Joined May 2018

- Tweets 5,966

- Following 443

- Followers 11,082

- Likes 1,560

2,433 Photos and videos

Pinned Tweet

Apr 10

🚨10X Stocks - My New Book Published worldwide on April 6th

Happy to share it’s already #1 New release and #9 Best seller in Business/Valuation on Amazon 😊

The book as the title says is about:

8 Frameworks on ‘How to Pick Multibaggers’

Order 👉 10X Stocks: How to Pick Multibaggers a.co/d/059DfXkj

5

4

23

15,211

🚨Apollo Blackstone just dropped $35B to fund Google TPUs for Anthropic.

The Structure: Here’s how it works ??

→ Apollo & Blackstone provide $35B in debt

→ SPV borrows it, buys Google TPUs

→ SPV leases TPUs to Anthropic

→ Anthropic pays lease over time

→ Broadcom backstops the senior tranches (A1 & A2)

🚀TPU orderbook is EXPLODING —

• Anthropic: 1M TPUs committed

• Meta: multibillion lease starting 2026, potential outright purchase 2027

• Broadcom’s AI revenue: $4.4B → $8.4B in just 3 quarters (106% YoY)

• Q2 FY26 guidance: $10.7B in AI semiconductor revenue

• Target: $100B by 2027

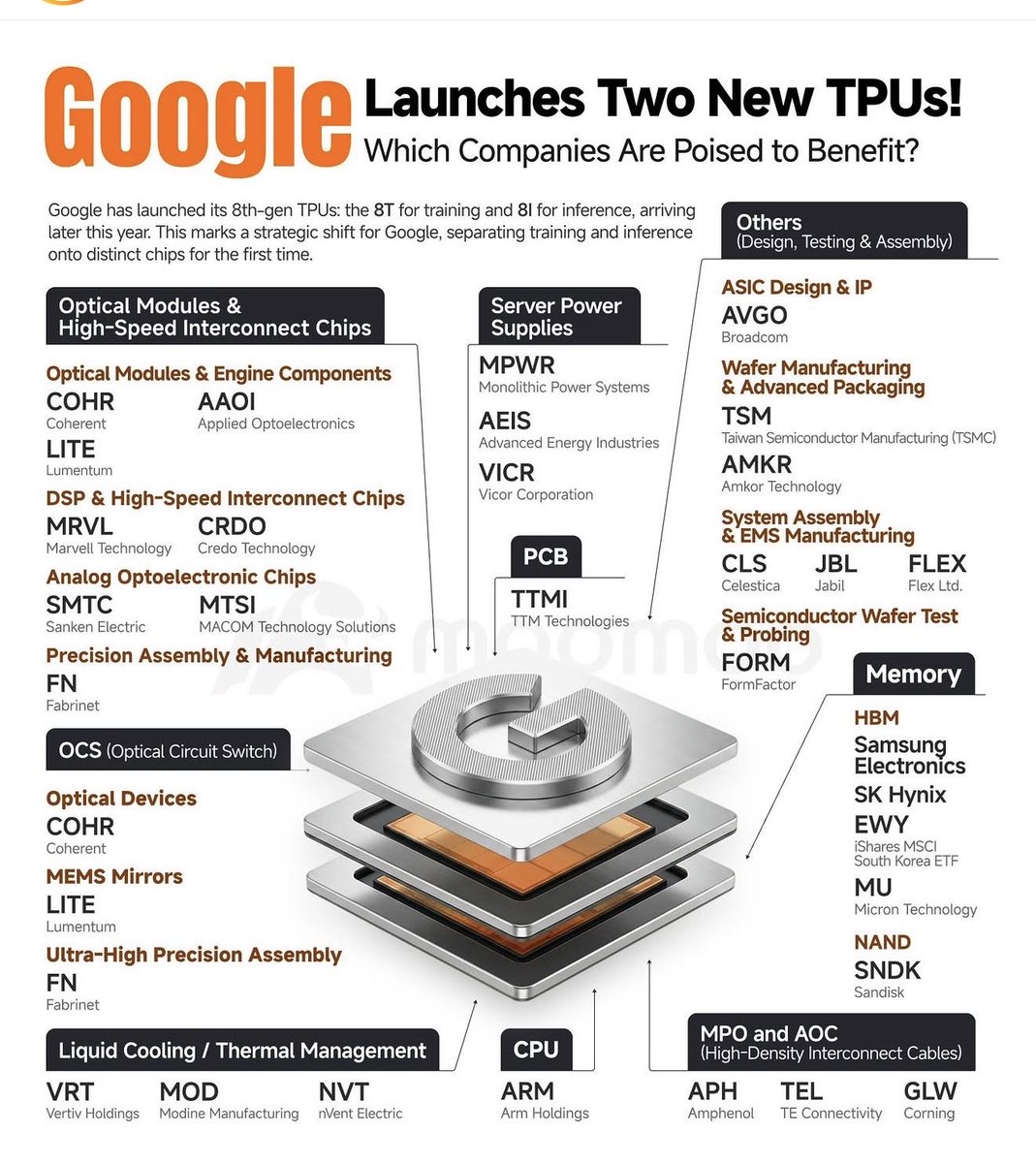

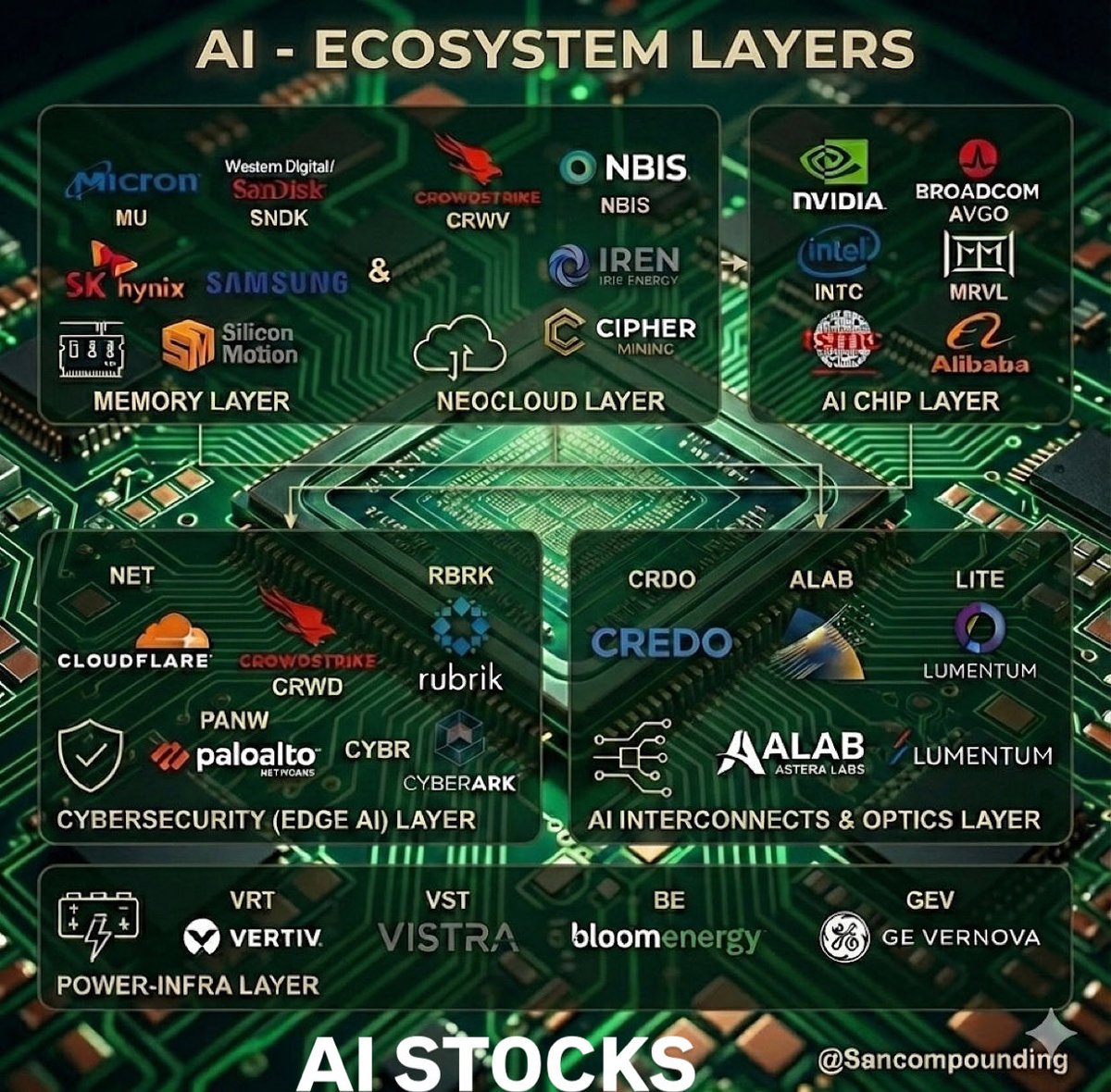

➕Google just launched 2 new TPUs — 8T for training, 8I for inference. Who benefits?

1. $AVGO (Broadcom) and $MRVL sits at the center of this — designing the TPUs AND backstopping the debt.

2. Optics & Engines → $COHR $AAOI $LITE

3. AI Interconnect → $MRVL $CRDO $ALAB

4. Server Power → $MPWR $AEIS $VIC

5. Memory / HBM → $MU $SNDK $DRAM

6. MPO/AOC Cables → $APH $TEL $GLW

5

9

726

Jun 15

🚨🚨THE GUY WHO WROTE ‘AGI BY 2027’, LEOPOLD SITUATION FUND, JUST MADE

1,000% RETURNS !!!

He’s not long $NVDA. He’s long $8.5B in puts on it ( $AMD, $AVGO, $TSM, $MU, $ORCL).

What he is long: $CRWV, $IREN, a fresh 5.6% stake in $NBIS, $BE

He is Long the bottleneck. Why?

Here’s a 3-point mapping from the Leopold famous AI Paper, to how Situational Awareness is actually positioned :

1.“Unhobbling” → inference demand → AGI-by-2027 compute scaling →

SAF’s largest long-side conviction is the GPU neocloud buildout: as the picks-and-shovels for the compute curve.

