Joined December 2023

- Tweets 10,006

- Following 300

- Followers 298

- Likes 158,971

1,030 Photos and videos

Robert Alan retweeted

May 31

On a humid summer morning, two young men crossed a border.

Both sought opportunity. Both dreamed of a better life.

One crossed from India into the United States. He was greeted with visas, work permits, diversity programs, and endless talk of the “American Dream.” Politicians, activists, and corporations insisted he was the future of America, that his presence made the country stronger, that questioning his right to be there was “intolerant.”

The other crossed from Bangladesh into India. He was met with barbed wire, detention camps, mass deportations, and politicians declaring he was a threat to jobs, culture, and national security. Indian leaders said their borders must be protected, their workers defended, their resources reserved for their own people.

Same dream. Same reason for crossing.

Two very different standards.

India lectures America about compassion while preaching nationalism at home.

They demand open doors from us, yet slam them shut on their neighbors.

If the Indian Dream for Bangladesh is prison camps and exclusion,

why should the American Dream for India be limitless opportunity?

48

762

2,269

35,981

Robert Alan retweeted

May 25

When I left Texas at 18 to join the Army, they told us if we fought overseas, we’d be preserving our way of life back home. Twenty years later, I finally came back…

…and now Texas is just a bunch of Indian shops, Afghan markets and halal stores.

This is my state, but it feels so far from home.

Is this really what we fought for?

1,793

10,622

35,034

522,283

May 21

One of the most noble goals ever described for mankind

God's speed

May 19

NEWS: Elon Musk laid out SpaceX's core mission in precise terms during his Forbes interview, describing the specific test he uses to define a genuinely self-sustaining civilization beyond Earth.

If resupply ships from Earth stop arriving for any reason, does the civilization on the Moon or Mars continue to grow or does it collapse? Passing that test is the actual goal, not simply putting humans on another planet.

To reach it, Elon estimates humanity needs to deliver roughly 1 million tons of cargo to the Moon or Mars to build sufficient industrial capacity.

He was careful to define what multi-planetary actually means. It is not about leaving Earth and relocating somewhere else. That would simply be a single-planet civilization in a harder place to live. The goal is for humanity to extend outward while keeping Earth intact, eventually becoming a spacefaring civilization spread across multiple worlds.

SpaceX's Starship, targeting full reusability as early as this year, is the vehicle Musk says makes the million-ton goal physically achievable. He described this as a "fundamental breakthrough" he hopes to see happen in 2026.

2

103

Robert Alan retweeted

Apr 11

Erst wenn das letzte Auto am Straßenrand verstummt, die Firmentore endgültig verriegelt sind, die Heizkörper kalt und der Kühlschrank nur noch gähnende Leere zeigt – erst wenn der Hunger die Kinder nachts weinen lässt und die Familie schlaflos in der Dunkelheit liegt – werden die Letzten begreifen: Sie haben viel zu lange zugesehen.

Sie haben zugesehen, wie die Grundlagen dessen, was ein Leben lebenswert macht, still und systematisch zerlegt wurden.

Sie haben zugesehen, wie Fleiß bestraft, Leistung verhöhnt und Verantwortung zur Last erklärt wurde.

Sie haben zugesehen, wie die Lichter einer ganzen Zivilisation langsam, aber unaufhaltsam erloschen – und haben geschwiegen, weil es bequemer war, den Blick abzuwenden.

Erst wenn die eigene Not sie endlich erreicht, wenn die abstrakten Warnungen zu bitterer, greifbarer Wirklichkeit geworden sind, werden sie verstehen, dass sie selbst, durch ihr langes Schweigen, durch ihre Feigheit vor der Wahrheit und ihre Bereitschaft, sich täuschen zu lassen, den Untergang mit ermöglicht haben.

218

2,233

6,588

75,789

Robert Alan retweeted

Apr 11

One wrong move by government here, and you will see, at the very least, 250k Irish people descend on the capital in a blink.

They must step down, there is no other way.

I cannot see another way.

We have already heard the warning of using the army against its own people.

We have heard the threat that they will come for the protestors after the protest ends.

We have then seen the attempted character assassinations on the protest leaders.

