Joined November 2021

- Tweets 2,280

- Following 104

- Followers 633

- Likes 4,080

408 Photos and videos

I gave you a decent opportunity to load up $IONQ when risk/reward looked extremely favorable.

Then the stock soared nearly 50%.

Did you listen?

If I hadn't already built my core position in $IONQ back at ~$8, I'd definitely be tempted to initiate a starter position here around $28 (~$10B market cap).

1

7

447

Congress listened.

x.com/i/status/2044414411226…

Apr 15

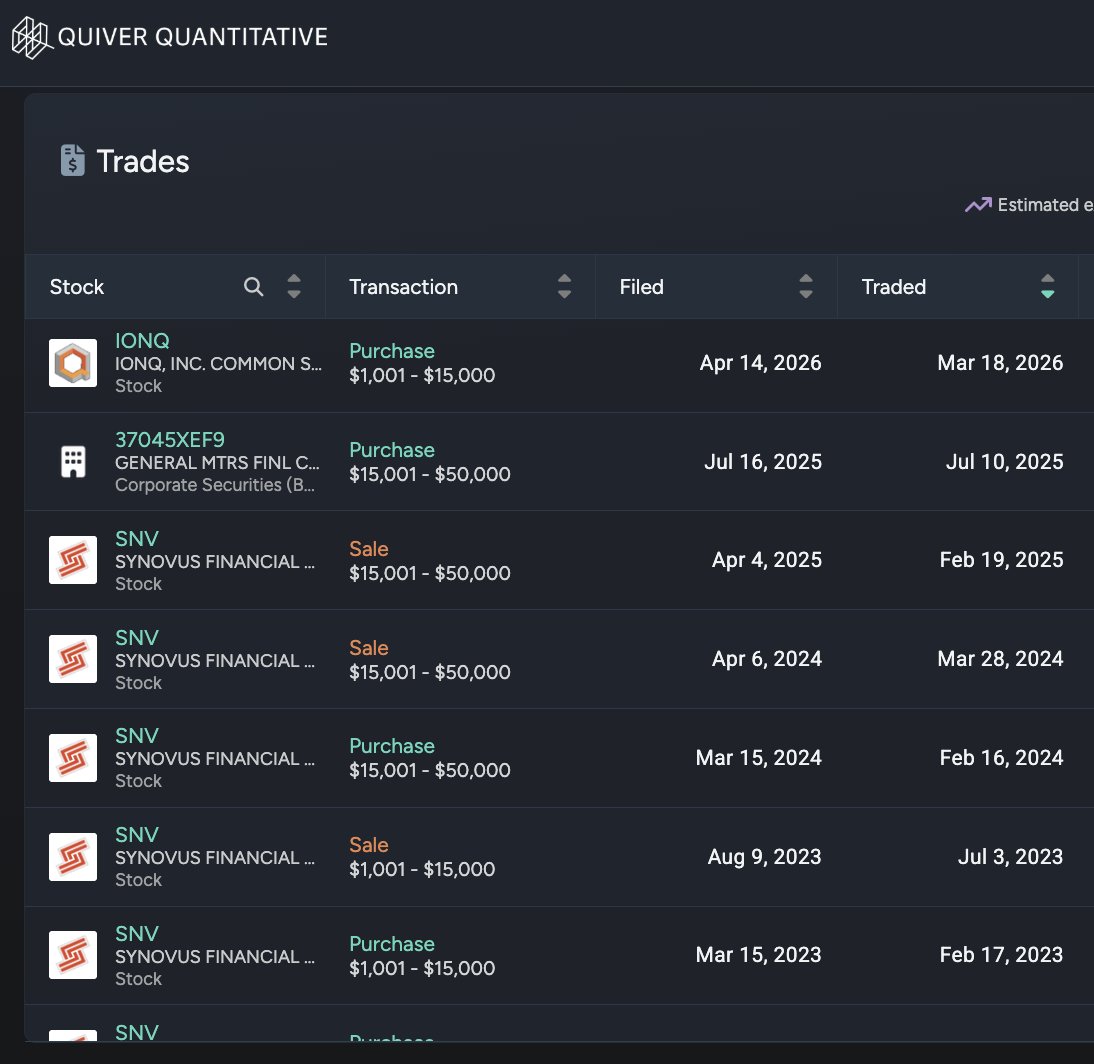

BREAKING: We just caught another interesting trade.

