Joined April 2025

- Tweets 2,430

- Following 126

- Followers 2,374

- Likes 8,978

1,184 Photos and videos

Pinned Tweet

2 May 2025

Stronghold (SHx) is pure digital gold.

Built by ex-Ripple & Stellar leads. Ripple invested. Integrated with IBM, ACH, ISO 20022 & FedNow

Not hype. Real rails, already running.

Hidden gem. Not for long

bit.ly/4jTkSVY

#SHx #Fintech #Ripple #Stellar #DePIN #ISO20022 #XRP

12

35

158

47,435

Jun 13

🍿 Well well well...

17 Sep 2025

👀 Why Stronghold Could Become a Super App

Full post: strongshx.notion.site/Why-St…

As we saw in @strongholdpay latest video, it highlighted how institutions pay far less tax on crypto thanks to legal structures that individuals cannot access.

In this post I dive deeper, unpacking the current financial system and the laws that shape it, before exploring why this matters and how Stronghold may be building something bigger, a super app.

⚠️Please read it all the way through. Make sure you read through the context before jumping to the part where I explore the super app idea.

And when you reach the end, if you’ve actually enjoyed it, don’t forget to give this a like and share. It helps the community understand Stronghold’s potential scale and shows your support for the work I’ve put into bringing this together 🤝

🧠 Know what you hold.

$SHx $XLM $XRP #DigitalAssets #RWA #Blockchain #CryptoMarket

1

3

16

632

Jun 11

I can no longer stay silent about this.

For far too long, many Europeans trusted that others would protect what they had inherited. They believed governments had things under control, that borders would be respected, that laws would be upheld, and that the culture passed down by their parents and grandparents would remain alive for their children.

But there are moments in history when a people must stop, look around and ask: what country are we leaving behind?

We may disagree on politics, parties and ideas. But something deeper unites us. The culture we share, the history we inherited, and the country we wish to protect. Within that foundation, we can still understand one another, because we speak from the same roots. The real problem begins when that foundation is lost, fragmented or replaced. Because without a shared culture, there can be no united people moving towards the same future.

Today, across Europe, there is a growing sense that everything has changed, and not for the better. Far from it. Reports of violent crime, attacks in broad daylight, sexual assaults, child exploitation networks and incidents that leave entire communities in shock are becoming increasingly common. Many people no longer live with the same peace of mind. They avoid certain areas, change their daily habits and wonder whether their children will enjoy the safety previous generations once took for granted.

Many citizens feel they are no longer a priority in their own countries.

This is a question of balance, responsibility and respect. How many people can a country welcome without compromising the quality of life of its own citizens? How can we ensure that those who arrive respect the values, laws, culture and customs of the country that receives them?

One great concern is that many European countries are changing at a speed that no longer allows for genuine integration. In many cities, the transformation is not merely demographic. It has become cultural, social and even civilisational. Customs, traditions, ways of living together, family values, freedom of expression, respect for the law and equality between men and women. Pillars that shaped Europe for generations are being challenged in places where integration has failed, or never truly happened.

The problem begins when communities live apart from the local culture, keep their own rules, and profoundly change the atmosphere of cities, schools and neighbourhoods. Imposing their own culture.

A people does not disappear only through war. It can also disappear slowly, when it stops renewing itself, when it has fewer children while receiving populations in such numbers, and with birth rates far higher than those of the local population.

If nothing changes, in just two generations Europeans may wake up in a Europe they no longer recognise as their own. A Europe where native culture, customs, values and collective memory are no longer society’s common foundation, but merely a memory of what once existed.

A transformation accelerated by the permissive policies of the European Union and by national leaders who opened the doors without ensuring integration, balance or cultural continuity.

The time has come to wake up.

Not as enemies of anyone, but as guardians of what we have received. As citizens who understand that a nation is not merely territory. It is memory, culture, laws, customs, sacrifice and continuity.

Defending our country is not about hating anyone. It is about demanding respect for our laws, our values and our way of life. It is about remembering that integration must be real, that borders matter, and that the identity of a people cannot be sacrificed by decisions made far away from its citizens.

Enough is enough!

Now is the time to speak and to act. Because if we do not defend our country, no one will do it for us. Defend today what you want to see preserved tomorrow, for your children, for future generations, and for all those who will inherit the country we leave behind.