New addition validates the thesis → Situational Awareness recently bought 12.4 million shares of Nebius Group, representing a 5.6% ownership stake — a fresh bet on “gigawatt-scale AI factories”

2.Industrial mobilization theme → repurposed bitcoin miners turned AI compute operators — Core Scientific, IREN, Cypher, Applied Digital — and optical components remain prominent i.e fastest path to spinning up gigawatts.

3.Power as the binding constraint → energy infrastructure remains the core long bet, with Bloom Energy continuing as a flagship position delivering on-site power directly to data centers, bypassing the strained grid

1

43

197

17,231

Sandeep Anand retweeted

Jun 14

4 Amazing Books You Must Read In 2026

3

32

192

6,357

Jun 13

🚨Jevons Paradox in action !! — A 🧵

Why are AI token prices crashing while spend explodes?

1/ Competitive price war:

OpenAI is reportedly weighing major cuts to API pricing as Anthropic’s Claude Code pulls developer share.

Anthropic’s coding assistant crossed $1 billion in revenue within 6 months of launch

♾️Pricing power is shifting fast.

2/ The math:

Claude Opus 4.8: $5/$25 per M tokens

GPT-5.4: $2.50/$15 per M tokens

💸Both now offer 90% caching discounts, making effective costs competitive for cache-heavy workloads

3/ Open-source overhang:

As long as China’s AI labs stay open-source funded by $BABA, the floor on intelligence pricing keeps falling toward zero — structural deflationary pressure on the whole industry

4/ But here’s Jevons in action — usage is outpacing the price drops:

$UBER burned through its entire 2026 AI budget in 4 months as Claude Code adoption jumped from 32% to 84% across its 5,000-engineer org, with per-engineer monthly API costs ranging $500-$2,000

5/ Result:

🚀Anthropic’s ARR (annualized run rate) surged from $9B at end of 2025 to $47B by May 2026 — a 422% jump in five months

Cheaper tokens → more agentic workflows → more inference → more chips, memory, power, optics demand.

Enterprise AI budgets are set to 2-3x, not shrink.

Every layer of the stack benefits:

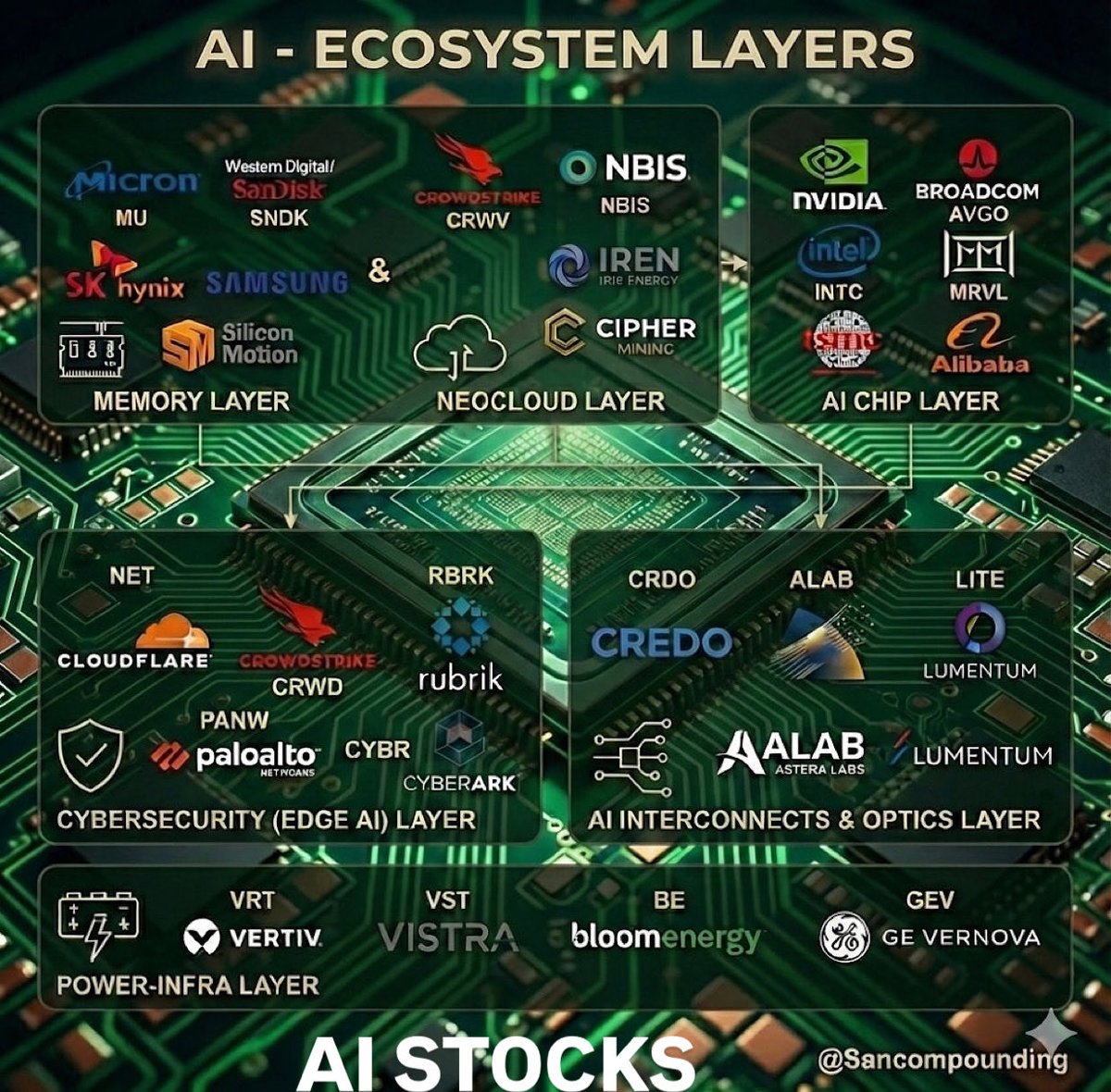

🧠 AI Chips: $NVDA $AVGO $MRVL — more inference = more silicon demand

💾 Memory: $MU $SNDK $SKHynix $DRAM — HBM/DRAM supercycle from token volume explosion

