Canadian Small Cap Coverage for Active Investors Not Financial Advice. Please see our disclaimer: tokstocks.com/disclaimer

Joined March 2022

- Tweets 4,405

- Following 1,332

- Followers 1,765

- Likes 24,987

828 Photos and videos

Jun 9

The hate is high and rightfully so for $SOMA.V but below is a good nuanced take.

Jun 9

$SOMA.v has become a total basket case. Stock has plunged from 2.56 in January to 0.83 yesterday and will probably take another hit today due to the announced share offering. Management is to blame here. They overpromised when it was clear, at least to them, that they would not be able to deliver on their promises.

So where do we stand today? Fully diluted mcap incl. the pending share offering with broker warrants and incl. last week’s debt-for-equity transaction is CAD 126.2M = USD 90.6M based on yesterday's closing price. If Soma can’t solve its problems and increase production in a substantial way, the stock is not and will not be a buy. However, leverage to higher production and cash flows has become extremely large. If Soma managed an annual runrate production of 30 koz by year-end, the annual AISC margin at 4.5k gold would be USD 67.5M or 74.5% of fully diluted mcap. That would already be worlds better than where we stand today. If Soma managed to come close to achieving its old 2026 production target of 55 koz (won’t happen before 2027), the annual AISC margin at 4.5k gold would jump to USD 170.5M or 188% of fully diluted mcap. In this case the after-tax FCF would exceed the fully diluted mcap. Last year Soma speculated about achieving an annual production of 70 koz by 2027, but I won’t go there.

Result: If Soma can turn things around and achieve the first line of its previous growth target, the stock is a steal. However, caveat emptor (buyer beware). IMO one can’t have the necessary conviction right now that the company will recover operationally. Management needs to deliver first and regain the lost trust before an investment in the company makes sense.

327

TokStocks retweeted

For those interested, some technical mining talk. You might get the impression I hate equivalent grades and prefer NSR rock values instead.

A rare conversation with @KJKLtd.

4 Free Tools That Expose Mining Promoter Lies (an Engineer's Guide)

Watch it: youtu.be/eBQETcFQ64g

3

4

29

6,000

Jun 1

Exactly what I wrote in my last Substack article.

Junior miners are now outperforming the majors.

The Venture is breaking out of a 10-year base.

This looks like the real deal - years in the making.