6

17

49

11,642

Jun 8

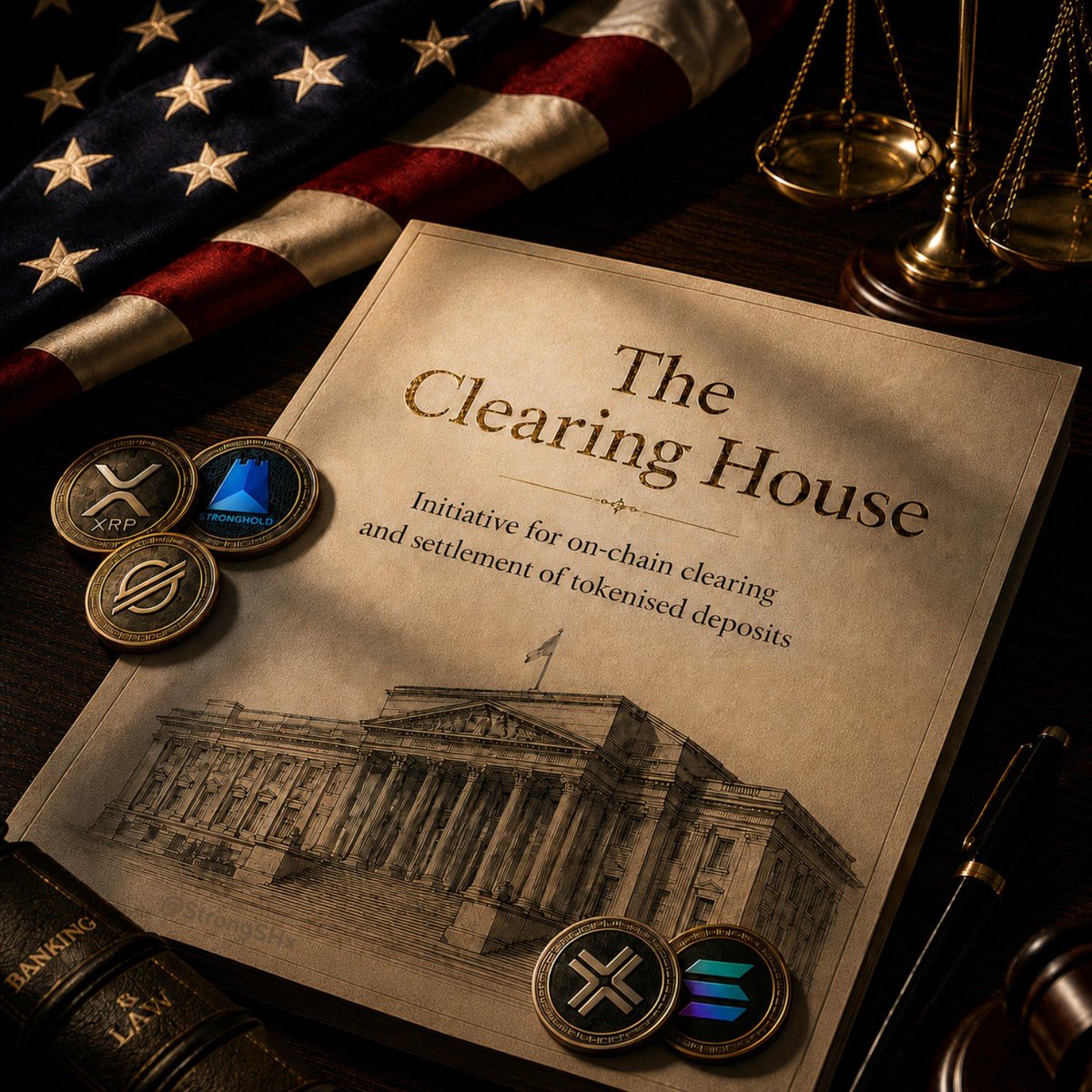

🇺🇸 TCH wants to connect US banks to tokenised deposits on-chain

Last Friday, The Clearing House announced an initiative to enable on-chain clearing and settlement of tokenised deposits between banks.

The solution aims to combine regulated banking infrastructure with blockchain native capabilities. Programmability, interoperability, richer transaction data, and 24/7 settlement.

The initiative will have two main components:

🔹 On-chain clearing and settlement of tokenised deposits between banks, within the existing banking framework.

🔹 A connectivity layer between blockchain activity and traditional fiat rails, including RTP and CHIPS.

According to TCH, the use cases include programmable treasury, real-time liquidity management, cross-border payments, agentic commerce, digital asset settlement, and automated financial workflows.

The list of institutions, for many of us, is no longer a surprise.

Names such as Bank of America, BMO, BNY, Citi, Citizens, Fifth Third, HSBC, Huntington, JPMorgan, KeyBank, PNC, Regions, Santander/Getnet, TD Bank, Truist, U.S. Bank, and Wells Fargo all appear in the announcement.

As we have seen, these banks have been looking to gain more and more exposure to the crypto world. Banks increasingly want to capture the stablecoin narrative without handing control over to crypto-native issuers.

The market is moving into a phase where regulated payments tokenisation interoperability 24/7 settlement are becoming real banking priorities.

✨ And this is where projects such as Stronghold, Stellar, Ripple, Axelar, and Solana enter the conversation.

Not because this news directly validates any specific token, but because it validates the sector where these projects are trying to capture value.

A more digital, programmable, and interoperable financial infrastructure, where payments, settlement, liquidity, cross-border flows, and tokenised assets become connected to traditional rails and blockchain networks.

Although this is good news for the tokenisation thesis, it also increases competition.

If the major banks manage to build a closed network via TCH, part of the institutional volume could remain inside that banking ecosystem, without any direct need for public tokens.

This is where the difference between narrative and real utility starts to matter.

It is not enough to be exposed to payments, tokenisation, or settlement themes. Utility will have to appear in the areas where banks cannot, do not want to, or have no incentive to operate alone:

🪄 external interoperability, merchant networks, fintech rails, cross-border payments, global liquidity, compliance tooling, multi-network integration, and access to markets outside the closed banking system.

Ultimately, the more banks move towards tokenised rails, the clearer the question becomes:

Which projects will complement this infrastructure, and which ones will be replaced by it?

3

8

472

Jun 5

🌈 They might need to add another band to the rainbow.

Funny how every dip gets a headline, yet Bitcoin keeps following the same structure I mapped out months ago.

Feb 10

🌪 Can you survive this? 🌪

In late January 2025, my focus was on the macro structure. After a strong impulsive move higher, Bitcoin was starting to show signs of exhaustion, and the ~65k area stood out as a logical target for a correction and liquidity grab. At the time, that view felt premature to many.