☁️ Neoclouds: $CRWV $NBIS — capacity gets soaked up instantly

🔌 Optics/Interconnects: $CRDO $ALAB $LITE $AAOI— data movement scales with tokens

⚡ Power: $VRT $VST $BE $GEV — compute growth = power demand growth

📈Cheaper AI doesn’t kill the trade. It accelerates it.

3

681

Jun 12

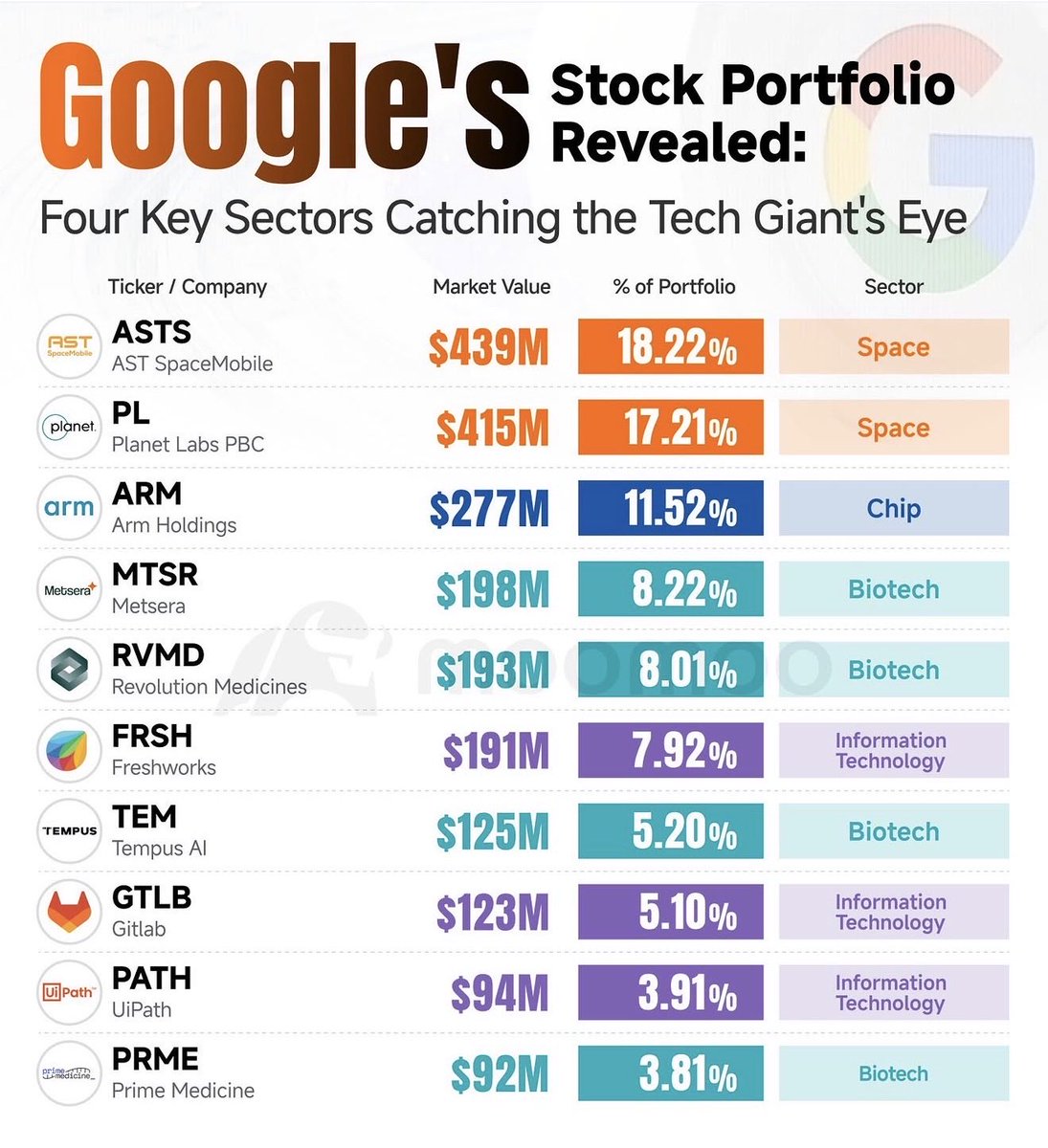

Missed $SPCX IPO Allocation? Take a look at $GOOGL’s top 2 holdings.

Here’s why Google might be bullish on these Space companies 👇

$ASTS (AST SpaceMobile) — $439M, 18.22% of portfolio

Building a satellite-based cellular network that connects directly to unmodified smartphones. Google’s stake hints at interest in space-based connectivity infrastructure that could complement Android’s global reach.

$PL (Planet Labs) — $415M, 17.21% of portfolio

Operates one of the largest fleets of Earth-imaging satellites, generating daily data on virtually the entire planet’s landmass. That’s a goldmine for AI training data — squarely in Google’s wheelhouse.

➕Combined, these two space plays make up ~35% of $GOOGL’s disclosed equity portfolio — a massive bet on the space economy’s next decade.

🚀Space isn’t just rockets anymore. It’s connectivity data, and Google wants both.

2

32

107

8,359

Jun 12

🚨 $CRWV, $NBIS, $ALAB has entered Nasdaq-100

✅ 3 out of 5 from this tweet 1 year back has entered Nasdaq-100👇.

By the by this basket is up 250% last 1 year 🚀

DYOR. No investment advise.

4 Jul 2025

Michael Dell’s post is super bullish for

my “AI Super -5”

1. $CRDO

2. $CRWV

3. $NBIS

4. $ALAB

5. $TSSI

Here are Margin-FCF profile of “Super -5”

1. $CRDO

Gross Margin : 65%

FCF Margins :: 6.6%

EPS : Turned ve from (.2) to 0.3

2. $CRWV

Gross Margin : 74%

FCF Margins :: No FCF (Huge Capex)

EPS : Loss

3. $NBIS

Gross Margin : 41%

FCF Margins :: No FCF (Huge Capex)

EPS : Loss

4. $ALAB

Gross Margin : 76%

FCF Margins :: 22%

EPS : Turned ve from (.6) to 0.3

5. $TSSI

Gross Margin : 12%

FCF Margins :: 4%

EPS : 0.4

✅I like $ALAB and $CRDO based on all growth and margins metrics

✅But IAAS Data Center companies $NBIS and $CRWV cannot be measured on earnings basis. They have huge operating leverage and will benefit at an inflection point where Sales surpass Fixed Cost / breakeven

