Investor. Investing in stocks to ditch the 9-5 job and gain financial freedom. Track Record (from stock picks): 2025 ( 75%)

Joined April 2021

- Tweets 5,462

- Following 1,338

- Followers 6,568

- Likes 10,603

530 Photos and videos

StockShare | Investing and Finance retweeted

How in the fuk does $tsla go absolutely fukin nowhere when markets are up like 6,000 points?

70

5

222

13,681

Good insights on the Nasdaq TFSA

STXNDQ on the JSE tracks the Nasdaq-100 at 0.46% TER - chunkier than QQQM offshore but you buy in rands and can hold it in your tax-free account.

Over a couple of decades that tax saving beats the fee difference comfortably. justonelap.com/buying-the-na…

3

608

I have some as a speculative play.

But not really that speculative because the data does look promising

$MRDN

$MRDN is a Unicorn: DD growth, trades .8x in 2.5x sector, global scaler B2B/B2C, 20 countries, Fed Brazil Lic, World Cup, content maker Expanse, 800% beat flipped positive w/.18 eps, 90% insider owned, 200mil rev, cash, low debt, huge TAM and catalysts.

2

467

Mass testing of robotaxis.

Mass rollout of cybercabs.

Mass testing of cybercabs.

Mass robotaxis/revenues for Tesla.

Can't wait! 📈💥🚀

55 Cybercabs in Dallas, Texas. These things are really stacking up now.

102 Cybercabs were spotted at the outbound lot at Giga Texas yesterday, so a lot more are continuing to be shipped around the U.S. The testing continues!

3

232

StockShare | Investing and Finance retweeted

Jun 15

$OSCR JUST HIT $30 OVERNIGHT! ON ITS WAY TO $45-$55 BY EOY!!

17

9

231

25,412

Something big is coming

1

5

588

StockShare | Investing and Finance retweeted

Jun 14

$MRDN is a Unicorn: DD growth, trades .8x in 2.5x sector, global scaler B2B/B2C, 20 countries, Fed Brazil Lic, World Cup, content maker Expanse, 800% beat flipped positive w/.18 eps, 90% insider owned, 200mil rev, cash, low debt, huge TAM and catalysts.

x.com/uboat159/status/204730…

1

2

6

3,348

StockShare | Investing and Finance retweeted

Jun 14

All good things come to those who wait:

6/12: $SPCX IPO

6/16: $SPCX options start trading

6/17: Kurv SpaceX Enhanced Income ETF ($XSHP) starts trading

🚀 Taking Off Soon: XSHP - Kurv SpaceX Enhanced Income ETF.

Built for investors seeking monthly income potential from SpaceX exposure. Available on 6/17.

Learn more: bit.ly/4vKWyM0

4

8

42

4,710

StockShare | Investing and Finance retweeted

Excellent nuggets in here $MRDN

$MRDN Market cap $180 Million

$SGHC Market Cap $6.8 Billion

A lot of growth opportunity for Meridian.

Accelerators include: post reverse split, low to no debt, FIFA world cup, increased betting, etc.

Long term investment idea:

$MRDN

I seriously don't know why this isn't talked about.

Look here. This seems like an asymmetric opportunity that fits a few categories (Fast Grower Turnaround Asset Play).

Fast Grower: This is a small cap with rapid scaling potential through organic growth and five synergistic subsidiaries (Expanse Studios growing 400% , MexPlay 52%, RKings doubled). Revenue has been compounding double-digits, with clear line of sight to acceleration. ☑️

Turnaround: Post-reverse merger, the company delivered its first GAAP profitable quarter in Q1 2026. This is the classic inflection point we want: management fixing the core business and metrics turning (very bullish).☑️

Asset Play: Extremely tight share structure (very low public float high insider ownership) combined with a valuation that still looks disconnected from the underlying business value and future cash flow potential (seems like a great play here).☑️

It has some cyclical exposure (consumer discretionary spend in EMs), but the dominant drivers are secular growth event driven catalysts.

