A structural atlas of investable industries.

Joined May 2026

- Tweets 53

- Following 71

- Followers 20

- Likes 6

33 Photos and videos

Jun 15

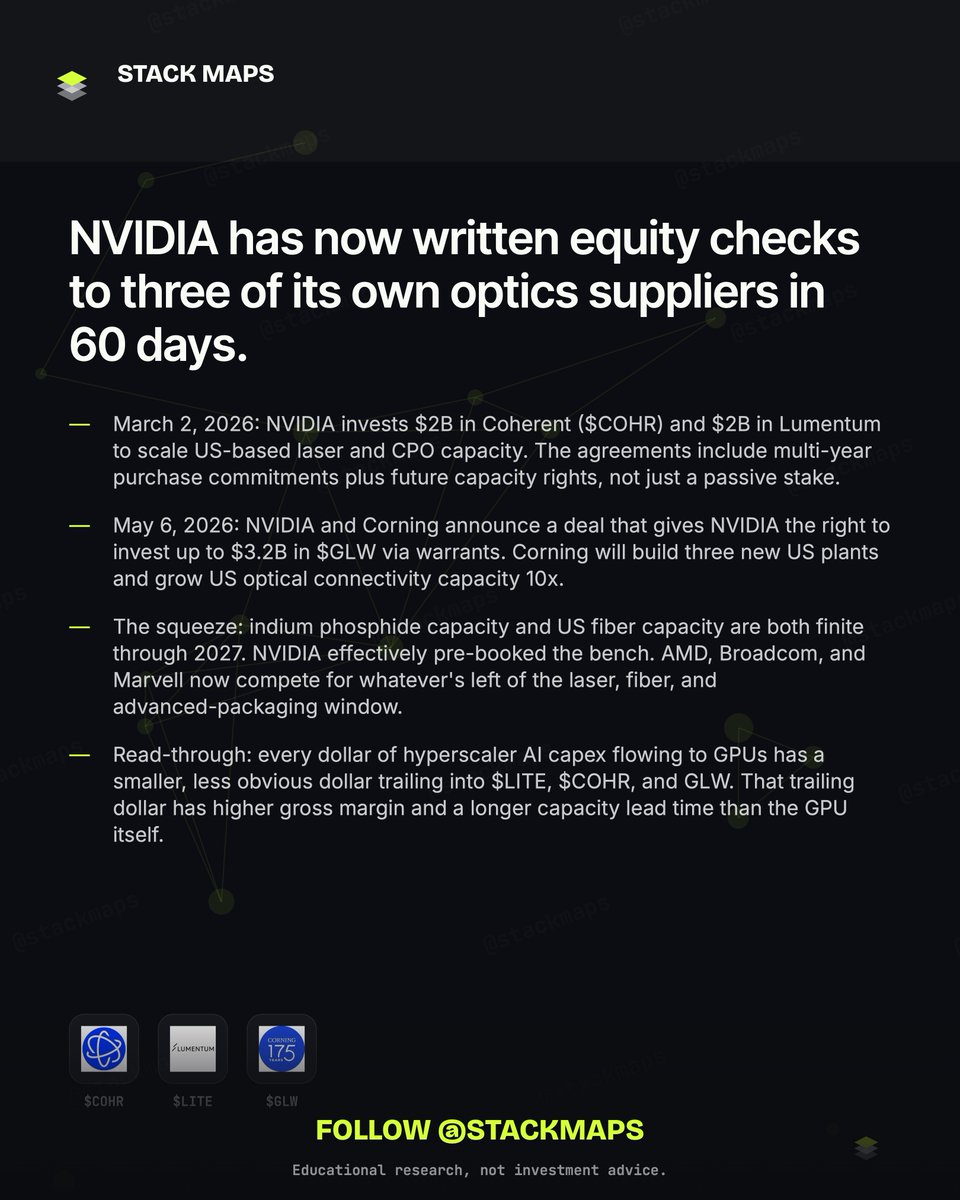

NVIDIA has now written equity checks to three of its own optics suppliers in 60 days.

$COHR: $2B. $LITE: $2B. $GLW: up to $3.2B in warrants.

This isn't a partnership story. It's a vertical lock on the physical layer of AI. Who actually gets squeezed:

March 2, 2026: NVIDIA invests $2B in Coherent ($COHR) and $2B in Lumentum to scale US-based laser and CPO capacity. The agreements include multi-year purchase commitments plus future capacity rights, not just a passive stake.

May 6, 2026: NVIDIA and Corning announce a deal that gives NVIDIA the right to invest up to $3.2B in $GLW via warrants. Corning will build three new US plants and grow US optical connectivity capacity 10x.

The squeeze: indium phosphide capacity and US fiber capacity are both finite through 2027. NVIDIA effectively pre-booked the bench. AMD, Broadcom, and Marvell now compete for whatever's left of the laser, fiber, and advanced-packaging window.

Read-through: every dollar of hyperscaler AI capex flowing to GPUs has a smaller, less obvious dollar trailing into $LITE, $COHR, and GLW. That trailing dollar has higher gross margin and a longer capacity lead time than the GPU itself.

Source: sec.gov, corning.com, cnbc.com

Follow @StackMaps 🔔 for the rest of this stack mapped end to end. DMs open.

#AI #datacenter

Educational research, not investment advice.

1

1

223

Jun 12

RT @GoldmanSachs: SpaceX is redefining industries on Earth and aiming to create new ones beyond it.

On June 11, it successfully priced its…

1,136

Jun 12

In 2008, SpaceX was three launch failures deep and weeks from dead. Today it priced the largest IPO in human history. The 24-year road to $SPCX, in one thread 👇

2002: Elon Musk founds SpaceX with money from the PayPal sale. The goal sounds absurd at the time: drop the cost of reaching orbit by 10x, eventually settle Mars.

2006 to 2008: Falcon 1 fails three times in a row. The company is nearly bankrupt. Flight 4, in September 2008, reaches orbit. SpaceX survives by weeks, then wins a NASA cargo contract that December.

2010 to 2012: Dragon becomes the first commercial spacecraft to orbit and return, then the first to berth with the ISS. The commercial space era starts here.