Representative Greg Steube just filed a purchase of stock in the quantum computing company $IONQ.

This is the first time we have seen anyone in Congress buy the stock.

We'll be watching $IONQ closely.

1

141

Launch. Satellites. Solar. Subsystems. Photonics.

Vertically integrated end-to-end $RKLB 🛸👽

Apr 14

Welcome to the Rocket Lab team, Mynaric!

Today we officially acquired Mynaric, adding laser optical communications to our growing space systems portfolio. A big moment for our teams and for the space industry as we make leading satellite laser communication technology available at the volume and speed demanded by commercial and government satellite customers across Europe, the U.S., and rest of world.

4

362

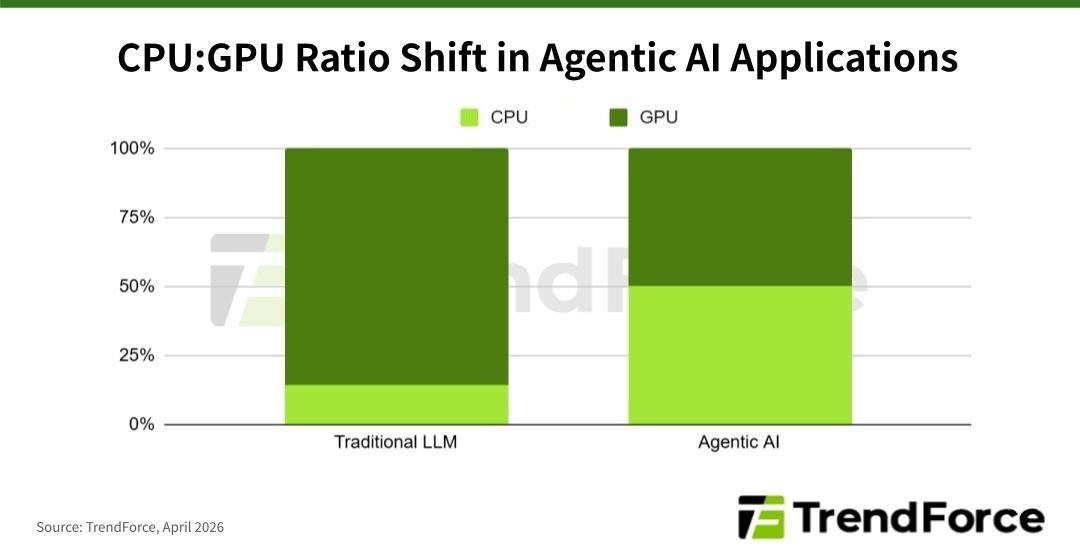

Agentic AI workflows rely on both CPUs and GPUs, each playing a distinct but equally critical role.

While the GPU enables fast inference, the CPU handles the orchestration layer: scheduling tasks, executing tools, managing branching logic, coordinating multi-step reasoning, and ensuring the entire pipeline runs smoothly and efficiently.

$ARM is exceptionally well positioned to capture a significant share of the massive transition from traditional LLM workflows to advanced agentic AI systems.

$ARM everywhere ⌁ DD drop 🔖🛸

They said they would do it, they're actually doing it.

$ARM is now a direct silicon provider in the agentic AI era.

⌁ Big announcement

In agentic AI systems, the CPU serves as the orchestration layer, managing parallel reasoning loops, dynamic tool calling, memory management, accelerator scheduling, data movement, and continuous agent execution.

Agentic AI is projected to require >4x current CPU capacity per GW because agents generate far more tokens and inter-agent traffic than static models.

This is in this environment that $ARM decided to drop its first-ever production CPU built on Neoverse V3 cores: the Arm AGI CPU, which is ruthlessly optimized specifically for those agentic workloads.

The company claims it delivers over 2x performance per rack versus latest x86 on industry workloads while slashing CAPEX by roughly $10b per GW of data-center capacity.

