Joined July 2020

- Tweets 1,590

- Following 771

- Followers 67

- Likes 927

29 Photos and videos

Smart Investor retweeted

Mamata Bano is not even MLA now forget CM

TMC broken into pieces & she is not even consulted for LoP post in WB assembly

Firhad Hakim quits as Kolkata Mayor just now

Mahua Moitra cozying with CONgress to secure some political future

Useless Shatrughan Sinha, Kirti Azad & Derek No Brain hiding in their rat holes completely clueless

People of WB searching for Abhishek Banerjee mercilessly

Filthy mouth Kalyan Banerjee is a laughing stock now

Even Sayoni Ghosh & Sagarika Ghosh aren’t visiting Mamata Bano’s house. Of course they are opportunists & are dumping Mamata

Mamata Banerjee sold Hindustan for Power

Karma is biting her like never before

And I am really happy to see all these developments along with my fellow Nationalists

Jai Hind

Vande Mataram

Bharat Mata Ki Jai

168

1,489

5,697

101,372

Smart Investor retweeted

Keeping all politics and everything else aside, I just want to acknowledge the power and enigma of KARMA 🙏🏼

A mother who lost her daughter, her everything, didn't even get the chance to do her daughter's last rites properly, cannot even say her daughter's name out in the public, was beaten and humiliated in the public, offered money to keep silent, and a lot more; all of which happened when Mamata Banerjee was is power, was the CM of our state and also the Health Minister.

Today that mother is sitting right where Mamata Banerjee sat a month back. Yes she did not get her daughter back but somewhere somehow she found relief.

On the other hand Mamata Banerjee has lost her position as a CM, lost her own seat against Suvendu Adhikari, lost many of her own loyal party members, got kicked out of Nabanna and is also about to lose her own party's flag and symbol.

Well I don't know what else can define Karma. Ratna Debnath waited for almost 2 years but Karma never forgot to keep an account.

Har Har Mahadev 🧿

84

729

2,859

95,284

Smart Investor retweeted

🚨 SHOCKING

Old video resurfaces showing Kalyan Banerjee threatening to beat Suvendu & Sukanta to DEATH 🤯

🗣️ “Let Suvendu Adhikari and Sukanta Majumdar come to Dankuni without CISF security.

-> They won’t be able to return once they arrive.” (3 Nov, 2025)

218

3,306

7,199

163,171

Smart Investor retweeted

May 30

ये वीडियो ज्यादा से ज्यादा शेयर करें...

बंगाल के अंदर तत्कालीन BJP अध्यक्ष JP नड्डा जी पर TMC के गुंडों द्वारा हमला हुआ था

तब इस पर 'अभिषेक बनर्जी' ने कहा था :-

- यह तो जनता का गुस्सा है

- मैं इसमें क्या कर सकता हूँ?

- लोगों के आक्रोश का प्रकोप मेरी ज़िम्मेदारी नहीं है।

174

5,628

9,470

105,570

Smart Investor retweeted

🚨 SHOCKING

Old video resurfaces showing ABHISHEK BANERJEE describing the attack on J.P. NADDA as ‘PUBLIC ANGER’ 😳

🗣️ "Nadda was in trouble today in Diamond Harbour. What can I do about it? Outburst of people’s anger is not my responsibility.”

189

5,030

13,302

236,787

Smart Investor retweeted

May 21

Bandra Terminus Demolition work going on smoothly today the 3rd Day.

I Visited the site & thanked Police & Railway Police Force for making

"Bangladeshi Mukta Bandra Terminus "

Requested Railway Officials to construct Fence & Boundary Wall immediately

Police investigation going on to nail down the Master Mind behind yesterday's Stone Throwing

Kirit Somaiya

374

2,015

9,122

202,099

Smart Investor retweeted

May 21

Spoke to some of my old friends in Mumbai.

They said everyone is surprised and happy by the action against illegal encroachment at Bandra station. Most people believed it would never be removed.

But the work was completed peacefully and without much noise, apart from some minor stone-pelting.

Now, this should become an example for the entire country. The PM or HM alone cannot take responsibility for everything.

The message has already been given from the Red Fort speech and during the Bengal elections.

Delhi Haryana, Rajasthan MP Gujarat.. Every BJP-ruled state should learn from the Bandra action and work against illegal Bangladeshis and Rohingyas.

Now or never. There cannot be a bigger motivation than this. RT if you agree.