232

TokStocks retweeted

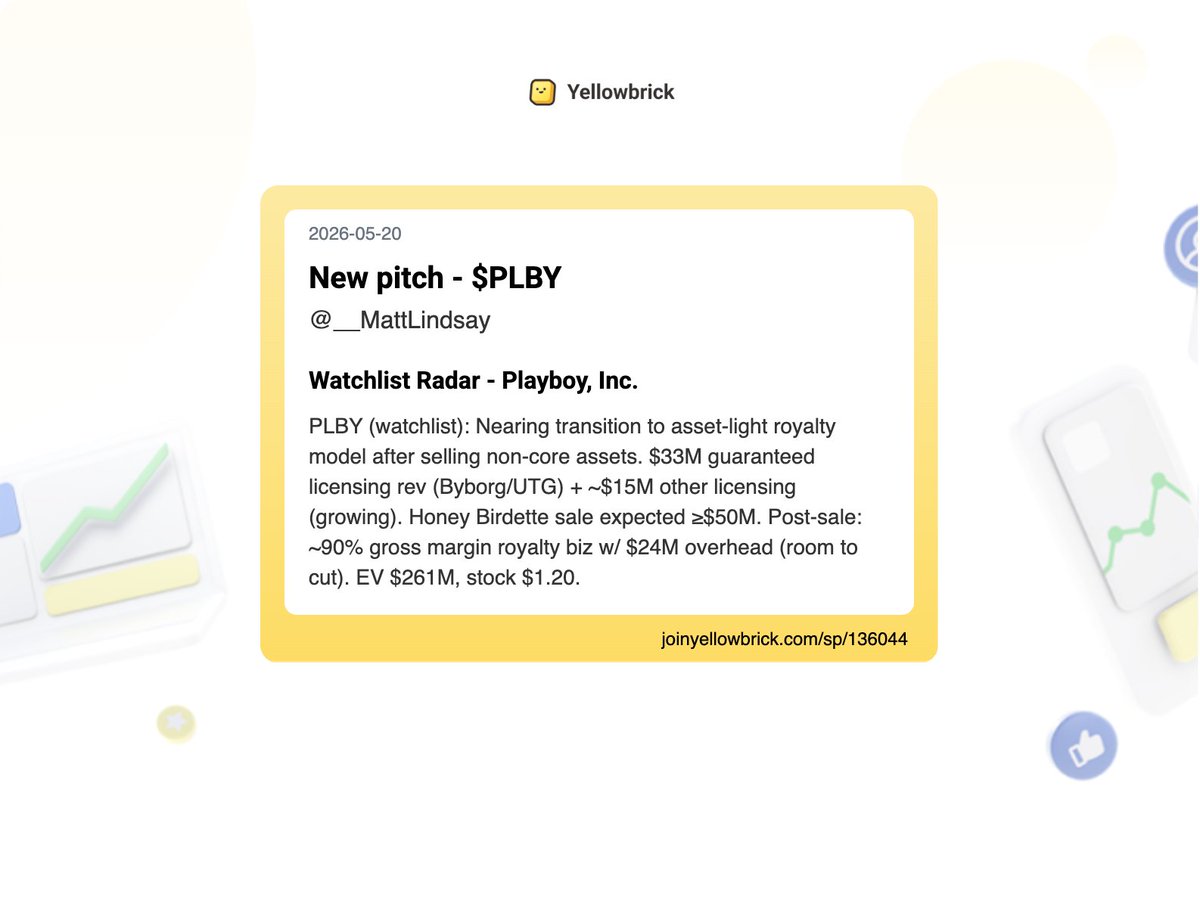

Added 78 new stock write-ups to the site (pt final):