December 2015: a Falcon 9 booster lands back at Cape Canaveral. First orbital-class booster landing ever. Reuse goes from punchline to business model.

2020: Crew Dragon flies NASA astronauts. 2024: a launch tower catches a returning Super Heavy booster out of the air. 2025: 165 orbital launches in a single year, more than every other launch provider on Earth combined.

June 12, 2026: SPCX begins trading on Nasdaq. ~$1.77T valuation. From three failures and a near-death December to the largest IPO ever, in 24 years.

Follow @StackMaps 🔔 for the long arcs behind every ticker.

#SpaceX #SPCX

Educational research, not investment advice.

1

3

758

Jun 12

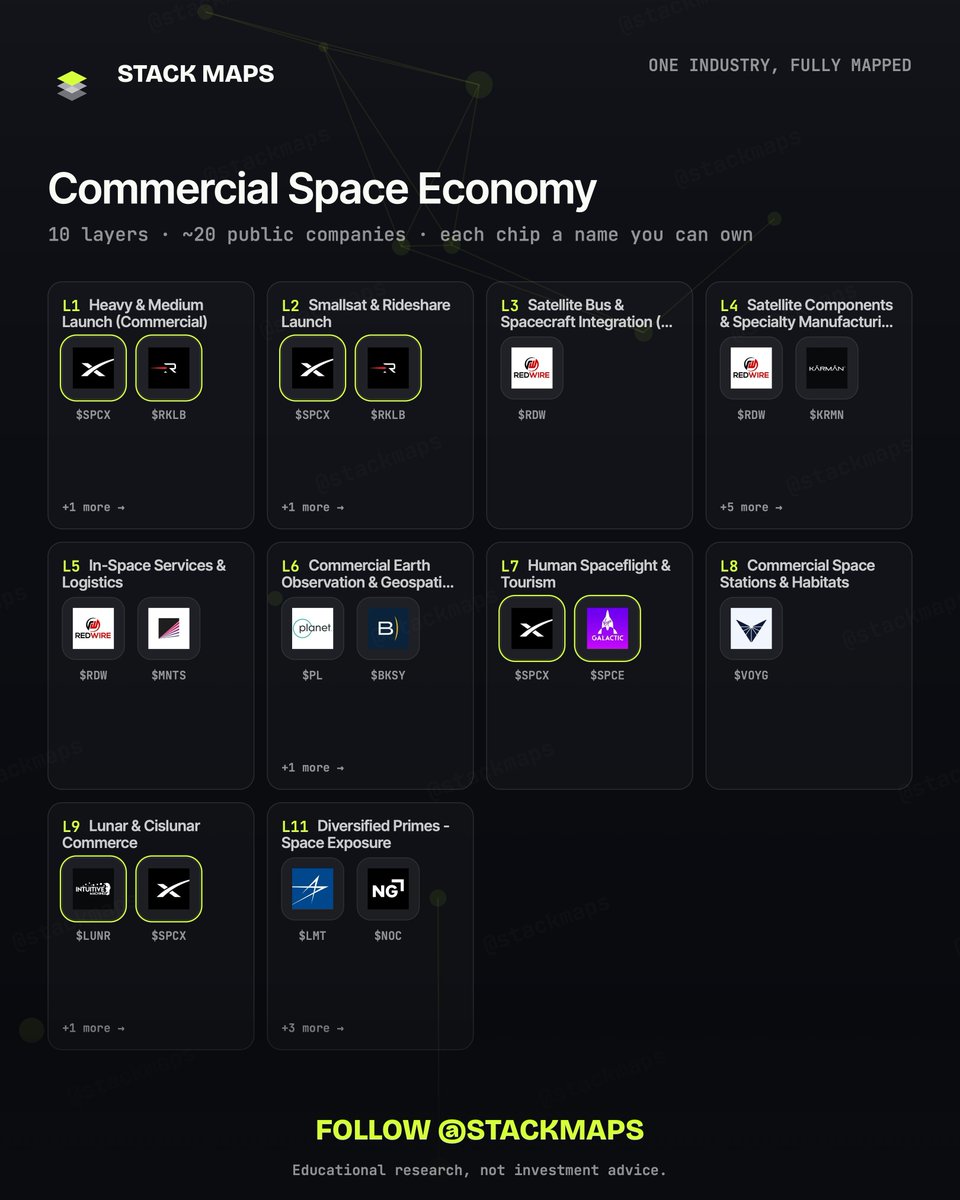

$SPCX didn't just join the market today. It joined the map. Here's where SpaceX actually sits in the 11-layer Commercial Space Economy stack 👇

Layer 1, Heavy & Medium Launch: the anchor. Falcon 9 and Falcon Heavy moved ~86% of 2024 global upmass. The layer's other public names: $RKLB (Neutron, Q4 2026 target) and $FLY (Miranda, in development).

Layer 2, Smallsat & Rideshare: SpaceX's Transporter program is the price-setter for small payloads; $RKLB Electron is the dedicated-ride workhorse with 21 flights in 2025.

Layer 7, Human Spaceflight: Crew Dragon is the only operating US crew system, flying NASA rotations and private missions. $SPCE is the suborbital trailblazer in the same layer.

Layer 9, Lunar: Starship HLS is on contract for NASA's crewed Artemis landings, alongside $LUNR and $FLY landers already on the Moon's surface.

And over in our Broadband & D2C stack, Starlink anchors the direct-to-device layer against $ASTS, $GSAT and $IRDM. One ticker, five layers, two stacks. That's what vertical integration looks like on a map.

Want the full 11-layer map as a poster? DM 'SPACE'.

#SPCX #space

Educational research, not investment advice.

