Investing since 2018 / Berlin & Aalborg / happy to connect // Tweets reflect my personal opinions and are not investment advice. Do you own due diligence.

Joined June 2022

- Tweets 1,351

- Following 664

- Followers 1,870

- Likes 4,266

35 Photos and videos

Pinned Tweet

Feb 2

I am very happy and honored to share that I will be joining @Symmetry_Invest as an Investment Analyst, starting in March.

I would also like to sincerely thank everyone who supported me throughout my job search. I truly appreciate the advice, encouragement and trust along the way

9

79

6,091

Isaac retweeted

Jun 6

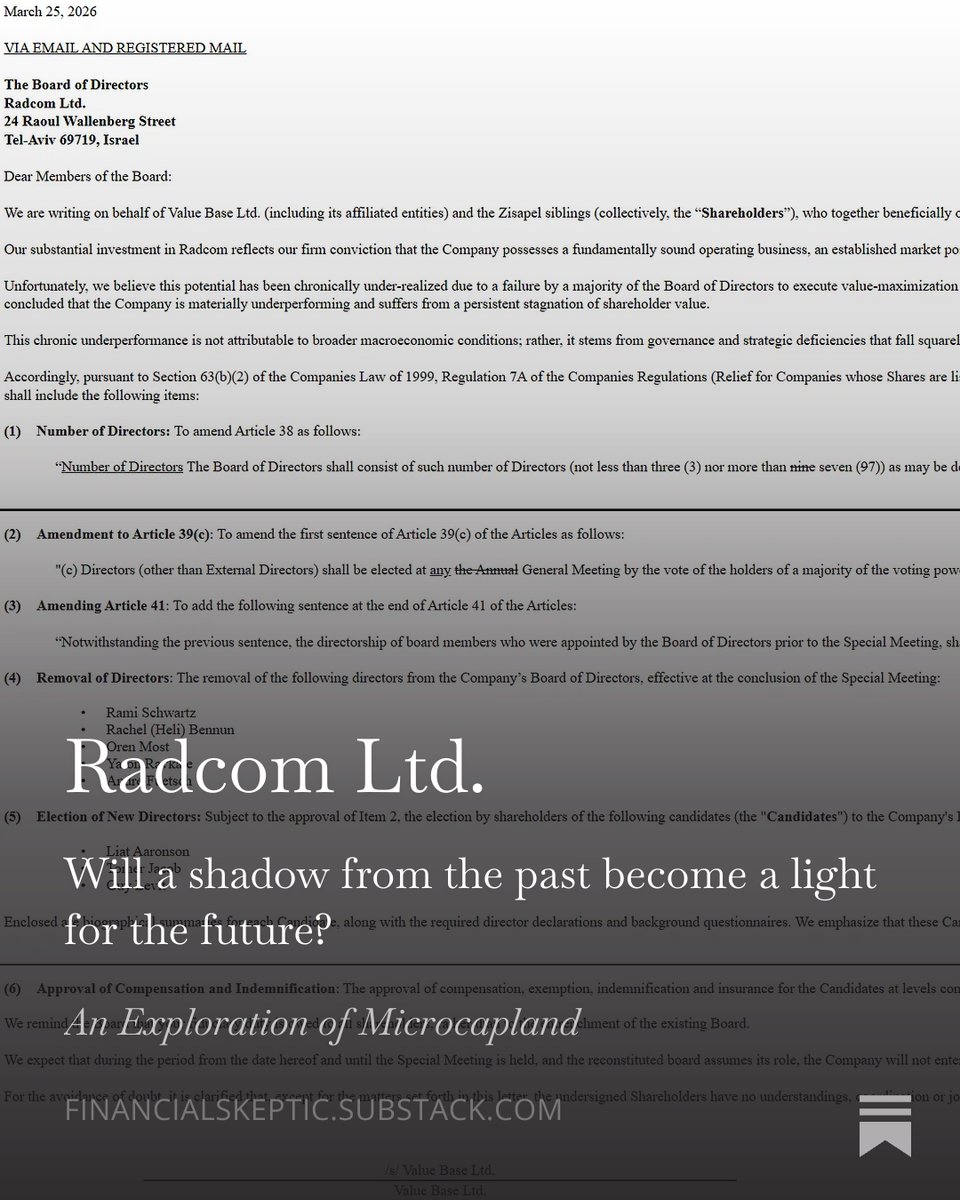

I see a lot of discussions on what's going on with $RDCM after the wild ride, so here's my take.