None of this has worked an iota as every single person in this country, outside of the political paywall and even within, is wide awake to it.

These threats, as well as being pitiful, are now futile.

Where else do they think they are going here?

Government, you have no more moves.

You’re going nowhere but out I am afraid.

It is check mate. The gig is up.

I don’t condone it, I don’t call for it, just calling it as I see it.

Sláinte 🥃⚔️

Apr 10

Irish Fuel Protest in numbers 🚜🚚🚌🇮🇪

Government Cabinet TDs: 15

Gardaí: 14,564

Army soldiers: 6,900

Prison spaces: 4,736

Farm Workers: 300,000

Haulage Workers: 30,000

The Government can't win this fight...

1,635

9,377

52,449

2,005,315

Robert Alan retweeted

Mar 7

Hi @PaloAltoNtwks!

This is a heads-up before your legal team gets contacted early next week, and possibly on Monday.

Your employee is in the video. His name is Madhu Raju, and he has been a Cloud Network Security Engineer at your company since June 2025.

As you can see, his video dancing at the World War 2 memorial in Washington, DC has over 1 million views on @X alone. It was also featured on @ndtv (India's CNN) and on the @timesofindia (India's New York Times). After the immense backlash, Madhu Raju took down all his social media accounts.

He also owns and operates a dance studio in Dallas named MAD Dance. He took down the studio's X profile, Instagram page, and website.

Fortunately, by the time he figured it out, my good friend @CyberGreen09 had already archived everything and built a dossier on him. He will be reported to the @StateDept on Monday morning for visa violations that will result in his visa being revoked.

You now need to do damage control. It is bad optics that you are hiring an H-1B visa holder in 2026. It is even worse that you are hiring an H-1B visa holder who is disrespecting veterans who died for America during the Second World War. My grand-uncle died liberating the Netherlands, and I was disgusted watching this video.

If you fire this employee and issue a statement, it will help repair most of the damage.

If you want to turn this into a positive public relations opportunity, hire an American for this role. There have been thousands of layoffs in the technology sector, leaving many unemployed.

You have my word and commitment that I will personally look for a fantastic American Cloud Network Security Engineer if you fire him. You will get free promotion, and I am sure that other individuals and organizations on X will be happy to do the same.

2,060

4,975

31,974

4,788,911

Robert Alan retweeted

Feb 22

What would America look like if 55 million Visas were cancelled?

If 55 million visas were cancelled overnight, America would change in ways few could imagine.

At first it would look chaotic. Hospitals short on nurses. Tech firms unable to staff support teams. Crops left to rot because migrant labor vanished. For a few months, the headlines would scream collapse. But then something else would happen.

Wages would climb. Trades and apprenticeships would surge. Colleges that depended on foreign tuition would close, but community colleges would thrive again as Americans re-trained. Housing prices in major cities would fall for the first time in decades. Renters would finally have leverage. Families that were priced out could buy homes again.

The GDP might dip at first, but the money would start circulating locally. People who thought they’d never matter in the economy would suddenly be needed again. The country would remember how to build, grow, fix, and teach without importing labor. It wouldn’t be easy, but it would be ours.

(U.S. Bureau of Labor Statistics, 2024; DHS Yearbook of Immigration Statistics, 2023; Borjas, G. “Labor Market Effects of Immigration,” NBER 2018; U.S. Census Bureau, 2024 ACS; Institute of International Education, 2024 Open Doors Report.)

196

1,172

4,675

65,838

Robert Alan retweeted

Dear, @RepThomasMassie

By popular demand and seemingly obvious logical strategy, I am hereby offering to make the most BANGER 🔥 campaign ad for you for absolutely FREE.

What they are doing to you and the evil behind it has never been more full on display. It is so far beyond political discussion that I barely have words and I honestly fear for your safety, let alone your success.

Mr Massie, you have my word that I will make you a campaign ad so brutal, Mariam Adelson will be begging me to join her team and take her $500k tomorrow. I won't because I too value humanity and honesty and still have a soul.

You have stood mostly alone in showing the world that there is no price worth your soul. That deserves more than applause, it deserves HELP.