2

156

Jun 12

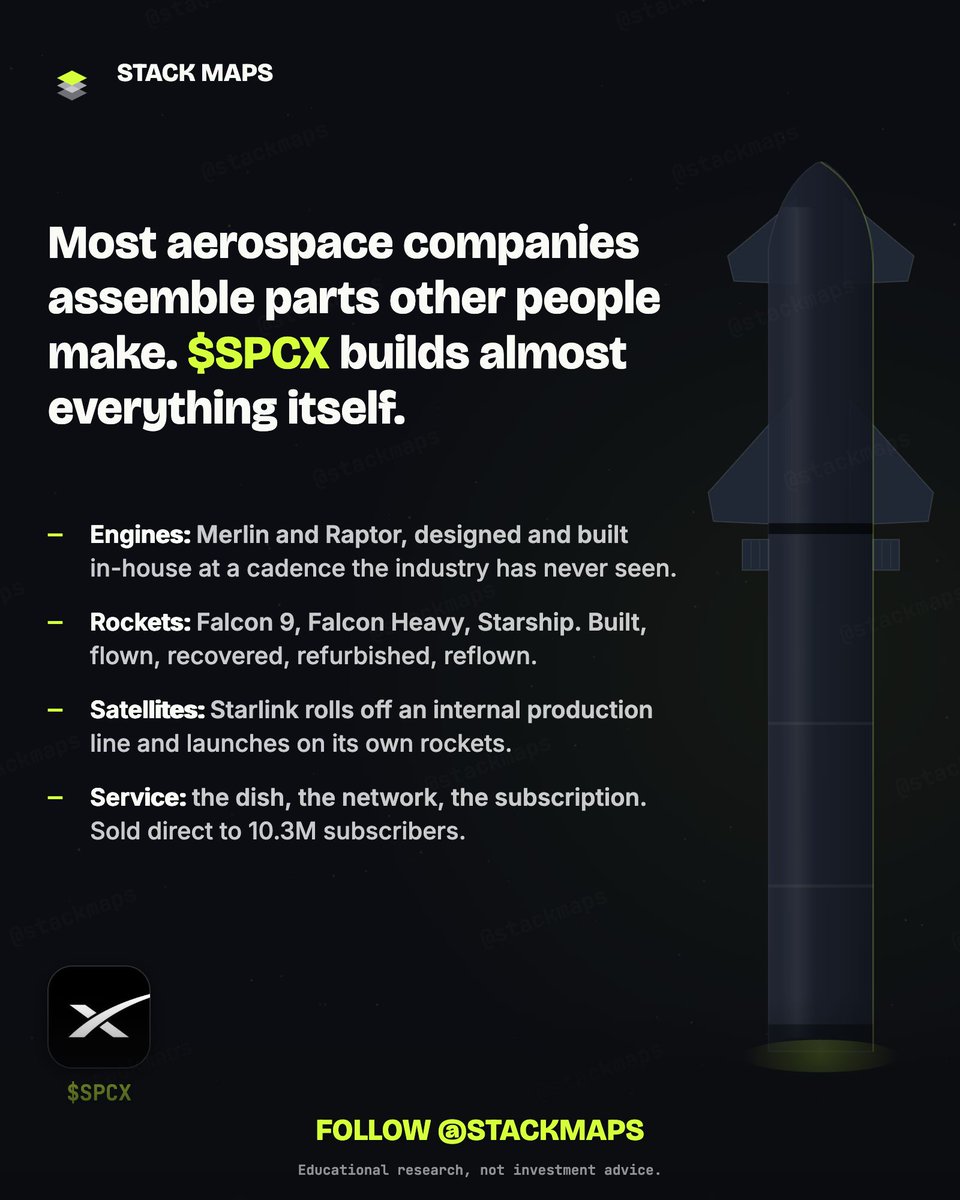

Most aerospace companies assemble parts other people make. $SPCX builds almost everything itself: the engines, the rockets, the satellites, even the dish on your roof. The vertical integration inside SpaceX is the real moat, and it's worth understanding 👇

Engines: SpaceX designs and builds its own. Merlin for Falcon 9, Raptor for Starship. Most launch companies buy engines from suppliers; SpaceX prints them in-house at a cadence the industry has never seen.

Rockets: Falcon 9, Falcon Heavy, Starship. Designed, built, flown, recovered, refurbished and reflown by one company, with the reuse loop feeding cost data straight back into design.

Satellites: Starlink birds roll off an internal production line. When your rocket is also yours, you can afford to launch thousands of your own satellites and iterate the design constantly.

Terminals and service: the user dish, the ground network, the subscription. SpaceX sells the end service directly to 10.3M subscribers instead of wholesaling capacity.

Engines to invoices, one company. That loop (build, fly, recover, learn, rebuild) is what competitors, public or private, have to answer. It's also why the S-1 reads like four companies stapled together.

Follow @StackMaps. We break entire industries into investable layers like this.

#SPCX #SpaceX

Educational research, not investment advice.

1

94

Jun 11

$MP Q1 2026, by the numbers. The DoD price-floor architecture started showing up on the income statement. Six things that matter, in order.

1. Revenue $90.6M, up 49% YoY. Add the price protection agreement income and the consolidated number is $132.9M, a 28% sequential jump from Q4.

2. NdPr production: 917 metric tons, a company record, up 63% YoY. Sales: 1,006 tons, more than double prior year and 79% above Q4.

3. Adjusted EBITDA flipped to $36.6M from a $2.7M loss a year ago. Adjusted EPS $0.03 vs a consensus $0.01 loss.

4. Materials segment alone (revenue PPA): $114.5M, roughly double Q1 2025. Magnetics: $21.1M revenue, $9.6M adjusted EBITDA. $MP

5. Cash short-term investments: $1.7B at quarter end. Q1 capex $77.4M, about 60% going to magnetics, i.e. the 10X build.

6. Apple prepayments now total $72M, with $32M received in February. Heavy rare-earth separation commissioning starts imminently at Mountain Pass.

Source: stocktitan.net, investing.com, gurufocus.com

Follow @StackMaps 🔔 for fresh stack maps every week. DMs open for the full poster.

#earnings #rareearths

Educational research, not investment advice.