This is a big deal. After more than 35 years, $ARM is finally shipping finished chips of its own, not just CPU subsystems.

⌁ Business model leveled up

For years $ARM lived on licensing plus royalties.

Now they capture direct silicon margin on top of that flywheel.

$META is lead co-developer and first customer of the AGI CPU (multi-generation roadmap committed).

Other launch partners/customers such as OpenAI, Cerebras, $NET, F5, Positron, Rebellions, SAP, SK Telecom have also been hilighted.

CEO Rene Haas clearly laid out the 2031 target: $25b annual revenue and $9 EPS, with the AGI CPU line positioned as a material piece of that expansion.

⌁ Last thoughts

I've followed the company for a while now, and this is the clearest execution signal yet under Rene Haas.

$ARM is engineering its own high-margin, high-volume product revenue flywheel atop the existing base.

If the first racks validate the claims in H2 2026, the revenue path to that $25b target starts looking realistic.

2

123

CRITICAL VALIDATION OF THE THESIS BUILT OVER THE LAST 5YEARS 🛸👽

This is no longer theory.

This is no longer a lab demo.

$IONQ has now definitively proven that they can scale quantum computation by using photonic links to interconnect physically separated trapped-ion processors, while fully preserving the coherence required for advanced quantum operations.

This is a pivotal moment I've been anticipating for years...

The roadmap is effectively de-risked.

We're now transitioning from standalone quantum processors to true distributed, networked quantum architectures.

Let's entangle some processors! 🛸

2

22

953

$IONQ ⌁ new benchmark DD drop 🔖🛸

$IONQ built the quantum equivalent of MLPerf, an application-centric framework that measures what actually matters in quantum computing.

The framework runs 13 benchmarks across optimization, quantum chemistry, machine learning, data loading, simulation, and foundational algorithms, shifting the decisive metric from raw component specs (qubits, fidelities, coherence) to end-to-end, workflow-relevant outcomes: Time-to-Solution (TTS), Energy-to-Solution (ETS), and verifiable solution quality.

It enforces two categories:

⌁ Closed benchmarks: implementation is fixed, enabling pure system-level comparison (apples-to-apples hardware fights).

⌁ Open benchmarks: lets algorithms evolve while holding the success bar fixed (algorithmic innovation measurements).

The benchmarks strip away problem-specific tricks and ask one question: how much useful complexity can the machine handle before output turns to noise?

⌁ Industry shift

This is the very moment quantum computing leaves the lab metrics behind because customers can now price real ROI instead of counting qubits.

Govs and enterprises evaluating RFPs will reference TTS and solution quality under frameworks like this.

The openness lowers the barrier for third-party scrutiny and forces every player to compete on outcomes that matter.

⌁ IonQ's positioning

Four results from the white paper illustrate what this kind of benchmarking reveals.

$IONQ's low noise and all-to-all connectivity not only contribute to high-quality results, but also yield TTS and ETS metrics that are commercially meaningful, particularly against architectures where noise floors extend solution time significantly or prevent convergence altogether.

By publishing the rules and leading on the workloads that drive early commercial value, $IONQ seizes the narrative.

They turned their architectural strengths into the de-facto reference.

Future runs will expose any regression.

We're still NISQ, fault tolerance isn't here yet but commercial traction is definitely accelerating.

9

469

$ALMU is up ~30% pre-market. They just secured more than $4 million in fresh US Gov contracts. 👽🛸

Aeluma is accelerating the scale-up of its heterogeneous integration platform for quantum dot lasers and AlGaAs quantum nonlinear photonics, technologies critical for next-gen quantum systems and high-speed datacom/AI infrastructure.

Key signals in the announcement:

⌁ Direct work with Tower Semiconductor ($TSEM) on wafer production and fabrication

⌁ Collaboration with Sumitomo Chemical Advanced Technology for advanced materials

⌁ Focus on transitioning from lab demos to manufacturable processes on large-diameter (200mm/300mm) platforms

Why this matters:

$ALMU's platform aims to solve one of the biggest bottlenecks in scaling photonics: integrating high-performance III-V devices onto silicon at volume and cost that actually work for real-world deployment.

