Sovereign banking stress — the data that moves before markets do. Monitoring 30 countries. Real purchasing power for 190 currencies. Reserve Letter every Sunday

Joined May 2026

- Tweets 1,229

- Following 61

- Followers 214

- Likes 1,464

14 Photos and videos

Pinned Tweet

Banking fundamentals led every major crisis of the last 20 years. The data was always there — months before markets moved. Most people weren’t watching it.

We are. 🧵

4

10

1,951

RT @RealDollarValue: @anasalhajji @tanvi_ratna connected this early. Ukraine strikes on Russian refineries and ports weren’t a problem for…

1

Whoever planned it wins and the planning ran across three separate tracks simultaneously.

Track one: George Mitchell spent 17 years drilling the Barnett Shale while his own engineers told him he was wasting money. His breakthrough well came in 1997. By 2011 the US passed Russia as the world’s largest gas producer. By 2018 it passed Saudi Arabia on oil. OPEC launched a price war in 2014 specifically to kill shale. Shale survived and got cheaper. The energy foundation was built before anyone called it dominance.

Track two: Weeks after 9/11, a Pentagon memo described taking out seven countries in five years — Iraq, Syria, Lebanon, Libya, Somalia, Sudan, finishing with Iran. Wesley Clark revealed it in 2007. Six of seven are now in various stages of collapse or regime change. The list was about who controls Middle East energy architecture. Iran was always last.

Track three: In 2014 the Ukrainian government fell. Victoria Nuland’s leaked call documented US involvement in who would lead what came next. Yanukovych fled to Russia. Ukraine pivoted West. Russia annexed Crimea. The conditions for what followed were set. Russia invaded Ukraine February 2022. Seven months later Nord Stream was destroyed — not damaged, destroyed. Europe’s direct pipeline link to Russian gas eliminated permanently. The continent had no alternative at scale. US LNG was the only answer. EU imports doubled. By 2023 the US was the world’s largest LNG exporter. The $750B Turnberry agreement locked Europe into 15-year US contracts before Hormuz ever closed.

February 2026 — Hormuz closes. Gulf market share routes to US suppliers. Two chokepoints removed in four years. One pipeline, one strait. Both accelerating the same destination: US energy as the structural anchor of every allied economy on earth.

Anas Alhajji is right. Whoever planned it wins. The plan predates every politician claiming the trophy. The presidents are the vehicles. The machine runs across decades.

Jun 13

🔴I was wrong to assume the Trump Administration opposed Ukraine striking Russian refineries and ports out of concern for higher oil prices.

🔴It turns out Ukraine is actually supporting the Trump Administration’s "Energy Dominance" agenda.

🔴By disrupting Russian exports, Ukraine is helping create opportunities for U.S. petroleum products to replace Russian ones in markets around the world—one country at a time.

🔴The U.S. has already captured the Russian market share in more than eight countries, none of which are in Europe.

🔴The same is happening now with the Hormuz Crisis: Capturing markets in Africa from Arab countries.

🐺 So the Trump Administration has no idea inventories are dropping? Yeah, sure

Link: afalhajji.substack.com/publi…

1

2

178

LatAm golden age is the hemisphere consolidation made visible at the company level. Energy exports up, banking stress resolving into political alignment, capital flows rotating toward the supply side of the disruption. The companies in that directory are operating inside an architecture that was built before they knew it existed.

Jun 12

Latin America is having its golden age, and we built a public directory of the companies leading it.

Straight Outta LATAM is a hub where global companies find the ones already operating here, and where LATAM teams find each other.

2

115

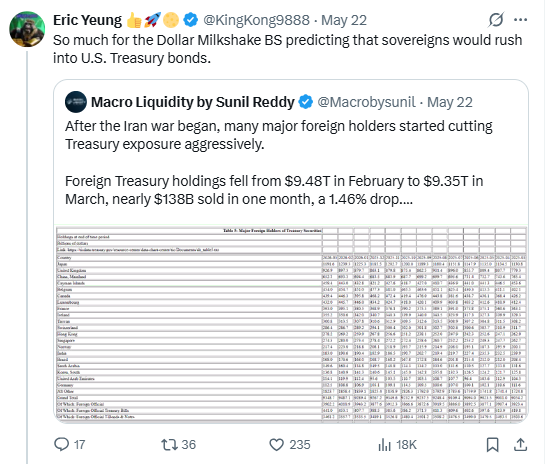

Brent is right — foreign holders selling Treasuries to get dollars is the mechanism, not the refutation. The dollar is the first destination. Always has been. Bond Gravity runs the second leg: once acute stress peaks and the disinflation signal clears, that same dollar liquidity finds duration. Yields peak, the curve responds, and $3T in sidelined mortgage demand releases. The Treasury selloff isn’t the end of the thesis. It’s the capital loading the spring. Same flow, two sequential destinations.