1

151

Jun 11

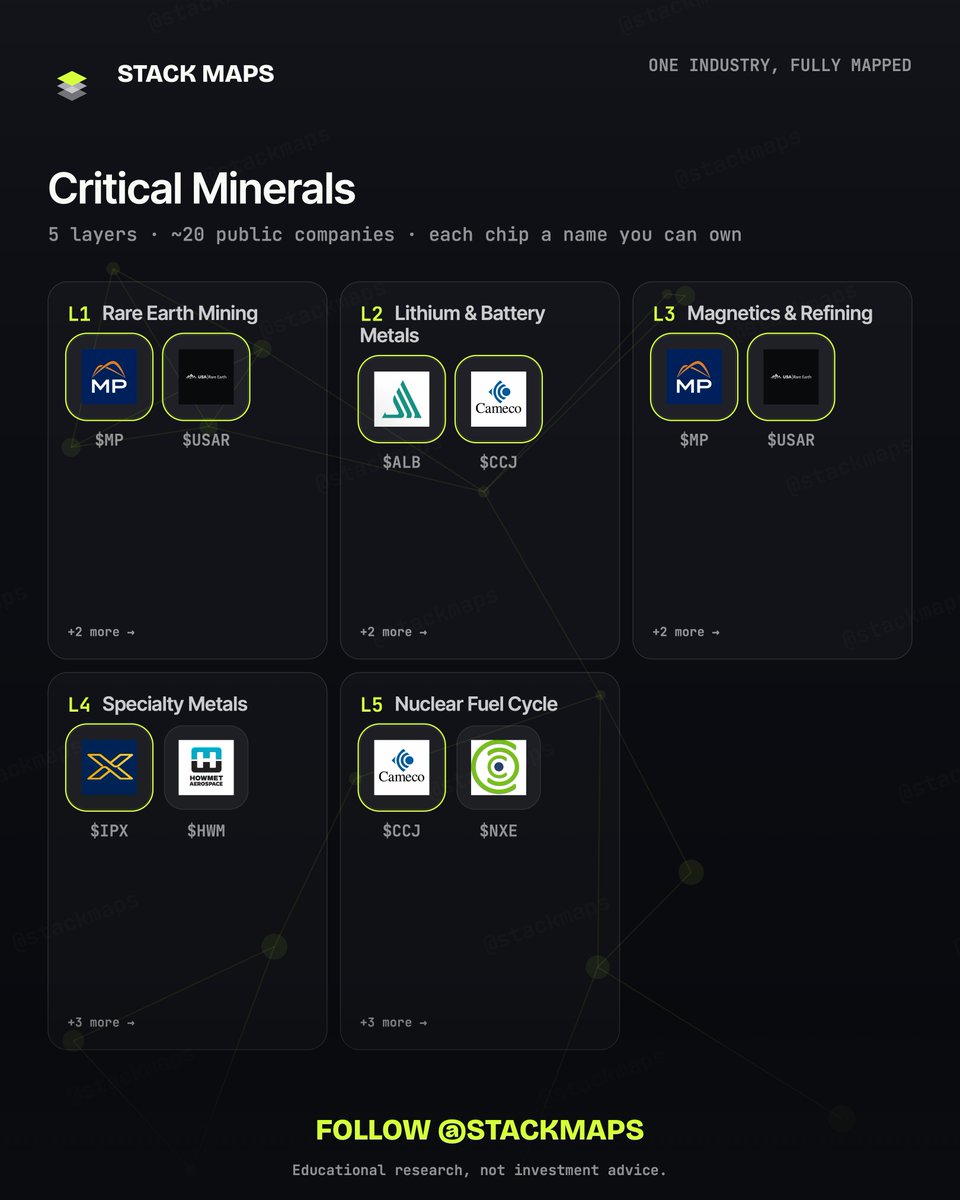

The Critical Minerals stack is 5 layers deep.

Most investors own one or two. Here's the lead of each layer — and the number that proves it. 👇

L1. Rare Earth Mining — $MP: Consolidated revenue/PPA income of $132.9M with $36.6M adjusted EBITDA, EPS $0.03

L2. Lithium & Battery Metals — $ALB: Albemarle Q1 sales up 33% to $1.4B; adjusted EBITDA more than doubles to $664M

L3. Magnetics & Refining — $USAR: USAR posts Q1 revenue ~$6M from LCM metals; adjusted net loss $24.1M (-$0.12/share)

L4. Specialty Metals — $IPX: IperionX commissions 300-ton six-axis SACMI press, tripling powder metallurgy capacity

L5. Nuclear Fuel Cycle — $CCJ: Westinghouse 2026 adjusted EBITDA share guided to USD 370–430M, down from 2025 Korean-project boost

Every figure above is from public earnings calls & company releases — not advice, just the map.

Follow @StackMaps 🔔 for a layer-by-layer breakdown of every investable industry.

#investing #stocks

Educational research, not investment advice.