Now time for some financials (3 core metrics):

1) Total Revenue: TTM ~$190M. Q1 2026 came in at $50.1M ( 17% YoY). Guidance and subsidiary momentum point to $210–250M annualized run-rate potential as Brazil scales.☑️

2) Gross Profit: Healthy and expanding margins. The company owns its tech stack and content (Expanse Studios), so it avoids the 15–25% aggregator fees that competitors pay. This structural advantage should widen as B2B content grows imo.☑️

3) Net Income: Clear inflection. Q1 2026 delivered GAAP net income of $2.26M ($0.18 EPS) versus a loss in the prior year. Adjusted EBITDA rose 26% to $6.3M. The prior big GAAP loss was largely a non-cash goodwill impairment (not just an operational cash burn btw).☑️

If we look at this in relation to our economy, I get even more bullish:

Government & Regulatory Tailwinds: Global wave of sports betting/iGaming legalization for tax revenue. MRDN has a 25 year regulatory track record and focuses on compliance/CSR, which helps it win licenses and crowd out black-market operators.☑️

Brazil World Cup Catalyst: The 2026 FIFA World Cup (which kicked off June 11, recently) is projected to be the largest betting event in history. Brazil is experiencing its first major regulated World Cup as a legal market. MRDN already holds the coveted Federal license and has local retail digital infrastructure.☑️

Consumer Psychology & EM Growth: Rising mobile/5G penetration young populations in Africa, Latin America, and parts of Europe support long-term growth in discretionary entertainment spend. Sports betting is sticky, especially around major tournaments (just look at any person this day in age lol).☑️

Risk on Environment: Benefits from broader digital entertainment and emerging market growth narratives, while being less exposed to saturated, high-CAC U.S. markets where big players dominate.☑️

There are a few more reasons I'm bullish this:

Valuation Disconnect: It's trading at roughly 0.85x TTM revenue while analysts see meaningful upside (average target ~$19.73). At more normalized sector multiples the stock would be substantially higher. The theses correctly highlight that this is not a story that fits neatly into simple DCF models because of the multi-subsidiary, multi-currency, high-growth nature.☑️

Share Structure Scarcity: Very low public float and high insider ownership (~80% range) mean that any meaningful institutional discovery or sustained buying can move the stock dramatically. Insiders rejected a $330M cash exit and have continued buying: strong alignment.☑️

Moat Durability: 25 years operating in difficult emerging markets, low CAC through retail betshops community trust, owned AI/tech stack, and owned content (Expanse). These are hard for large U.S. operators to replicate quickly.☑️

Management & Capital Discipline: CEO Zoran Milosevic emphasizes long-term execution over short-term promises and has a clear “we will not operate at a loss” philosophy. This matches the type of disciplined operator you tend to favor.☑️

Catalyst Path: Near-term (World Cup volume Brazil ramp), medium-term (subsidiary cross-selling margin expansion), and longer-term (continued global expansion and potential re-rating as a scaled international player).☑️

I mean cmon.

Read this:

It has just validated a profitability inflection, trades at a significant discount to its growth trajectory and sector multiples, and is entering a major catalyst window (2026 World Cup Brazil ramp) with structural moats that larger competitors have struggled to replicate in emerging markets.

Now tell me you're not bullish.

You can't lol.

If we're looking at the technicals, it is also showing us a bullish structure.

We got a double formation on the bottom, showing great support and reaction off of a long-term support line.

Now, we're retesting this resistance line again for the 3rd time (resistance gets weaker ever time we hit it).

We also have a cup and handle formation here.

I wouldn't want to be short this here.

Just my 2c.

Seems like a great stock for a long-term pick outside of the classic AI enabler/beneficiary, crypto, robotics, or health niche.

What are your thoughts?

1

6

711

StockShare | Investing and Finance retweeted

My stance on SpaceX changed yesterday:

I think it is a fantastic business.

But from investment perspective, I struggle to see how a $2 Trillion company will easily 2-10X from here in the next 3 years.

I will rather stick to growing companies at much cheaper valuations.

