76 Photos and videos

Tim retweeted

Jun 12

Jun 12

8/10 are American companies.

This is the greatest nation on the planet and always will be.

All we do is create insane value for everyone who wants to be an optimist about the future.

7

25

460

91,877

Tim retweeted

Jun 13

te koop op 6-jaar piek, bijna pre-covid

2

5

24

12,203

Tim retweeted

Jun 12

Jun 11

JUST IN: United Kingdom announces "PoliceAI" to help fight crime — claims it will free up 6 million human officer hours / year.

47

4,081

33,591

587,177

Tim retweeted

Since this was my final SG-1 episode after we received news of the cancellation, I also made sure to take a few not-so-subtle shots at the network.

Shortly, after SG-1 was cancelled, we stopped receiving network notes. As a gag, I wrote a scene into a script that saw our resident alien, Teal'c, inadvertently attend a reading of the Vagina Monologues. I assumed that, when they saw it, they would ask me to remove it...

#スターゲイト

205

518

4,717

171,285

Tim retweeted

Jun 11

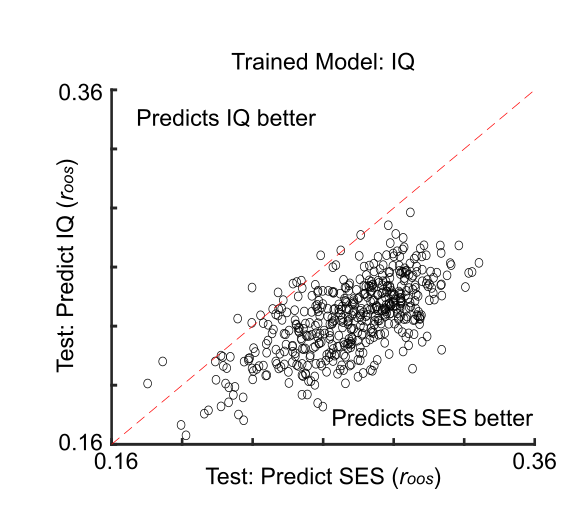

This whole thread is fucking fascinating and every technocratic liberal who scratches their chin about IQ, heritability, etc, needs to read it and get their shit rocked. It’s all SES. Always has been.

Jun 11

This was evidence of shortcut learning, a well-known problem in machine learning & AI.

Rather than models learning brain-IQ associations, they are learning links between brain-SES.

So much so that models trained to predict brain-IQ associations were better at predicting SES.

41

74

1,025

174,425

Tim retweeted

Here's my promised explainer. Doing my best to synthesize a lot of info here so check all my info; don't rely on it

So - the SpaceX IPO (SPCX:NASDAQ)

1/ Normally, a company with a massive valuation has to wait months to a year after its IPO before index funds are allowed to buy

