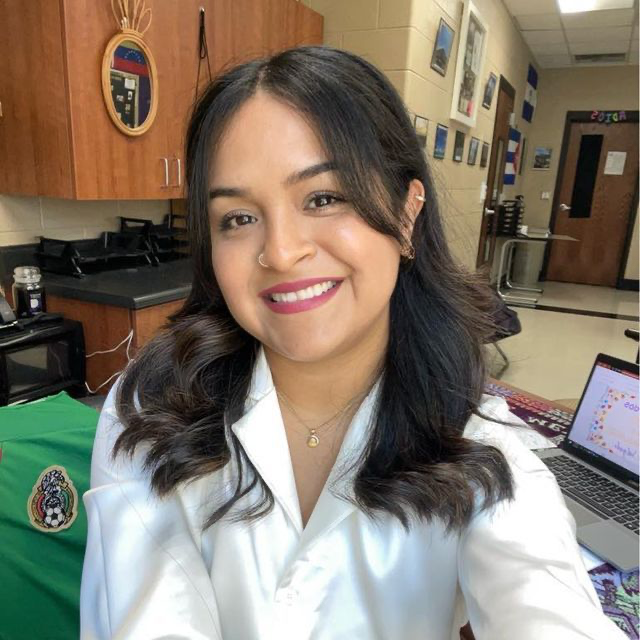

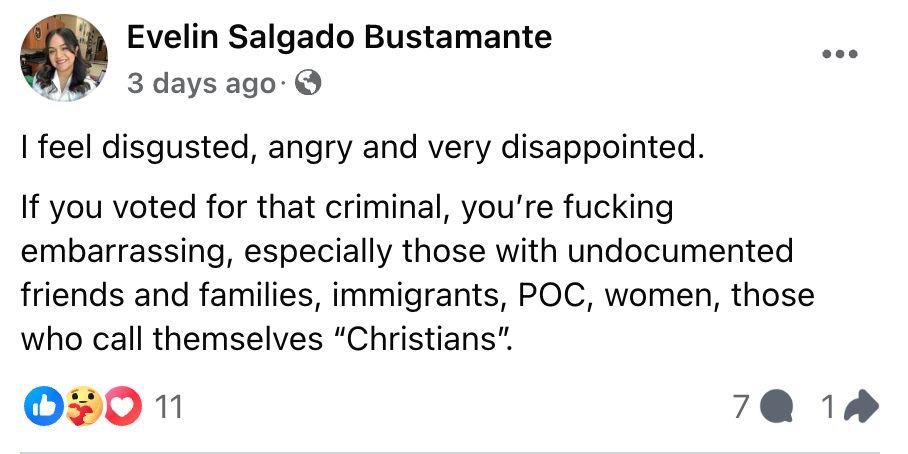

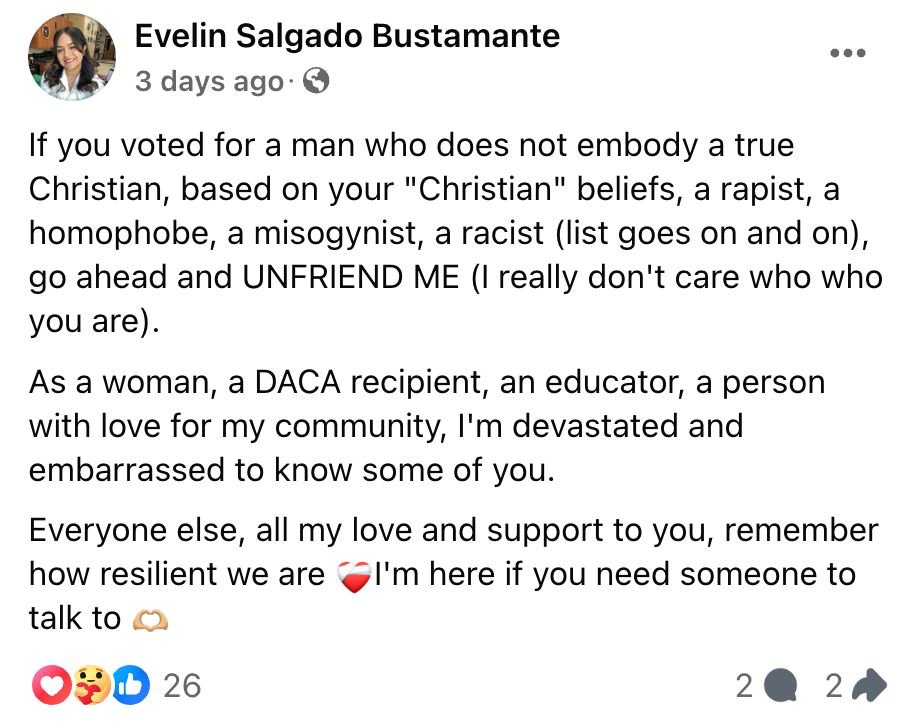

Meet Evelin Salgado Bustamante, a teacher at @MetroSchools in TN. Evelin is very angry at Christians who supported Trump and thinks anyone who voted for Trump is “f*cking embarrassing.”

This woman is in charge of teaching your children.

1

4

1,122

Ruf&R retweeted

24 Aug 2024

Bicyclist Wants To Be Treated Like A Car But Also Be Able To Just Kinda Break The Rules When He Wants To buff.ly/44pHZiS

147

778

7,620

252,838

Ruf&R retweeted

11 Sep 2023

The greatest living American hero. We should have listened.