As a big and sincere "THANK YOU!" for all you've done for this country by simply being honest, brave, and exposing corruption, I will make for you the kind of propaganda that they're paying hundreds of thousands of dollars for and I will do it BETTER (because TRUTH is easier to sell) and for you, Mr Massie, I will do it for absolutely FREE.

I have a proven track record, you've seen my work, PLEASE, let's talk. DM me.

And to everyone else, if you want to see this happen, please share this until it is seen. #YouAreThePower

#MassieAF 🇺🇸

252

1,902

9,261

210,921

Robert Alan retweeted

24 Dec 2025

We keep seeing charts comparing “wealth by generation,” and they almost always spark the same debate...and most of them are fundamentally misleading.

They compare wealth levels, not wealth *growth*, and stack generations with wildly different amounts of time in the system. Putting Millennials’ 20 years of accumulation next to the Silent Generation’s 80 years creates calendar illusion.

When you normalize the data properly, aligning generations by age, use per-person wealth, adjust for inflation, and compare 5-year lifecycle growth, a clear pattern emerges:

No younger generation is likely to replicate the Silent Generation’s wealth growth curve. Not because they’re worse with money, but because the conditions that created that curve no longer exist.

The Silent Generation benefited from strong real wage growth, affordable housing and education, employer-backed pensions, low healthcare risk, and decades of steady asset appreciation. They entered the economy before asset inflation took off and were able to compound early and uninterrupted.

Later generations entered a different system: higher housing and education costs, the disappearance of pensions, greater exposure to market volatility, and rising healthcare risk. Asset inflation now rewards incumbents, not entrants.

This doesn’t mean younger generations can’t build wealth. It means their growth curves are structurally flatter, especially early in life. Compounding starts later, gets interrupted more often, and depends far more on access to capital than on effort alone.

The Silent Generation’s curve wasn’t normal. It was exceptional, shaped by timing, policy, and structure.

If we want future generations to see anything like it again, it won’t come from better personal finance advice. It would require structural change.

16

3

159

24,669

Robert Alan retweeted

2 Dec 2025

The Trump administration should use the leverage of withholding federal funds to force Oregon to let her citizens separate and join Idaho, as we have voted to do. Defrauding SNAP is but one of the many abuses the state has perpetrated against the people of Eastern Oregon.

2 Dec 2025

🚨 BREAKING: USDA Secretary Brooke Rollins says she will be moving to HALT federal funding to states who refuse to turn over SNAP data to help root out fraud

“21 states including California, New York, and Minnesota, blue states continue to say no. As of next week, we have begun and will begin to stop moving federal funds into those states until they comply.”

2

14

69

1,530

Robert Alan retweeted

2 Dec 2025

If the Chiefs make the playoffs, I'll send someone who retweets this $200 or their choice of a jersey.

(Must be following)

#ChiefsKingdom

63

1,108

938

49,427

Robert Alan retweeted

13 Nov 2025

I’ve read the Epstein emails and my takeaway is this: The real story is the way the media and major institutional figures talked with him. My conclusion after reading is that the elite will face a true revolt from normal people in this next generation. Let me explain why…

It’s crystal clear now that our country and our major institutions have been run for decades (if not longer) by mostly deranged, hedonistic, incestuous elites who play their roles in these big institutions to give the veneer of a "system" with checks and balances. Such a system no longer seems to actually exist. It’s all rigged for their benefit. You can’t argue otherwise, not intelligently at least. Base level voters from left and right can see this now.

The media is bought and paid for. The academic thought leaders are mostly scumbags. The money men are mostly deviant weirdos and 98% of the politicians are uniparty figures who play roles because they’re narcissists who crave attention and power. It’s all grossly transparent now. Many of us know this but it’s worse for the next generation and here’s why I think they’ll eventually revolt unless something major changes…

All of this has accelerated as our dollar became less valuable, jobs became harder to get less rewarding for young people, homes priced out new generations, young people got lied to and saddled with six figure debt at 17 or 18, then they watched their local towns hollowed out and filled with people who won’t even be bothered to speak English. But… in one act of miraculous wonder, the internet has given us all access to long forbidden or censored knowledge and the ability to mass communicate the truth with one another.

Historically, this combination doesn’t work out well for the elite. The gravy train and good times for them always stop at some point.