⏹️$TSSI has very low Gross Margins which is evident- concentration risk on $DELL

1

4

1,988

Jun 12

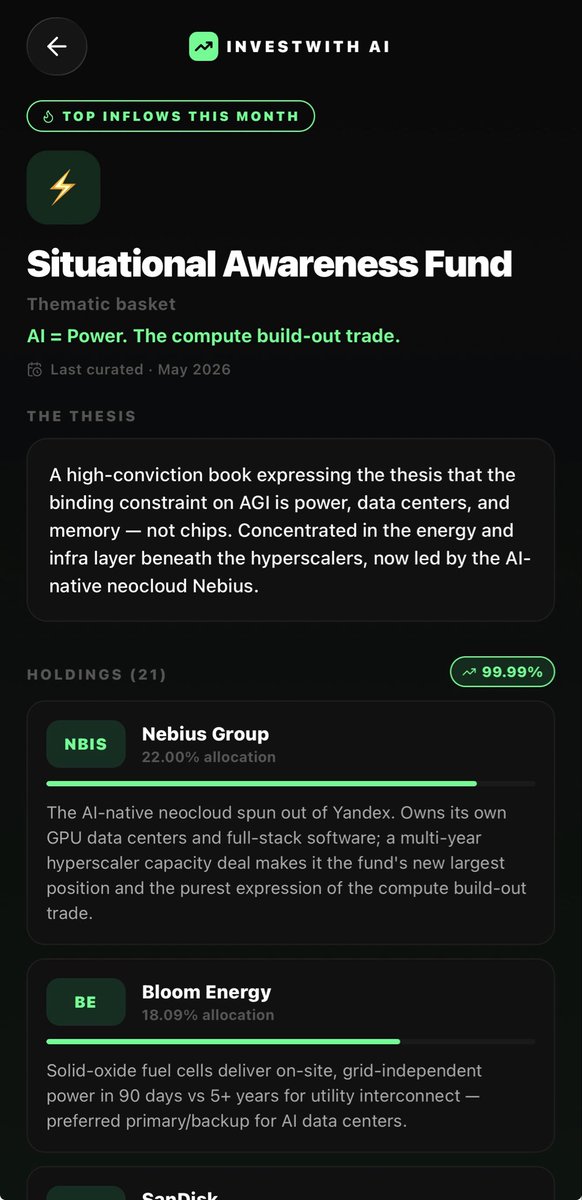

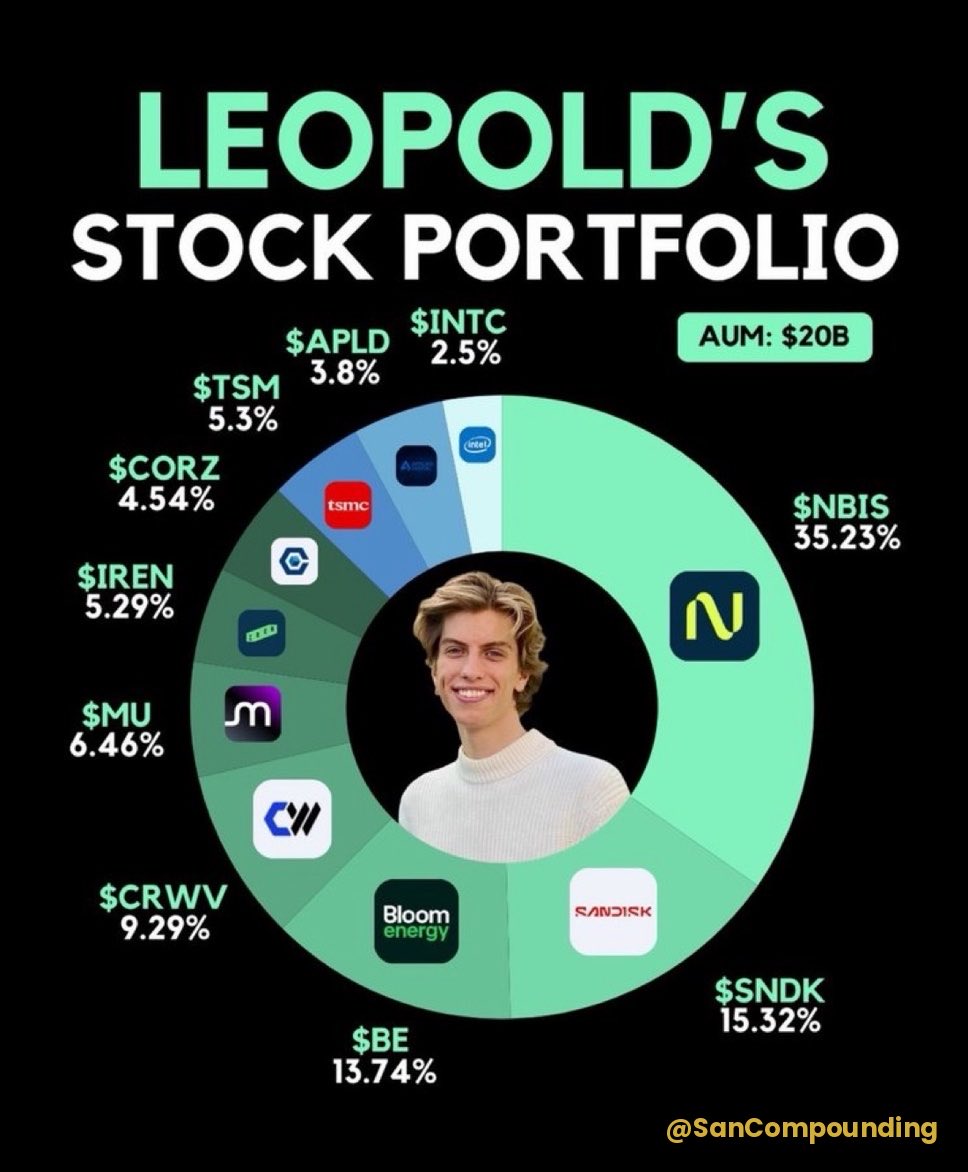

🚨Why does Leopold Aschenbrenner’s Situational Awareness Fund hold $NBIS at 35% — by far its largest single position??

The numbers (Q1 2026)

—Revenue hit $399.0 million in Q1, up 684% year-over-year and up 75% from Q4

—Core AI cloud ARR surged 54% QoQ to $1.92B, implying asset productivity of $0.941M per 1 MW of active capacity .

—2026 guidance is $3.0B–$3.4B revenue and $7B–$9B ARR

✍️The numbers backs conviction:

→ Contracted backlog $50B through 2031 vs $530M in 2025 revenue

→ Q126 ARR up 54% QoQ to $1.92B, sold out of capacity every quarter

→ Anchor deals: $19.4B Microsoft, $27B $META, $NVDA as direct equity holder

Bull Case?? Backlog-to-current-revenue ratio is roughly 100x. That’s the bull case (multi-year visibility nobody else in neocloud has)

The bear case ?? huge execution/financing risk to actually convert that into cash flow on schedule !

Capacity is the real constraint::

-Demand again exceeded capacity in the core AI cloud business — they operated at peak utilization and were sold out of capacity in Q4

-To meet this, $NBIS is targeting > than 3 GW of contracted power by year-end, ahead of the prior 2.5 GW target, with the vast majority coming from owned data centers for capital-efficient long-term unit economics

This is a bet that AI compute scarcity persists through 2030 and that Nebius’s owned-infrastructure model captures disproportionate share of it.

The risk isn’t demand — it’s financing $20-25B/yr capex fast enough to convert backlog into cash flow.