Government validation in quantum and photonics often serves as a strong signal for broader adoption in defense, AI optics, and high-performance computing.

Non-dilutive capital deepened manufacturing partnerships = reduced execution risk on the path to commercialization.

Aeluma $ALMU ⌁ Competitive landscape DD drop 🔖

AI interconnects (CPO/LPO for scale-up/scale-out in GPU clusters) are $ALMU's dominant near-term opportunity (~4B SiPh market 2026 growing 25-45% CAGR to $8-13B by 2030).

Co-packaged optics will obviously replace copper. The problem is the optical industry is currently trapped in a massive supply chain constraint.

The legacy approach is a dead end for hyperscale. It relies on fabricating InP lasers on tiny three-inch to four-inch wafers, then mechanically bonding them to silicon.

⌁ Aeluma enables scalability

The ultimate state of physics here is monolithic direct growth, meaning growing III-V compound semiconductors directly on massive 300mm silicon wafers.

$ALMU is taking this exact path. They use proprietary buffer layers and quantum dot active regions to absorb the lattice mismatch between InP and silicon.

Since quantum dots are isolated 3D nanostructures, threading dislocations isolate locally instead of killing the whole laser.

This allows $ALMU to tap into standard foundry economics. $TSM or $TSEM can process these 300mm wafers.

That drops the cost floor by an order of magnitude, enabling high-volume manufacturing.

⌁ Competition

Quite frankly, the competitive field is divided between companies solving for tomorrow and companies solving for 2028.

$INTC is the big dog in high-volume silicon photonics, currently shipping millions of hybrid transceivers.

They don't grow InP directly on silicon like $ALMU. Instead, they pre-fabricate InP dies on native substrates and bond them to silicon waveguides using molecular bonding.

It works for low volumes, but structurally fails when AI switches require thousands of integrated lasers per rack.

$AVGO and $MRVL dominate the DSP and switch ASIC layer, aggressively pushing Co-Packaged Optics (CPO) using similar bonded or pluggable architectures.

Then we have the optical I/O players like Ayar Labs. They bypass the integration physics completely by using an external laser source connected via fiber.

They've a massive ecosystem lock-in with $INTC and $NVDA. It gets products to market faster, but it also adds packaging complexity and coupling losses.

Incumbents win on execution/relationships today, while $ALMU wins on fundamental scalability/physics (large-wafer monolithic III-V/Si) for cost/performance at AI volumes (millions of lasers/SOAs).

Imo, the sharpest technical threats to $ALMU are actually private players.

Quintessent is the closest peer. They develop quantum dot lasers and integrate them onto commercial silicon photonics platforms with $TSEM.

They focus heavily on high-reliability AI interconnects and have earlier foundry traction.

$ALMU counters with larger 300 mm wafers, broader monolithic claims (direct growth vs. hetero bonding), in-house control, and diversified revenue (sensing/quantum de-risks).

There is also Ranovus, which is pushing multi-wavelength comb lasers and has strong ties with Cerebras. They lean heavily on hybrid elements for system integration though.

⌁ Last thoughts: why Aeluma

$ALMU has the strongest long-term tech moat (true monolithic on 300 mm wafer leading to unmatched scalability/cost at AI volumes) and a confortable $38.6 M cash runway.

Their large-wafer direct growth approach also works incredibly well for short-wave infrared sensing too, which enables high-volume defense/mobile applications (U.S. gov diversification: NASA quantum, RFSUNY lasers) and a diversified revenue stream.

If they successfully master high-yield, monolithic direct-growth of InGaAs/InP on 300mm silicon at scale, the industry will be forced to license their IP or adopt their wafers.

PS: I'll talk about $POET in a dedicated post

7

661

$LASR ⌁ Why is nLIGHT exceptional DD drop 🔖🛸

$LASR's edge comes from its vertically integrated coherent beam combination architecture.

It runs from proprietary high-brightness semiconductor chips through fiber amplifiers all the way to complete beam-combined high-energy laser systems, all built in the US.

That stack delivers native scalability plus built-in adaptive optics for real-time atmospheric correction.

No other fiber-laser supplier matches this exact combination at scale.