@__MattLindsay (watchlist) - $PLBY, $KITS.TO

@BlokeOak57182 - $RGL.L

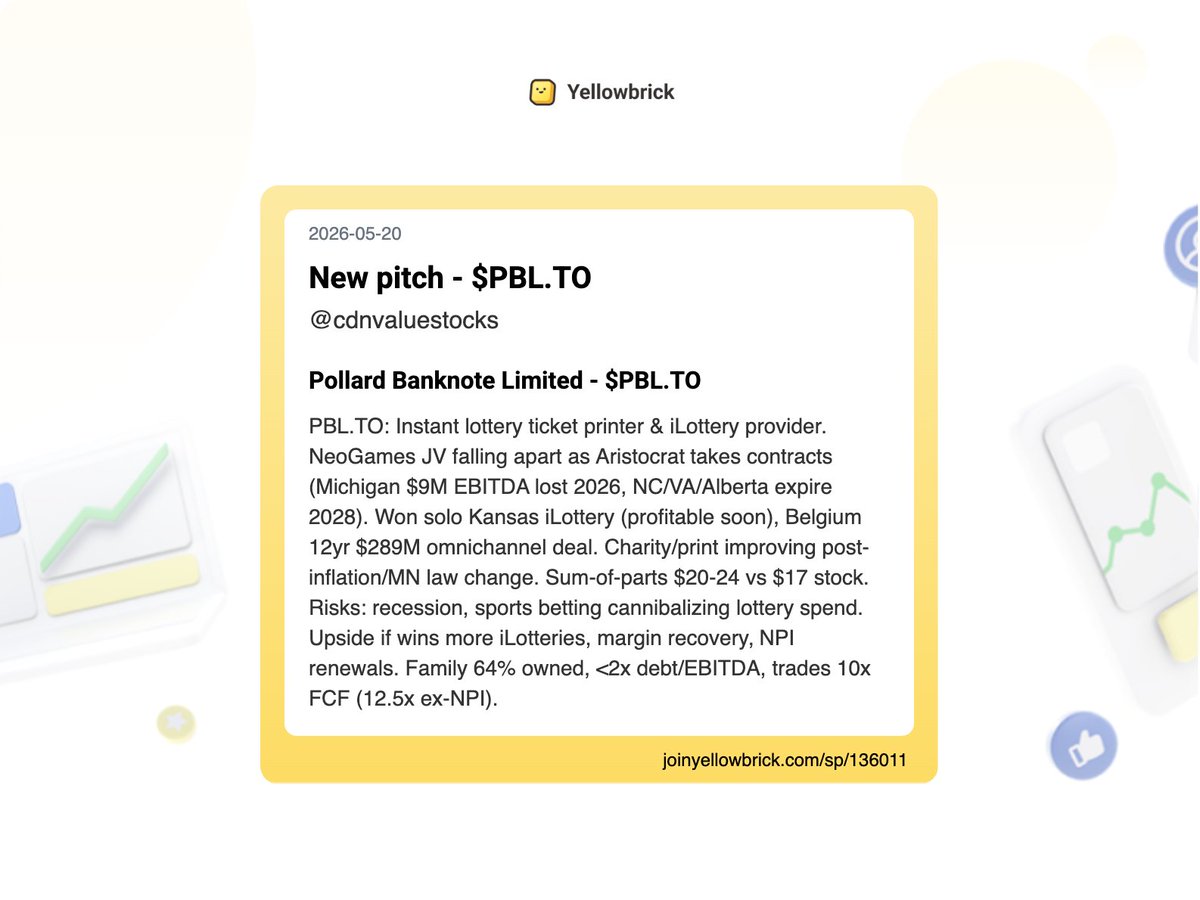

@cdnvaluestocks - $PBL.TO

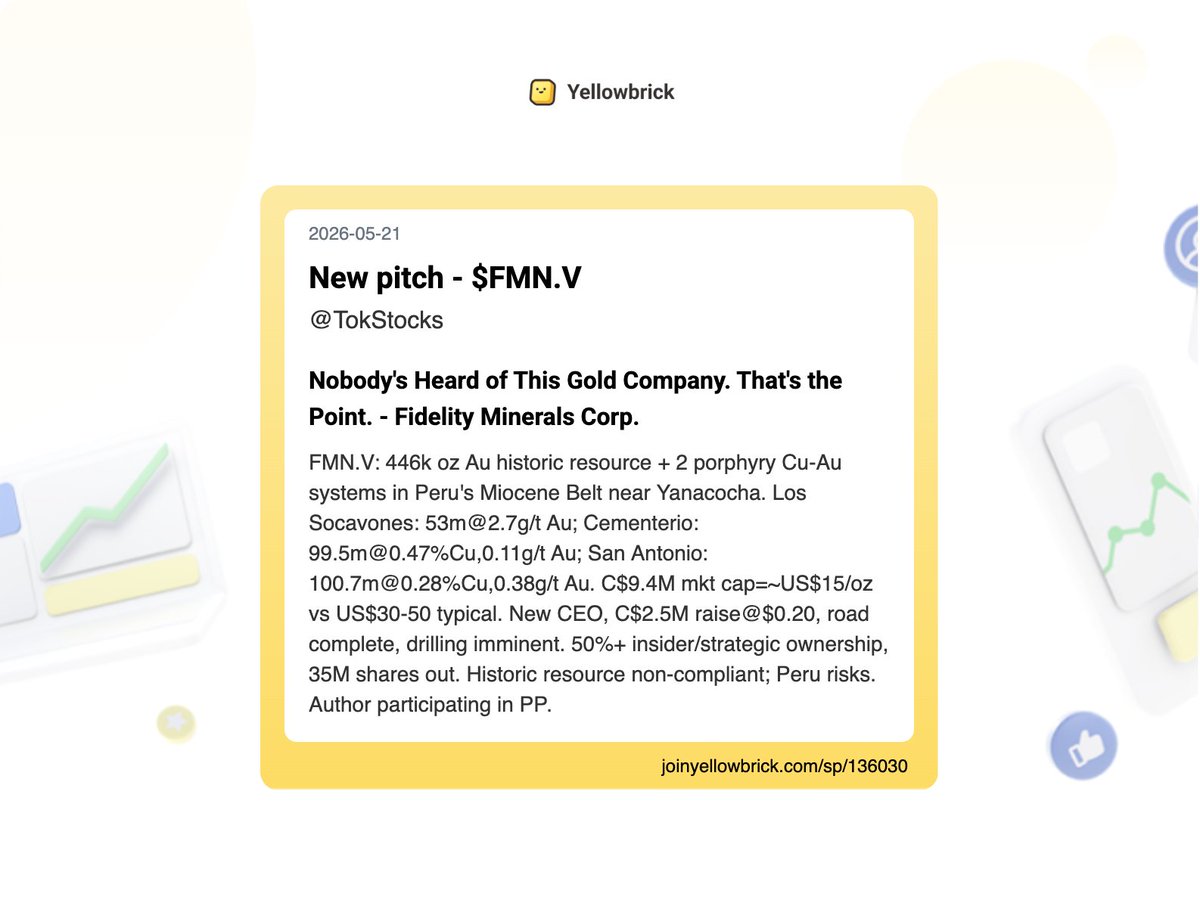

@TokStocks - $FMN.V

@norbucap - $AS (earnings)

fund letters

and more...

2

2

9

2,325

TokStocks retweeted

May 19

We’re breaking ground on Nouveau Monde Graphite’s Matawinie Mine — just six months after we referred it to the Major Projects Office. This will become the largest graphite mine in the G7.

It will create more than 1,000 career opportunities, catalyse nearly $2 billion of investments, and build a stronger, more independent Canadian economy.

455

365

1,863

145,388

May 8

First time I’ve ever agreed with MTG.

👽🛸👎

I really don’t care about the UFO files.

I just don’t.

I’m so sick of the “look at the shiny object” propaganda while they wage foreign wars, let rapist and pedophiles run free, and ruin the value of our dollar.

Unless they roll out live aliens and test demo UFOs or actually admit what we know this really is then I have way better things to do on this Friday.