2

1

13

6,202

Jun 12

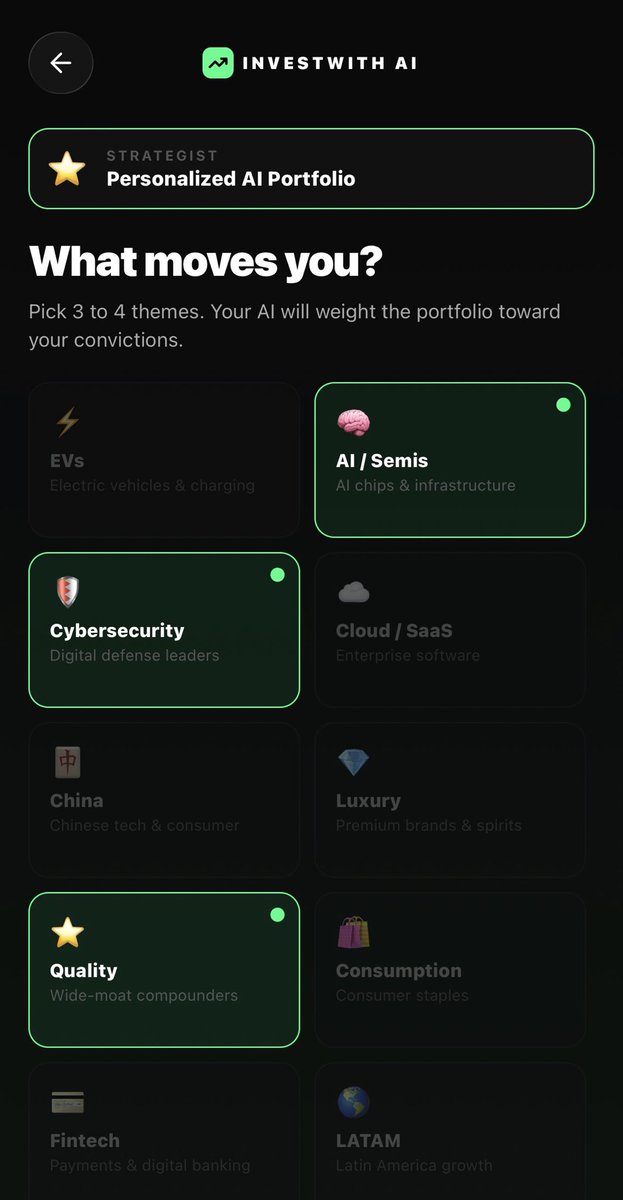

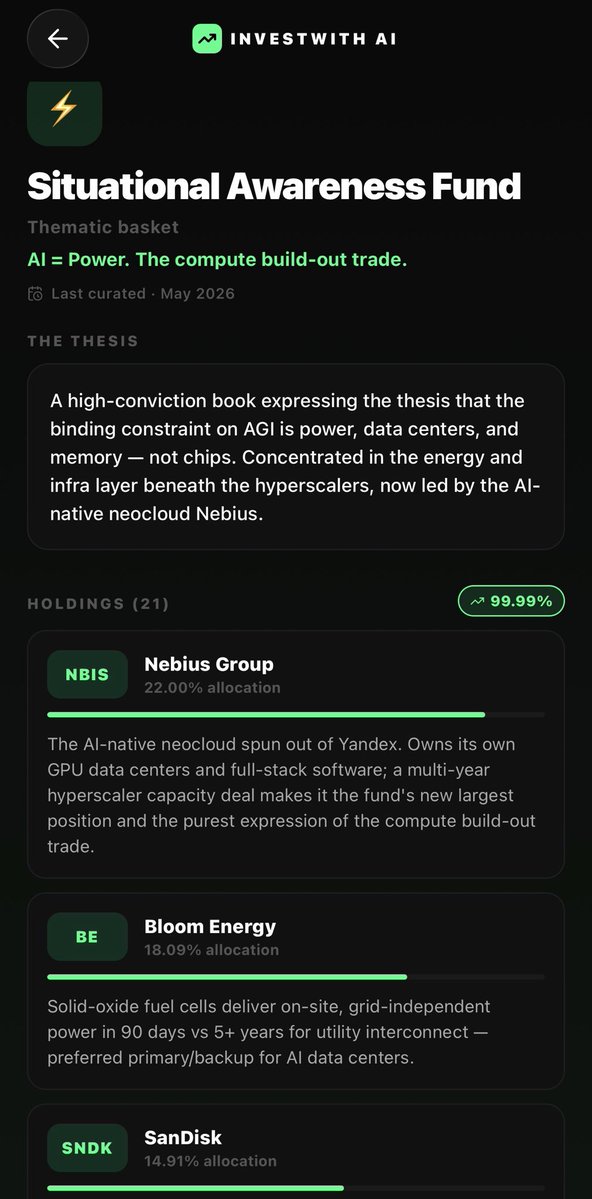

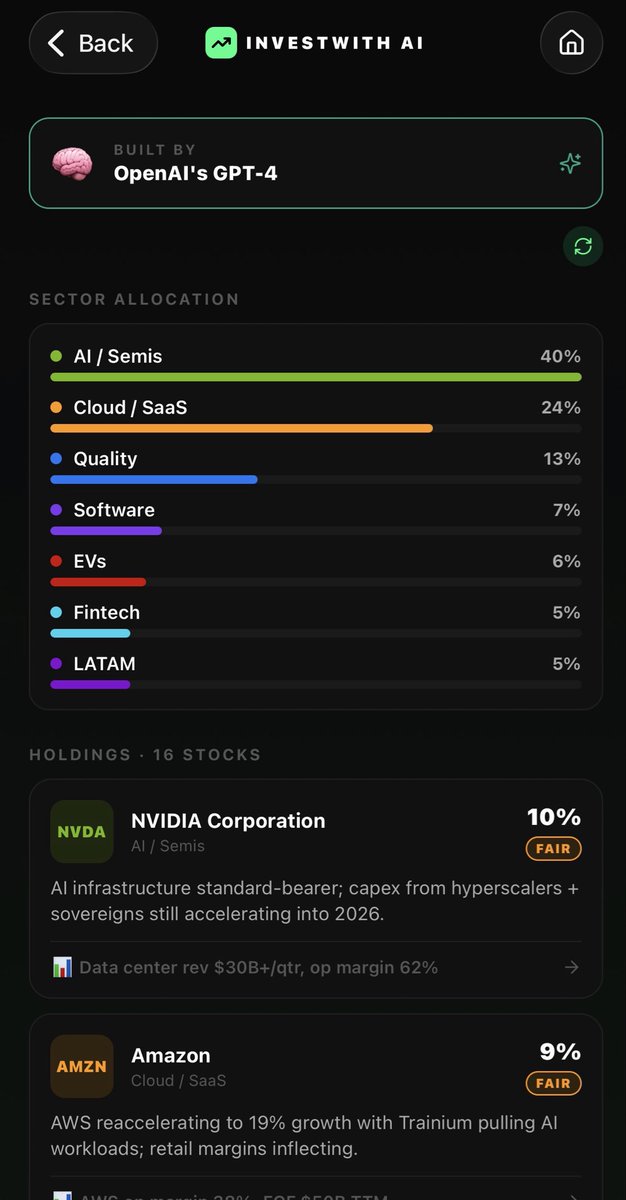

View Leopold portfolio and other Top AI funds holdings and thesis at InvestwithAI App -> apps.apple.com/us/app/invest…

614

Jun 11

🚨

$CRDO UP 250%

$ALAB UP 260%

Since my thesis about $CRDO and $ALAB in July 2025 👇

Follow the right side of the change always …

10 Jul 2025

$CRDO Clearly leading the way out today with $ALAB in my “AI - Super 5” pack.

Riding on momentum fueled by AI proliferation and increasing demand for faster and energy-efficient connectivity solutions, $CRDO Credo Technology Surges 144% in 3 Months.

🇺🇸The Bank of America analyst released report on Credo Technology Group, titled “Mgmt call takeaways: AI connectivity specialist, 5x growth oppty,”

Lets deep dive into CRDO’s Multiple Tailwinds as it Rides the AI Wave ::

🎯At the heart of Credo’s business is its Active Electrical Cables (AEC) product line, which posted double-digit sequential growth in latest Q4 2025.