56

Jun 10

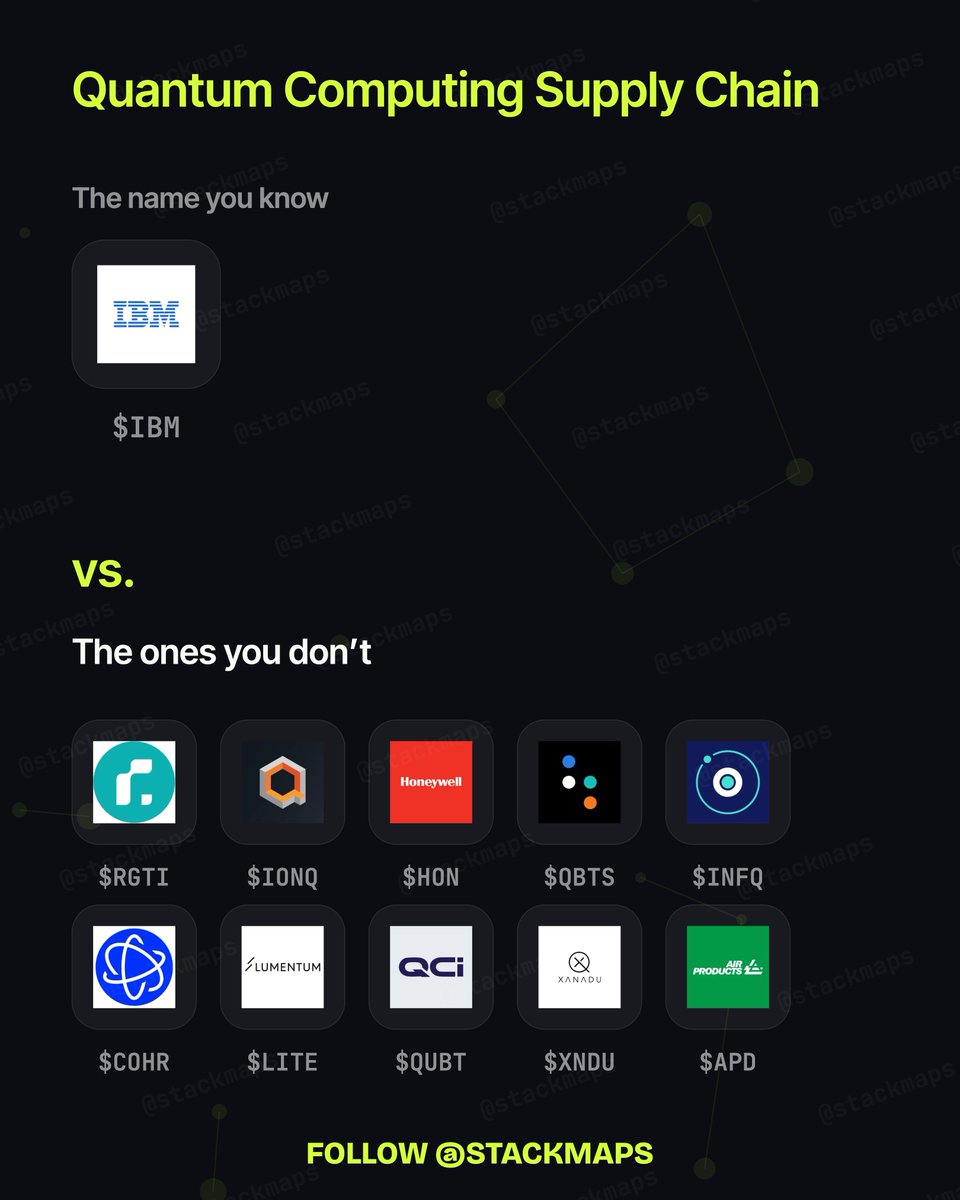

The Quantum Computing Supply Chain stack is 9 layers deep.

Most investors own one or two. Here's the lead of each layer — and the number that proves it. 👇

L1. Superconducting Qubit Hardware — $IBM: IBM reiterates FY26 guidance of 5% revenue growth and ~$1B free cash flow growth

L2. Trapped-Ion Hardware — $IONQ: IonQ posts record Q1 2026 quarterly revenue, stock surged 59.7% in May

L3. Annealing & Specialty — $QBTS: D-Wave reports $24.6M annual revenue against >$70M operating loss

L4. Photonics & Optics — $COHR: Coherent Q3 delivered 21% revenue growth, 55% EPS growth; Q4 guide implies acceleration

L5. Classical Co-Processor — $NVDA: NVIDIA revenue rose 85% year over year in latest quarter

L6. Cryogenics, Dilution Refrigerators, and H… — $APD: APD FQ2 2026 earnings beat expectations; helium supply risk from Hormuz Strait flagged

L7. Quantum Control and Measurement Electroni… — $KEYS: Keysight posts record Q2: orders 56% to $2.05B, revenue 31%, EPS 69%

L8. Photonics and Specialty Optics for Qubit… — $MKSI: Director Colella Gerald G sold ~34% of estimated MKSI holdings (~$6,668,075)

L9. Foundry, Cloud Distribution, and Post-Qua… — $ARQQ: Heritage Assets SCSp. disclosed a SCHEDULE 13D activist stake in ARQQ

Every figure above is from public earnings calls & company releases & SEC filings — not advice, just the map.

Follow @StackMaps 🔔 for a layer-by-layer breakdown of every investable industry.

#investing #stocks

Educational research, not investment advice.

2

82

Jun 9

The Aging Power Grid stack is 5 layers deep.

Most investors own one or two. Here's the lead of each layer — and the number that proves it. 👇

L1. Transmission Equipment — $ETN: Eaton posts Q1 record $7.5B revenue, $2.81 adj EPS, raises FY26 organic growth to 9-11%

L2. Generation Mix — $NEE: NextEra Q1 adjusted EPS up 10% YoY; 2026 guidance reiterated at high end of $3.92–$4.02

L3. Build & Interconnect — $PWR: Quanta raises FY2026 guidance: revenue $34.7-35.2B, adj EPS $13.55-14.25

L4. Utilities - Transmission Owners — $AEP: AEP posts Q1 2026 operating EPS of $1.64 and reaffirms FY2026 guidance of $6.15-$6.45

L5. Utility-Scale Battery Storage and Grid-Fi… — $TSLA: Tesla energy storage gross margin hit record 39.5% but deployments fell 38% Q/Q

Every figure above is from public earnings calls — not advice, just the map.

Follow @StackMaps 🔔 for a layer-by-layer breakdown of every investable industry.

#investing #stocks

Educational research, not investment advice.

1

71

Jun 8

$LITE is now a quantum stock by accident. The Lumentum-NVIDIA $2B deal in March 2026 is sold as an AI optics play. Read it again. The same indium phosphide pump lasers feed cold-atom and trapped-ion systems.

On March 2, 2026 NVIDIA announced multi-year strategic agreements with Lumentum to accelerate advanced optics technologies. NVIDIA is investing $2 billion in Lumentum to support R&D, future capacity and operations as the company builds U.S.-based manufacturing in a new fab.

Lumentum Q3 FY26 revenue:

$808.4M, up 90.1% YoY. The growth is AI transceivers, not quantum. But the same fab makes pump lasers and narrow linewidth laser assemblies, the exact components neutral-atom and trapped-ion startups buy.

Pump lasers cool atoms. Narrow linewidth lasers drive Rydberg transitions. The capacity that NVIDIA just funded is the same capacity quantum hardware vendors line up for.

