Mechanical Engineer. Data centers before they were hated. Creator of @BankviewUSA

Joined June 2022

- Tweets 2,395

- Following 2,111

- Followers 4,116

- Likes 7,516

Photos and videos

The comments

If we don’t stop this concert, it will be telling everyone that antisemitism is okay.

It’s NOT.

1

2

504

11h

$PDLB ecip deal is well known by now, but think Ponce and $UBAB could also benefit from a re-rate if they return enough capital.

Jun 12

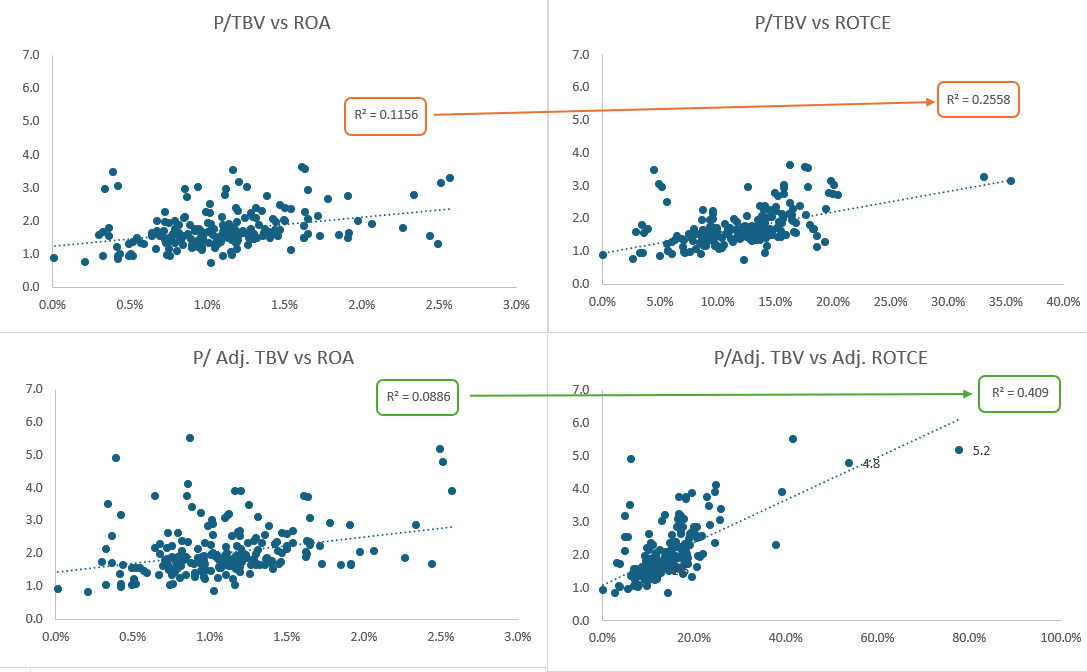

Is bank ROA a better predictor of P/TBV than ROTCE?

My own work says no (especially when adjusting for PDNA and unr. HTM losses), but if you know of contradicting research, please post the link in comments.

1

1

5

1,215

Jun 13

Dan has some good takes. This is not one of them.

America first surfer guy

Jun 13

Money well spent.

2

904

Jun 13

Key man risk x 1 trillion

Jun 13

Irony is, if he stops working it’s worth about $0.

Many such businesses.

1

1

9

1,764

Jun 12

Is bank ROA a better predictor of P/TBV than ROTCE?

My own work says no (especially when adjusting for PDNA and unr. HTM losses), but if you know of contradicting research, please post the link in comments.

1

4

1,915

Jun 11

Why does a bank that operates “primarily in Texas” move their main office to Tulsa months before the announcement?

Lighter touch supervision in OK?

Scotiabank announced that it has entered into a definitive agreement to acquire Maple Financial Holdings, the parent company of MapleMark Bank, a U.S. commercial bank with operations primarily based in Dallas, Texas. buff.ly/Rl4zfav

4

866

Jun 10

Does everyone agree w this Joe Stieven take?

Isn't P/TBV more closely correlated w ROE than ROA?

If so, shouldn't leverage get as much attention as other metrics?

8

11

1,815

Jun 8

The problem w @RepAnnWagner and @BradSherman's proposal is that current securitization rules are also pushing bank lending into the private markets.

Making them more attractive works against @SecScottBessent and @federalreserve's stated goal of stemming credit migration to NDFIs.