Radcom is a small Israeli software company that most people have never heard of. It quietly runs in the background of phone networks, helping carriers catch and fix problems before your calls ever drop. Boring, sticky, mission-critical. This is exactly the kind of infrastructure business that I like.

A couple of weeks ago, a big account on X mentioned it, the crowd piled in, and the stock shot up to ~$17. Then that same crowd got bored, wandered off, and it slid right back to ~$12. But had anything really broken?

I went digging through the actual SEC filings, and there was nothing there. No bad news, no cut to guidance, no insiders heading for the exits. It was just hype inflating and then deflating. The business itself didn't change at all.

Here's what makes it genuinely interesting once you look past the noise. Radcom is sitting on about $108M of cash with zero debt. That's roughly $6.35 a share — call it half the entire share price, just parked in the bank. Strip that cash out and you're paying almost nothing for a company that's profitable and still growing. For years, that pile sat there doing nothing, which is a big reason the stock stayed so cheap.

What changed is the part that matters: activist investors just took control of the board. These are people who want that cash actually put to work — a buyback, a special dividend, or, most interesting of all, selling the whole company. Businesses like this rarely come up, and the few that have sold went for rich prices. I see a material upside from here, and that giant cash cushion limits the downside while we wait.

It's not free money, of course. The company leans heavily on a handful of big customers (one is about half of sales), and there's always the risk the new board blows the cash on a bad acquisition instead of handing it back.

Net: I own a little, and I'd add on a weakness like this.

Huge credit to @FinSkeptic, whose work on Radcom is the best out there — if this interests you, go read him first.

Not investment advice, just me thinking out loud. I own shares and may buy more or sell the position without any warning. Do your own work.

1

3

18

1,403

Isaac retweeted

Jun 7

Buffett ran his first partnership at 26.

Ackman launched Gotham at 26.

At 19, today I get my chance to start.

I have joined Sapphire Capital EAF as Fund Advisor of PEQUITY U&U Global Opportunities, FIL. The strategy I have been writing about on Undervalued and Undercovered for years now has real money behind it.

49

26

923

622,551

Isaac retweeted

Jun 4

I have just published a post on the newsletter website. I would like to point out that, as always, I am merely explaining the reasons behind my own investment decision. This is not investment advice, and everyone should always do their own research. $SEN.AX