🚀 #reflections

1

7

497

I like this one

Jun 14

X is the only platform where you can talk to a trillionaire

1

479

StockShare | Investing and Finance retweeted

Jun 13

How can people not be bullish for $SOFI

I just don't get it

45

4

153

13,177

I like both but such a profound message

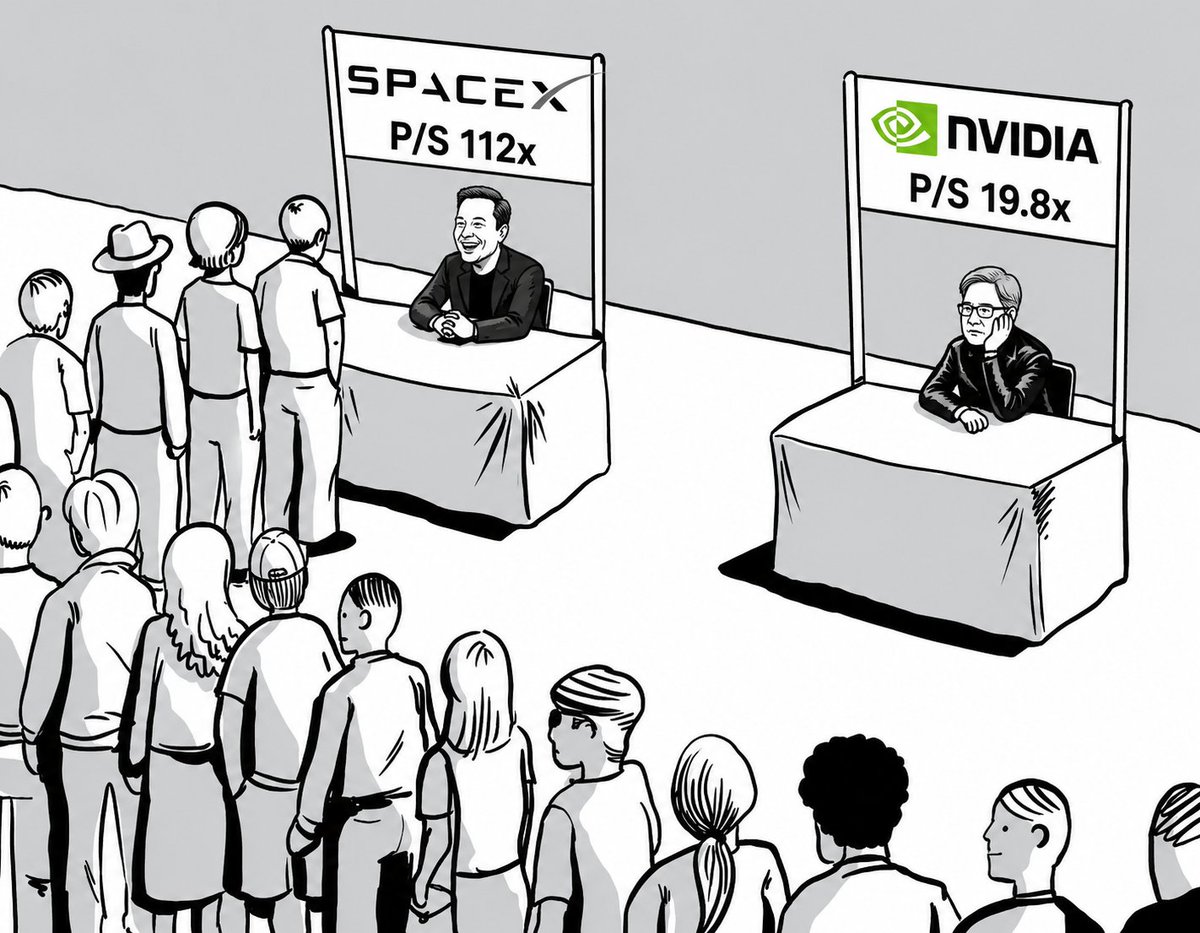

$SPCX $NVDA Crowds are lining up to buy SpaceX at 112x sales 👥🚀

Many investors think they missed Nvidia because it's already worth $5T.

Yet Nvidia trades at 19.8x sales, generates massive profits, and produces tens of billions in FCF 🤑

📊 SpaceX: 112x sales (unprofitable)

📊 Nvidia: 19.8x sales (highly profitable)

2

459

StockShare | Investing and Finance retweeted

Jun 13

I came across a data insight worth sharing.

EasyEquities reached its first R1 billion in cumulative deposits 934 days after launch.

This month, we added R1 billion in deposits in just 11 days.

What took over 2.5 years in the early days now takes less than 2 weeks.

That's an acceleration of almost 85x.

It's a reminder that compounding doesn't just happen in investment portfolios. It happens in businesses, brands, communities and trust. Progress often feels slow while you're living through it. Then one day you look back and realise just how much momentum has been built.

@EasyEquities

5

36

196

8,540