$LITE is a 90% AI-revenue stock with a real, second-order quantum supply position nobody is pricing. $NVDA underwrote both.

Follow @StackMaps 🔔 for the cross-stack ties fintwit misses.

#quantum #AI

1

123

Jun 8

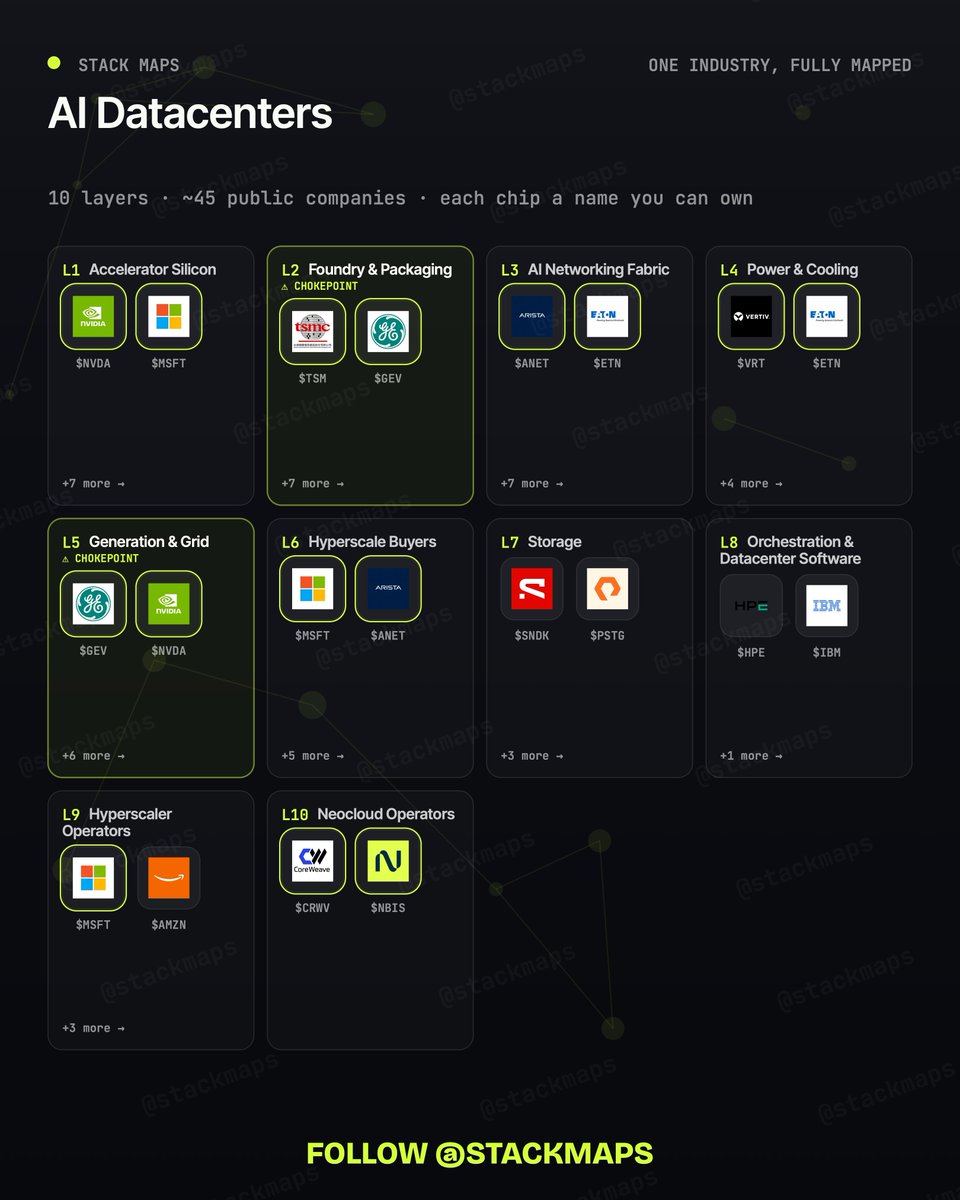

The AI datacenter trade is 10 layers deep.

Most people own 1 or 2. Here's the leader of each, with the actual Q1 2026 number that proves it.

A tour 👇

L1. Accelerator silicon.

$NVDA Q1 FY27 data center revenue: $75.2B, up 92% YoY. Networking alone (Spectrum-X, NVLink, InfiniBand) hit $14.8B, nearly tripling. Hyperscalers were ~50% of data center revenue; the other half is AI clouds, sovereign, enterprise.

L2. Foundry & packaging.

$TSM CoWoS is the binding constraint. ~75–80k wafers/month today, target 120–130k by end of 2026. ASP per wafer reportedly near $10k, the level of a 7nm process node. Advanced packaging hit ~10% of TSMC revenue in 2025.

L3/L4. Networking cooling.

$ANET Q1 2026 revenue $2.71B ( 35% YoY); raised 2026 AI fabric target to $3.5B.

$VRT Q1 revenue $2.65B, $15B backlog after Q4 orders surged 252% YoY. Book-to-bill of ~2.9x.

L5. Generation & grid.

$GEV Q1 orders $18.3B, 71% organic. Gas turbine backlog slot reservations went from 83 GW to 100 GW in one quarter. Electrification booked $2.4B of data-center orders, more than all of 2025.

$ETN backlog up 48% in Electrical sector.

L9/L10. Operators.

$CRWV: $99.4B backlog, $2.08B Q1 revenue, ~1 GW active power, targeting 8 GW by 2030.

$NBIS: $399M Q1 revenue ( 684% YoY), secured a 1.2 GW Pennsylvania site, $20–25B 2026 capex.

The hyperscalers ($MSFT $GOOGL $META $AMZN) are paying all the bills.

Follow @StackMaps 🔔 for layer-by-layer breakdowns of every investable industry.

#AI #datacenter

86

Jun 6

$XNDU built a 12-qubit photonic quantum computer where information rides on "squeezed light". Squeezed how? Below the vacuum noise floor of the electromagnetic field itself. The science behind Aurora, and why it changes the supply chain.