1/ AEC is gaining traction owing to its increasing adoption in the data center market. The demand for AECs is increasing as ZeroFlap AECs offer more than 100X better reliability than laser-based optical solutions.

📈Launched PCIe Gen6 AECs and increasing hyperscaler interest, this product line is expected to remain a growth engine going ahead.

2/ Optical Digital Signal Processors (DSPs), is another growth catalyst. CRDO achieved a key 800-gig transceiver DSP design win and unveiled ultra-low-power 100-gig per lane optical DSPs built on 5-nanometer technology.

CRDO expects its 3-nanometer 200-gig-per-lane optical DSP (port speeds up to 1.6 terabits per second) to boost the industry’s transition to 200-gig lane speeds.

3/ CRDO’s PCIe retimers and Ethernet retimers business is growing rapidly. — especially for scale-out networks in AI servers.

CRDO retimer business delivered “robust” performance in FY2025, driven by 50 gig and 100 gig per lane Ethernet solutions.

This growing demand underscores the increasing importance of high-performance solutions in the rapidly expanding AI server market. Shift to 100 gig per lane solutions will accelerate with AI Boom 🚀

1

4

794

Jun 10

🚨Jensen Huang’s Korea Visit: The 4 New Products & HBM Take is super-bullish 📈

First — $NVDA ‘s four major new product launches this year:

1. Vera Rubin platform (new rack systems already shipping)

2. Vera CPU

3. RTX Spark (Nvidia’s first AI PC/laptop)

4. Jetson Thor (edge robotics processor)

HBM commentary: Huang called SK hynix’s HBM “world’s best” and shouted “HBM!

He confirmed at the airport that all three major memory makers — Samsung, SK Hynix, and Micron — have been qualified for HBM4 supply for Vera Rubin, with SK hynix holding roughly 60-70% of allocated volume, Samsung 25-30%, and Micron the remainder

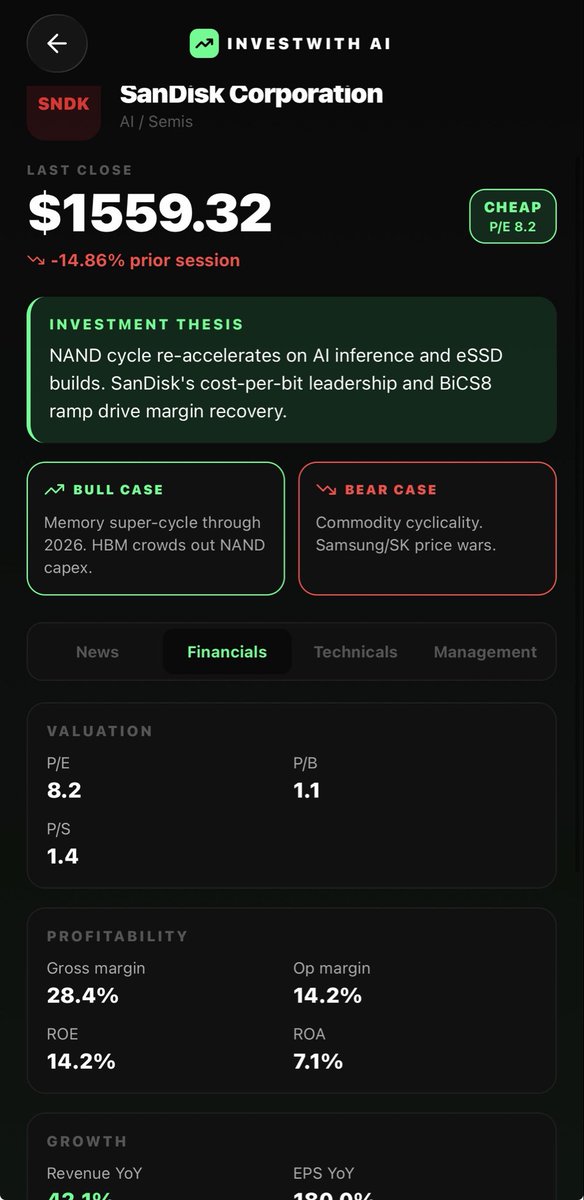

$DRAM ETF Holdings — Why Vera Rubin/HBM4 = Tailwinds ?

$MU (Micron) — Now one of three certified HBM4 suppliers for Vera Rubin.

— Even a smaller allocation slice on a much bigger HBM4 pie (vs HBM3E) is a major mix-shift to higher-margin product, plus broad LPDDR/DDR demand from AI PCs (RTX Spark) and edge (Jetson Thor)

$WDC / $SNDK (NAND spinoffs) — Less direct HBM exposure, but benefit from the broader “everything in shortage” dynamic — AI servers also drive enterprise SSD/NAND demand & DRAM tightness is spilling into NAND pricing as fabs reallocate capacity.

Samsung Electronics — Just landed HBM4 qualification for Vera Rubin (25-30% allocation), a comeback story after lagging SK hynix in HBM3E. Vera Rubin ramp in Q3 2026 is the catalyst that converts this qualification into revenue 🚀

SK hynix — The dominant HBM4 supplier (60-70% share) and the company Huang singled out as making the “world’s best” HBM — direct, largest beneficiary of the Vera Rubin ramp starting Q3 2026.

3

7

31

3,369

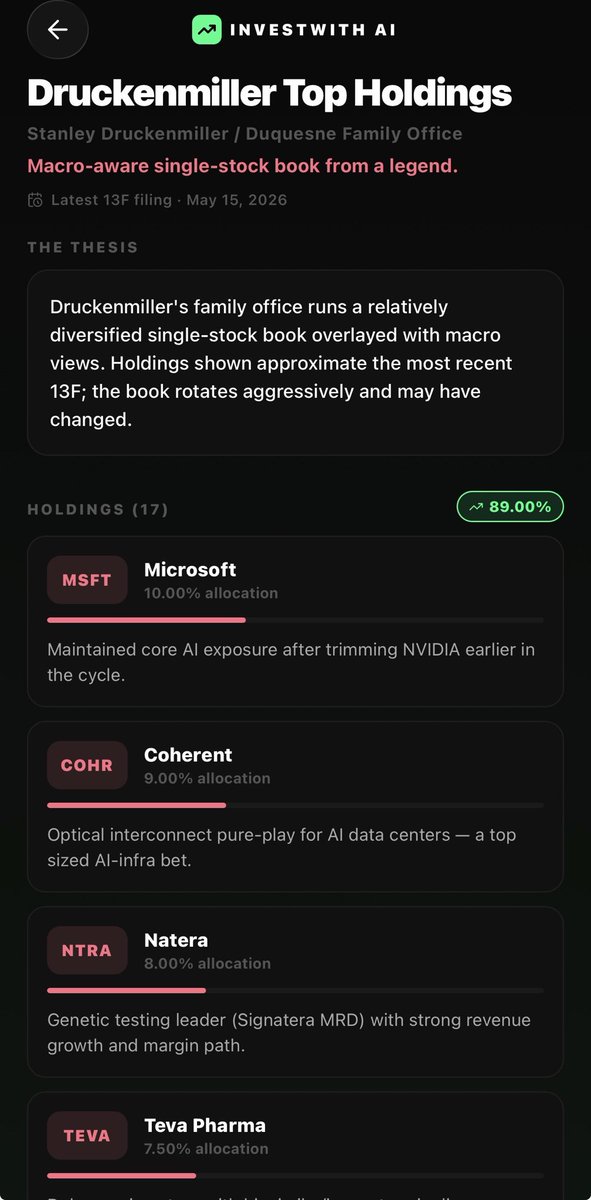

Jun 8

🚨Breaking— Markets bounce back big !!