200

TokStocks retweeted

May 1

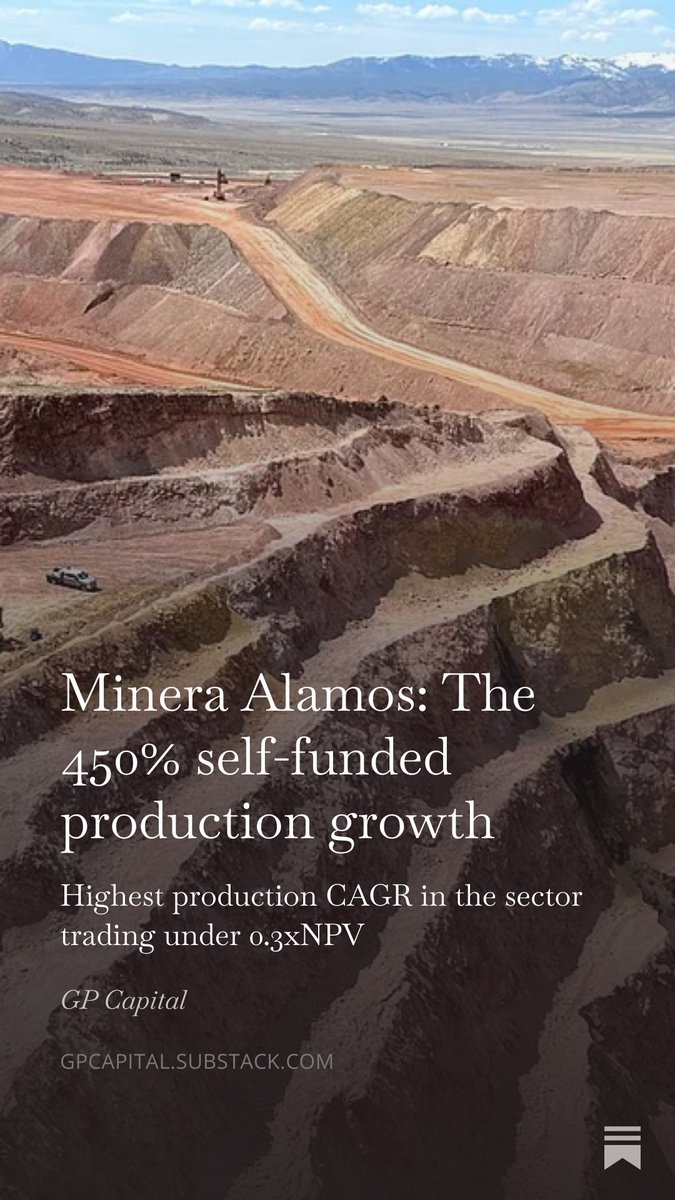

Just wrote a 7,000 word report on Minera Alamos.

Tldr:

-Highest producting CAGR in the sector 26-29 at 68%

-Trading under 0,3xNPV

-Production in the US

-A lot of insiders buying

Read the report here:

open.substack.com/pub/gpcapi…

$MAI.V $MAI.NE

7

8

55

33,401

TokStocks retweeted

May 1

Interesting price action in precious metals.

Seeing a lot of higher highs and higher lows heading into the weekend.

Also bouncing off oversold levels.

Take that for what it's worth.

4

3

79

11,026

TokStocks retweeted

Commodities just broke out of a 15-year base.

The supercycle accelerates - led by crude oil.

Hard asset investors win.

18

98

528

22,572

TokStocks retweeted

Apr 30

While I hear many throwing in the towel on Figma, $FIG, it’s a good time to recall the fundamentals amidst poor price action.

- 2027 P/S Ratio: 4.9x

- $1.7B Cash (20% of market cap)

- 136% Net Retention Rate (best in class)

- AI Credits & Monetization just turned on

Figma is a software business born in the AI era. The fact that they don’t have a bloated headcount like the incumbents in the industry should prove to be a tailwind.