For that reason, I think the next generation reorients the hierarchy of power in a manner we haven’t seen in a very long time. The only question in my mind that’s unanswered is whether this happens peacefully under the appearance of democratic elections or in a not so peaceful way. I hope it’s peaceful but I’m not convinced it will be.

Agree or disagree?

420

793

3,897

159,023

Robert Alan retweeted

12 Nov 2025

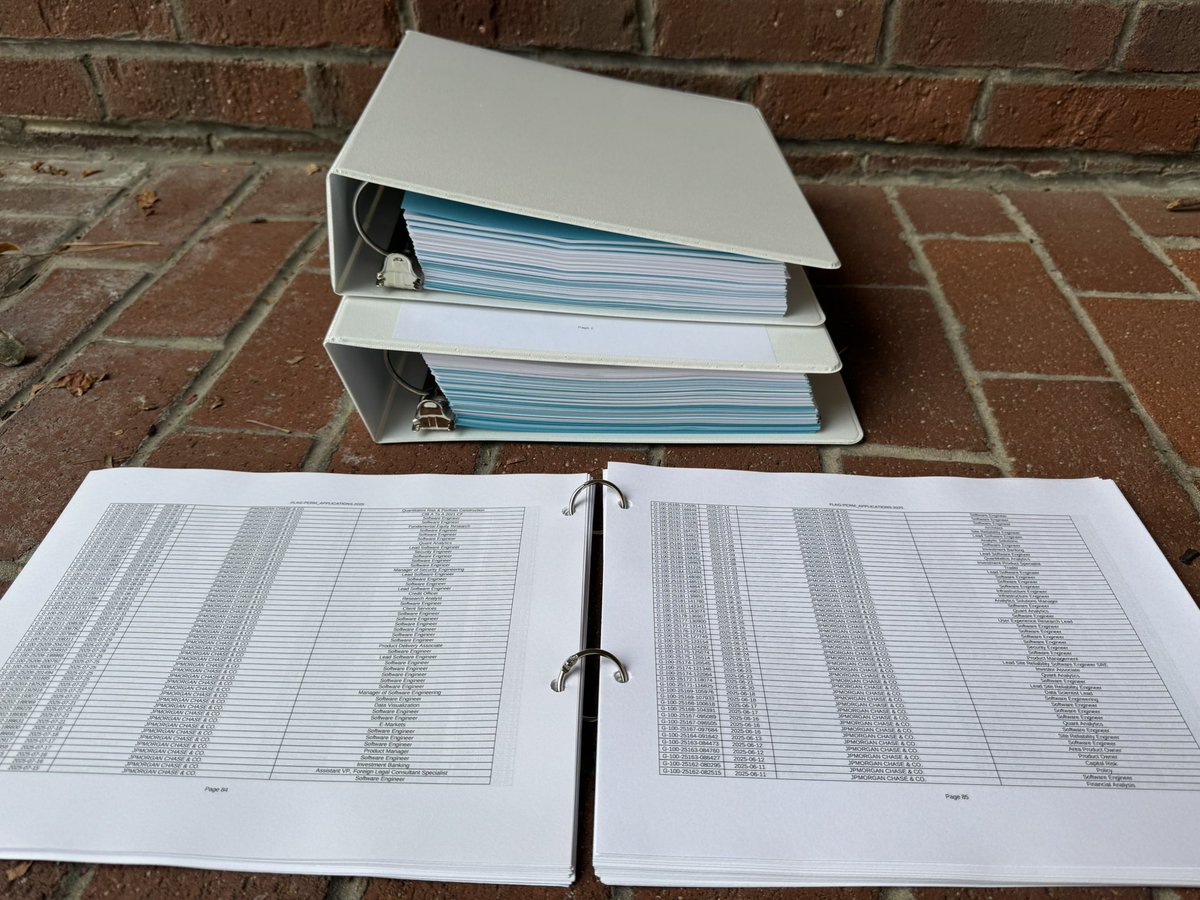

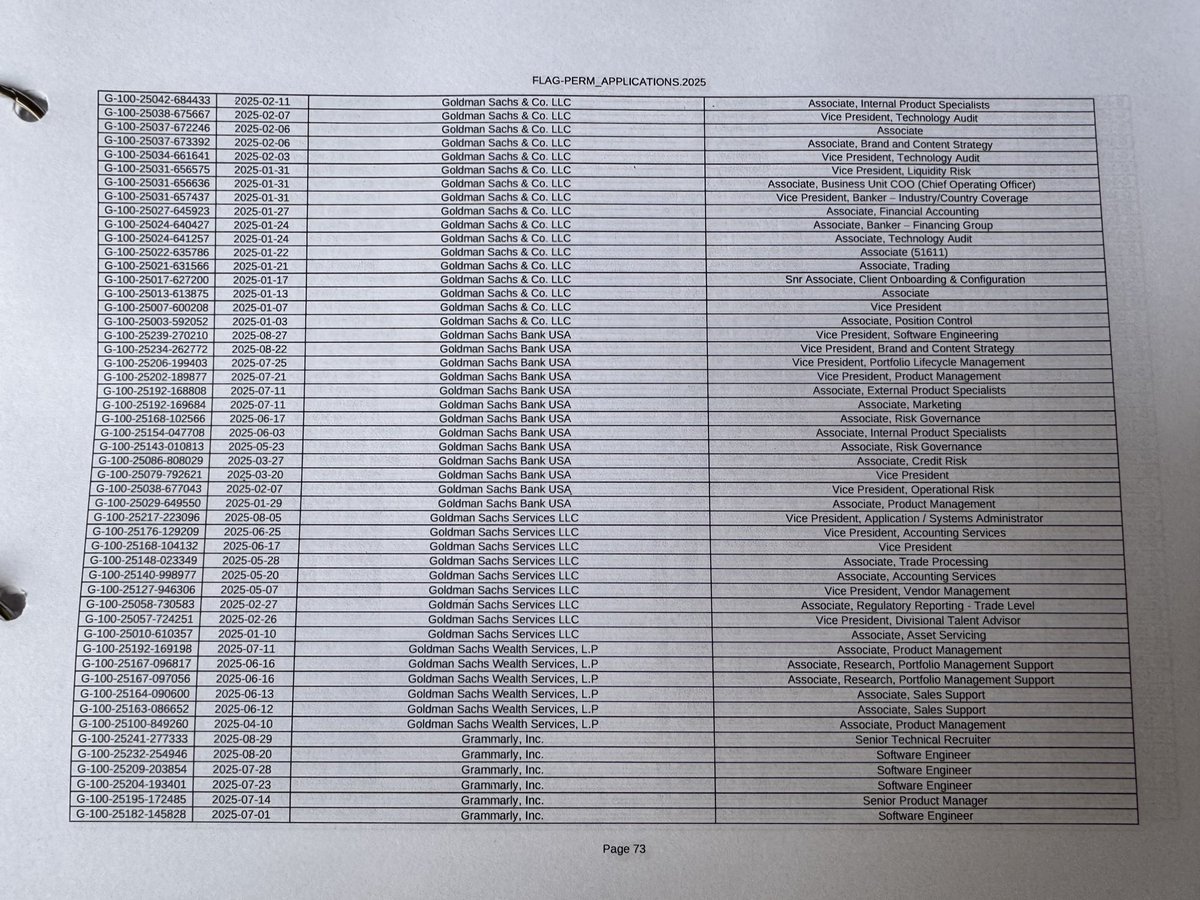

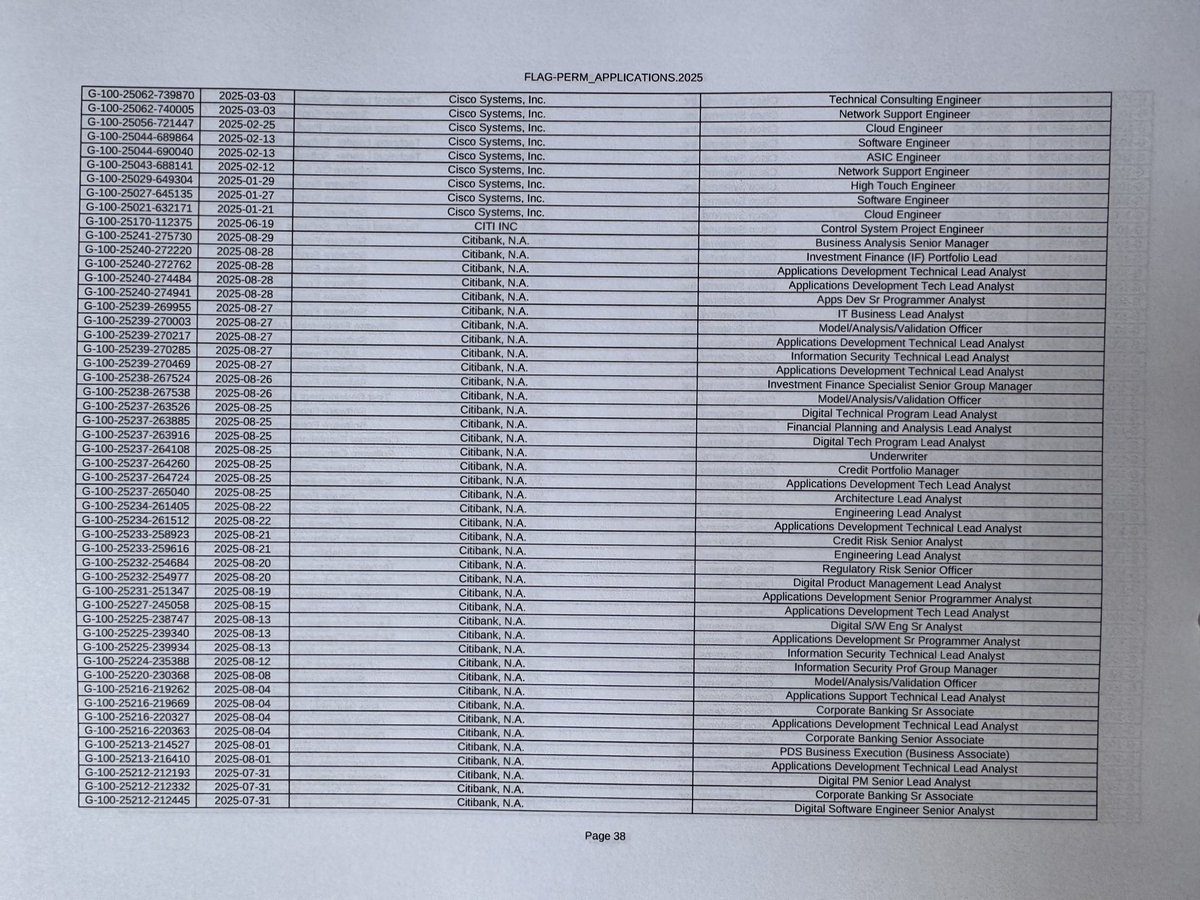

These binders hold all communications for 50 PERM roles I applied for.