5

615

Jun 7

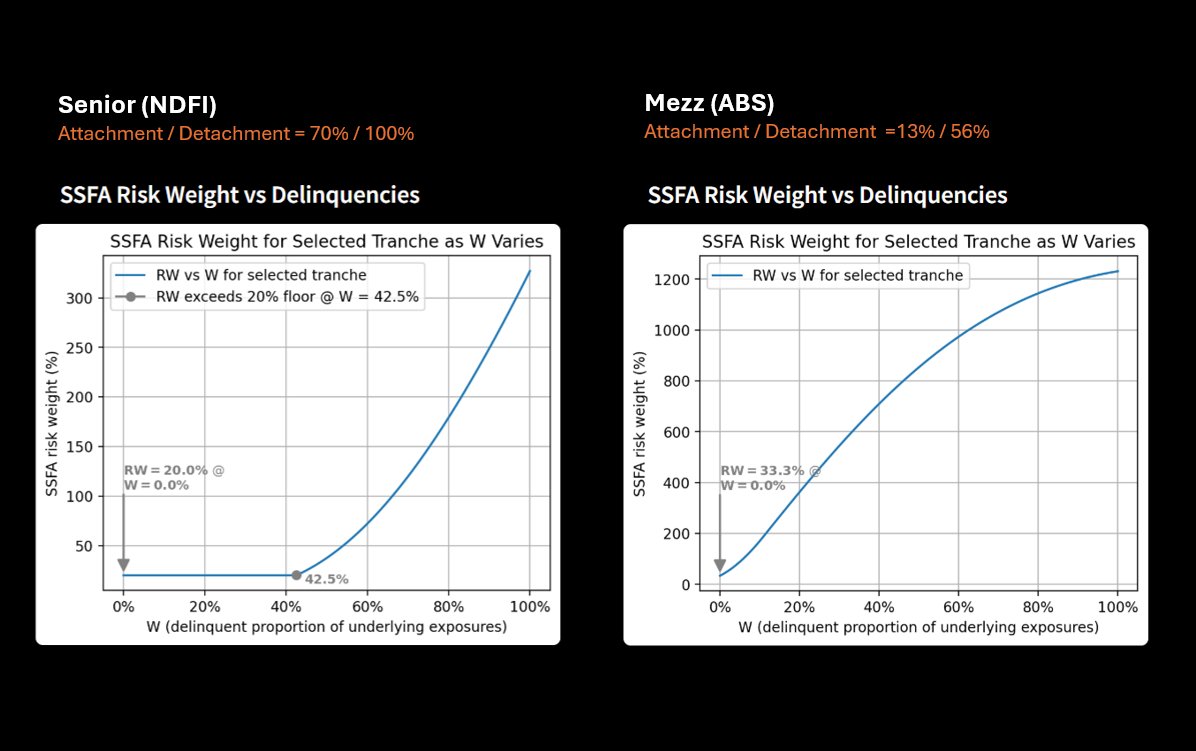

Hypothetical example:

A private $1B bank specializing in subprime auto starts seeing dqs rise to dangerous levels. (Let's call them Donut Bank 🍩) Supervisors get concerned and threaten to shut them down if they don't raise capital or bring down NPLs.

The bank pairs up w/ a private credit firm who agrees to "buy" the entire $700mm auto book for just under par, despite the high NPLs. The PC group intends to place the loans in a SPV, securitize and issue ABS.

As part of the terms, Donut Bank agrees to seller-finance 30% of the sale, classified as a senior NDFI loan on the call reports (Attachment point / Detachment point = 70%/100%). Since the NDFI is structured as an over-collateralized securitization, regulators allow a 20% risk weight against the loan using the simplified supervisory formula approach (SSFA).

In addition, Donut bank also turns around and buys back a mezz ABS security issued by the PC firm (A/D =13%/56%). This slice is also allowed SSFA treatment, but sits at a 33.3% RW at origination given the less senior position.

Since Donut Bank claims a true sale of the auto book to the PC group, bank call reports no longer track dqs of the underlying refence pool directly. They only show if the NDFI loan and ABS security are current on their contractual payments.

What the call reports DO track is the current SSFA risk weights of those same bank assets... and those RWs are tied to dqs in the reference pool, not the dqs of the bank assets.

SSFA risk weights are calculated quarterly. If we see them start to drift off the 20% floor (or up from the origination value), it could mean severe stress in the reference pool.

The chart to the left shows the RW vs DQ curve for the more senior NDFI loan and the right shows the ABS. To @shortbus_ace 's point, you'd need more than 40% of the reference pool to go delinquent before the NDFI RW starts to drift off the 20% RW floor in the call reports. The scenario is extreme and unlikely at most banks at a 30% advance rate.

But the mezz security is already off the risk weight floor at origination. Any new dqs in the reference pool will likely sent the SSFA RW higher before we see impairment in the ABS value.

If supervisors look into the Donut Bank deal and find that a true sale holds (and it's not just a Hail Mary attempt to round-trip subprime auto NPLs), the thing they should be watching is where the SSFA RW for the mezz ABS is drifting, not where the the ABS is marked. That's the leading indicator.

Jun 6

This went over my head and AI was not helpful, dumb it down for me

2

2

12

3,266

Jun 6

If an NDFI loan is structured as a senior security and the reference pool starts to see stress, the bank won’t show a DQ if the sr is still getting paid.

The thing to watch for is rising SSFA risk weights…. but even that assumes honest marks on the underlying assets.

2

7

1,738

Jun 5

Don't mistake leverage for genius.

...but don't mistake a lack of leverage for genius either

4

377