Aurora is a universal photonic quantum computer consisting of four modular and independent server racks photonically interconnected and networked together. This 12 qubit machine consists of 35 photonic chips and a combined 13 km of fiber optics all operating at room temperature.

The qubit is not the photon. It is the photon's light field. Xanadu approaches it through continuous-variable encoding: looking at the photon's light field distribution across amplitude and phase, squeezing them (reducing uncertainty in amplitude at the cost of phase) to encode data.

Aurora was published in Nature. The system

uses 84 squeezers and 36 photon-number-resolving detectors furnishing 12 physical qubit modes per clock cycle, with a cluster state entangled across 86.4 billion modes. That's the science.

The read-through to suppliers: photon-number-resolving detectors today are SNSPDs, the cryogenic single-photon detector everyone needs but few make. The component layer wins either way. $COHR $LITE.

Follow @StackMaps 🔔 for layer-by-layer reads on the quantum stack.

#quantum #photonics

1

318

Jun 6

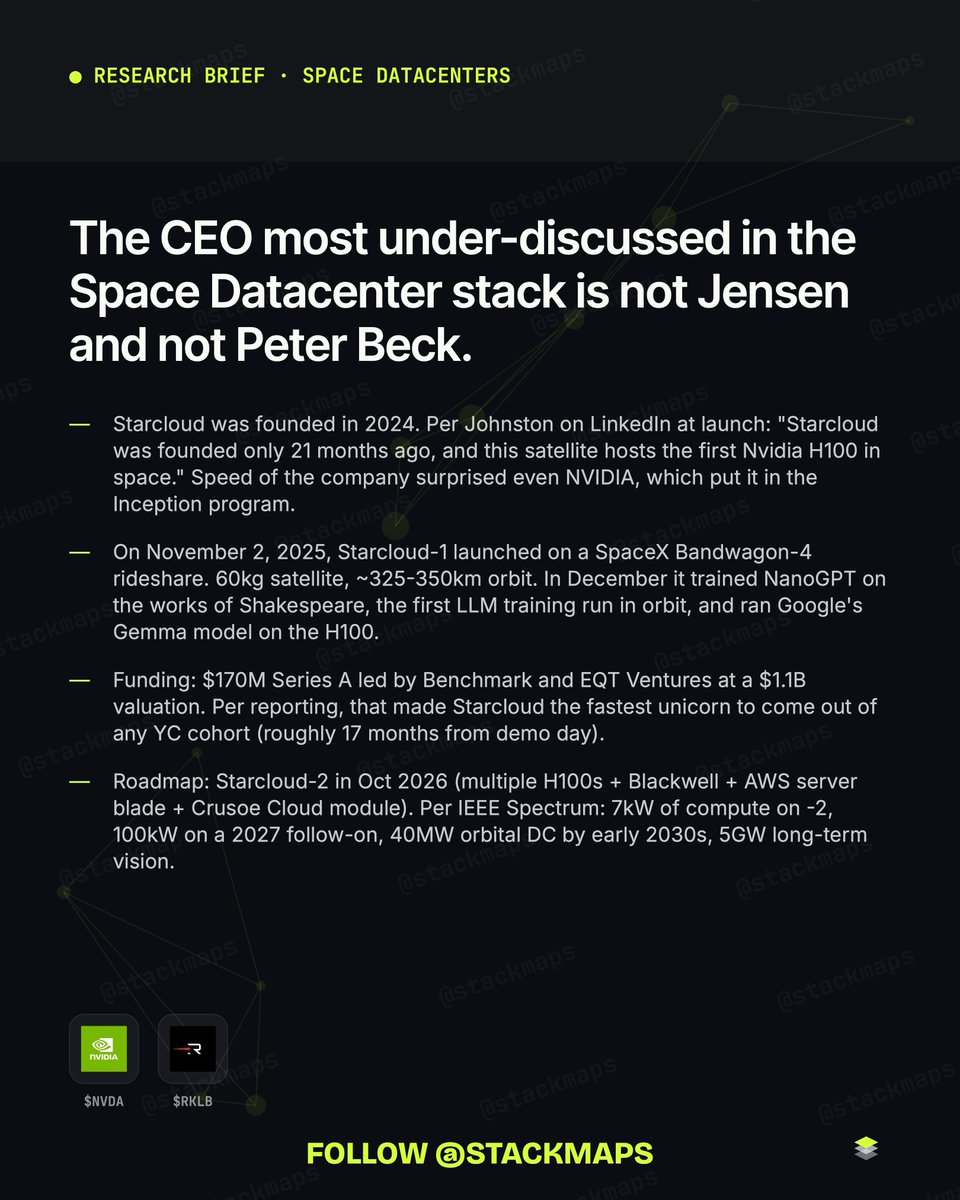

The CEO most under-discussed in the Space Datacenter stack is not Jensen and not Peter Beck.

It's Philip Johnston of Starcloud. The private operator that just put the first H100 in orbit and trained an LLM there 21 months after the company was founded. $NVDA

Starcloud was founded in 2024. Per Johnston on LinkedIn at launch: "Starcloud was founded only 21 months ago, and this satellite hosts the first Nvidia H100 in space." Speed of the company surprised even NVIDIA, which put it in the Inception program.

On November 2, 2025, Starcloud-1 launched on a SpaceX Bandwagon-4 rideshare. 60kg satellite, ~325-350km orbit. In December it trained NanoGPT on the works of Shakespeare, the first LLM training run in orbit, and ran Google's Gemma model on the H100.

Funding: $170M Series A led by Benchmark and EQT Ventures at a $1.1B valuation. Per reporting, that made Starcloud the fastest unicorn to come out of any YC cohort (roughly 17 months from demo day).

Roadmap: Starcloud-2 in Oct 2026 (multiple H100s Blackwell AWS server blade Crusoe Cloud module). Per IEEE Spectrum: 7kW of compute on -2, 100kW on a 2027 follow-on, 40MW orbital DC by early 2030s, 5GW long-term vision.

Why you should care even though Starcloud is private: every public name in this stack ($NVDA, $RKLB-adjacent optical, ground station operators) is downstream of how fast Starcloud scales. If they file an S-1, the read-through hits L5 and L7 first. $NVDA

Follow @StackMaps 🔔 for operator-level intel mainstream coverage skips.