What I ll ‘Buy More Of’ will be in alignment with what Druckenmiller is betting on - AI Buildout theme !!

$DRAM

$CRDO

$COHR

See what Stanley Druckenmiller holds at InvestwithAI apps.apple.com/us/app/invest…

1

2

11

4,096

Jun 7

🧵 In 1995, tech companies started borrowing to build.

By 1999, Nasdaq had risen 400% 📈

Today in 2026:

• Google raises $85B (largest equity deal in history)

• Meta considering tens of billions more

• SpaceX, OpenAI, Anthropic: $3.6T in IPOs queued up

The leverage cycle just kicked into overdrive. 🚀

(The 90s Parallel)

Here’s what happened last time capital flooded in:

📅 1995–1997: VCs debt funded the network buildout

📈 S&P 500: 37.6%, 23%, 33% those 3 years

📅 1998–1999: Tech & telcos issued junk bonds

📈 Nasdaq TRIPLED from autumn 1998 → March 2000 peak

Capital availability = the fuel.

Fast forward to 2026:

💰 Global tech issued $428B in bonds in 2025 alone — record high

💰 The Big 4 hyperscalers will spend $725 B in capex this year

💰 That’s 94% of their operating cash flow

→ They’ve had to turn to equity AND bond markets

This is the leverage cycle going parabolic.

In the 90s, companies had no revenues and borrowed to survive.

Today: GOOG generates $170B operating cash flow/yr and STILL raised $85B

META generates $115B operating cash flow/yr and may raise more.

This isn’t desperation capital. This is acceleration capital. 🏎️

What it means for stocks??

The 1995–2000 run lasted 5 full years after the leverage cycle started.

We may be in year 2 or 3 of this AI capex supercycle.

The stocks levered to this buildout:

$CRWV $NBIS $MRVL $ALAB $LITE $VRT $CRDO $AAOI $NET $DRAM

Stay long.

2

9

33

2,014

Jun 6

🚨Markets crashing

AI Stocks are crashing !

I asked ‘InvestwithAI’ what stocks to buy?

🤖 Here is the personalized portfolio AI engine simulated 👇

1. $NVDA

2. $VST

3. $META

4. $SNDK

5. $TSMC

6. $PNG.NE

7. $AAPL

8. $MSFT

9. $IREN

10. $ANET

11. $GOOGL

You can choose any themes and the AI engine in the App will simulate a stock portfolio. apps.apple.com/us/app/invest…

DYOR. No investment advise

2

6

1,003

Jun 5

🚨 You could have prepared for today’s crash yesterday itself!!

My AI App already gave a heads up yesterday and I had tweeted this shift from semis to consumer by Claude 👇

InvestwithAI apps.apple.com/us/app/invest…

Jun 4

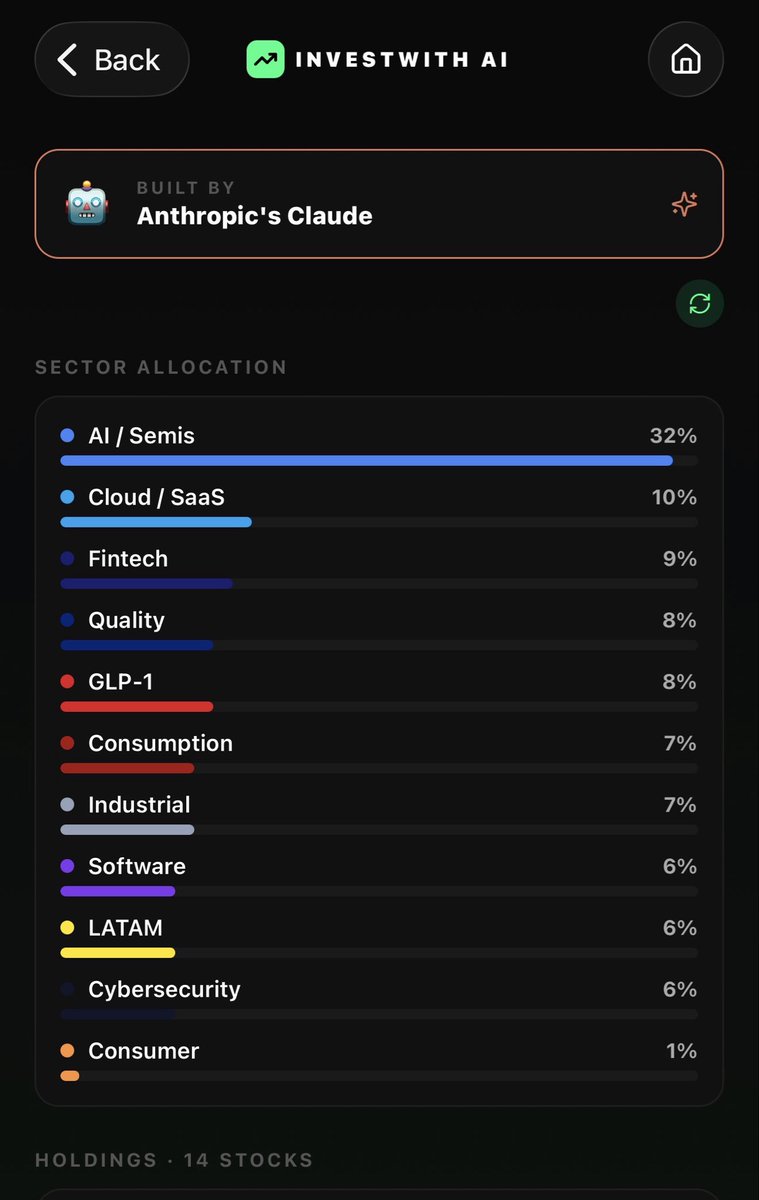

🚨 Breaking: The Claude Portfolio in InvestwithAI App is Adding Consumer names.

Claude has reduced 10% allocation from Semi and AI. Has started adding to consumer names in US snd LATAM.

🚀Trend is shifting live. Added by Claude today:

$CMG

$MELI

$FIVE

$V

But ChatGPT still leaning heavy into Tech/Semis !! Claude appears to be smart ✅

2

3

1,153

Jun 5

🚨 Follow the ‘Godfather of AI’ 📈

Jensen is quietly building a strategic Berkshire of AI companies — $18.37B invested across 6 companies.

FABs. Optics. Neoclouds. EDA. AI-RAN. Jensen isn’t buying stocks. He’s buying control points.

🔥 Here’s what he’s buying and why the 1-year returns are insane 👇

∙$INTC 422% over the past year

∙$NBIS 529% over the past year

∙$COHR, $LITE 400% over the past year

∙$NOK 157% in 2026 YTD alone, 45% in 2025 (TTM 300% )

∙$CRWV -1.6% over past year (IPO’d March 2025, YTD 53%)

∙$SNPS 2.5% over the past year

This isn’t a portfolio. It’s a supply chain.

🔵 $INTC → domestic FAB access = TSMC hedge

⚪ $CRWV $NBIS → captive GPU demand loop

🔷 $COHR, $LITE → owns the optics bottleneck at 100K GPU scale

🟣 $SNPS → lock-in via CUDA-accelerated chip design

🟢 $NOK → AI-RAN = GPU into every 5G tower

4

25

84

6,056

Jun 4

🚨 Breaking: The Claude Portfolio in InvestwithAI App is Adding Consumer names.

Claude has reduced 10% allocation from Semi and AI. Has started adding to consumer names in US snd LATAM.

🚀Trend is shifting live. Added by Claude today:

$CMG

$MELI

$FIVE

$V

But ChatGPT still leaning heavy into Tech/Semis !! Claude appears to be smart ✅

7

13

11,894

Jun 3

🚨 Leopold fund went All-in on Neoclouds for same reason !!