Kiss your pensions goodbye, folks

May 20 - SpaceX's (SPCX) S-1 filing

Ludicrous targeted valuation: $1.8T despite $4.28B loss over last year

June 11 - offering price set

June 12 - first day of trading / IPO

July 6 - index funds add the stock

Absolutely unheard-of fast-tracking

39

446

2,393

478,732

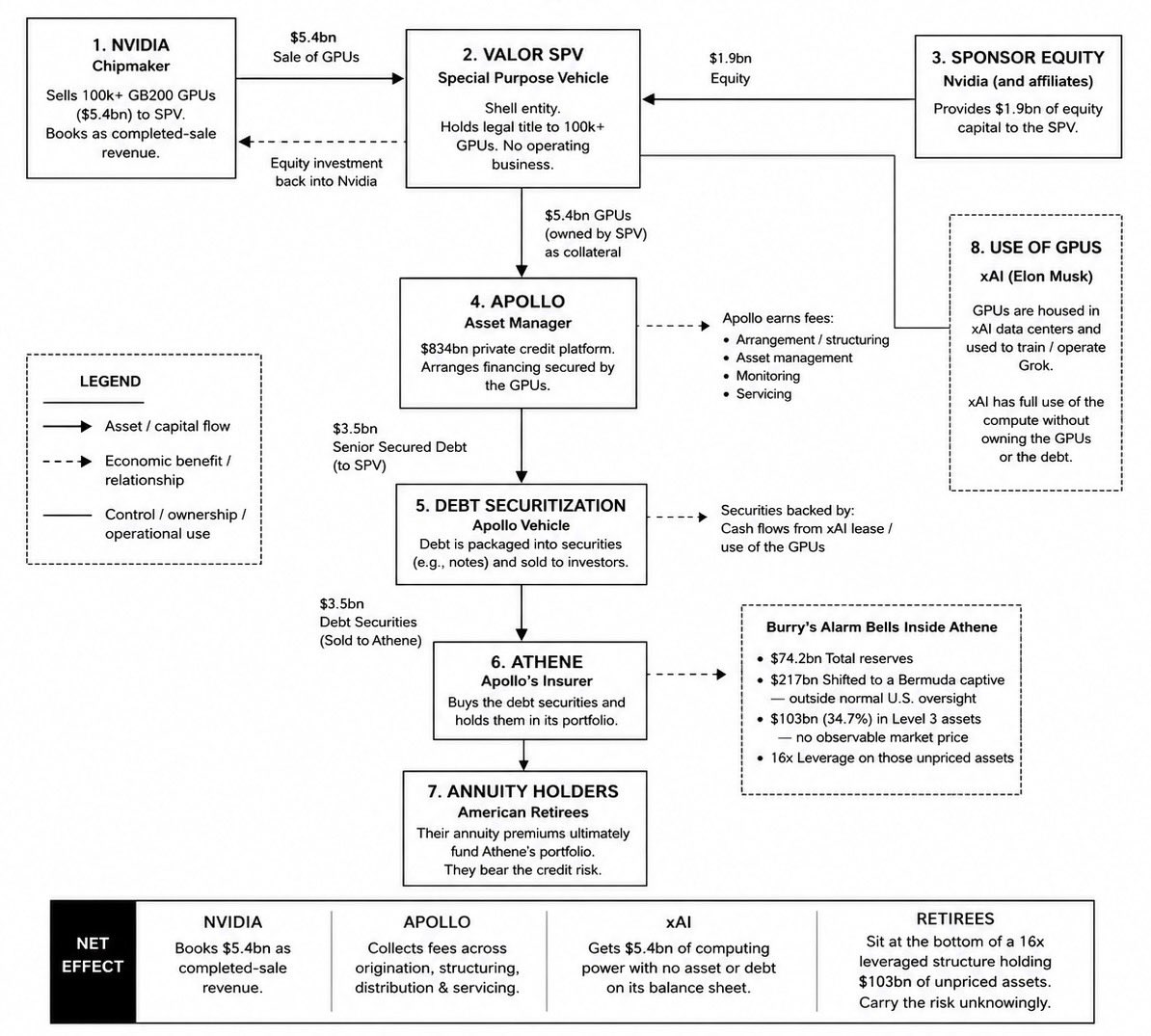

I worked as a Big 4 auditor for a decade, here’s my take on the Burry “Fugazi” thread

The transaction is real and the figures check out. Apollo led a $3.5bn capital solution for Valor Compute Infrastructure to fund a $5.4bn purchase of GB200 GPUs leased to xAI on a triple-net structure. Nvidia went in as an anchor LP. All publicly disclosed

But the accounting isn’t prima facie erroneous, and the thread oversells two things

On Nvidia’s revenue. Selling to an SPV is fine. The question under ASC 606 (US revenue standard) is whether control actually transferred. If VCI bears the risks and rewards, Nvidia books the sale legitimately

The REAL issue is the $1.9bn Nvidia ploughs back into VCI as an LP. That’s the round-trip. Net, Nvidia took in roughly $3.5bn of outside cash but booked $5.4bn of revenue

If part of your “sale” is funded by capital you re-injected, that portion isn’t a sale. The honest treatment is either net the $1.9bn off the transaction price, or run a “variable interest entity” (VIE) analysis and consolidate VCI. Recognising gross revenue on round-tripped capital is the potential weak apot

On “legally invisible.” This is rhetoric. The chips sit on VCI’s balance sheet, xAI carries an ROU asset and lease liability under ASC 842 (US leasing accounting standard). Nothing vanishes. It’s held by an entity nobody consolidates, and whether that non-consolidation is correct is the VIE question above

On Level 3 (fair value measurement tier). “No outside party can verify what they’re worth” is wrong. Level 3 means no observable inputs for that specific asset, NOT unverifiable

We typically ALWAYS brought in valuation specialists particularly for high risk material txs, you use observable comps and secondary GPU prices as model inputs, and auditors treat it as a critical audit matter. It gets more scrutiny, not less

The legitimate concern is smaller than this post lets on. Level 3 marks are management estimates exposed to optimistic bias, 34.7% concentration is high for retail annuity backing, and that sits on top of 16.6x leverage and a Bermuda captive outside US statutory oversight. Stack GPU residual-value risk on a multi-year lease and that’s the main concern

Burry’s substance is defensible. The “retirees unknowingly carry invisible risk” packaging is sensationalised. Policyholders hold fixed contractual claims, their exposure is to Athene’s solvency, not directly to GPU residuals

TLDR: auditors need to test whether the sale is overstated by the $1.9bn round-trip, and apply extra scrutiny to the unobservable Level 3 inputs

I’d hate to be the Audit partner signing these transactions off particularly given the public interest and frequency of similar transactions

Arthur Anderson Déjà vu?

May 31

🚨Michael Burry just said Elon Musk and Nvidia's deal is built on fake numbers.

Burry published a detailed breakdown calling the entire structure "Fugazi", his word for fake.

He is alleging that billions of dollars in Nvidia chips are being hidden off balance sheets, and that American retirees are unknowingly funding the whole thing.

Nvidia, the world's largest AI chip company sold $5.4 billion worth of its most advanced GPUs, the GB200, to a company called Valor.

Valor is not a real operating business. It is a special purpose vehicle, a shell company created specifically to hold these chips and nothing else. Nvidia also invested $1.9 billion of its own money directly into Valor on top of the sale.

Those 100,000 chips are now physically inside xAI's data center. xAI is Elon Musk's artificial intelligence company, the one that builds Grok. xAI is using every single one of those chips right now to run its AI models.