#space #startups

1

144

Jun 5

There is no publicly traded pure-play for orbital data center thermal management. That is the most overlooked fact in this entire stack.

Layer 4 (radiative cooling) is the binding constraint nobody can buy directly. Here is why that matters and where to look. $HON

Earth-based data centers dump heat into air or water. In space there is no convection. Only radiation. Jensen Huang said it directly at GTC 2026: "there's no convection, there's just radiation, and so we have to figure out how to cool these systems out."

Starcloud's published vision: a 5GW orbital data center with cooling and solar panels ~4km on a side. The radiator surface area required for gigawatt compute is the actual engineering bottleneck. It is currently being solved in-house at primes and private operators.

Public exposure today: $HON sells space-grade thermal loops as a side business inside its aerospace segment. That is the closest listed name. It is not a pure-play. There is no $MCHP-equivalent specialty radiator vendor on US exchanges yet.

This is the layer most likely to mint a new ticker in the next 12 to 24 months. Either via a private operator IPO (Starcloud, Axiom) bringing thermal capability with it, or via a focused supplier spinning out. Worth watching this slot in every quarterly S-1 sweep.

Until then, the cleanest way to play L4 is to assume the prime integrators absorb the engineering risk and demand it back through bus-level pricing. $LMT $NOC $LHX are indirect proxies. None of them are clean. $HON

Follow @StackMaps 🔔 if you want the missing-ticker watchlist for every stack.

#space #thermal

1

116

Stack Maps retweeted

If you think SpaceX is a rocket company with an internet business, you're basically valuing Amazon on book sales in 2005.

146

322

3,994

441,309

Jun 2

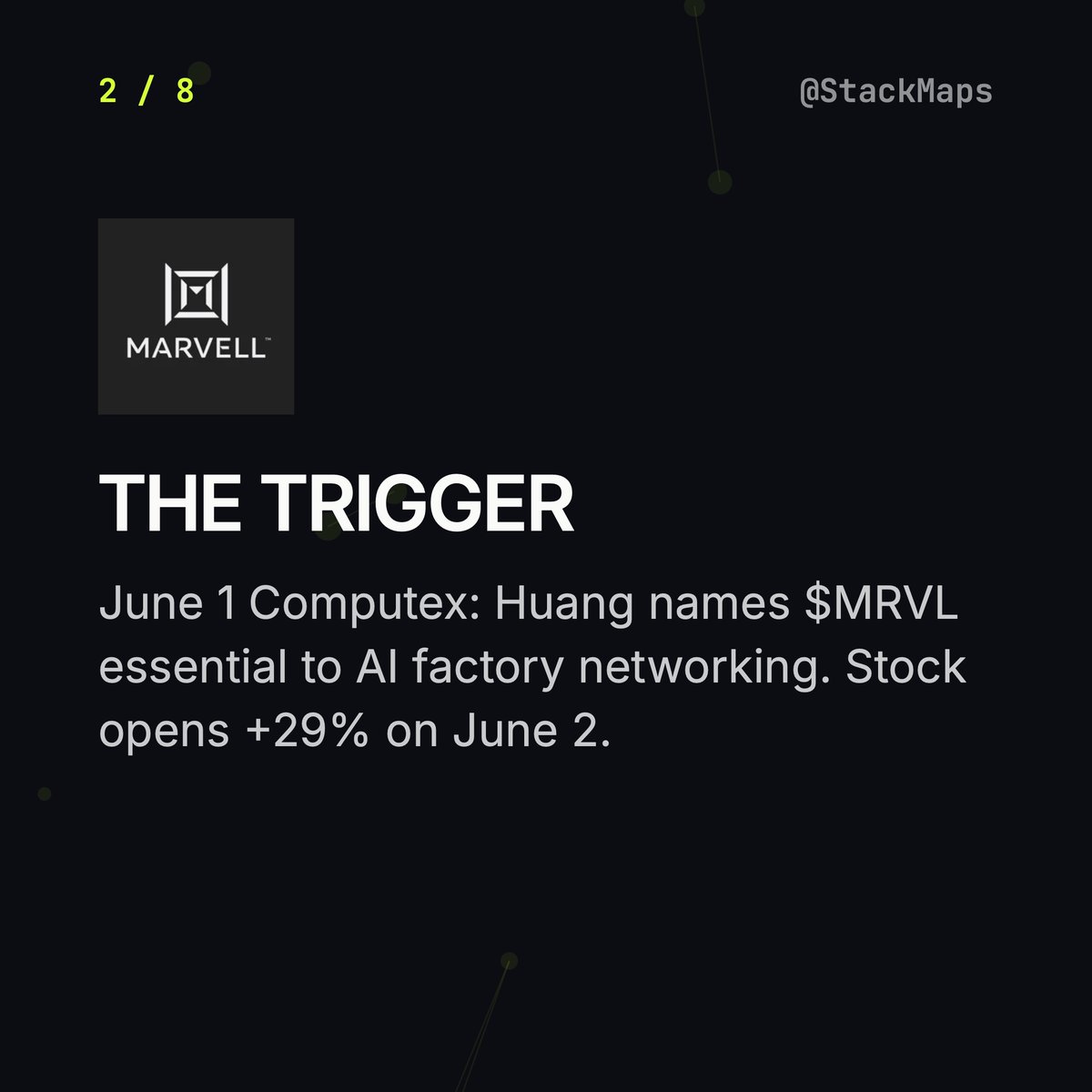

$MRVL 32.5% in one day. Here is the layer-by-layer map of who else gets re-priced when Jensen ($NVDA) calls one chip company "the next trillion-dollar company."

1

11

77,030

Jun 2

L5 Cardiometabolic adjacents. AstraZeneca's oral elecoglipron (ECC5004) entered Phase 3 in early 2026. Roche's CT-388 delivered 22.5% placebo-adjusted weight loss at 48 weeks in Phase 2 and starts Phase 3 this year. Sanofi sits on Lantus/Toujeo legacy.

1

1

93