136

999

4,945

182,887

Ruf&R retweeted

19 Jul 2023

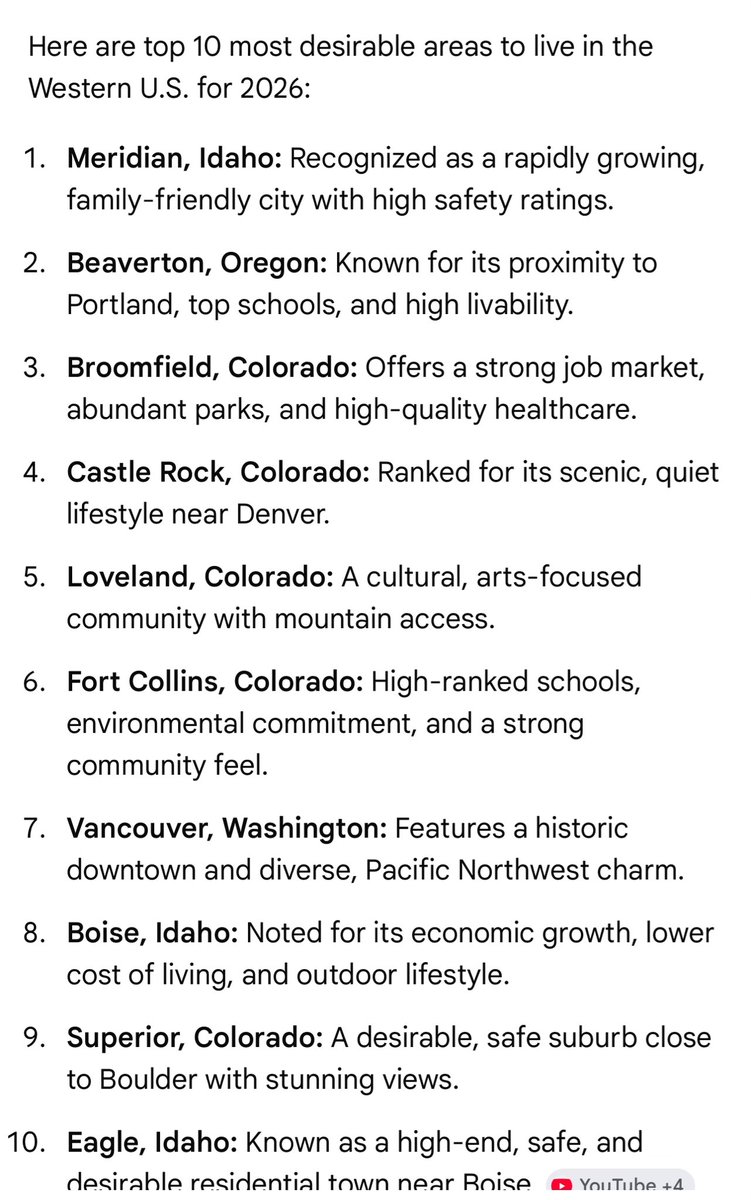

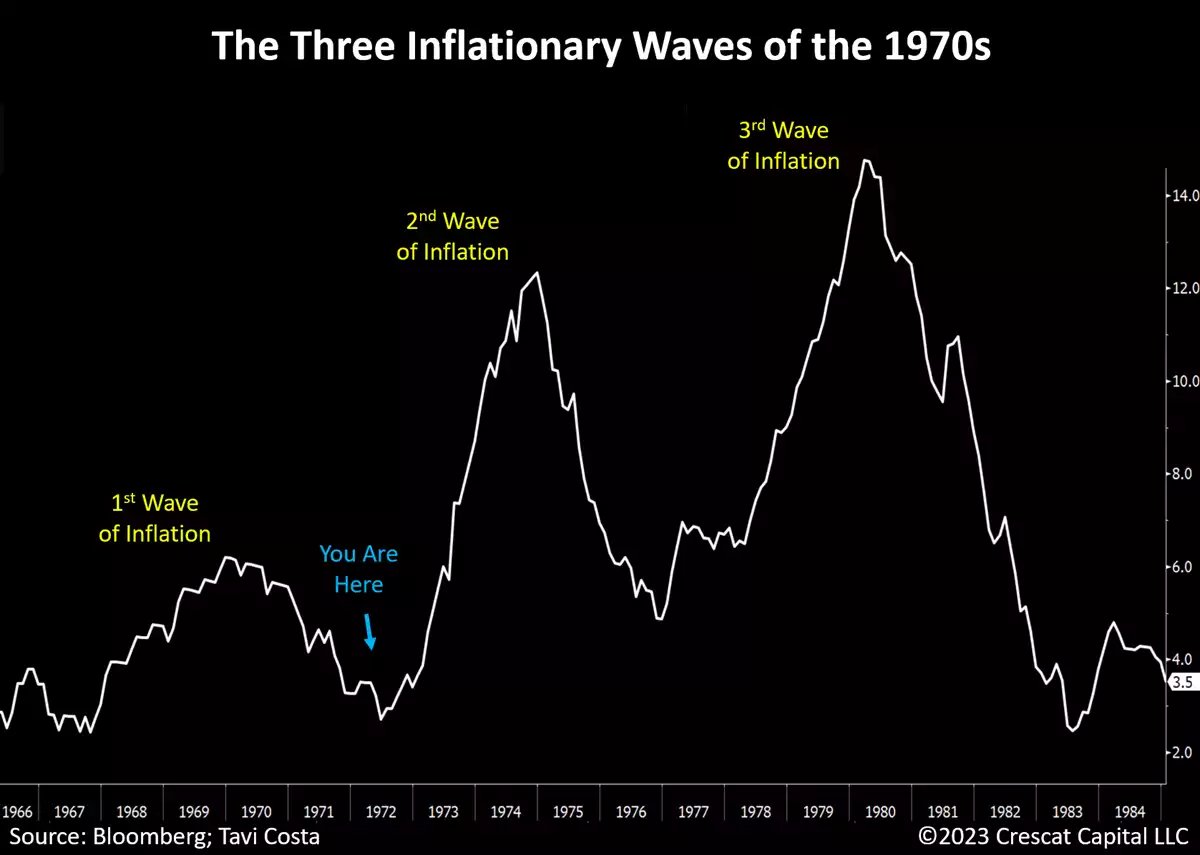

Last week’s CPI report marked a significant milestone as it is the first time in 102 years that we have witnessed twelve consecutive months of declining CPI on a YoY basis.

The last time we experienced that was in 1921 after the Spanish Flu pandemic marking the actual bottom for inflation rates at -15.8%.

Today, after the same monthly sequence of falling CPI, the rate is still positive and above the Fed’s target.

The overwhelming focus on the recent slowdown in inflation appears to be rooted in backward-looking analysis.

