Nothing here is financial advice! just my own observations and opinions

Joined June 2018

- Tweets 462

- Following 12

- Followers 111

- Likes 171

143 Photos and videos

And Magnachip $MX still managed to end the day red 😂

But i believe in it. it has Insane Potential at just ~$220M Marketcap

JIUST IN: $1,000,000,000,000 added to the US stock market at open

133

Deep Dive: Everspin Technologies $MRAM

Everspin Technologies is one of the most interesting small-cap “real memory technology” stocks, but it is not simply a mini Micron, SanDisk, or Kioxia. Those companies operate in massive DRAM, NAND, SSD, and storage markets. Everspin is different. It focuses on MRAM, short for Magnetoresistive Random Access Memory.

MRAM is a type of memory that combines some advantages of RAM and flash storage. It is fast, non-volatile, durable, and highly reliable. In simple terms: MRAM can keep data even when power is lost, while still offering much faster write endurance than traditional flash memory.

That makes it especially useful in areas where data loss is unacceptable: industrial systems, aerospace, defense, medical devices, automotive, networking, satellites, casino gaming machines, and other mission-critical applications.

---

What does Everspin actually do?

Everspin sells Toggle MRAM and STT-MRAM products. These are not mass-market memory chips like NAND used in SSDs or HBM used in AI servers. Instead, they are more specialized memory products for demanding environments.

That is both a strength and a weakness.

The strength: Everspin does not have to compete directly against giants like Samsung, SK Hynix, Micron, Kioxia, or SanDisk in brutal commodity markets.

The weakness: MRAM is still a niche technology. The market is much smaller than DRAM or NAND, and Everspin still has to prove that MRAM can scale into larger commercial applications.

---

Why the stock is interesting

Everspin is not just a “future story” with no revenue. The company already generates real sales, has strong gross margins, and has a relatively clean balance sheet.

For 2025, Everspin reported around $55.2 million in revenue, including about $48.3 million from MRAM product sales. Gross margin was above 50%, which is attractive for a small semiconductor company. The company was slightly unprofitable on a GAAP basis, but profitable on a non-GAAP basis.

Q1 2026 was also solid, with around $14.9 million in revenue, including $14.1 million from MRAM products. The company also guided for roughly $15.5–16.5 million in Q2 2026 revenue.

So the key point is: Everspin already has a real business. This is not a pure pre-revenue lottery ticket.

---

The bull case

The bull case is that MRAM slowly moves from a niche memory technology into a much larger category.

Everspin’s long-term target is to move from roughly $55 million in annual revenue toward $100 million by FY2029. That is not explosive Nvidia-style growth, but for a small specialty memory company, it would be meaningful.

The biggest near-term trigger is the company’s $40 million agreement with a U.S. prime contractor for military and aerospace MRAM applications. For a company with around $55 million in annual revenue, a $40 million agreement over roughly 2.5 years is very significant.

This is where the story gets interesting: defense, aerospace, industrial automation, satellites, and edge computing all need highly reliable memory. MRAM fits that use case very well.

Everspin also has optionality in areas like FPGA configuration memory, chiplets, edge AI, and in-memory computing. That is the more speculative part of the story. If MRAM becomes more important in these next-generation architectures, Everspin could become much more valuable.

---

Why it is not “the next SanDisk”

This is very important: Everspin is not a direct SanDisk replacement or a mini Micron.

SanDisk/Kioxia are NAND and flash storage giants. They benefit directly from AI data centers, SSD demand, storage growth, and huge volume markets.

Everspin does not sell mass-market NAND. It does not produce HBM for AI GPUs. It is not directly plugged into the Nvidia AI server supply chain in the same way as HBM or SSD suppliers.

So the mistake would be thinking:

“Memory is hot, SanDisk is running, Micron is running, so Everspin must be the next one.”

The better way to think about Everspin is:

1

2

690

A small specialty memory company with real products, real revenue, defense exposure, and long-term upside if MRAM adoption grows.

That is a very different thesis.

---

Main opportunities

1. Small market cap in a hot sector

Everspin is tiny compared to Micron, SanDisk, Kioxia, Samsung, and SK Hynix. If investors start looking for smaller memory names, $MRAM can move fast.

2. Real revenue and strong margins

Unlike many speculative semiconductor names, Everspin already sells real products and has gross margins above 50%.

3. Defense and aerospace upside

The $40 million military/aerospace agreement is a major validation point. If more contracts follow, the market could start valuing Everspin more like a strategic defense semiconductor supplier.

4. MRAM fits critical applications

Industrial, medical, satellite, automotive, and defense systems need reliable non-volatile memory. MRAM is well suited for those markets.

5. Optionality in edge AI and advanced computing

This is the sexy part of the story. MRAM may become useful in certain edge AI, chiplet, FPGA, and in-memory computing applications. If that happens, Everspin’s addressable market could expand meaningfully.

---

Main risks

1. The stock is not cheap anymore

After the run, Everspin trades at a high revenue multiple for a company growing at a moderate pace. The stock already prices in a lot of optimism.