Their CBC systems already reached 300kW-class output in 2023 and sit on a clear roadmap to 1-MW class by 2026.

Right now they ship 10kW, 30kW and 50kW units, with 50kW systems heading into Stryker vehicles this year and a new 70kW laser weapon system rolling out in 2026.

The result is sustained brightness and power that exceed DoD HELSI targets while preserving beam quality. Competitors simply don't deliver at equivalent size and power.

⌁ Capabilities that open impossible markets

This tech unlocks compact, vehicle-mobile directed-energy weapons with unlimited magazines and speed-of-light engagement against drone swarms, rockets, artillery and hypersonics.

The Stryker-integrated 50kW system gives maneuver forces layered air defense at roughly $10 per shot versus millions for a Patriot round.

Earlier chemical lasers were too toxic and bulky for mobile use; early solid-state designs lacked the brightness to stay lethal through turbulence at range.

Coherent beam combination phase-locks multiple fiber amplifiers, and the adaptive optics layer then corrects real-time phase distortions so lethal fluence lands kilometers away.

That combination was physically out of reach before.

⌁ Some closing thoughts

The architecture directly solves the cost-exchange problem we see playing out with proliferating cheap drones.

$LASR already holds proven prototypes, doubled its US manufacturing footprint this year, and secured multi-hundred-million dollars DoD contracts.

With one of the only fully domestic high-power supply chains and the only kW-to-MW scaling path on track for 2026, the flywheel is turning.

Demand compounds across ground, naval, air and space platforms because the physics now works at tactical scales where it never could.

5

390

If I hadn't already built my core position in $IONQ back at ~$8, I'd definitely be tempted to initiate a starter position here around $28 (~$10B market cap).

5

1

30

3,212

The state of $ASML's EUV machines right now 🔖🛸

The TWINSCAN EXE:5200B High-NA and NXE:3800E Low-NA platforms, priced at ~ $350-400 million each, are the only production tools on the planet capable of patterning the critical layers for sub-2 nm logic nodes and leading-edge DRAM.

$INTC has completed acceptance testing and installed the first commercial EXE:5200B units for its 14A (≈1.4 nm) process, with high-volume manufacturing ramp targeted for 2026–2027.

$TSM, Samsung, and SK hynix are in various stages of evaluation or early deployment, with $ASML scheduling 10 High-NA and 56 Low-NA shipments for 2027.

Low-NA NXE systems (0.33 NA) continue to dominate 2 nm and 3 nm production at $TSM and others, but High-NA is the irreversible next step.

$ASML's current stack took 25 years and over €6 billion to master btw.

From public information, Chinese prototypes sit orders of magnitude behind on power and yield.

The MOAT is wild.

$ASML ⌁ NOBODY CAN REPLICATE THIS STACK RIGHT NOW dd drop 🛸🔖

$ASML's state-of-the-art EUV systems are the TWINSCAN EXE:5200B (High-NA) and NXE:3800E (Low-NA) platforms.

The physics foundation is identical across both families and rests on 3 non-negotiable pillars that no other wavelength or technology can replicate at scale today.

⌁ First, EUV photons are generated using laser-produced plasma (LPP) at a wavelength of 13.5 nm.

Molten tin droplets (≈25 μm diameter, traveling at 70 m/s) are injected into the source chamber 50 000 times per second.

A pre-pulse laser flattens each droplet into a thin disk.

Then, a main CO₂ laser pulse (10.6 μm wavelength, tens of kilowatts peak power) vaporizes and ionizes the tin, creating a plasma with electron temperatures of tens of eV.

The EUV emission arises from 4d–4f electronic transitions in highly ionized Sn atoms/ions; the spectrum peaks sharply at 13.5 nm, the spot where tin conversion efficiency, mirror reflectivity, and minimal absorption all peak.

They're demonstrating 1000 watts at intermediate focus, running 500-600 watts in production today.

Every lost watt caps wafers per hour.

⌁ Second, the entire optical column is vacuum and mirrors only.

EUV photons are absorbed within nanometers by any material, air, glass, quartz, even thin films. Transmission optics are impossible.

Every surface in the illuminator and projection optics is a Mo/Si multilayer mirror engineered for Bragg reflection at 13.5 nm incidence angles.