98

1,258

5,324

158,331

Smart Investor retweeted

Apr 26

Gujarat GCC Conclave | Vibrant Gujarat Regional Conference, Surat

Gujarat is bringing together industry leaders for a focused dialogue on the future of Global Capability Centers (GCCs), creating a platform for strategic insights, collaboration, and growth.

Led by GIFT City in collaboration with the Department of Science & Technology (DST), this roundtable convenes global enterprises to explore expansion opportunities through India’s first IFSC—driven by regulatory clarity, tax efficiencies, and seamless access to global markets.

Witness the conversation. Be a part of the opportunity.

📅 1st May 2026

📍 Auro University, Surat

#GIFTCity #GCC #DStT #GlobalCapability #IndiaGrowth #GlobalBusiness #GatewayToGlobalFinance #VibrantGujarat2026 #FinancialEcosystem #VGRC

@PMOIndia @CMOGuj @VibrantGujarat

2

3

24

1,076

Smart Investor retweeted

A Muslim woman was throwing pieces of meat outside Jain temples and shops in Bhopal.

When locals confronted and caught her, she immediately played the woman card: screaming "harassment" and "molestation" to escape.

295

3,374

6,859

114,812

Smart Investor retweeted

I rarely write about individuals especially in negative context. I saw both an extremely insensitive post and subsequent apology from @FI_InvestIndia.

In 2017, his wealth was concentrated primarily on these three stocks - Yes Bank, India Bulls and DHFL. I remember tracking his tweets where he kept on holding these companies despite drastic fall in prices. Those stock prices never recovered. He deleted all the past tweets to remove any trace of him holding these companies and getting wiped out due to the same.

Any of us can do blunders in markets. He is no exception. The surprising part is after losing so much wealth, never going for any employment again, he continues to claim he is financially independent.

If tweets are his source of income, that's perfectly legitimate. But claiming to be financially independent after losing wealth is extremely misleading.

145

100

1,254

229,249

In two villages of Gujarat, there's not a single Muslim family residing & there are no mosques and yet hundreds of Nikah certificates were issued by "an officer".

Gujarat DCM @sanghaviharsh bhai has ordered strict action against the people involved.

108

4,396

15,285

240,916

Smart Investor retweeted

Feb 20

7 ILLEGAL BUILDINGS being demolished in Mumbra🔥🔥

DevaBhau ka bulldozer sirf Mumbai main nahi, Cobra 🐍 ki territory main bhi huan hain 🔥🔥

Recall how #JitendraAwhad used to call himself a Cobra 🐍 jo har kisiko das jayega?😂

How all these illegal structures came up under his benevolent eye ?

Kaise Haraya usko uske hi ex-dost ki beti ne😂😂

#BulldozerDeva ne jo kaha, woh kar dikhaya 💪💪🔥🔥

Detect, detain & deport of ghoospaithiye from Maharashtra will BREAK all records this year 🔥🔥

Feb 20

OMG

I am still rubbing my eyes in disbelief

It was always said that BMC officials don’t have GUTS to go to M dominated areas like Md Ali Road, Jogeshwari & Kurla

But with proper political backing & police action, it’s possible 🔥🔥

Last year, DevaBhau got all ILLEGAL BHONGAS📢 removed from m0sks

This year, illegal shops & encroachments removed by BulldozerDeva🔥🔥

I am sure there’s co-ordination with MHA to get ghoospaithiye detected, detained & deported 🔥🔥

Dhanyawad BulldozerDeva for helping us honest tax paying Mumbaikars reclaim our city🙏🙏

With FIRST BJP Mayor & head of Standing Committee in BMC , we will soon get the Mumbai of our dreams, our aspirations

39

487

1,359

58,898

Feb 20

Very few can articulate as good as @manurishiguptha when it comes to market insights build with strong reasoning backed by visible evidence. Tks