But here is what Burry is flagging.

Neither Nvidia nor xAI owns those chips on paper. Valor, the shell company holds legal title. That means $5.4 billion in GPU assets do not show up on Nvidia's balance sheet as inventory.

They do not show up on xAI's balance sheet as assets. They are legally invisible to both companies.

Nvidia gets to book the $5.4 billion as a completed sale and record it as revenue. xAI gets full use of the chips without owning them. And the risk disappears into a shell company in the middle.

Now here is where American retirees enter the picture.

Valor needed $3.5 billion in debt to fund this structure. Apollo provided it. Apollo is one of the largest asset managers on earth with $1.03 trillion under management and $834 billion specifically in private credit.

Apollo raised the $3.5 billion, packaged it into debt securities, and sold those securities to Athene.

Athene is Apollo's own insurance company. It sells fixed and indexed annuities, retirement savings products, to ordinary Americans.

When a retiree buys an Athene annuity, they believe their money is sitting in safe, stable investments. That money is now inside a structure funding Elon Musk's AI data center.

The numbers inside Athene are most alarming.

Athene holds $74.2 billion in reserves. It has moved $217 billion in assets into a captive insurer based in Bermuda, meaning those assets sit outside normal US insurance regulation and oversight.

Of the entire portfolio, 34.7%, equal to $103 billion, is classified as Level 3 assets.

Level 3 is an accounting classification that means there is no observable market price for these assets. No outside party can independently verify what they are actually worth.

The leverage sitting on top of those unpriced assets is 16 times.

Burry's says:

Every step of this structure is technically legal and publicly disclosed. But the entire thing was deliberately engineered across 8 to 12 steps to move credit risk off balance sheets and away from any market pricing.

- Nvidia books the revenue.

- Apollo collects the fees.

- xAI gets the computing power.

- And retirees sitting at the bottom of a 16x leveraged Bermuda insurance structure, holding $103 billion in assets with no market price carry the risk without knowing it exists.

76

164

1,133

227,374

Tim retweeted

May 31

🚨Michael Burry just said Elon Musk and Nvidia's deal is built on fake numbers.

Burry published a detailed breakdown calling the entire structure "Fugazi", his word for fake.

He is alleging that billions of dollars in Nvidia chips are being hidden off balance sheets, and that American retirees are unknowingly funding the whole thing.

Nvidia, the world's largest AI chip company sold $5.4 billion worth of its most advanced GPUs, the GB200, to a company called Valor.

Valor is not a real operating business. It is a special purpose vehicle, a shell company created specifically to hold these chips and nothing else. Nvidia also invested $1.9 billion of its own money directly into Valor on top of the sale.

Those 100,000 chips are now physically inside xAI's data center. xAI is Elon Musk's artificial intelligence company, the one that builds Grok. xAI is using every single one of those chips right now to run its AI models.

But here is what Burry is flagging.

Neither Nvidia nor xAI owns those chips on paper. Valor, the shell company holds legal title. That means $5.4 billion in GPU assets do not show up on Nvidia's balance sheet as inventory.

They do not show up on xAI's balance sheet as assets. They are legally invisible to both companies.

Nvidia gets to book the $5.4 billion as a completed sale and record it as revenue. xAI gets full use of the chips without owning them. And the risk disappears into a shell company in the middle.

Now here is where American retirees enter the picture.

Valor needed $3.5 billion in debt to fund this structure. Apollo provided it. Apollo is one of the largest asset managers on earth with $1.03 trillion under management and $834 billion specifically in private credit.

Apollo raised the $3.5 billion, packaged it into debt securities, and sold those securities to Athene.

Athene is Apollo's own insurance company. It sells fixed and indexed annuities, retirement savings products, to ordinary Americans.

When a retiree buys an Athene annuity, they believe their money is sitting in safe, stable investments. That money is now inside a structure funding Elon Musk's AI data center.

The numbers inside Athene are most alarming.

Athene holds $74.2 billion in reserves. It has moved $217 billion in assets into a captive insurer based in Bermuda, meaning those assets sit outside normal US insurance regulation and oversight.

Of the entire portfolio, 34.7%, equal to $103 billion, is classified as Level 3 assets.

Level 3 is an accounting classification that means there is no observable market price for these assets. No outside party can independently verify what they are actually worth.

The leverage sitting on top of those unpriced assets is 16 times.

Burry's says:

Every step of this structure is technically legal and publicly disclosed. But the entire thing was deliberately engineered across 8 to 12 steps to move credit risk off balance sheets and away from any market pricing.

- Nvidia books the revenue.

- Apollo collects the fees.

- xAI gets the computing power.

- And retirees sitting at the bottom of a 16x leveraged Bermuda insurance structure, holding $103 billion in assets with no market price carry the risk without knowing it exists.

954

4,086

16,319

4,256,066

Tim retweeted

May 31

Full structure

May 31

🚨Michael Burry just said Elon Musk and Nvidia's deal is built on fake numbers.

Burry published a detailed breakdown calling the entire structure "Fugazi", his word for fake.

He is alleging that billions of dollars in Nvidia chips are being hidden off balance sheets, and that American retirees are unknowingly funding the whole thing.