2. Growth is solid, but not explosive

The company is not currently growing like an AI hypergrowth stock. Revenue growth has been decent, but investors need to see acceleration.

3. MRAM may remain a niche

This is the biggest risk. MRAM might stay useful in specialized applications but never become a mass-market memory category.

4. AI hype could be exaggerated

Everspin is not an HBM supplier. It is not the same type of AI infrastructure winner as Micron or SK Hynix. If investors realize that the AI connection is more indirect, the stock could correct sharply.

5. Competing technologies

ReRAM, FRAM, embedded flash, NOR flash, SRAM, and other non-volatile memory solutions can compete with MRAM depending on the use case.

---

My view

Everspin is one of the cleanest small-cap memory technology plays on the market. It has real products, real revenue, high gross margins, a strong niche, and a potentially important defense/aerospace growth angle.

But I would not call it “the next SanDisk.”

SanDisk is a scaled NAND/SSD giant benefiting directly from the AI data center storage cycle. Everspin is a much smaller specialty memory company betting on broader MRAM adoption.

So for me, $MRAM is best described as:

A high-risk, high-upside specialty memory stock with real technology, real revenue, and big optionality if MRAM becomes more important in defense, aerospace, industrial systems, edge AI, and embedded computing.

The opportunity is real, but the stock is no longer undiscovered. At the current valuation, Everspin needs to keep delivering stronger revenue growth, more design wins, and proof that the defense/aerospace deal is not just a one-time boost.

Final take:

$MRAM is not a mini SanDisk. But it could be one of the most interesting small-cap memory technology bets if MRAM adoption expands over the next few years.

130

Imagine you get $100k free today.

Turn it into $1M in 12 months or you lose it all.

Only one stock allowed. No diversification.

What’s your pick?

#Stocks #Investing

$SIVE $AAOI $AXTI

468

327

$SIVE Sivers Semiconductors deep dive:

Current price: around $9.30–$9.60 depending on Stockholm vs OTC quote.

This is one of the wildest semiconductor stories in Europe right now: tiny current revenue, huge AI/optics/SATCOM optionality, and a valuation that already prices in a lot of success.

1) What they do

Sivers is not a classic commodity chip company. They focus on:

• Photonics for AI data centers / optical interconnects

• DFB lasers

• SATCOM / mmWave / beamforming

• 5G/6G, FWA

• Defense & aerospace

• LiDAR

Basically: picks-and-shovels for faster, lower-power connectivity.

2) The bull case

The opportunity is massive if Sivers converts design wins into volume production.

Their reported opportunity pipeline is now around $799M, up 77% YTD. That is the whole story. The stock is not trading on today’s revenue. It is trading on future ramps.

Key drivers:

• Jabil collaboration for 1.6T optical transceiver modules

• Automotive/industrial LiDAR ramp expected from Q4 2026

• SATCOM/FWA momentum

• U.S. defense exposure

• Potential U.S. dual listing

• AI data center demand for optical networking

3) Revenue expectations

FY25 revenue was only around 306M SEK, roughly $33M.

Consensus/estimates I found suggest:

• 2026E revenue: ~340M SEK

• 2027E revenue: ~487M SEK

• 2028E revenue: ~675M SEK

So yes, growth is expected. But even on 2027 numbers, the stock is still trading at a very high sales multiple.

4) The biggest problem: valuation

At around 27B SEK market cap, Sivers is already priced like a future winner.

Rough math:

• FY25 P/S: ~90x

• 2026E P/S: ~80x

• 2027E P/S: ~56x

That is not “cheap semiconductor stock” territory. That is “the market expects major execution and real product ramps” territory.

5) Recent financials were weak

Q1 2026 revenue fell 22% YoY to 61.9M SEK.

Adjusted EBITDA was negative.

Operating cash flow was negative.

The company is still loss-making.

Management says some defense-related revenue shifted from Q1/Q2 into H2 2026 due to U.S. budget delays. That may be true, but the market now needs to see that revenue actually show up.

6) Main risks

• Valuation is extremely high

• Revenue is still tiny vs market cap

• Execution risk on 2026/2027 ramps

• Customer concentration risk

• Pipeline does not equal revenue

• Negative cash flow

• Potential future dilution

• Accounting restatements / PCAOB adjustment noise

• FX headwinds

• Momentum/short-squeeze behavior can reverse violently

7) What would make me more bullish

I want to see:

• Q2/Q3 revenue acceleration

• Real production orders, not only pipeline

• Gross margin improvement

• Product revenue mix increasing

• Cash burn improving

• Clear confirmation of LiDAR ramp

• More details around Jabil/data center revenue potential

• U.S. listing progress without further accounting surprises

8) My view

Sivers is a high-upside, high-risk semiconductor story.

The tech exposure is very attractive: AI data centers, optical interconnects, SATCOM, defense, LiDAR.

But the stock has already moved like the future is guaranteed. At this valuation, Sivers has to execute almost perfectly.