1

7

18

3,845

Isaac retweeted

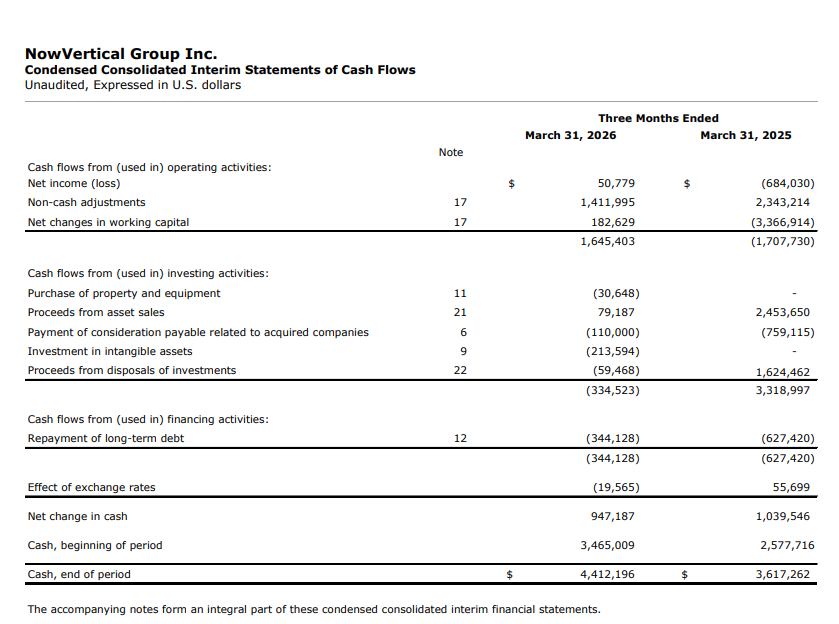

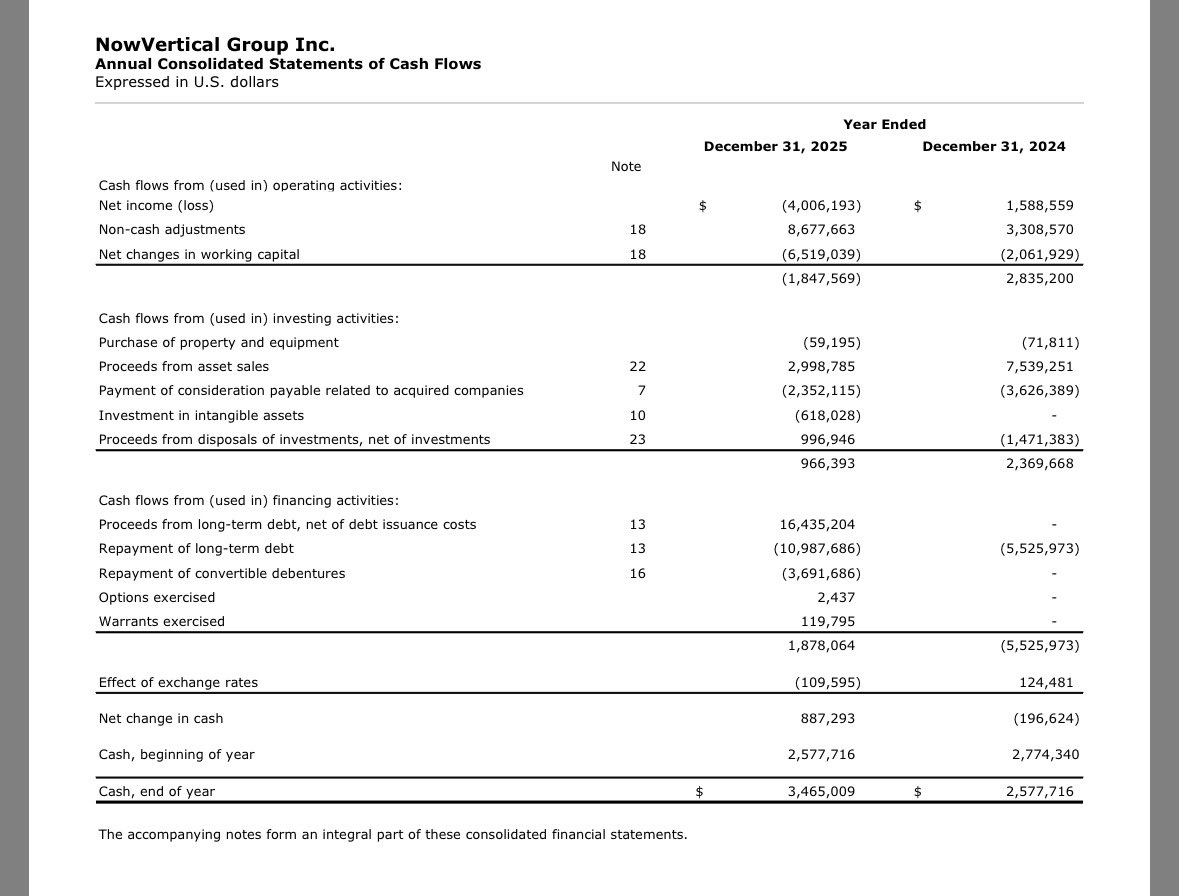

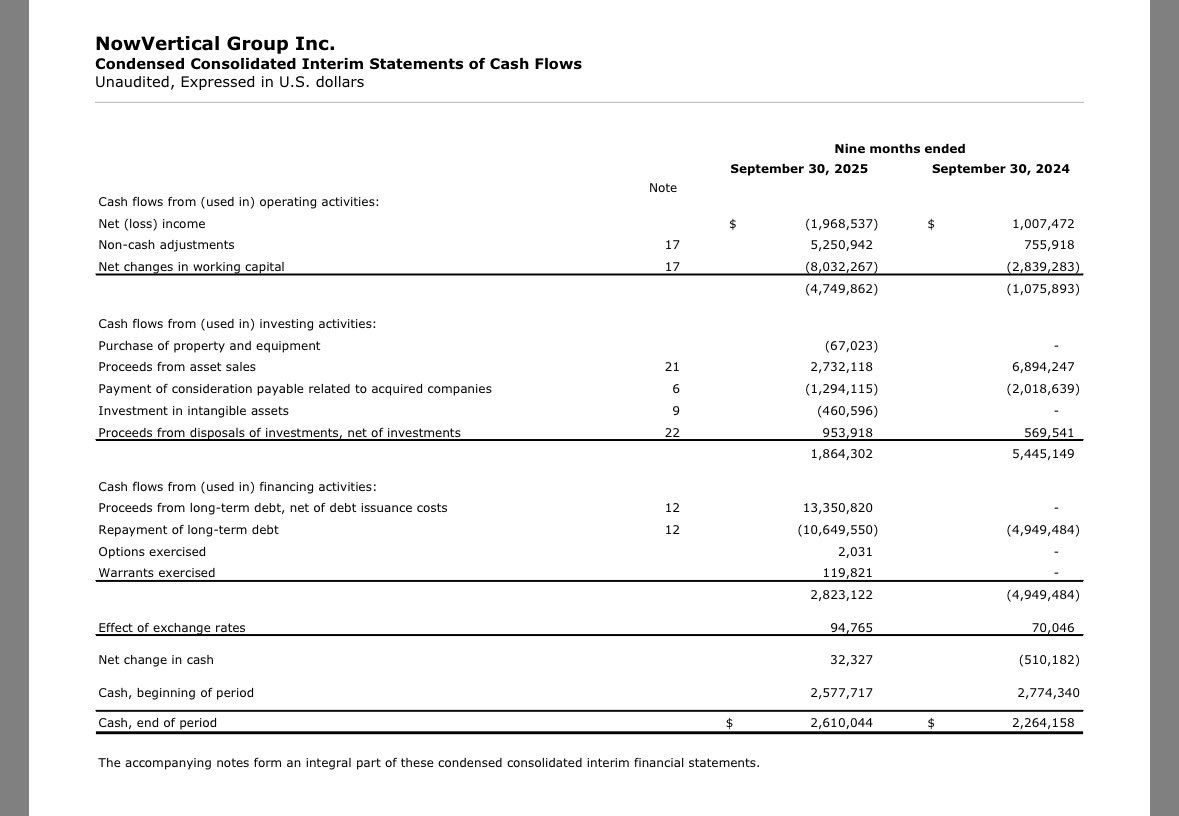

$NOW.V Headline results are as expected, offering neither a positive nor a negative surprise. However, they generated strong positive cash flow, even when adjusting for changes in working capital.

3

2

30

4,508

Isaac retweeted

$RDCM Final confirmation that everything went as planned from an activist perspective. New directors filed their Form 4s. Activists now control the board.

app.tracktacle.com/publicati…

3

19

4,832

Isaac retweeted

May 16

$RDCM holders, get your votes in for the proxy fight.

Lynrock will vote its full ~19% record-date stake, even though they've trimmed their economic position.

Record-date holdings, not current holdings, are what count at the meeting.