Nvidia, the world's largest AI chip company sold $5.4 billion worth of its most advanced GPUs, the GB200, to a company called Valor.

Valor is not a real operating business. It is a special purpose vehicle, a shell company created specifically to hold these chips and nothing else. Nvidia also invested $1.9 billion of its own money directly into Valor on top of the sale.

Those 100,000 chips are now physically inside xAI's data center. xAI is Elon Musk's artificial intelligence company, the one that builds Grok. xAI is using every single one of those chips right now to run its AI models.

But here is what Burry is flagging.

Neither Nvidia nor xAI owns those chips on paper. Valor, the shell company holds legal title. That means $5.4 billion in GPU assets do not show up on Nvidia's balance sheet as inventory.

They do not show up on xAI's balance sheet as assets. They are legally invisible to both companies.

Nvidia gets to book the $5.4 billion as a completed sale and record it as revenue. xAI gets full use of the chips without owning them. And the risk disappears into a shell company in the middle.

Now here is where American retirees enter the picture.

Valor needed $3.5 billion in debt to fund this structure. Apollo provided it. Apollo is one of the largest asset managers on earth with $1.03 trillion under management and $834 billion specifically in private credit.

Apollo raised the $3.5 billion, packaged it into debt securities, and sold those securities to Athene.

Athene is Apollo's own insurance company. It sells fixed and indexed annuities, retirement savings products, to ordinary Americans.

When a retiree buys an Athene annuity, they believe their money is sitting in safe, stable investments. That money is now inside a structure funding Elon Musk's AI data center.

The numbers inside Athene are most alarming.

Athene holds $74.2 billion in reserves. It has moved $217 billion in assets into a captive insurer based in Bermuda, meaning those assets sit outside normal US insurance regulation and oversight.

Of the entire portfolio, 34.7%, equal to $103 billion, is classified as Level 3 assets.

Level 3 is an accounting classification that means there is no observable market price for these assets. No outside party can independently verify what they are actually worth.

The leverage sitting on top of those unpriced assets is 16 times.

Burry's says:

Every step of this structure is technically legal and publicly disclosed. But the entire thing was deliberately engineered across 8 to 12 steps to move credit risk off balance sheets and away from any market pricing.

- Nvidia books the revenue.

- Apollo collects the fees.

- xAI gets the computing power.

- And retirees sitting at the bottom of a 16x leveraged Bermuda insurance structure, holding $103 billion in assets with no market price carry the risk without knowing it exists.

70

471

2,584

273,160

9500 likes voor dit?! Voor een account die eind vorig jaar is gemaakt? Dit is echt zo enorm geboost dat het niet grappig meer is, zelfs Wilders krijgt niet zoveel botlikes als dit.

May 29

Mijn naam is Mieke. En ik ben een oorspronkelijke, inheemse, trotse Nederlander. 🇳🇱

#wijbestaan

2

133

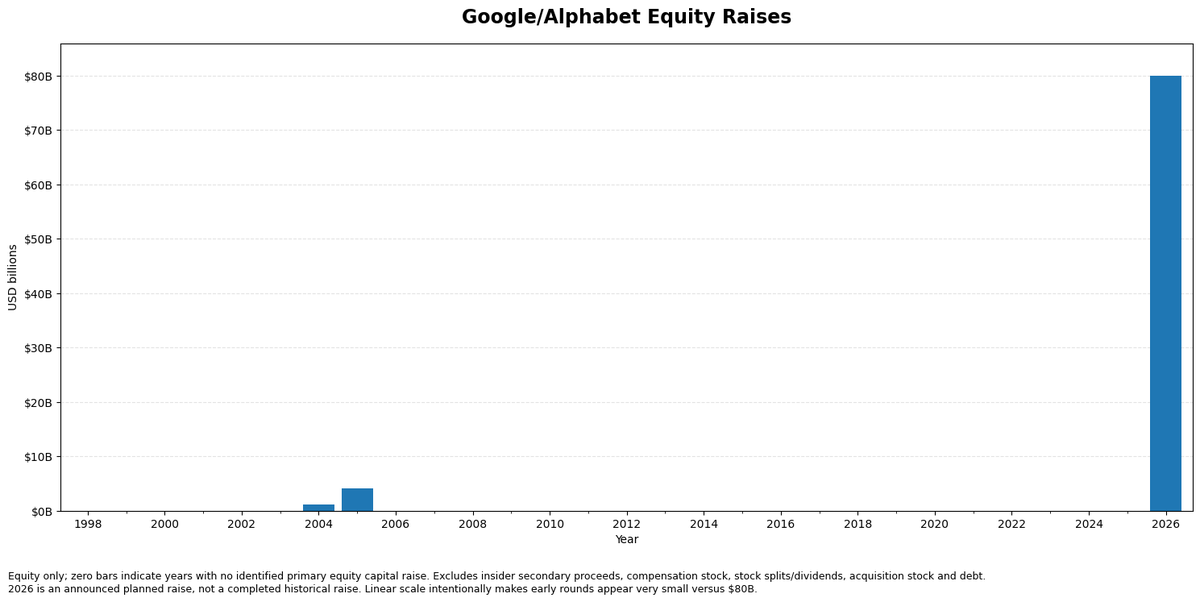

Rule changes for the SpaceX $SPCX IPO:

Index providers waived the profitability requirement and cut the seasoning window from 90 days to 5.