What followed was only a partial version of that process. Price did correct, but only down to the ~74k area. From there, it pushed higher again and printed a new ATH (grey box). That top was meaningful, but also limited. Roughly 14% above the January ATH, without strong structural expansion or sustained acceptance above those levels.

It was precisely at that top that I highlighted a point of inflection. The market was forced to choose a path:

🔹 Either it validated real strength with continuation into a new ATH, almost in a parabolic move, a scenario I illustrated on the chart with the red candle projection.

🔹 Or it failed that validation and began a deeper corrective process towards the ~65k area, illustrated by the blue candle projection.

What followed was the full activation of the sell model. Distribution at the top gave way to a break in market structure, with key levels lost and clear imbalance and order blocks left unmitigated.

The subsequent price action, impulsive moves lower followed by consolidation, reflects a market in liquidity reorganisation, position rotation, and volume building.

⚠️ From my perspective, a correction to ~65k is no longer sufficient to complete this cycle. For the structure to resolve cleanly, price needs to work through deeper liquidity zones, located between ~48k and ~37k, where historical volume and significant fair value gaps (FVGs) converge.

---

Even if Trump already has a Powell replacement willing to turn the money printers back on and push prices to a new ATH, the market could still be engineered to trade down into this zone first.

Like I said before, price couldn’t care less about the news.

---

$SHx $XLM $XRP #Bitcoin #Economy #CryptoMarket #StockMarket

1

2

8

620

Jun 5

🇺🇸 The CLARITY Act may become one of the biggest turning points in US digital asset regulation.

The market is already moving like it knows what comes next.

🔹 JPMorgan, Citi and major US banks are preparing tokenized deposits.

🔹 Stripe, Visa and Mastercard are backing stablecoin infrastructure.

🔹 IBM has decades of deep banking infrastructure behind it. Now, with Digital Asset Haven, that same institutional layer is moving into custody, compliance and multichain digital assets.

And the OCC already opened the operational door. US banks can hold crypto assets to pay network fees, test DLT platforms and operate directly on blockchain networks when tied to permitted banking activities.

Stablecoins already got their federal framework with the GENIUS Act.

Now CLARITY could define the wider digital asset market, separate SEC/CFTC roles and give institutions the rules they need.

Looks like the biggest players already know CLARITY is getting close.

2

5

18

526

Jun 4

🎬 Now let’s give them some hope.

Send it back to ~70k as we head into the weekend.

#Bitcoin #Crypto #CryptoMarket #Stocks

$XLM $XRP $SHx

Jun 2

👀 It almost looks like magic, doesn’t it?

"We’ll see what unfolds over the next 5 weeks."

As promised, five weeks later, we're revisiting this discussion.

✅ Liquidity taken above ~78k

✅ Market back below ~70k

⌛ Acceptance beneath ~70k

⌛ Reject ~60k / 2025 Low

⌛ Sell-off into the 48k–37k liquidity zone

Interestingly, the structure kept to schedule. And, almost as if by magic, the headlines appeared right on cue to support the scenario I had outlined.

In my previous post, I highlighted that the ~78k area had yet to be properly tested, and that a rejection followed by acceptance below ~70k could confirm continuation of the corrective leg.

The market went a step further.

Rather than reacting at ~78k (0.5 Fibonacci), price extended towards ~82,850 (0.618 Fibonacci), where it formed the range high on 6 May.

By 13 May, just over four weeks after the original analysis, the structure began showing clear signs of change. Price started rejecting the lower boundary of the previous range and lost acceptance at the levels that had been supporting the bullish continuation thesis. As a result, the upside expansion failed to generate sufficient displacement, and the macro outlook shifted in favour of seeking liquidity at lower levels.

The most interesting part?

Since yesterday, the headlines have started to arrive.

🧸 Strategy sells 32 BTC.

🧸 Iran suspends talks with the US and threatens to block the Strait of Hormuz. Again...

🧸 Oil surges.

🧸 USDT loses more than $1B in market capitalisation.

🧸 Mt. Gox moves 10,422 BTC (~$739M).

🧸 US mega-caps erase roughly $370B in market value on the last 48h.

Coincidence? It almost seems as though the elites know how to trade and world leaders all get together to manufacture panic...

The narrative is presented as though these events are causing the sell-off. Yet, as I've been showing over recent months, the structure was already pointing in that direction way before these headlines emerged. In fact, as far back as 3 June 2025, I highlighted the possibility of this trajectory.

Soo...

For this range to retain its bullish scenario, the ~65k area MUST hold and price needs to reclaim ~70k quickly. A sustained recovery above that level would keep the possibility of structural rebuilding and bullish continuation on the table.

As you can probably guess... I'm not particularly convinced by the bullish case.

If the market begins repeatedly rejecting the ~70k region and turns it into resistance, the probability of continuation towards the liquidity zones I've been highlighting for months increases significantly.

The structure is approaching a decision point.

---

Once price reaches the 48k–37k liquidity zone, we’ll see whether the conditions for a genuine trend reversal are actually in place.

That area is probably where buying alts starts to make sense again.

Assuming, of course, another “totally unexpected” FTX style collapse doesn’t arrive right on cue.

---

📚 Here’s a small task for you:

Open a few charts on the 3/4H timeframe and mark the weekly high and low.

Check how often one of them forms on a Tuesday or Thursday.

Crypto, stocks, indices, FX. It doesn’t matter.

Don’t treat it as a rule. Treat it as a weekly pattern worth studying.

Time is the key.

#Bitcoin #Crypto #CryptoMarket #Stocks $XLM $XRP $SHx

2

8

903

Jun 4

⚠️ A friendly reminder.