1

1

8

1,904

Isaac retweeted

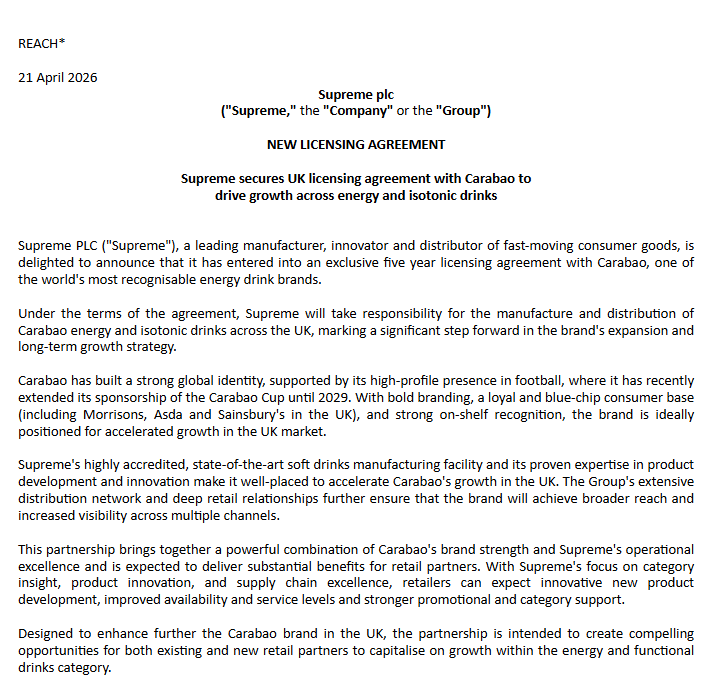

#SUP @SupremePLC new licensing agreement

With Tonino Lamborghini to develop, manuf & distribute prem energy drink range (6 SKU's) across UK/Euro/ME & China

Will expand SUP beverage category presence & capitalise on Tonino Lamborghini's luxury lifestyle brand appeal

3

9

2,351

Isaac retweeted

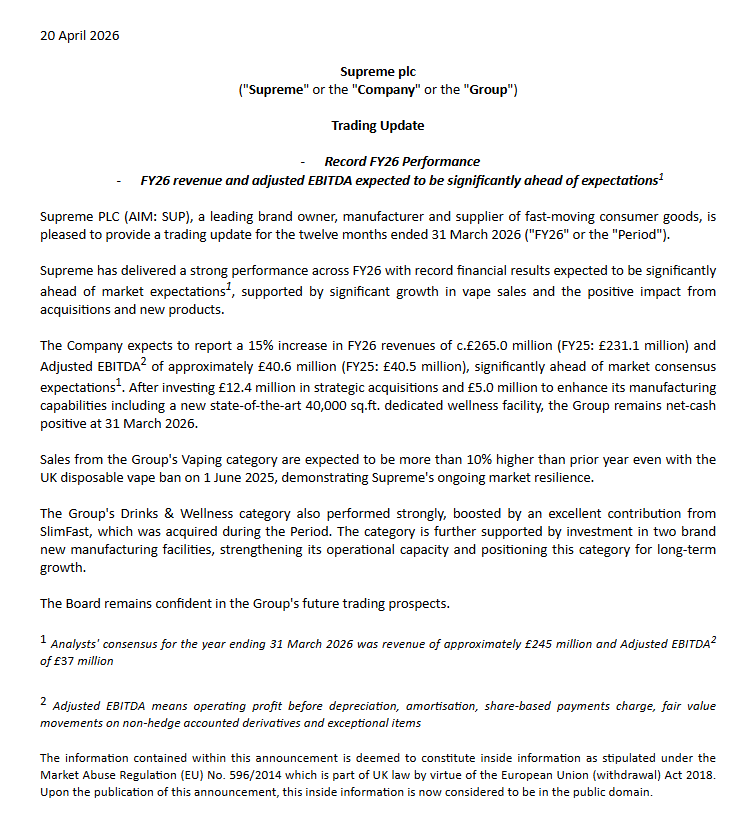

Apr 21

$SUP.L #SUP Supreme plc, solid 48 hours of updates:

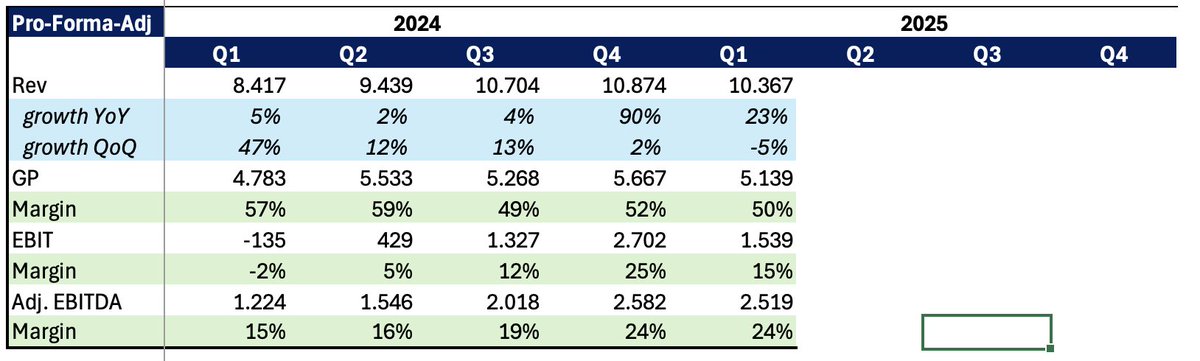

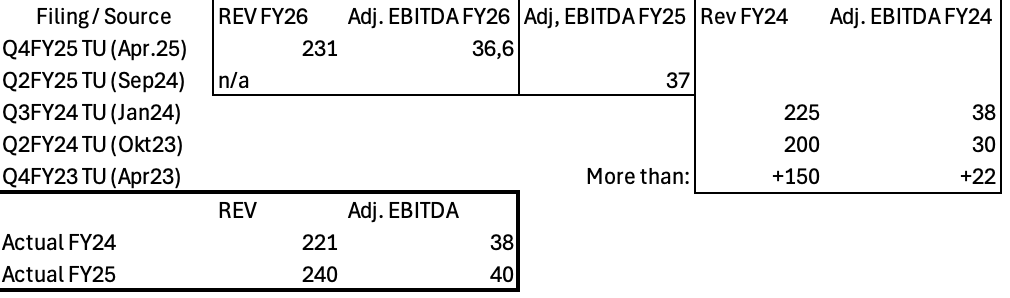

1. FY'26 TU: Revenue 15% (YoY), adj. EBITDA in 40.6m (flat vs 2025), ahead of consensus. Net cash positive, vaping sales 10%

2. Exclusive 5-year licensing deal in UK with Carabao for energy drinks, leveraging soft drinks plant

4

25

4,425

Isaac retweeted

Apr 20

#SUP

In a crisis riddled world marked by wars from Ukraine to the Middle East – one would expect consumer demand to wobble. Yet across the UK’s FMCG, drinks, wellness and vaping markets, consumption remains remarkably resilient. Why? Because these are everyday, affordable products -small-ticket essentials and “feel-good” purchases that people continue to enjoy.

Enter @SupremePLC , an entrepreneurial group that’s quietly building one of the UK’s most diversified and agile FMCG platforms. By assembling a stable of high-performing brands - ranging from Typhoo Tea and Clearly Drinks to Sci-MX and SlimFast, alongside its heritage vaping arm. Crucially, that pivot towards Drinks & Wellness is not just defensive - it’s tapping into powerful structural growth trends around health, hydration and nutrition.

And today’s FY26 trading update shows that strategy is working.

@SupremePLC delivered a standout performance for the year to March, with revenues jumping 15% to £265m and EBITDA hitting £40.6m, comfortably ahead of expectations . This is no small feat given the well-publicised disruption from the UK’s disposable vape ban. Yet impressively, vaping sales still grew more than 10% year-on-year, underlining management’s successful transition to alternative formats.