The records bound together with the three rings are 10k open PERMs being processed by the DOL right now.

Almost all the roles I applied are being filled with foreigners on H1-B — even the 90% from firms that never contacted me during the labor market test.

This is the truth of the H1-B program.

It’s about displacement.

107

738

2,812

204,050

Robert Alan retweeted

8 Nov 2025

The fight between Pro-Israel vs America First conservatives is heating up...

1,402

7,155

28,146

1,187,067

1 Nov 2025

Oof, hire a copy editor

Imagine calling yourself a journalist and actually writing "less visitors" 🙄

friggin (sic)

31 Oct 2025

Las Vegas has seen 2 MILLION less visitors so far in 2025 compared to 2024.

Caesars Entertainment reported 90,000 empty rooms.

Consumers are out of money.

156

Robert Alan retweeted

13 Oct 2025

TOUCHDOWN XAVIER WORTHY!!🔥🙌

FOLLOW TRAIN FOR 7 MINUTES! 🚂

MUST RT & LIKE THIS!

#ChiefsKingdom

Stops at 7:56 CST / 8:56 EST

3

10

1,643

26 Sep 2025

Indeed

9 Jun 2023

A good day for the rule of law

1

258

🚨 Dallas ICE Shooting Raises Serious Questions

Less than 24 hours after Texas Imam Omar Suleiman vowed to “fight with everything we’ve got” over the arrest of MAS leader Marwan Marouf, a gunman opened fire on the Dallas ICE facility, leaving multiple agents critically wounded.

