OctoGen in Nov. Doing lifeline data dump; Ask.

Joined February 2026

- Tweets 18,253

- Following 81

- Followers 114

- Likes 16,472

664 Photos and videos

You can't go home again....so build a new one.

youtube.com/watch?v=Q_XgghFZ…

1

Magical mushroom music channeling a tea party:

youtube.com/watch?v=ouxo-5tO…

1

Blues Boogie ... Haw...Haw...Haw ...Haw !!

youtube.com/watch?v=jRMzVMe1…

5

ReadOnly retweeted

In the days before women became narcissistic and shut out extended family members, mothers had 50% of the childcare taken off her hands by alloparenting, which allows her to labor and earn income. Mothers can still do that if they learn to stop alienating entire family networks.

1

5

26

838

ReadOnly retweeted

Trump on Iran: Hormuz Strait will be open to all immediately after deal is signed

87

27

461

51,539

ReadOnly retweeted

RIP Feminism. My latest in this weekend's @DailySignal.

"Feminism is not dead because women no longer seek purpose—it is fading because it misidentified where that purpose comes from. It promised fulfillment through autonomy and self-elevation, but what it often produces is restlessness and dissatisfaction."

1

3

27

2,776

ReadOnly retweeted

Jun 13

Delicious.

Jun 12

The sheer scale of a trillion dollars can be hard to comprehend. Let me put it in perspective. You would be able to buy 42 miles of high speed rail in California with that much money.

10

17

252

14,526

ReadOnly retweeted

"Wage gains have been wiped out since Trump took office," per Axios

137

602

5,390

222,581

ReadOnly retweeted

A school district in Louisiana says some of its teachers will receive bonuses of more than $50,000 this year thanks to increased tax revenue linked to a Meta data center, per WSJ

145

132

2,659

299,374

ReadOnly retweeted

The algorithm pre-decides how many people will like it, then only shows it to that many people.

Literally nobody else among your followers sees it.

I posted 3 hours ago about my latest book, and of my 17k followers, X is telling me only 57 people saw it. This platform is broken.

4

3

27

638

ReadOnly retweeted

We need an image like this for every western nation so we can explain the situation very slowly for the normies.

7

13

119

1,169

ReadOnly retweeted

This could eventually play out as the mother of all "three fan principles" E&M, 5th edition, pages 257-259.

Shown on right in picture is from original 1948 printing, leather bound from John Magee's library

Editions past #6 have been altered not to be trusted

31

14

284

46,460

ReadOnly retweeted

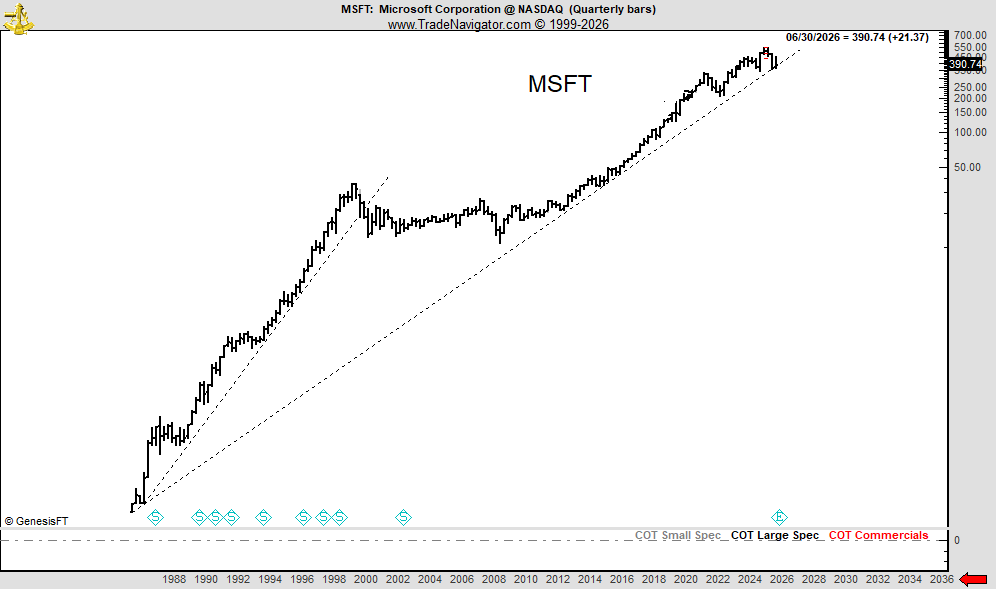

I look at this differently

There is risk per trade at the time of trade entry using initial stop

compared to

Risk per trade when a protective stop is advanced with a winning trade

and

there is total composite risk of all positions held

and

there is highly correlated risk.

I may hold five to eight positions at any given time

But, they may be entirely uncorrelated such as a portfolio of short grains in Europe, long a grain in Canada, stock index in Japan, Sugar in London, Copper in New York and interest rate in Chicago

My max initial risk per trade is 70 basis points - and I try to reduce this to 35 basis points within a week

My max risk on highly correlated trades is 200 BPs (e.g., Bonds and Notes long or Beans and Meal short) and that is composite initial risk which does not happen very often

The real risk belongs to stock swing or position traders because in times of extreme volatility due to a news event that can be ALL ONE TRADE

My max initial risk per trade is 70 basis points - and I try to reduce this to 35 basis points wB

I am more concerned about risk per trade anERY

1

1

30

3,610

ReadOnly retweeted

If people don’t like their sexed bodies, it doesn’t mean they’re in the wrong body. It means they need therapy in order to get used to their body because they’re going to be stuck with it for the rest of their lives. I’m not sure why this isn’t obvious to some.

103

232

2,193

20,763

ReadOnly retweeted

🚨 BREAKING: In a bombshell moment, Florida Gov. Ron DeSantis ABOLISHES H-1B VISAS from being used at state universities

"We can do it with Florida RESIDENTS or AMERICANS! If we can't? Then man, we need to REALLY look deeply at what's going on with this situation!"

DeSantis exposed that H-1B AUDITS found colleges were bringing in Chinese people on visas to talk to students about "public policy," among other issues.

"Why do we need to bring someone from CHINA to talk about public policy?!"

"I am directing today the Florida Board of Governors to PULL THE PLUG on the use of these H-1B visas at our universities."

HUGE! I LOVE my state! @GovRonDeSantis ☀️

106

1,122

6,008

89,194