Just because price has fallen doesn't mean it's cheap.

Markets have a habit of making people feel clever right before making them feel poor.

There will be a time to buy.

The challenge is surviving long enough to recognise it.

#Bitcoin #Crypto #CryptoMarket #Stocks

$XLM $XRP $SHx bitcoin:native

Feb 5

⚠️ Be careful folks. Do not try to catch falling knives.

As I mentioned last Friday, a move towards 76k was very likely over the weekend, and if that level failed to hold, the next major support would be 65k, which is roughly where we are now.

During this drop, there is still the possibility of a short squeeze towards 80k.

If 65k does not hold, the next key level would be around ~48k, potentially testing the previous low/order block located near 49k. I know, WILD.

Stay safe.

$SHx $XLM $XRP #Crypto #Bitcoin #DigitalAssets #Economy

2

2

6

328

Jun 3

20 Oct 2025

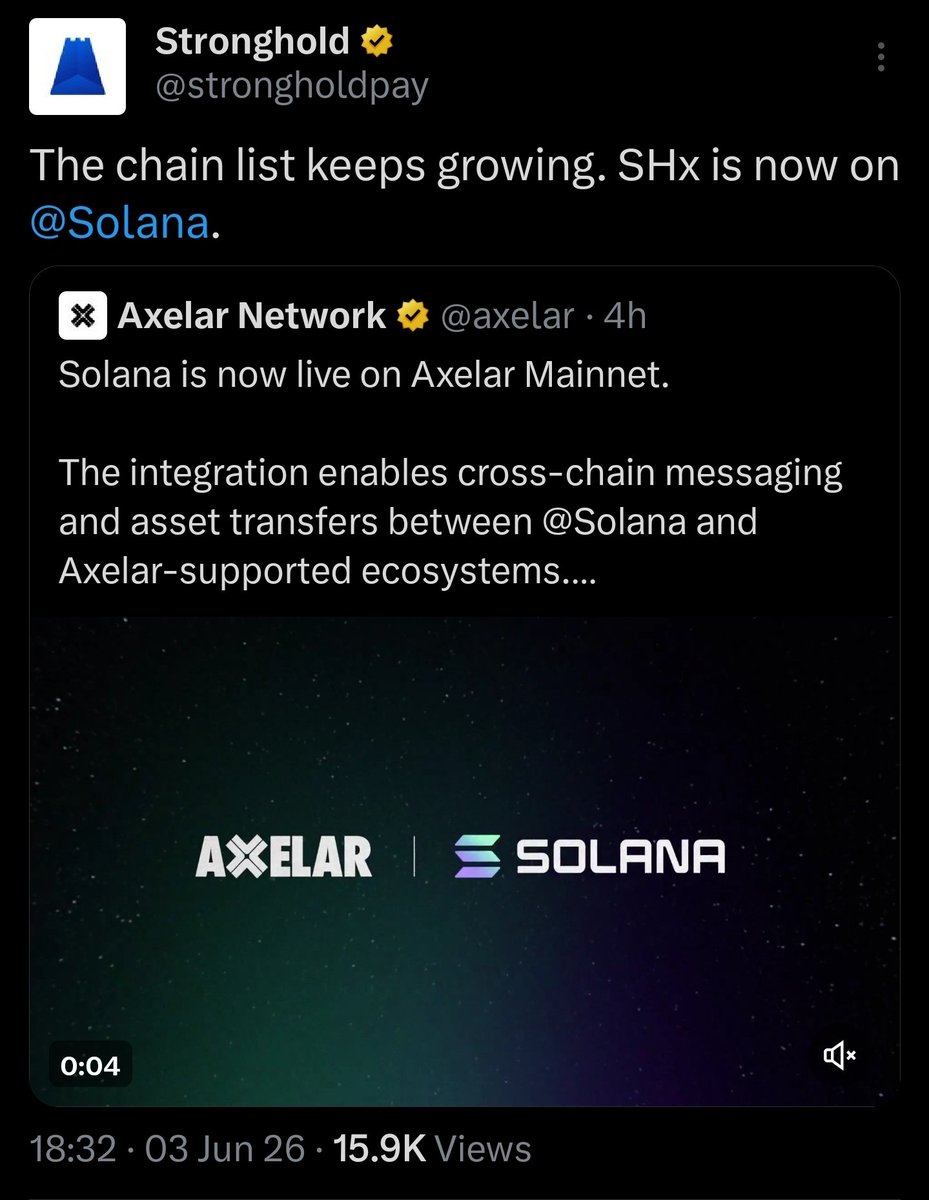

Solana Axelar Stronghold? 🌉✨

It seems that Sean Bennett has his radar locked onto Solana, and it’s not hard to see why. With Axelar already serving as a bridge for the Stronghold ecosystem, a future integration with Solana could open doors that today hardly seem possible.

Stronghold has built its reputation on a fast, regulated, and interoperable payments infrastructure, based on Stellar and Axelar. Solana, in turn, offers deep market liquidity and a vibrant DeFi and gaming ecosystem. It also boasts one of the largest user bases in Asia, with strong presence in Japan, South Korea, and Southeast Asia. Regions where Stronghold has already begun expanding.

Solana would significantly extend Stronghold’s DeFi reach, with thousands of Web3 applications, multi-billion liquidity markets, and institutional partnerships with Visa, Shopify, and Circle. It’s a network where capital moves not only through payments but also through trading, NFTs, gaming, and yield, creating opportunities that Stronghold could translate into tangible payment solutions.