1

2

15

3,848

TokStocks retweeted

Apr 29

BREAKING NEWS

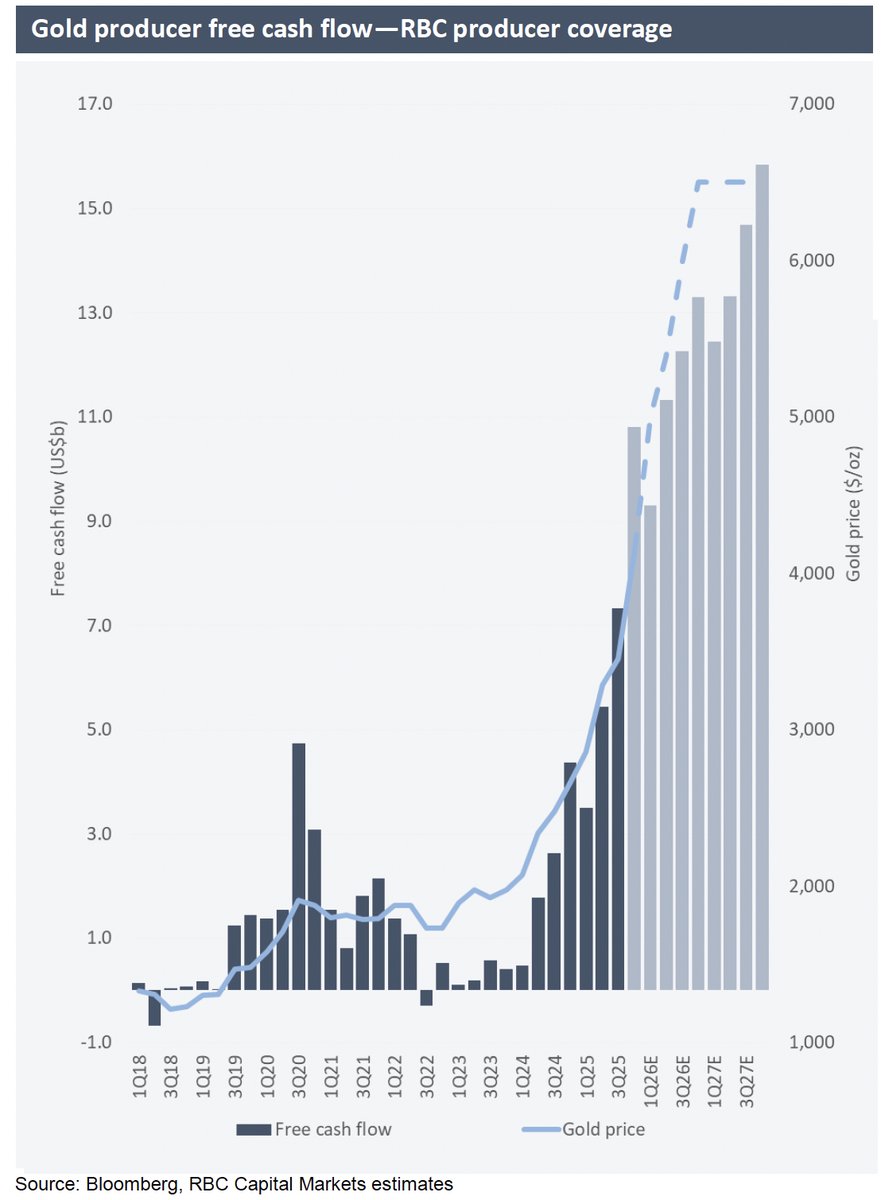

CENTRAL BANKS ADDED GOLD HOLDINGS AT THE FASTEST PACE IN MORE THAN A YEAR IN THE FIRST QUARTER

Here we go again…

21

190

1,301

83,683

TokStocks retweeted

Apr 28

Gold price could see $8,000 on de-dollarization, Deutsche Bank projects dlvr.it/TSGYQh

25

151

615

60,100

This guys gets it..

& there is more.

Will comment later today or early this week on the bigger picture of the announcement today.

Congrats to all involved.

#LNG $ARX.TO

Apr 27

$TOU.to $ARX.to - also given the sizable Cdn retail & Institutional ownership of $ARX.to, the scrip portion of the transaction is unattractive to hold. I would expect once today's arb flows get settled, that sizable holders of ARC look to rotate funds into other large cap Cdn energy and Tourmaline $TOU.to is the most logical choice.

2

1

29

6,061

TokStocks retweeted

Apr 27

McLaren Golf about to supplant PXG in wealthy 12-handicapper bags across this great nation.

84

52

2,777

193,849

TokStocks retweeted

Apr 27

The Canada Strong Fund is Canada’s first national sovereign wealth fund. It will invest in the major projects that are transforming our economy — and give Canadians a direct stake in our nation’s prosperity.

1,502

563

4,655

264,465

Shell agreed to buy Canadian producer ARC Resources for $13.6 billion, in a deal that will expand the company’s oil and gas production. bloomberg.com/news/articles/…

18

33

107

44,573

Apr 25

Good job! Nice interview! A couple of the good ones got together for a great pod.

Apr 25

Canada is known for exporting commodities

Another commodity in hot demand is Canadian cannabis according to @Stocks_Stones micro cap investor

For a look at ways to play this watch the full episode! youtu.be/odjCVG36ETc?si=zUTH…

1

4

790

Apr 25

RT @ericnuttall: Ninepoint Energy Strategies Update: the "battle for the barrel"™️ and what it means for the oil price in the weeks ahead:…

62