“Compute through 2027 is sold out.” — OpenAI CFO confirmed on @theallinpod

“If you do not have compute, you do not have revenue.”

OpenAI is passing on opportunities RIGHT NOW because of the shortage.

📝Market prices AI infrastructure on a 2-year horizon.

OpenAI buys on 6 year conjecture 📈

Where she feels most SHORT: 2030, 2031, 2032.

⛔️A single GW-scale data center = $50B 3 years to build.

The plays ?

The named proxies: $ORCL $CRWV $NVDA

But the real constraint? Power and land.

The neocloud stack I’m watching:

🔲 $CRWV — $99B backlog, OpenAI Meta locked in, take-or-pay contracts

🔲 $NBIS — AI-native cloud, NVIDIA partnership, 5GW target by 2030

🔲 $IREN — Direct NVIDIA cloud-services contract, DSX partnership

🔲 $APLD — Power campus execution play, CoreWeave as anchor tenant

🔲 $ORCL — Hyperscaler with long-dated AI contracts

The market is still pricing this on a 2-year lens.

The CFO of the most compute-hungry company on earth is buying on a 6-year lens.

💵 That gap is the trade !!

9

24

164

31,686

Jun 3

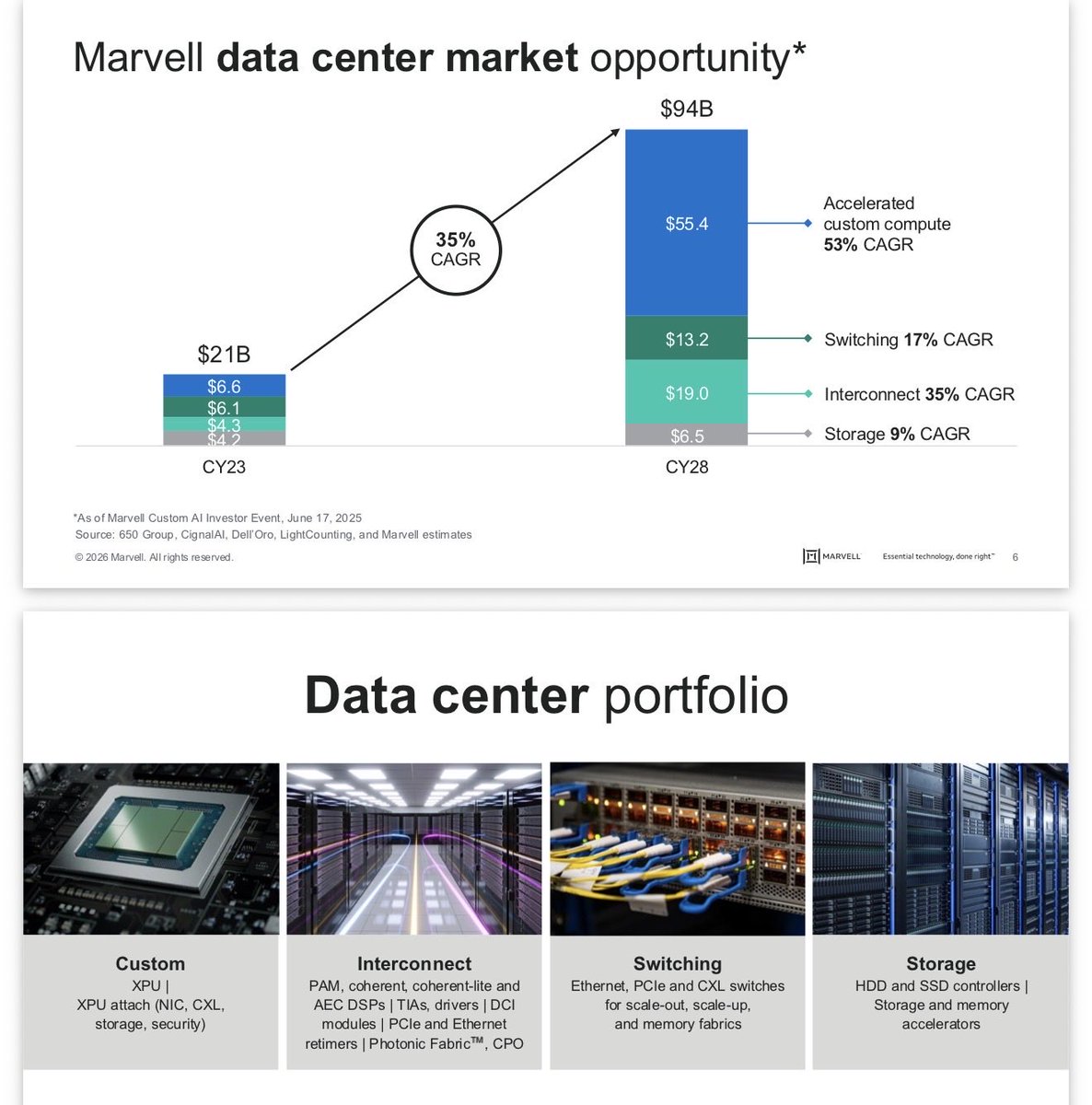

$MRVL Revenue Structure — Breakdown-

How they actually report it:

Officially, $MRVL reports 2 end markets:

1/ Data center = $6.1B (74% of total) for FY2026, vs $4.2B in FY2025 and $2.2B in FY2024

2/ Communications & Other = $2.1B (26%) for FY2026

So full-year FY2026 total = $8.2B, up 42% YoY 📈

Most recently, Q1 FY2027 data center hit $1.83B (76% of revenue), with comms & other at $585M (24%)

Within Data Center — the real breakdown you want:

The two pillars are:

1. Custom Silicon / XPU (ASIC)

This is the biggest and fastest-growing bucket — Google TPUs, Amazon Trainium, and Microsoft custom AI chips.

Custom silicon programs entered volume production in Q1 FY2026 and are the primary driver of the 76% YoY data center surge .

Analyst estimates put custom at roughly 55-65% of data center revenue in FY2026, likely approaching $ 3.5-4B for the year.

2. Electro-Optics (DSPs, TIAs, laser drivers, DCI modules)

$MRVL’s electro-optics portfolio — including high-speed PAM4 DSPs, TIAs, laser drivers, and datacenter interconnect modules — leads the market and contributes substantially to AI revenue .

The most recent Q1 FY2027 call specifically called out strength in 800G and 1.6T scale-out optics, scale-up optical solutions for NPO and CPO applications, and scale-across datacenter interconnect modules .

Optics is estimated at roughly 25-35% of data center revenue !!

3. Data Center Networking / Switching

Ethernet switches (51.2T), PCIe/CXL switches (via XConn). Smaller but growing.

The forward story:

Celestial AI (acquired Feb 2026) brings Photonic Fabric optical interconnect technology for scale-up connectivity, with Marvell expecting meaningful revenue starting H2 FY2028, targeting a $500M ARR by Q4 FY28, doubling to $1B by Q4 FY2029 .

So the optics bucket is about to get a major uplift layer on top of the existing DSP/transceiver business.

The ASIC/XPU side is what’s driving the valuation re-rate — it’s why $MRVL trades at a significant premium. Optics is the asymmetric upside kicker, especially post-Celestial AI.

Trading at life-time high P/S of 30 !!

1

9

28

3,862

Jun 2

Jensen calls $MRVL As next Trillion dollar company .

So let’s brainstorm the next Trillion Dollar List :

$SPCX | $1.75T (IPO target) | Direct IPO

$WMT | $817B

$ORCL | $687B

$V | $650B

$MU | >$1T Already crossed

$AMD | ~$300B

$BABA | ~$310B

$TCEHY | ~$500B

OpenAI | TBD | $852B (private)

Anthropic | TBD | $965B (private)

1

4

2,423