Reflectivity compounds multiplicatively; 10-12 mirrors in the optical column reduce transmission to a few percent, which is why source power scaling is existential.

In High-NA (0.55 vs Low-NA 0.33), the optics become anamorphic: 4x reduction in the scanning (Y) direction but 8x in the cross-scan (X) direction.

This keeps incidence angles on the reticle below the critical grazing angle where multilayer reflectivity collapses.

⌁ Third, resolution is locked by the Rayleigh criterion.

The printable critical dimension CD equals roughly k1 x lambda/NA, with lambda is fixed at 13.5 nm.

Low-NA at 0.33 gives 13 nm features.

High-NA at 0.55 drops it to 8 nm.

High-NA therefore eliminates one or more multi-patterning steps for sub-2 nm layers, slashing cycle time, defects, and cost.

⌁ Last thoughts

No competitor can replicate this stack.

The plasma source, multilayer optics, and vacuum mechatronics required >25 years and €6 billion in R&D; Chinese attempts remain prototypes with orders-of-magnitude lower power and yield.

Physics dictates that any alternative wavelength (e.g., 6.7 nm) demands entirely new plasma materials, mirrors, and lasers. It'd lead to another decade-plus effort with no guarantee of higher efficiency.

5

453

16 Sep 2024

Tell em that quantum is coming.

2

7

1,076

77

$FSLR took a MASSIVE step forward 💥

The non-exclusive perovskite patent licensing deal with Oxford PV is a major derisking of the single most important long-term technology vector for the company.

Instead of defending a static CdTe position against ever-cheaper commoditized silicon…

$FSLR now has a clear runway to keep innovating its platform: pushing efficiency higher, costs lower, and staying ahead of the curve for decades.