In the Asian market, this complementarity becomes even more relevant. Solana has over 100 million active users in the region, while Stronghold is establishing roots in Japan through its partnership with JPYC. Since Axelar already connects Avalanche, where JPYC operates, to Solana, Stronghold could use its existing Axelar bridge to enable JPYC payments directly in Solana based apps and games. Effectively opening a corridor between local stablecoins and the global ecosystem.

🪄 And it’s in gaming that the potential truly explodes ✨️

Solana is a leader in this sector, processing millions in assets and micro-transactions daily. Stronghold could provide regulated payments, fiat settlement, and compliance solutions for Web3 gaming companies, acting as an institutional layer on top of Solana’s native liquidity.

Imagine in-game purchases paid with regional stablecoins like JPYC, settled in seconds and audited through Stronghold.

🇯🇵 As we all know, Japan, is one of the largest video game markets in the world. 🕹

---

Soo... basically, Solana would give Stronghold access to liquidity and global scale, while Stronghold would give Solana the regulatory framework and institutional trust it still lacks. Together, connected through Axelar, they could unite speed, liquidity, and regulation in a single ecosystem, paving the way for the future of digital payments at the heart of Asia.

...🐇

$SHx $XLM $XRP #DigitalAssets #RWA #CryptoMarket #Crypto

4

12

1,125

Jun 2

👀 It almost looks like magic, doesn’t it?

"We’ll see what unfolds over the next 5 weeks."

As promised, five weeks later, we're revisiting this discussion.

✅ Liquidity taken above ~78k

✅ Market back below ~70k

⌛ Acceptance beneath ~70k

⌛ Reject ~60k / 2025 Low

⌛ Sell-off into the 48k–37k liquidity zone

Interestingly, the structure kept to schedule. And, almost as if by magic, the headlines appeared right on cue to support the scenario I had outlined.

In my previous post, I highlighted that the ~78k area had yet to be properly tested, and that a rejection followed by acceptance below ~70k could confirm continuation of the corrective leg.

The market went a step further.

Rather than reacting at ~78k (0.5 Fibonacci), price extended towards ~82,850 (0.618 Fibonacci), where it formed the range high on 6 May.

By 13 May, just over four weeks after the original analysis, the structure began showing clear signs of change. Price started rejecting the lower boundary of the previous range and lost acceptance at the levels that had been supporting the bullish continuation thesis. As a result, the upside expansion failed to generate sufficient displacement, and the macro outlook shifted in favour of seeking liquidity at lower levels.

The most interesting part?

Since yesterday, the headlines have started to arrive.

🧸 Strategy sells 32 BTC.

🧸 Iran suspends talks with the US and threatens to block the Strait of Hormuz. Again...

🧸 Oil surges.

🧸 USDT loses more than $1B in market capitalisation.

🧸 Mt. Gox moves 10,422 BTC (~$739M).

🧸 US mega-caps erase roughly $370B in market value on the last 48h.

Coincidence? It almost seems as though the elites know how to trade and world leaders all get together to manufacture panic...

The narrative is presented as though these events are causing the sell-off. Yet, as I've been showing over recent months, the structure was already pointing in that direction way before these headlines emerged. In fact, as far back as 3 June 2025, I highlighted the possibility of this trajectory.

Soo...

For this range to retain its bullish scenario, the ~65k area MUST hold and price needs to reclaim ~70k quickly. A sustained recovery above that level would keep the possibility of structural rebuilding and bullish continuation on the table.

As you can probably guess... I'm not particularly convinced by the bullish case.

If the market begins repeatedly rejecting the ~70k region and turns it into resistance, the probability of continuation towards the liquidity zones I've been highlighting for months increases significantly.

The structure is approaching a decision point.

---

Once price reaches the 48k–37k liquidity zone, we’ll see whether the conditions for a genuine trend reversal are actually in place.

That area is probably where buying alts starts to make sense again.

Assuming, of course, another “totally unexpected” FTX style collapse doesn’t arrive right on cue.

---

📚 Here’s a small task for you:

Open a few charts on the 3/4H timeframe and mark the weekly high and low.

Check how often one of them forms on a Tuesday or Thursday.

Crypto, stocks, indices, FX. It doesn’t matter.

Don’t treat it as a rule. Treat it as a weekly pattern worth studying.

Time is the key.