Authorities have not yet confirmed a motive — but the timing is chilling. When influential leaders talk about “fighting” federal law enforcement, some radicals will inevitably take those words literally.

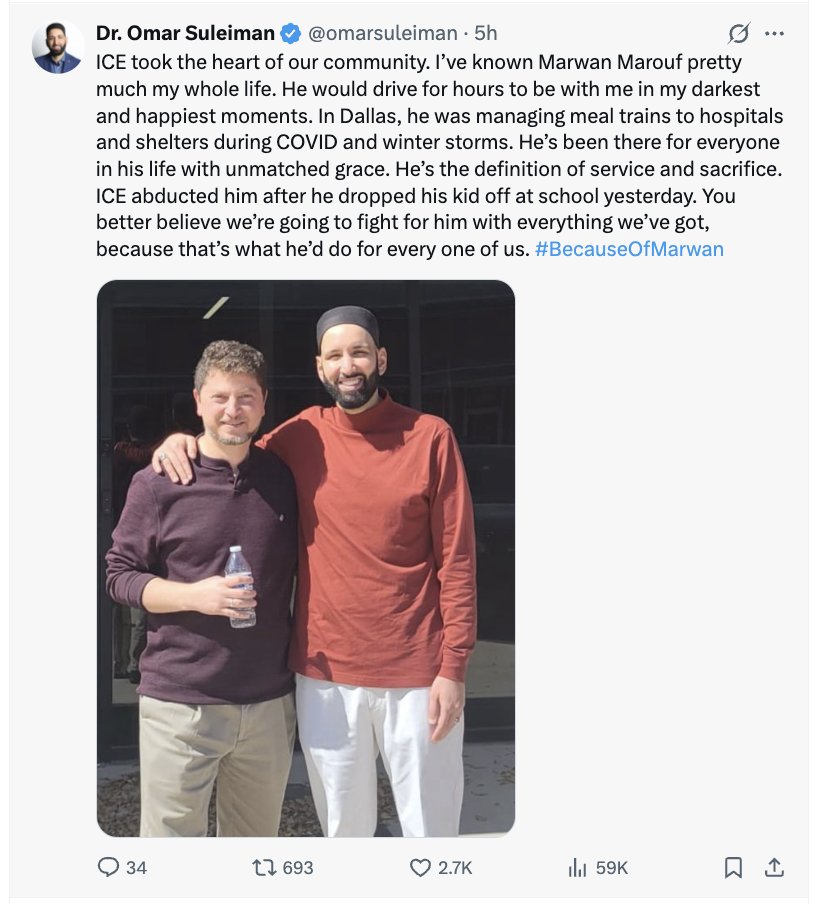

🚨 TEXAS VICTORY ALERT 🚨

The radicals are LOSING THEIR MINDS.

Omar Suleiman is crying on X that ICE “took the heart of our community” because his close friend Marwan Marouf — a top Muslim American Society (MAS) leader and brother-in-law to the Hamas-linked Elashi family — is finally in custody and facing deportation.

This is precisely what happens when the law is enforced:

📌 MAS = Muslim Brotherhood’s U.S. arm

📌 Elashi family = Holy Land Foundation terror-financing case

📌 Marouf = tied into the same Hamas-linked network that made Dallas ground zero for jihad funding

Texas, don’t miss the bigger picture:

The “heart of their community” is a man embedded in an extremist infrastructure. And now he’s behind ICE bars.

👏 This is a HUGE counterterrorism victory for our state and for America.

The radicals are panicking. That tells you all you need to know.

See the full report: rairfoundation.com/breaking-…

307

2,166

4,640

378,158

Robert Alan retweeted

17 Sep 2025

Meet Lola, the owner of Lola’s tacos who has a concession at State Farm Stadium where Charlie Kirk’s memorial is going to be held.

She posted amongst other disgusting things the following :

“One less fascist in this country.

Now on to the next one!”

This business needs to be removed from State Farm Stadium @StateFarmStdm NOW!!!

5,312

36,200

82,193

3,149,897