For me, this is not a “cheap value” stock. It is a speculative execution story.

If the 2026/2027 ramps hit, the upside can still be big.

If they don’t, the downside can be brutal.

High risk. High potential. Definitely one to watch.

Not financial advice.

2

654

Jun 14

$20,000 invested in SanDisk $SNDK Exactly 1 Year ago is worth $895,770.19 today

Return: 4,378.85%

Profit: $875,770.19

WOW

102

Jun 13

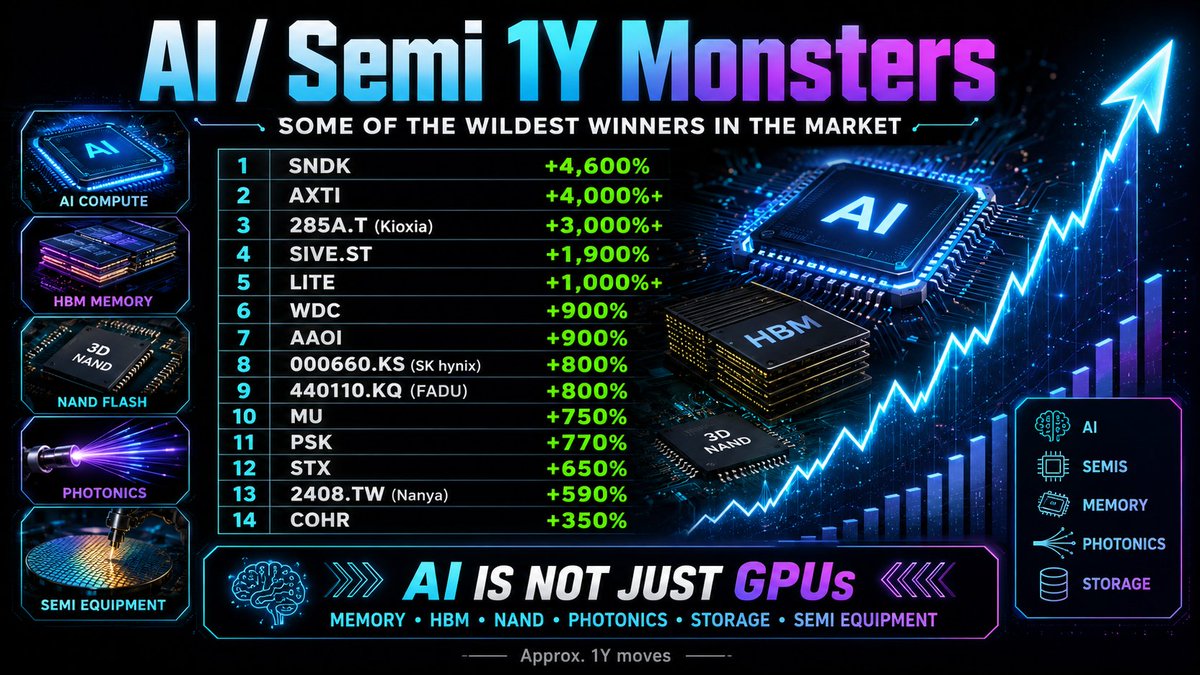

Some of the wildest 1Y moves in AI / semiconductors / memory / photonics are insane:

$SNDK 4,600%

$AXTI 4,000%

285A.T Kioxia: 3,000%

$SIVE 1,900%

$LITE 1,000%

$WDC 900%

$AAOI 900%

000660.KS SK hynix: 800%

440110.KQ FADU: 800%

$MU 750%

$STX 650%

319660.KQ PSK: 770%

Nanya Technology: 590%

$COHR 350%

AI is not just GPUs.

Memory, NAND, HBM, SSD controllers, optical networking, photonics and semiconductor equipment have produced some of the biggest winners in the entire market.

Not financial advice.

3

425

Jun 13

$MX (Magnachip Semiconductor) is currently trading at a P/S ratio of around 1.2–1.3x.

$SIVE (Sivers) is trading above 70–80x.

Massive valuation gap between two semiconductor stocks. $MX looks cheap on fundamentals, while $SIVE is heavily priced in on AI photonics hype. Interesting contrast, do what you will with this Information.

3

1

1

835

Jun 13

$META is a $1000 stock trading at $567

$INTC is a $200 stock trading at $125

$MX is a $25 stock trading at $6 (My FAV)

$WDC is a $800 stock trading at $565

$MU is a $1500 stock trading at $980

$AMD is a $700 stock trading at $500

$STX is a $1200 stock trading at $850

$QCOM is a $250 stock trading at $170

1

2

501

Jun 13

$SNDK is currently trading around $2,000 after another strong session.

Exactly one year ago it was sitting below $50 right after the spin-off. Insane move.

🔥Where do you see $SNDK by December 31, 2026?

$2,500? $3,000? $4,000 ? Drop your predictions below 📷

$MU $SNDK $WDC $STX $PSTG $NTAP $RMBS $LRCX $AVGO $TSM

1

270