The Illusion of a Floor/Bottom/Support – In case the SIP Shield Cracks

And a call for a tribute to the market legend Siddhartha Bhaiya of Aequitas

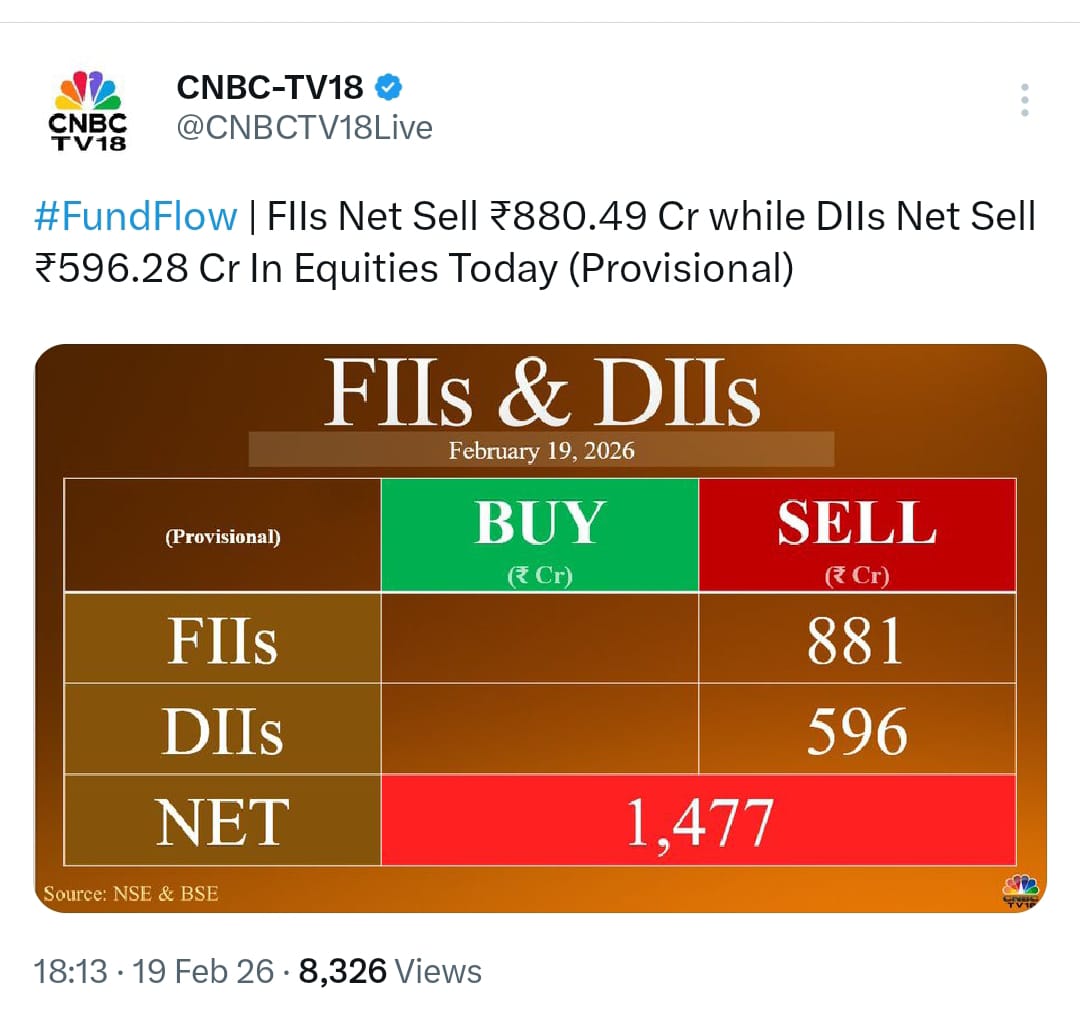

Yesterday's (19th Feb) market action was a sobering reminder of just how fragile India's equity rally has become.

Despite a combined FII and DII net selling of a mere ₹1,477 crore, which is barely 0.0018% of the mutual fund industry's ~₹81 lakh Cr AUM as of Jan 2026 and just about 5.9% of the ~₹30,000 Cr monthly SIP inflows recorded last month, Nifty and Bank Nifty plunged nearly 1.4%. A negligible ripple in the ocean just erased billions in market cap.

Investing in India has transitioned from a financial decision to a "demonstration of patriotism." In reality, the FIIs just need to "NOT SELL", and indices soar. These flows are peanuts in the grand scheme, yet they are swinging the markets wildly.

For 5 years, the middle-class SIP machine has powered Indian Markets to stratospheric heights under the banner of "financialization of savings" But what happens if a global headwind sparks even a modest 5-10% redemption from that ₹81 Lakh Cr AUM?

Where is the counterparty?? Who is the counterparty?? SADLY - THERE IS NONE

Domestic buyers (retail institutions) have been the nonstop fuel. But in a true exodus, FIIs - who've been net sellers of barely ~2-3% of their total holdings so far over 5 years (cumulative outflows ~₹98K Cr) could flee faster, creating an unfillable vacuum.