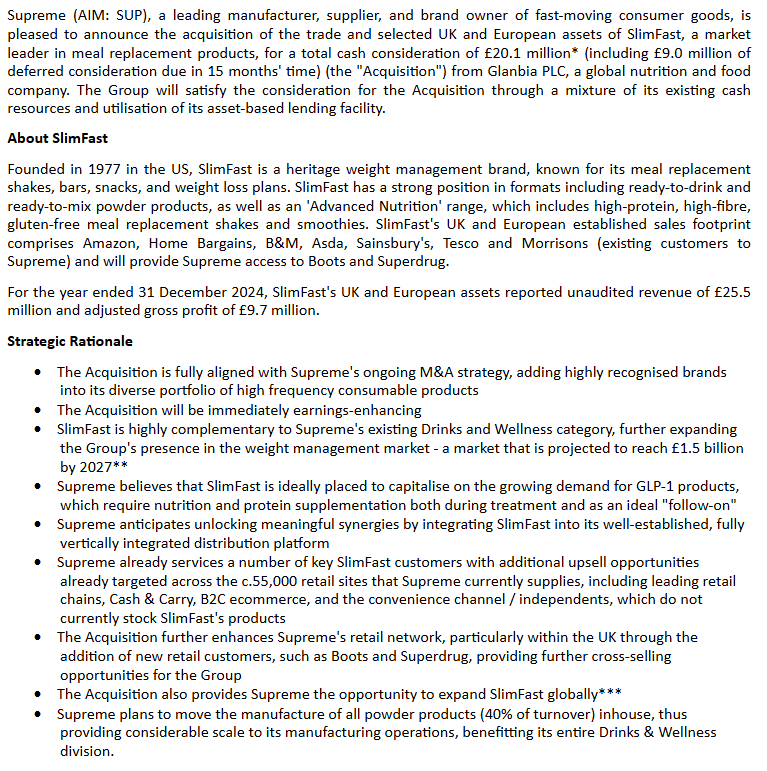

Elsewhere, the £20.1m acquisition of SlimFast in Oct’25 has already made an “excellent” contribution, while ongoing investment in manufacturing, including a new 40,000 sq.ft wellness facility, positions the division for sustained expansion. Combined with a vertically integrated model and access to 55,000 retail outlets, Supreme has built a powerful engine for cross-selling and margin enhancement.

CEO @sandykik / Sandy Chadha commenting: the group has delivered “record financial results… significantly ahead of expectations,” supported by acquisitions, new products and strong underlying trading.

Looking forward, @ShoreCapital has upgraded FY26 expectations to £265m revenue and £40.6m EBITDA, with FY27 revenues climbing further to £295m. Moreover, the shares trade on attractive 7.2x FY26 PER and 4.0x EV/EBITDA multiples, alongside offering a 3.4% dividend yield with net cash (est £3.1m). FY27 multiples remain modest too at 7.6x PER and 4.0x EV/EBITDA, suggesting the market is yet to fully price in the group’s diversification and earnings power.

Sure there’s a new UK vaping tax being introduced from Oct’26 onwards. Yet equally Supreme looks like a business leveraging its scale, channel strength, FMCG brands and product diversification to deliver growth in even the toughest of backdrops.

Disclosure: @SupremePLC is a @VOXmarkets client.

3

16

1,905

Isaac retweeted

Anybody on fintwit looking to hire? Anybody on fintwit looking to be hired? Send me a dm.

About to launch a little project to give back to the community: fintwitjobs.

Would appreciate a RT for visibility!