This forces over $30 trillion in passive 401k and retirement money to buy SpaceX at IPO valuations.

Bloomberg Intelligence estimates S&P 500 funds must absorb 19% of SpaceX's float within 6 months.

Russell 1000 and Nasdaq 100 funds will absorb 24%.

The rules built to protect passive investors:

1. S&P 500 has required 12 months of trading and 4 quarters of GAAP profitability since 2002. Both waived.

2. Nasdaq cut its inclusion window from 90 trading days to 15.

3. FTSE Russell cut its to 5.

All three benchmarks are now structured to buy SpaceX at IPO pricing.

551

1,591

10,014

11,636,755

Tim retweeted

May 29

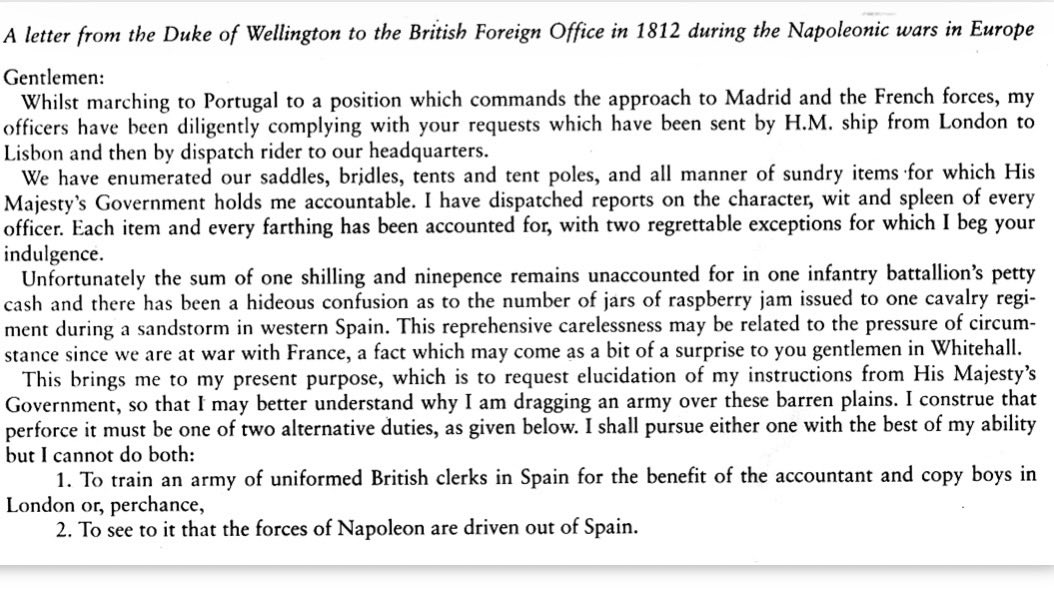

Having lived and/or worked in DC for over a decade, I can’t believe I’d never heard of this letter from the Duke of Wellington to a bunch of bureaucrats in London during the Napoleonic wars.

If you haven’t either, please enjoy (link below if the font is too small):