Jun 10

Imagine thinking that the Milkshake is bullish treasury bonds when the entire Milkshake was predicated on Treasury yields rising and Treasury bonds falling.

And then imagine not understanding the reason treasury bonds are being sold is because the sellers need...dollars.

😅

220

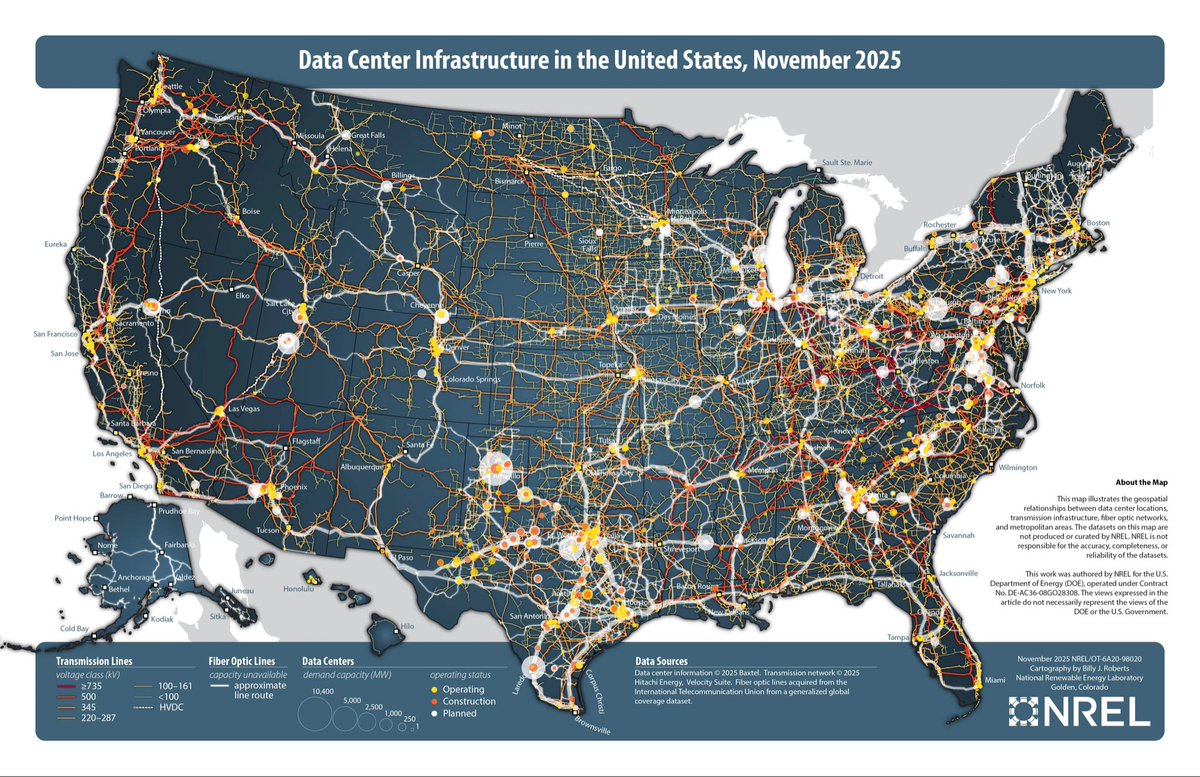

The US government is building the energy infrastructure of AI dominance in real time and natural gas is the foundation.

In July 2025, Trump signed EO 14318 Accelerating Federal Permitting of Data Center Infrastructure. Fast-tracked permitting, federal land, explicit inclusion of natural gas as qualifying energy infrastructure. In March 2026, seven major AI companies signed the White House Ratepayer Protection Pledge committing to build their own generation capacity.

The numbers: 36.6 gigawatts of data center capacity currently under construction. 201.5 gigawatts in planning. Natural gas planned capacity up 24 gigawatts since January 2026 alone. Non-renewable energy additions surged 71% from 2025 to 2026 while renewable growth flatlined at 2%. Natural gas grid connection costs $24/kw vs $253/kw for solar. Utilities have a 5-year wait list. Data centers are going behind the meter building their own gas plants on site. SoftBank broke ground on a $33.3 billion, 9.2 gigawatt gas plant in Piketon, Ohio on former DOE land to power a 10 gigawatt data center. The US needs 51 gigawatts available to AI data centers by 2027 to retain 75% of global AI compute inside its borders.