🛸👽

3

195

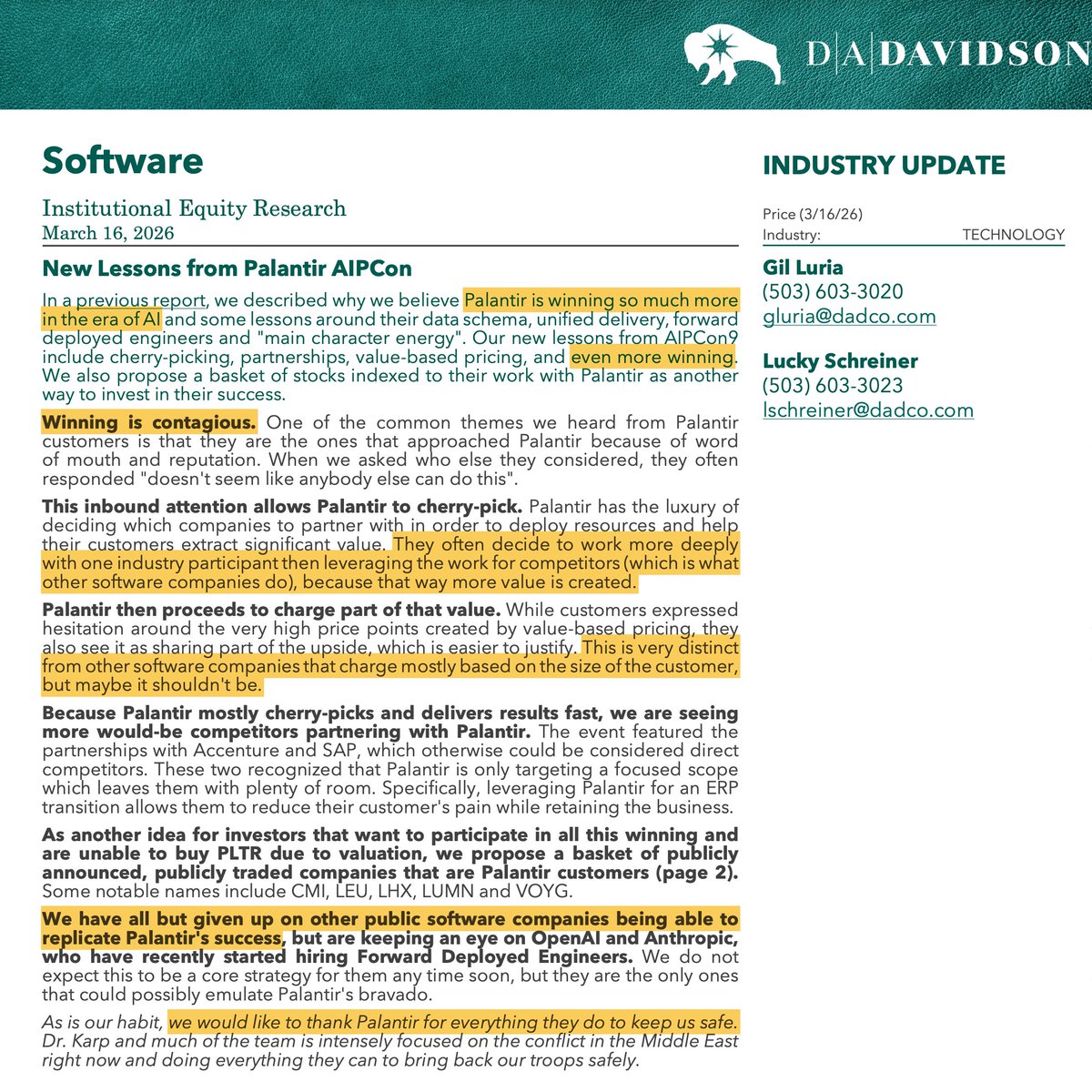

Palantir's proprietary stack (Gotham, Apollo, Foundry, AIP) has still no direct one-for-one replacements at scale, far from that.

That's why they've secured critically important relationships over the years and embedded their software so deeply into client workflows.

Now, knowledge compounds ⵉˣᵖᵒⁿᵉⁿᵗⁱᵃˡˡʸ through forward-deployed engineers (FDEs) and AI FDEs.

Nobody can compete..

$PLTR

1

89

The very top of the AI tsunami is now visible on the horizon.

By the time half of it comes into view, in hindsight, any market correction will look like a massive buying opportunity.

1

118

The aspect of $IONQ that most people, including many investors, overlook is its quantum networking business.

A massive moat is being built here.

$IONQ is aggressively building the quantum internet stack with key breakthroughs and moves:

⌁ Achieved a major milestone in quantum frequency conversion, shifting photons from visible (trapped-ion compatible) to telecom wavelengths.

This enables long-distance quantum links over existing fiber optics infrastructure, a critical step for scalable quantum networks.

⌁ Bolstered capabilities via strategic acquisitions, including:

Qubitekk (completed early 2025), which added core quantum networking patents and infrastructure tech.

Lightsynq (completed June 2025) brought photonic interconnects and quantum memory expertise to speed up both computing and long-haul networking.

Super-majority stake in ID Quantique (completed May 2025), a global leader in quantum-safe networking, QKD systems, and secure comms.

Skyloom (announced Nov 2025, completed Jan 2026) which brings lightwave-optics for free-space optical comms, enabling distributed entanglement and ultra-secure space/ground links.

⌁ Delivered real-world deployments, like the Geneva Quantum Network (GQN), Switzerland's first citywide dedicated quantum network (launched Nov 2025), connecting research, enterprise, and government sites with hundreds of km of fiber using IDQ's QKD tech.

$IONQ now owns all critical layers for scalable quantum networking, including in space.

It's THE full-stack leader in quantum-secure communications.

1

2

33

2,493

I bought more $INFQ when I heard Matthew Kinsella say this:

"I spend a lot of my time thinking about how Infleqtion could fail...

Only the paranoids survive!"

It clicked instantly.

1

28

1,936

$OKLO's Aurora fast fission reactor can interchangeably use:

⌁ Fresh HALEU (from DOE-managed or enriched sources).

⌁ Recovered HALEU.

⌁ Surplus plutonium (as a "bridge" fuel; criticality experiments completed in 2025 at Nevada national security site with LANL validation).

⌁ Recycled transuranic-bearing materials from used fuel.

This versatility attacks the single biggest chokepoint in advanced nuclear scaling: fuel availability and sovereignty.

2

1

221