32

202

1,356

85,458

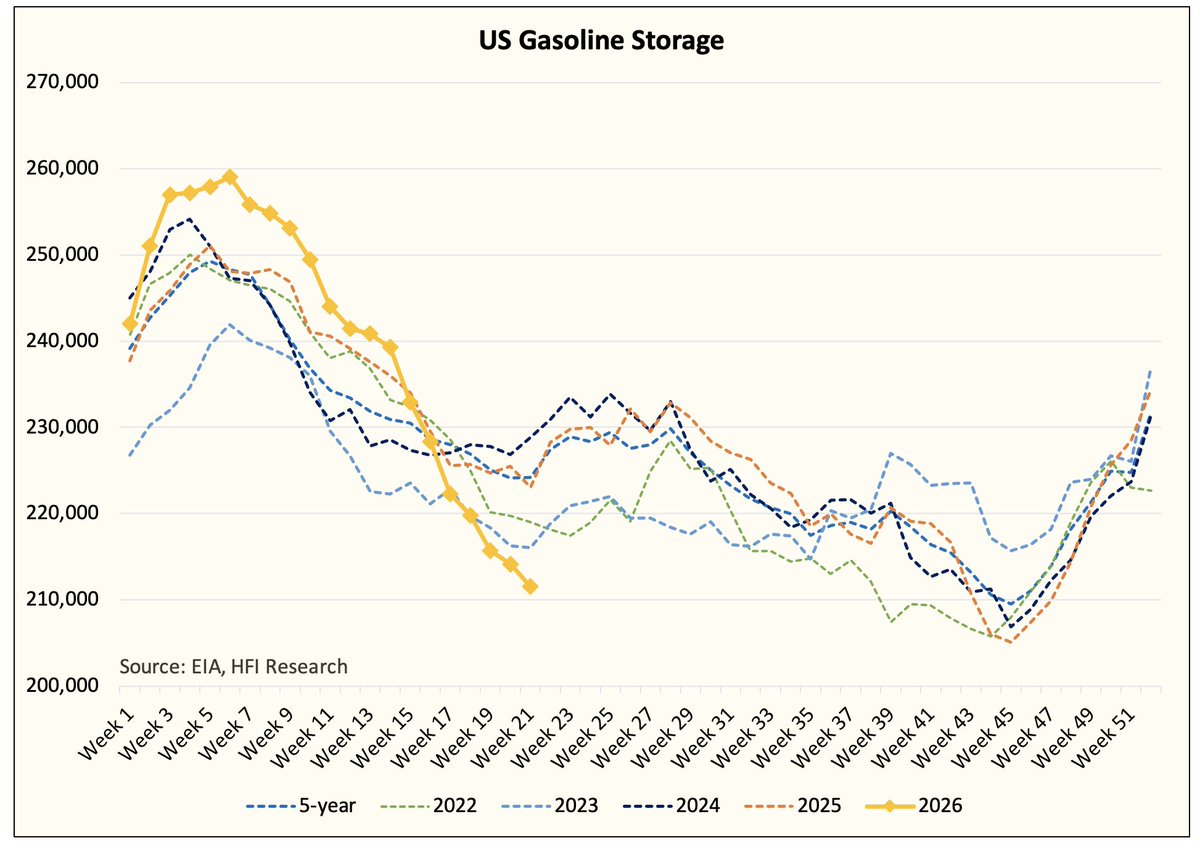

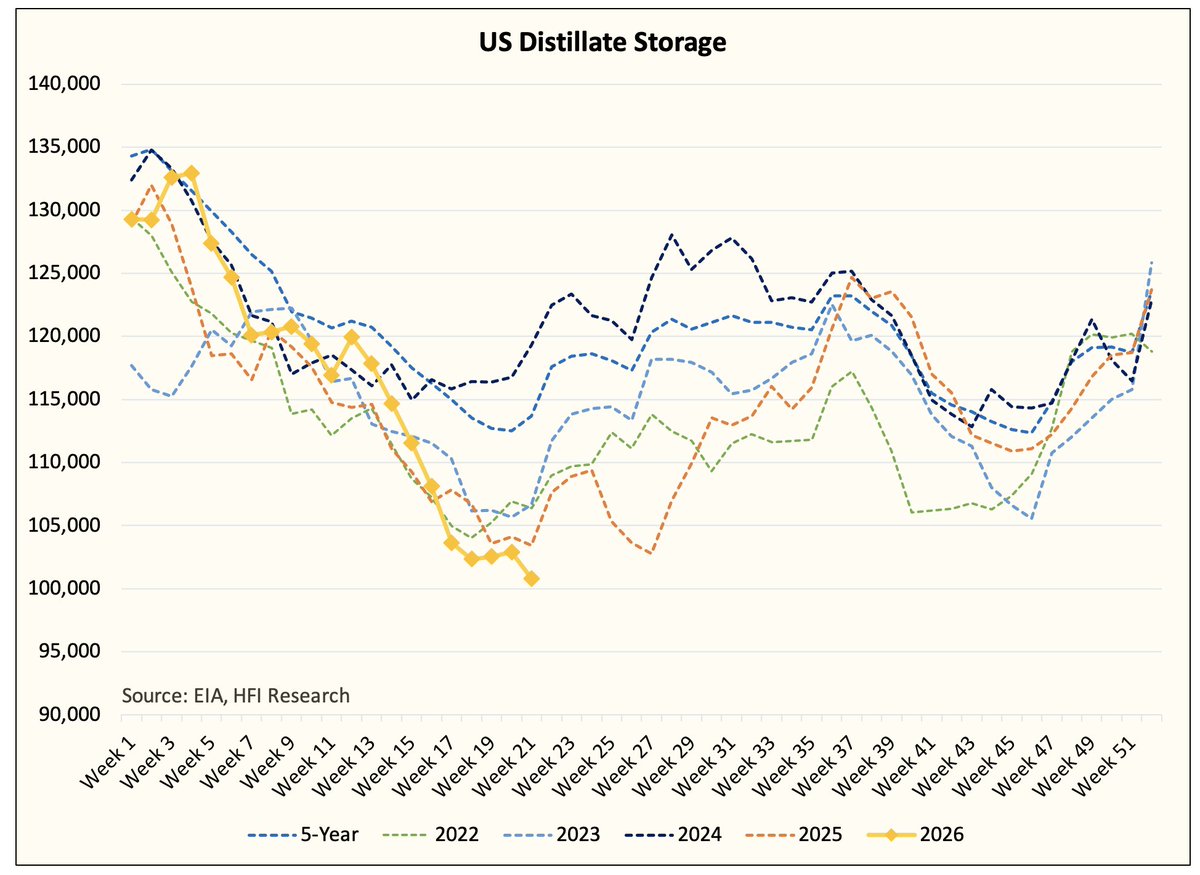

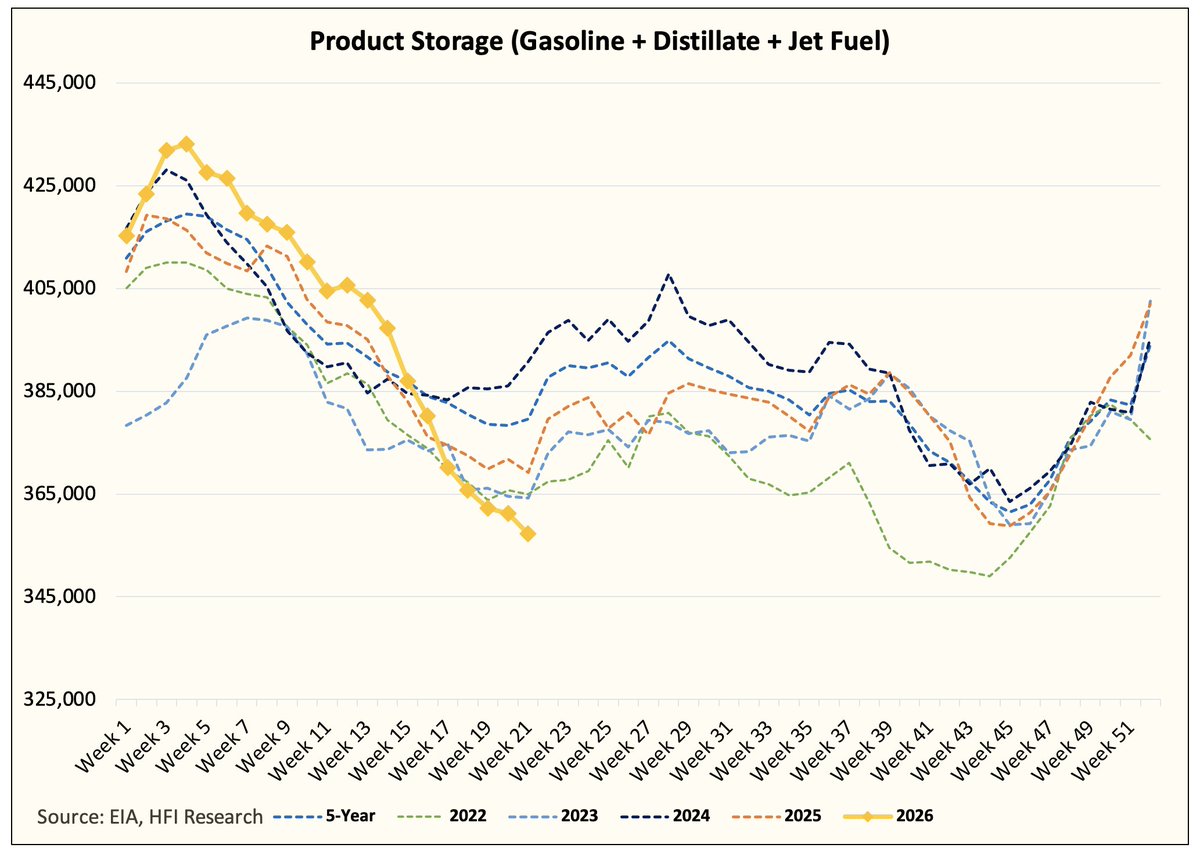

So at over 3 months of Hormuz closed the US is hardly at 2022 levels. Pretty astonishing how much reserve is in the system.

May 28

We are ~9 million bbls away from hitting a storage level that's the equivalent of living paycheck to paycheck for gasoline and distillate.

Once we get there, even a minor disruption (any sort of outage) will result in gasoline lines at gas stations.

I guess we are really doing this.

20

Tim retweeted

May 27

I am once again thinking of William Shatner going through a profound existential crisis after being in space, trying to explain the terrifying emptiness he felt whilst Jeff Bezos sprayed champagne in his face and interrupted him to say 'WAZZUUP' whilst dabbing to Barenaked Ladies