#Bitcoin #Crypto #CryptoMarket #Stocks $XLM $XRP $SHx

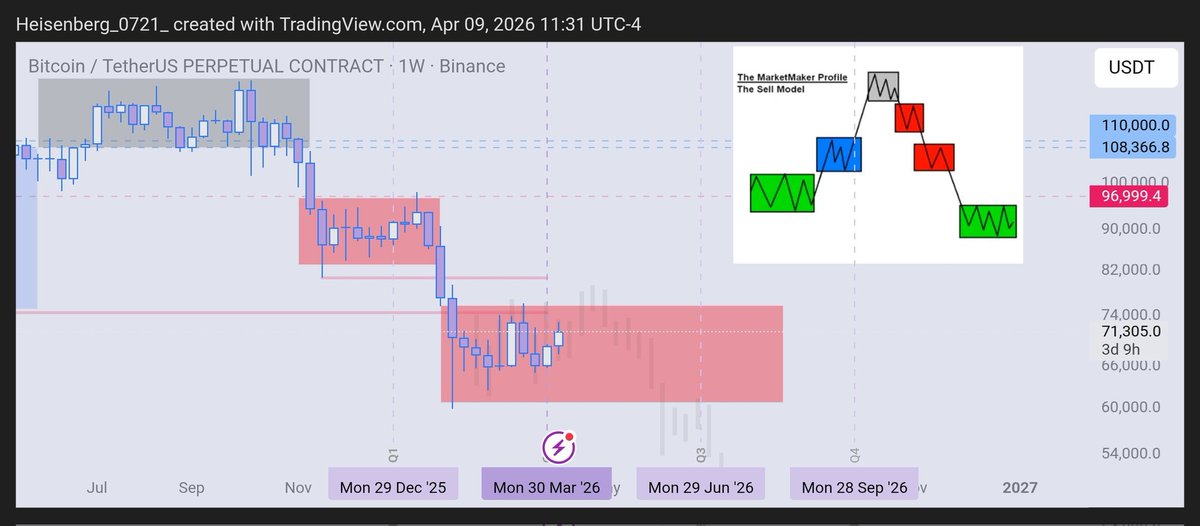

Apr 9

⚠️ The process is still unfolding

Back in February, I outlined a macro structure where Bitcoin had entered a distribution phase after a limited expansion beyond the January ATH. What followed was a break in structure and the beginning of a deeper corrective process.

Today, price is trading around ~71k. And more importantly, it remains trapped inside the same range.

This is not random.

If you look at the chart, you’ll notice vertical lines marking specific time references. One of them aligns with the start of Q2, April 1st. Price has respected this structure with precision, reinforcing the idea that this is a time based process, not a reaction to headlines.

The range is building. And with it, pressure.

So far, there hasn’t been a proper retest of the ~78k zone. That level remains key.

🔹 A move into that area, followed by rejection and acceptance back below ~70k, would likely confirm continuation of the corrective leg. Where it may ultimately set the stage for a deeper leg down.

🔹 Until then, this remains a controlled environment. Liquidity being engineered, positions rotating, structure forming.

Nothing here is impulsive.

We’ll see what unfolds over the next 5 weeks.

---

As always, news doesn’t move price.

May 15th, Powell’s expected exit, will be closely watched. The real question isn’t the event itself, but whether the market has already priced it in.

Based on the structure I shared, you can probably guess my view...

---

#Bitcoin #Crypto #MarketStructure $BTC $XRP $XLM $SHx

3

8

3,989

May 27

🍿 Today, DTCC announced plans to bring tokenized assets onto the Stellar network.

Funny... because the roadmap continues to follow exactly the path we expected: 2025 and 2026 for testing, connectivity, migrations, and certification. 2027 for production.

This was never a sprint.

Every new announcement isn't the end of the story. It's another confirmation that everything is moving forward exactly as planned.

🌊 Liquidity follows infrastructure.

$SHx $XLM $XRP #ISO20022 #RWA #Tokenization #DigitalAssets

6 Oct 2025

🧠 You think It’s late? The Smart Money hasn’t even entered yet

The bulk of institutional capital, the money that truly moves the world, has yet to enter the crypto market.

As we know, ISO20022 is the new global standard for financial messaging, defined by SWIFT and adopted by central banks, payment systems, and clearing institutions.

This standard will come into full global implementation on 22 November 2025, defining how financial data is structured and exchanged to enable seamless interoperability across institutions and platforms.

And from 1 January 2026, anyone still using MT messages will face extra fees for translation and contingency services until migration is complete.

Who’s going to want to pay more?

No one. 🤷🏻♂️

The DTCC, which clears and settles the vast majority of securities transactions in the United States, is currently adapting its systems (DTC, NSCC, FICC) to communicate using this framework.

But there’s a reason its timeline is longer.

The DTCC sits at the very end of the settlement chain, where data from exchanges, banks, and custodians converges. Before it can upgrade its own infrastructure, it must ensure that all upstream entities — exchanges, brokers, and correspondent banks — are fully stabilised in the new format.

📍 The full testing and certification phase is taking place between 2025 and 2026, with ongoing adoption expected in 2026/27.

Once this migration is finalised, settlement messages will be able to integrate with digital asset networks and ISO20022 compliant systems worldwide, creating a unified infrastructure between traditional and tokenised money.

---

We’re in the phase where the infrastructure is still being built. Just before the avalanche of liquidity 🌊

When the migration is complete, blockchain will cease to be a parallel universe. It will become the central nervous system of the new global financial market.

$SHx $XLM $XRP #RWA #DigitalAssets #ISO20022 #Economy

1

6

43

1,253

Apr 20

✅️ SHx is now bridged to XRPL, just like I told you it would happen.

Getting closer and closer... 🐇

$SHx $XRP $XLM #Crypto #ISO20022 #RWA #DigitalAssets

29 Nov 2025

🧩How Close Are We?

In August, I spoke about the possibility of Ripple, Stellar, IBM and Stronghold beginning to converge.

Was I really that far from the truth? Regulatory shifts, unexpected returns and alliances once thought unlikely are now starting to surface.

The picture is coming together… piece by piece.

If you want to understand what may genuinely be unfolding, it’s all explained in the video 🫡

youtu.be/AhZeynnUI7I?si=ZvEF…

$SHx $XLM $XRP #Crypto #ISO20022 #DigitalAssets #RWA

2

3

27

1,369

StrongSHx retweeted

Apr 9

⚠️ The process is still unfolding

Back in February, I outlined a macro structure where Bitcoin had entered a distribution phase after a limited expansion beyond the January ATH. What followed was a break in structure and the beginning of a deeper corrective process.

Today, price is trading around ~71k. And more importantly, it remains trapped inside the same range.

This is not random.

If you look at the chart, you’ll notice vertical lines marking specific time references. One of them aligns with the start of Q2, April 1st. Price has respected this structure with precision, reinforcing the idea that this is a time based process, not a reaction to headlines.