In fact:

Since last week’s CPI report, oil has broken out, gold rallied back above $2,000, silver surged, and agricultural commodities appreciated substantially.

While the macro environment today differs from that of the 1970s or 1940s, a lesson from history remains: inflation tends to develop through waves.

We have recently witnessed the conclusion of the first wave and are likely in the process of reaching a bottom in the recent deceleration period, with a new upward trajectory underway.

The primary reason for this is the persistence of underlying issues that continue to drive inflation rates higher:

▪️ Irresponsible levels of government spending

▪️ Escalating deglobalization trends, which necessitate the revitalization of manufacturing capabilities in economies.

▪️ Wage-price spiral, particularly driven by low-income segments of the society

▪️ Ongoing supply constraints due to chronic underinvestment in natural resource industries.

Just as base effects played a crucial role in reducing inflation rates, we anticipate that the opposite effect is on the horizon, with CPI likely to reach a bottom in the near future.

76

336

1,199

309,136

Ruf&R retweeted

4 May 2023

Biden official: It's going to cost trillions of dollars. There's no doubt about it.

Me: So, if the U.S. spent $50T to become carbon neutral by 2050, how much is that going to reduce world temperatures?

Biden official: *No answer*

2,447

7,442

30,664

2,430,101

Ruf&R retweeted

19 Oct 2021

Here are all of the studies that show masks lack statistical effectiveness that @VoteGloriaJ claimed today have been "debunked."

I will post all of these studies, and I look forward to @VoteGloriaJ's response to @JasonZacharyTN linking to the peer reviews that debunk them:

1/

8

123

338

Ruf&R retweeted

19 Oct 2021

Even the trained police dogs know who the aggressors are in the COVID police state and it isn’t us.

543

4,713

16,832

Ruf&R retweeted

11 Oct 2021

Super storm Brandon grounds flights across America and is now disrupting the railways too.

23

131

709

Ruf&R retweeted

7 Oct 2021

“New data coming out of Florida school districts show virtually zero difference between masked vs. unmasked counties, even as Covid-19 cases plummet across the state.”

townhall.com/tipsheet/scottm…

19

479

1,106

Ruf&R retweeted

26 Sep 2021

Hospitals are treating nurses like shit and wondering why there's a shortage. This is a decades long problem exacerbated by a pandemic. This thread is so depressing and frightening.

25 Sep 2021

Senior nurses on my unit are leaving. They have been on this unit for decades and they’re leaving to to elsewhere.

A clue why? Everyone has 9 patients this morning. Manager says she can’t take an assignment but to call her if she’s needed. When we called her all night. 😐🤷🏻♀️🖕🏼

13

22

137

Ruf&R retweeted

25 Aug 2021

"Face coverings are no longer advised for pupils, staff and visitors either in classrooms or in communal areas." gov.uk/government/publicatio…

18

196

601

I think its a fair argument. Hadn’t considered POC at Capitol riots. Have any POC been charged? that’s the only real difference between the two events. One event resulted in actively seeking participants for charges, the other dropped all charges. Jan 6th targeted rage correctly

1

Ruf&R retweeted

14 Aug 2021

Throughout the entire course of this pandemic, only one thing has become crystal clear - this virus is just gonna virus, regardless of man's feeble attempts to stop it. We can realize this and learn to live with it, or we can destroy ourselves trying to do the impossible.

16

121

471

Ruf&R retweeted

12 Aug 2021

“In sum, of the 14 RCTs...three suggest, but do not provide any statistically significant evidence in intention-to-treat analysis, that masks might be useful. The other eleven suggest that masks are either useless—or actually counterproductive...”

city-journal.org/do-masks-wo…

11

23

Ruf&R retweeted

11 Aug 2021

Angry at your school board? Tired of power hungry politicians mandating everything under the sun? Well your ire should be pointed in one direction. At @GovBillLee and @CSexton25 they had and still have the power to end this stupidity the right way, through the legislative process

4

12

40

Ruf&R retweeted

9 Aug 2021

Urge your TN legislators to call a special session and deal with masks in schools, jabs for jobs, and vaccine passports now!

Click on the link to take action!

tennesseestands.org/urge-leg…

3

11

27