63

1,290

22,797

310,642

Tim retweeted

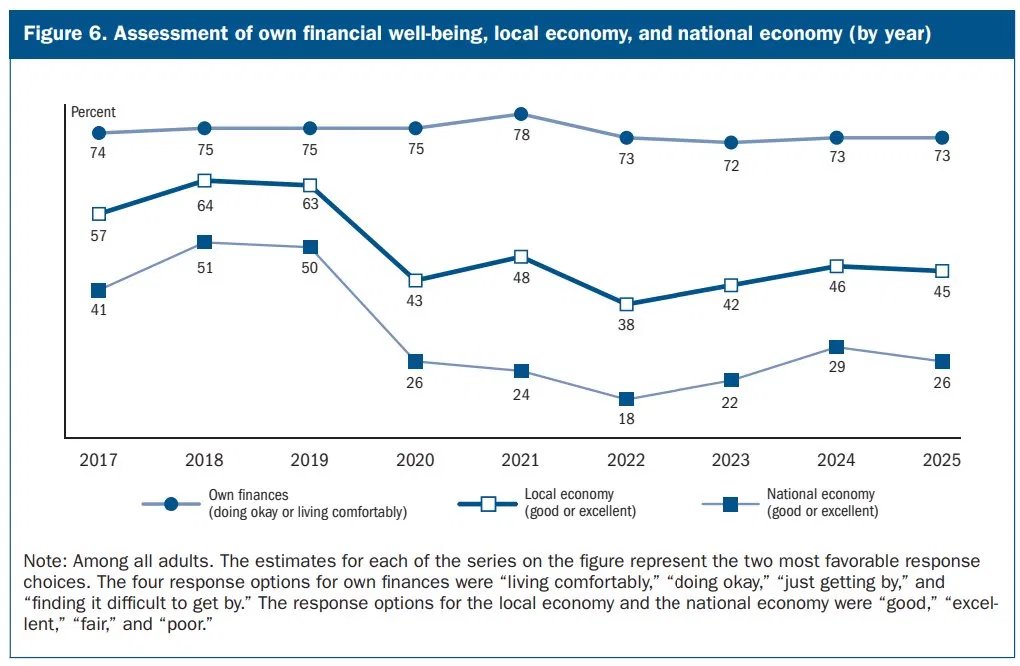

May 26

The funny thing is people rate their own economic circumstances far more favorably now than they did during the Great Recession. This lines up with the data. It's the external economy that rates poorly. Explanations that rely on people not doing well individually don't fit.

May 26

At the meta level, the vibecession question is simple: either you believe the economy is worse than during the Great Recession, as consumer sentiment implies, despite ~0 empirical evidence to this effect, or you agree that there's a gap between sentiment and material conditions.

30

102

832

115,711

Tim retweeted

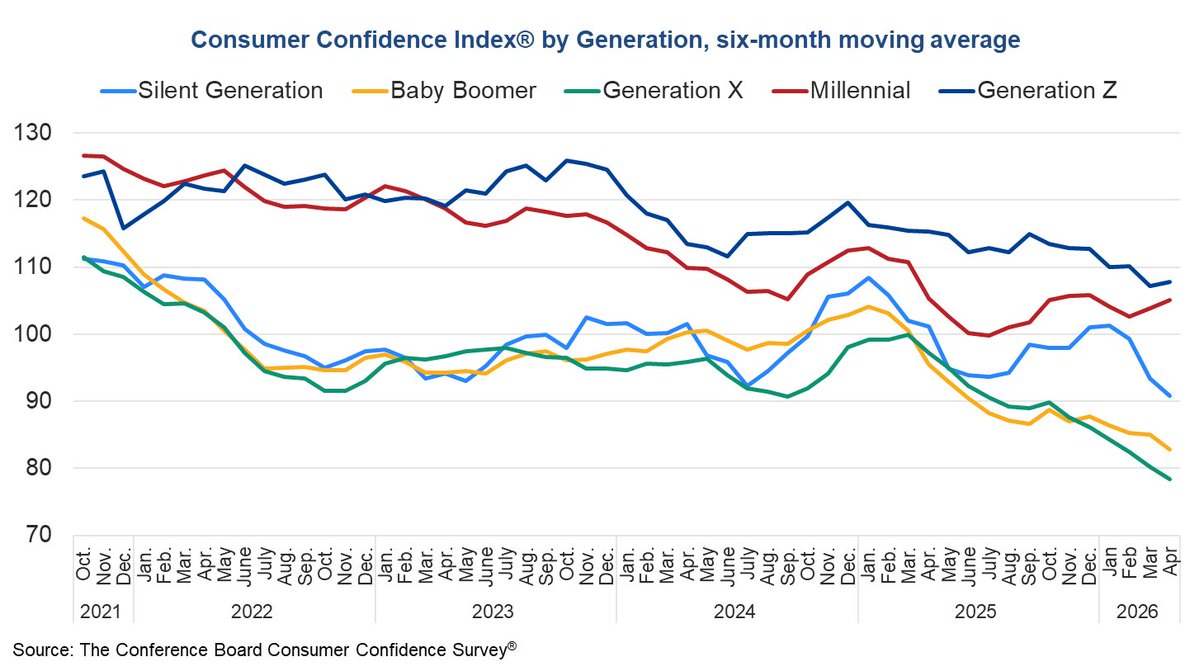

May 25

Narrative violation: Gen Z has the highest consumer confidence. Gen X and Boomers are the pessimists.

I do feel that undercuts many of the material explanations for the vibecession, insofar as uniquely awful economic conditions for young people are a main driving force.

51

104

963

93,099

Tim retweeted

May 24

I have been screaming about this for MONTHS and Blind Squirrel just put out the best breakdown I have seen yet on the mechanics of why the SpaceX IPO could destabilize the entire market.

The numbers are RIDICULOUS:

$86 billion in stock to place at a $1.75 trillion valuation. Even under the most generous assumptions about index demand, closet benchmarkers, and retail participation, the bankers are STILL short roughly 40 to 50% of the demand needed just to get the deal to 1x covered.

And once passive funds are forced to mechanically buy in, they have to SELL $44 billion of existing holdings to make room.

In a market where top of book liquidity has already collapsed, that selling could feel like a trillion dollars of price impact.

Your 401(k) is the exit liquidity for insiders who bought in at less than 5% of the current valuation.

Read this and share it with everyone you know:

open.substack.com/pub/arcadi…

21

53

188

45,465