Meanwhile the export architecture locked in simultaneously. The EU committed $750 billion in US energy — 39 million tonnes of LNG per year under term contracts. Japan committed $550 billion — 7.5 million tonnes of new contracts signed in 2025 alone, indexed to Henry Hub. South Korea committed $100 billion — 12 million tonnes per year representing a quarter of its total LNG demand, with KOGAS, POSCO, and Hanwha all signing long-term US supply agreements. The US secured $57 billion in Indo-Pacific energy deals in March 2026 alone. Total US LNG exports hit 15 Bcf/day in 2025 forecast to exceed 18.1 Bcf/day by 2027. The US is now the world’s largest LNG exporter, ahead of Australia and Qatar.

Two structural demand anchors for the same commodity. EU, Japan, and South Korea locked into US gas through trade architecture. AI data centers locked into US gas through physical infrastructure. Both permanent. Both dollar-denominated. Both running simultaneously. The dollar isn’t defended by diplomacy. It’s defended by what the world needs to compute and what every allied economy needs to run.

1

91

Triffin said reserve status would drain the issuer — France sent a warship to Manhattan to haul its gold home. Nixon closed the window before the vault hit zero. Then Simon flew to Riyadh. He didn’t save the dollar. He reversed the dilemma. Gold anchored dollars to a finite vault that could be emptied. Oil anchored dollars to a commodity every economy on earth buys every single day — no alternative, no opt-out. The recycling loop followed: petrodollars back into Treasuries, financing the deficit, deepening the dependency. $14.5 trillion in dollar liabilities outside the US today. Every EM restructuring runs through dollar instruments. Every energy invoice clears in dollars. Triffin identified the trap in 1960. Simon turned it into the weapon in 1974. That’s the entire de-dollarization story.

Should be a shrine devoted to William Simon in DC bc he closed greatest deal in U.S. history. His negotiations transformed a fledgling currency that had lost its anchor to Gold (Triffins Dilemma) into a Dagger that can strike the heart of any other country's Economy. 👇

research.santiagocapital.com…

1

216

World Dollar Value | Sovereign Risk | Macro Intel retweeted

Three explosions on the main Dagestan gas pipeline. NSR running one sanctioned Arc7 carrier. Black Sea export terminal hit by Ukraine. Now the southern Russian gas corridor. Every alternative route to replace Hormuz volume is under pressure simultaneously. The alternative infrastructure isn’t just constrained — it’s being systematically targeted.

2

2

241

World Dollar Value | Sovereign Risk | Macro Intel retweeted

AI needs 24/7 baseload power that renewables can’t provide. Natural gas fills it. US is the world’s largest gas producer — Turnberry locked in EU demand for 15 years, AI is now locking in domestic demand permanently. Two structural demand anchors for the same commodity building simultaneously. The energy architecture thesis just got a second engine.

1

3

500

Unit labor costs 0.5%. The inflation isn’t in wages — it’s in container rates up 109%, jet fuel 78%, PPI 6.0% from a closed strait. Wall Street is treating a shipping lane disruption as an overheating labor market. The model and the shock are completely mismatched. Pavlovian is the right word for it.

Jun 9

As Wall St keeps pushing rate hikes!

Wall Street’s Keynesian reflex has become a substitute for analysis: every strong jobs print is lazily labeled ‘inflationary’ and automatically translated into ‘the Fed must hike,’ with almost no serious engagement with the underlying cost structure.

Unit labor costs in Q1 2026 are rising at roughly 0.5% year‑on‑year, hardly the stuff of a wage‑price spiral and yet the Street clings to a narrative that treats employment growth as inherently dangerous rather than interrogating productivity, margins, and real wage trends.

What passes for ‘macro’ is increasingly just Pavlovian trading around payroll headlines, while the actual labor‑cost data that should anchor the inflation debate is ignored because it doesn’t fit the story. Yes Wall St lives in a post factual world.

1

3

254

RT @RealDollarValue: @anasalhajji And the futures market ran this calculation weeks ago. December WTI $75, spot $91 — the gap between suppl…

1

World Dollar Value | Sovereign Risk | Macro Intel retweeted

The story isn’t the designation — it’s the date. June 30, DoD prohibited from contracting with every entity on this list. Alibaba, Baidu, BYD, CATL, Tencent, Huawei. 22 days. Every compliance department at every US-aligned institution runs the same screen. The decoupling has a countdown, not just a direction.

1

3

541

World Dollar Value | Sovereign Risk | Macro Intel retweeted

Concentrated gains, speculative activity rising, 70% of bear indicators triggered. The crowding in semis already showed what happens when the unwind starts — SOX -10% single day. BofA is warning on the broader market. The question isn’t whether it corrects. It’s where the capital routes when it does.