5

46

192

96,647

Isaac retweeted

Apr 17

Symmetry is happy to share our 2025 annual letter

Danish: symmetry.dk/wp-content/uploa…

English: symmetry.dk/wp-content/uploa…

2

3

50

8,396

Isaac retweeted

Apr 12

Our annual letter is to be distributed within the next 1-2 weeks. If you want it directly in your mail-box: sign up here:

symmetry.dk/nyhedsbrev/

1

12

2,641

Isaac retweeted

Apr 10

$NOW.V

Updated again after the stock price fell 15% yesterday. Based on Q4 (~annualized)

Bear ($3.5 Mio. FCF)

Market cap / FCF: ~4.5x

EV / FCF: ~8.3x

Base ($5.0 Mio. FCF)

Market cap / FCF: ~3.2x

EV / FCF: ~5.9x

Bull ($6.5 Mio. FCF)

Market cap / FCF: ~2.4x

EV / FCF: ~4.5x

Bear Case: FCF $3.5 Mio. Market cap / FCF: ~5.2x EV / FCF: ~9.0x

Base Case: FCF $5.0 Mio. Market cap / FCF: ~3.7x EV / FCF: ~6.3x

Bull Case: FCF $6.5 Mio. Market cap / FCF: ~2.8x EV / FCF: ~4.9x

2

16

2,700

Isaac retweeted

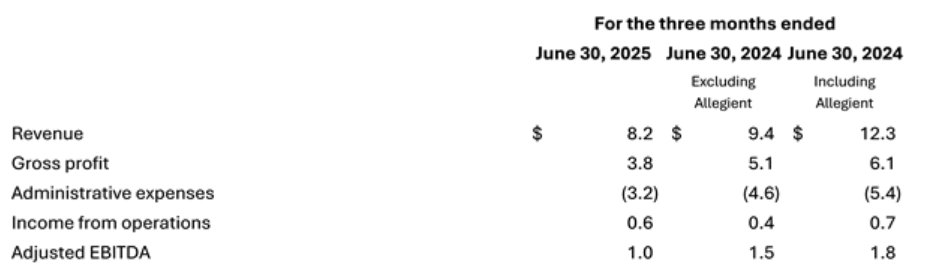

$NOW.V If I am not mistaken, we have $3m in operating cash flow in Q4 and $1.4m excluding changes in working capital, which confirms what management said about cash outflows. The remainder of the results is mediocre.

4

3

30

7,816

Isaac retweeted

Thread on Berkshire’s acquisition record…

I’ve always been fascinated by $BRK acquisitions of entire companies, mostly because it’s a lot harder to judge performance than it is for stock market investments. It’s a lot easier to do a case study on Berkshire’s purchases of Coke, Gillette, Washington Post, AmEx, etc. because most everything you need to determine returns valuations are public.

Some years ago I started trying to analyze Berkshire’s wholly owned acquisitions for lessons learned by doing rough estimates on deal prices, revenue, PTI at acquisition (a lot of this information is actually public), estimating financials today (which by reconciling segment information in the annual report, I think is possible to come out with pretty reasonable estimate) and coming up with some rough number for how much of net income over the years was distributed back up to Berkshire – you can actually come up with some very realistic and fairly precise estimates for modified IRR, essentially the same annualized return they’d get had these been public company investments.

Thought I’d share a few of the things I’ve noticed and collected. This is probably a strange thread, but I really don’t promote anything, don’t have a Substack and thought at least some people would find this fascinating. I’ll just emphasize for the record something that’s obvious – I think these numbers are directionally pretty correct, but they are just my estimates and don’t want to make the mistake of implying any false precision.

20

57

321

70,329

Isaac retweeted

Apr 1

I have just published a post on the newsletter website. I would like to point out that I am, as always, merely explaining the reasons behind my own investment decision. This is not investment advice, and everyone should always do their own research.

Radcom $RDCM provides telecommunications network operators with cloud-native software for 5G network intelligence and service assurance.

The company has a great business, but it lacks a shareholder-friendly capital allocation strategy. An activist group wants to change this, and in my view, there is a good chance that they will achieve their goals. Given the moderate valuation, I found the situation very interesting.

2

9

40

9,783

Isaac retweeted

Mar 11

What are your favorite companies with a market cap under $500m—and why do you think they’ll outperform?

13

3

17

7,194

Isaac retweeted

13

12

152

33,621

Isaac retweeted

4

2

64

32,017