The range is building. And with it, pressure.

So far, there hasn’t been a proper retest of the ~78k zone. That level remains key.

🔹 A move into that area, followed by rejection and acceptance back below ~70k, would likely confirm continuation of the corrective leg. Where it may ultimately set the stage for a deeper leg down.

🔹 Until then, this remains a controlled environment. Liquidity being engineered, positions rotating, structure forming.

Nothing here is impulsive.

We’ll see what unfolds over the next 5 weeks.

---

As always, news doesn’t move price.

May 15th, Powell’s expected exit, will be closely watched. The real question isn’t the event itself, but whether the market has already priced it in.

Based on the structure I shared, you can probably guess my view...

---

#Bitcoin #Crypto #MarketStructure $BTC $XRP $XLM $SHx

Feb 10

🌪 Can you survive this? 🌪

In late January 2025, my focus was on the macro structure. After a strong impulsive move higher, Bitcoin was starting to show signs of exhaustion, and the ~65k area stood out as a logical target for a correction and liquidity grab. At the time, that view felt premature to many.

What followed was only a partial version of that process. Price did correct, but only down to the ~74k area. From there, it pushed higher again and printed a new ATH (grey box). That top was meaningful, but also limited. Roughly 14% above the January ATH, without strong structural expansion or sustained acceptance above those levels.

It was precisely at that top that I highlighted a point of inflection. The market was forced to choose a path:

🔹 Either it validated real strength with continuation into a new ATH, almost in a parabolic move, a scenario I illustrated on the chart with the red candle projection.

🔹 Or it failed that validation and began a deeper corrective process towards the ~65k area, illustrated by the blue candle projection.

What followed was the full activation of the sell model. Distribution at the top gave way to a break in market structure, with key levels lost and clear imbalance and order blocks left unmitigated.

The subsequent price action, impulsive moves lower followed by consolidation, reflects a market in liquidity reorganisation, position rotation, and volume building.

⚠️ From my perspective, a correction to ~65k is no longer sufficient to complete this cycle. For the structure to resolve cleanly, price needs to work through deeper liquidity zones, located between ~48k and ~37k, where historical volume and significant fair value gaps (FVGs) converge.

---

Even if Trump already has a Powell replacement willing to turn the money printers back on and push prices to a new ATH, the market could still be engineered to trade down into this zone first.

Like I said before, price couldn’t care less about the news.

---

$SHx $XLM $XRP #Bitcoin #Economy #CryptoMarket #StockMarket

5

15

4,720

StrongSHx retweeted

Feb 10

🌪 Can you survive this? 🌪

In late January 2025, my focus was on the macro structure. After a strong impulsive move higher, Bitcoin was starting to show signs of exhaustion, and the ~65k area stood out as a logical target for a correction and liquidity grab. At the time, that view felt premature to many.

What followed was only a partial version of that process. Price did correct, but only down to the ~74k area. From there, it pushed higher again and printed a new ATH (grey box). That top was meaningful, but also limited. Roughly 14% above the January ATH, without strong structural expansion or sustained acceptance above those levels.

It was precisely at that top that I highlighted a point of inflection. The market was forced to choose a path:

🔹 Either it validated real strength with continuation into a new ATH, almost in a parabolic move, a scenario I illustrated on the chart with the red candle projection.

🔹 Or it failed that validation and began a deeper corrective process towards the ~65k area, illustrated by the blue candle projection.

What followed was the full activation of the sell model. Distribution at the top gave way to a break in market structure, with key levels lost and clear imbalance and order blocks left unmitigated.

The subsequent price action, impulsive moves lower followed by consolidation, reflects a market in liquidity reorganisation, position rotation, and volume building.

⚠️ From my perspective, a correction to ~65k is no longer sufficient to complete this cycle. For the structure to resolve cleanly, price needs to work through deeper liquidity zones, located between ~48k and ~37k, where historical volume and significant fair value gaps (FVGs) converge.

---

Even if Trump already has a Powell replacement willing to turn the money printers back on and push prices to a new ATH, the market could still be engineered to trade down into this zone first.

Like I said before, price couldn’t care less about the news.

---

$SHx $XLM $XRP #Bitcoin #Economy #CryptoMarket #StockMarket

3 Jun 2025

Back in March, I made this post on TradingView. It reminded me of a move we saw when price was around 28k. Now, I think we’re at another decision point. For this pump to continue, I want to see a monthly candle close above 109k

Time to choose. Red or blue.

#BTC #Bitcoin #Crypto

2

4

25

7,735

Feb 5

⚠️ Be careful folks. Do not try to catch falling knives.

As I mentioned last Friday, a move towards 76k was very likely over the weekend, and if that level failed to hold, the next major support would be 65k, which is roughly where we are now.

During this drop, there is still the possibility of a short squeeze towards 80k.

If 65k does not hold, the next key level would be around ~48k, potentially testing the previous low/order block located near 49k. I know, WILD.

Stay safe.

$SHx $XLM $XRP #Crypto #Bitcoin #DigitalAssets #Economy

Jan 30

🚨 Bitcoin faces a critical technical moment today

One of the most significant Bitcoin options expiries of the month takes place today, with institutional positions clustered around clearly defined price levels. As these contracts expire, traders and market makers adjust hedges, releasing built up pressure in the market. Historically, such moments act as short-term catalysts, especially when price gravitates towards areas where most options expire worthless. The so called max pain.

This is not a fundamental event, but its technical impact could prove decisive over the next 24 to 72 hours.