No counterparty implies - no floor, no bottom, no support. Slides could accelerate unchecked.

With a counterparty (or lack of it thereof) risk, Indices could easily retrace 30-50% or more. We are trading at a forward P/E of 22x - one of the world's most expensive markets - while peers like China (12x) and Brazil (11x) come across as markets on fire sale.

What's more concerning is that our economy isn't producing cutting-edge, global-problem-solving companies to absorb this capital deluge. Instead, we are creating sub-optimal firms in a hyper-competitive environment (food delivery, resellers, etc.), that are gulping and then burning funds at nosebleed valuations.

Ironically, Swiggy - a recent market darling came out with a QIP barely a little after its IPO.

To put this a bit more succinctly -

"ब्याह की मेहंदी उतरी नहीं और चले बेइज्जत होने"

"The honeymoon isn't over, and the debaucherous scandal has begun."

These "futuristic growth" companies won't see free cashflows or dividends for years, maybe decades. The Ola, Paytm, Swiggy, Zomato, and Nykaa debacles weren't outliers. They were an example of criminal breach of retail investors' trust.

Scale that up, and you have a market built on expensive storytelling rather than fundamentals.

Institutional cheerleaders like Raamdeo Agrawal Ji of Motilal and Nilesh Shah Ji of Kotak bear some definite burden of responsibility here.

They’ve herded retail into this setup, pushing "long-term" narratives while ignoring the structural risk of the exit door.

If redemptions hit, the psychological toll on India’s new investor class (that took birth during the COVID lockdown) will be devastating. It won't just be a financial loss; it will stall the "financialization of savings" story cold.

Trust and Confidence, takes decades to build but only one liquidity vacuum to shatter.

Siddhartha Bhaiya of Aequitas who left us suddenly with an insurmountable emptiness, called out the Indian markets as a bubble of epic proportions. Let's prove him wrong by selling just just 2% of the MarketCap of India as an experiment or risk evaluation/mitigation exercise.

If we succeed in proving him wrong, he will still smile in his abode up there - as markets will stay safe, as will the retail investors ......

Is it time to question the dream before it turns into a nightmare??

As Bob Dylan says - The answer my friend is blowing in the wind......

1

25

Smart Investor retweeted

Feb 8

TMC MP Kalyan Banerjee loses his mind reading chargesheet! Screaming “WHO PRINTED THIS?!” 😂

Forgot we live in a democracy, Kalyan Babu? Yes, people can print your crimes. Shocking, right? This is TMC’s defense: attack the printer, ignore the corruption!

Thanks for the endorsement though: #PaltanoDorkarChaiBJPSorkar

Keep melting, we appreciate it! 👏

38

400

1,182

36,468

Smart Investor retweeted

Feb 5

Dear 60% population of West Bengal, read, reflect, and ruminate......

220

5,635

19,102

181,104

Bansuri Swaraj is one of the lawyers that represented WB GOVT EMPLOYEES in SC in DA case.

Kapil Sibal and Abhishek Manu Singhvi represented TMC Govt.

Remember BENGALIs,who fought for the right of our family members,our brothers,our sisters,our uncles and aunts.

41

918

4,158

47,992

Smart Investor retweeted

Feb 5

Very unfortunate that Hon’ble @MahuaMoitra ji is being trolled. We who count ourselves as fans of the revered, internationally versatile, NYT columnist demand to know how anyone got access to Sakshat Durga’s IMessage chats at 12.42 am!

79

666

4,508

234,268

Smart Investor retweeted

Jan 27

I thought your brain was far superior than Rahul Gandhi…..but now I know, I was wrong.

Mr Singhvi, This is 2009, look where LoP sitting, can’t even count the line number.

Rahul’s politics now looks less like leadership and more like a child crying in the aisle because he didn’t get his candy.

Jan 27

Protocol is not a favour; grace is not optional. When both are missing, it says more about the moment than the men slighted. Disturbing, but sadly unsurprising in these times.

24

313

809

27,561

Smart Investor retweeted

Someone told me you are legal expert

This is 2009, look where LoP sitting

I know once ur in congress u have to act like buffoon

Jan 27

Protocol is not a favour; grace is not optional. When both are missing, it says more about the moment than the men slighted. Disturbing, but sadly unsurprising in these times.

75

1,929

8,264

688,003