1

3

1,289

World Dollar Value | Sovereign Risk | Macro Intel retweeted

Fields without pipes, pipes without fields — both stranded without the chokepoint between them. The Middle East has the fields. The US controls the chokepoint architecture and is building the alternative infrastructure simultaneously. Turnberry, Venezuelan compliance, Mozambique. The closure and the fix are the same event.

3

2

316

Peace resolves the war. It doesn’t reverse the 15-year LNG contracts, Venezuela oil restructuring, or Colombia energy recovery. Americas EM was already repricing toward the new energy architecture before the first missile flew. The EM line hides which half of the world is on which side of it.

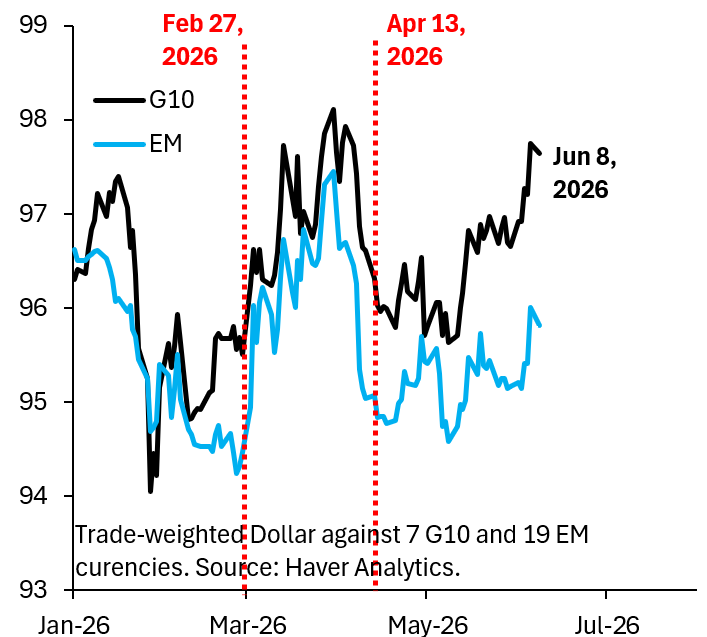

Jun 8

There's a very interesting decoupling between the Dollar vs the G10 (black), which is near its highs, and USD vs EM (blue), which is much weaker. The signal that matters for future Dollar direction is the latter. USD will tumble as soon as we get peace...

robinjbrooks.substack.com/p/…

1

1

11

8,093

World Dollar Value | Sovereign Risk | Macro Intel retweeted

The 1980s collapse was Saudi Arabia flooding in ‘85 to reclaim share — not the war itself. This time spare capacity routes through US export infrastructure, and OPEC can’t flood without destroying their own fiscal breakevens. Same war logic, different supply architecture. That difference is the whole trade.

1

2

17

1,291

World Dollar Value | Sovereign Risk | Macro Intel retweeted

H-1B fraud probe closes the skilled worker pipeline. AI replacing entry-level knowledge work. Green card pathway frozen. The knowledge worker labor market is compressing from both ends simultaneously. Dallas real estate is pricing what the NFP headline isn’t showing yet — white-collar demand destruction is already running.

1

2

489

World Dollar Value | Sovereign Risk | Macro Intel retweeted

DoubleLine and Oaktree buying AI bust protection while VXN/VIX just hit the highest daily close in 8.5 years. Tech leverage is unwinding ahead of the broad market. The credit heavyweights are positioned for what equity hasn’t priced yet. The sequence runs credit stress first, then the headline number.

3

7

356

World Dollar Value | Sovereign Risk | Macro Intel retweeted

China’s gold reserves fell $3.4B in May — mostly price depreciation, not selling. Gold crashed on Friday’s NFP as the dollar reasserted. Safe haven order: dollar first, Treasuries second, gold third. The de-dollarization trade isn’t in the gold price. It’s in the $14T in dollar liabilities still climbing outside the US.

2

5

618

World Dollar Value | Sovereign Risk | Macro Intel retweeted

SK Hynix is Nvidia’s HBM supplier. The cooperation plan is Korea protecting the one asset keeping its tariff exemption alive — chip dominance. Chinese memory challenging both simultaneously. KRW 1474 while KOSPI runs 226% YoY. The exemption and the currency don’t both survive the same outcome.

1

5

1,286

World Dollar Value | Sovereign Risk | Macro Intel retweeted

Not arguing prices rise — December futures at $75 already price demand destruction. The question is who controls the supply response. In ’85 it was Riyadh flooding to reclaim share. This time spare capacity routes through US export infrastructure. Same price logic, different control architecture.

1

9

566