These events have gained historical relevance as the market has matured and attracted professional capital. In several previous cycles, similar expiries marked local bottoms or relief moves following periods of sustained pressure.

🩸This weekend is expected to be highly volatile. A move towards 76k is a possibility.

If price drops into this zone, it will need to react quickly and show strength at this level. Otherwise, the next step would likely be a move towards 65k.

$SHx $XLM $XRP #Crypto #CryptoMarket #Economy #RWA

2

17

1,349

Feb 4

Earnings, Are Driving This Market

Around 40% of S&P 500 companies have already reported results. It is not the full picture, but it is enough to identify clear patterns. Roughly 80% have beaten analysts’ expectations, by an average of about 9%. These results are spread across sectors and are not concentrated in a small group of names. In a macro environment often described as fragile, shaped by caution and recurring growth concerns, companies continue to deliver.

This helps frame the outlook for 2026. Earnings growth closer to 15% than to 10% does not remove volatility or prevent corrections. Historically, however, it changes the market backdrop. The more common outcome is a trending market with intermittent noise, rather than a structural breakdown.

🔹 Corrections are part of the process. In periods of solid earnings growth, they tend to act as adjustments, not as signals of a cycle ending.

🔹 Consistent earnings growth reduces the risk of prolonged bear markets and increases the probability of positive returns over the year.

Looking into 2026, market scares are to be expected. The core issue sits with fundamentals. With companies confirming results and estimates being revised favourably, a move of around 15% fits within a reasonable range. Closing the year above 31 December 2025 levels becomes less dependent on liquidity alone.

Liquidity accelerates moves. Earnings sustain cycles.

$SHx $XLM $XRP #Economy #Stocks

2

11

479

Feb 2

🚨 BREAKING | Europe 🇪🇺

Ripple has just taken a historic regulatory step in the EU. It has received preliminary approval for an Electronic Money Institution (EMI) licence in Luxembourg. One of Europe’s most demanding financial hubs.

The authorisation was issued by Luxembourg’s regulator (CSSF) in the form of a preliminary approval. It is not yet the final licence, but it confirms that the process has passed the main assessments around compliance, governance, and risk control.

🔹What this unlocks:

Once the EMI licence is finalised, Ripple will be able to offer regulated payment services across the EU, using the passporting framework. One licence, access to 27 countries.

🔹Regulatory context:

This move fits directly into Europe’s new regulatory framework, MiCA. The EU is drawing a clear line between speculative projects and serious financial infrastructure. Ripple is positioning itself firmly on the institutional side of that divide.

🔹Why this matters:

Traditional financial institutions only work with regulated entities. This approval strengthens Ripple’s position as a payments infrastructure provider aligned with the European financial system.

🔹On the assets (XRP, XRPL, RLUSD):

The licence does not represent a direct approval of the tokens. However, it creates the legal framework required for the expansion of real, regulated, institutional use cases within the EU.

$XRP $SHx $XLM #Ripple #CryptoNews #ISO20022 #DigitalAssets

5

3

18

599

Jan 30

🚨 Bitcoin faces a critical technical moment today

One of the most significant Bitcoin options expiries of the month takes place today, with institutional positions clustered around clearly defined price levels. As these contracts expire, traders and market makers adjust hedges, releasing built up pressure in the market. Historically, such moments act as short-term catalysts, especially when price gravitates towards areas where most options expire worthless. The so called max pain.

This is not a fundamental event, but its technical impact could prove decisive over the next 24 to 72 hours.

These events have gained historical relevance as the market has matured and attracted professional capital. In several previous cycles, similar expiries marked local bottoms or relief moves following periods of sustained pressure.

🩸This weekend is expected to be highly volatile. A move towards 76k is a possibility.

If price drops into this zone, it will need to react quickly and show strength at this level. Otherwise, the next step would likely be a move towards 65k.

$SHx $XLM $XRP #Crypto #CryptoMarket #Economy #RWA

3 Jun 2025

Back in March, I made this post on TradingView. It reminded me of a move we saw when price was around 28k. Now, I think we’re at another decision point. For this pump to continue, I want to see a monthly candle close above 109k

Time to choose. Red or blue.

#BTC #Bitcoin #Crypto

3

15

1,924

Jan 30

Did you miss me?

I hope so. I certainly did 🥲

I’ve been more absent than I’d like because my 9–5 went into full chaos mode. To give you an idea, at one point I was operating at around 8x my normal pace. It was intense. The good news is that things are finally starting to settle, and I’ll be able to be more present again, sharing everything I consider relevant with you.

As for the market, nothing has changed. Absolutely nothing.

Those who have been following closely and doing their homework know we’re still at a very early stage. The infrastructure is being built, tested and certified. None of this happens overnight.

As we know, since January this year, entities continuing to use MT messages will face additional translation and contingency fees. That alone is already a strong catalyst for change. No one wants to increase operating costs unnecessarily.

Just look at the DTCC roadmap, which sits at the very end of the settlement chain. Its timeline is naturally longer because it depends on the stabilisation of the entire upstream ecosystem. Exchanges, banks, brokers and custodians. Everything points to this year being largely focused on testing and certification. A true transition year, laying the groundwork for final implementation closer to the end of 2027.

---

Did you see what happened to gold? Nothing we hadn’t talked about so far.

Just wait until copper explodes as well. The move has already started.

---

Liquidity always comes after the foundation.

And that’s exactly where we still are.

$SHx $XLM $XRP #RWA #ISO20022 #DigitalAssets #Crypto

10

9

58

1,830