Joined December 2017

- Tweets 1,959

- Following 431

- Followers 32,326

- Likes 3,926

421 Photos and videos

I wonder what milestones and contracts these will unlock even before beta service starts.

The market seems to believes there will be plenty of time to play $SPCX and then get back into $ASTS by the time they get more sats up.

Meanwhile short borrow availability is near zero.

Encapsulation complete.

BlueBirds 8, 9, and 10 are now secured inside Falcon 9's fairing ahead of launch.

A stacked configuration powered by advanced carbon fiber structures, engineered to withstand ascent forces comparable to carrying a fully loaded space shuttle orbiter during launch. 💪

Next stop: launch. 🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀

Built in Texas. Broadband from space. Designed to connect directly to everyday smartphones. 🌎📶📱

#ASTSpaceMobile #Broadband #ConnectingtheUnconnected #BlueBirds

2

1

44

6,238

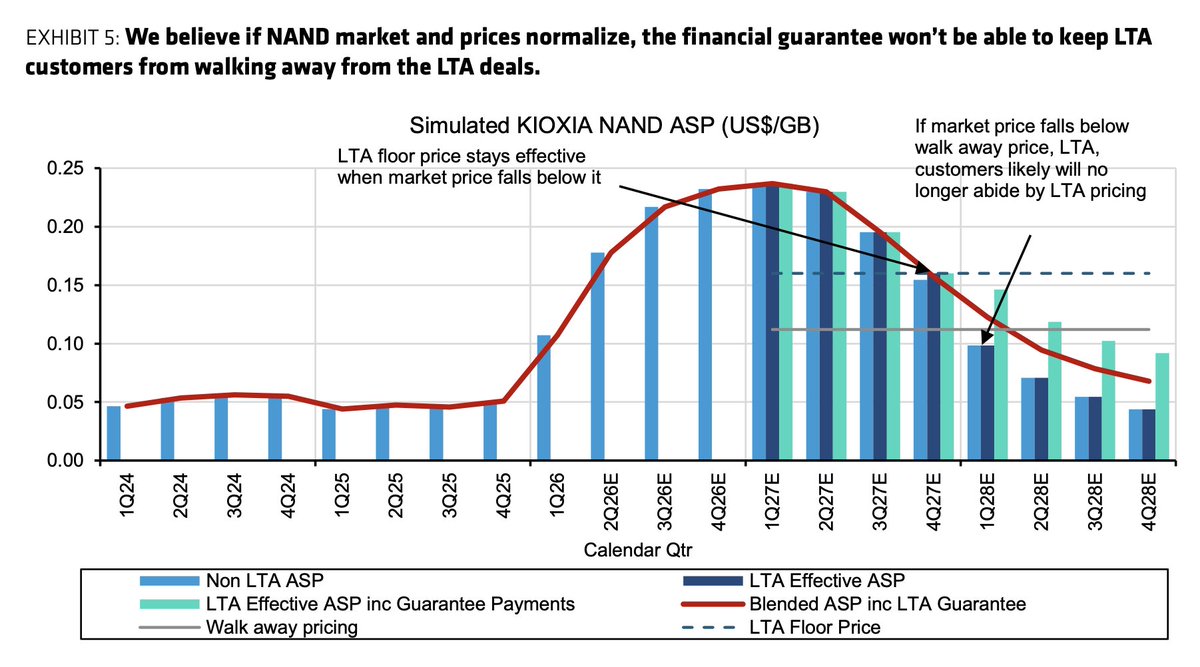

Bernstein is the most bearish major shop on Kioxia 285A $KXIAY and this was actually a 135% raise in one go from ¥17,000 to ¥40,000.

Their issue is that super high margins might not last past 2028 (the cyclical argument again).

I am ok with the party lasting until 2028 😏

8h

Bernstein issues underperform rating on Kioxia ($285A):

Price target set to ¥40,000 , implying greater than 50% downside risk. The firm acknowledges that near-term momentum remains strong, with NAND pricing still rising, earnings growth expected to remain material, and the stock continuing to benefit from the broader AI-driven memory shortage. However, Bernstein’s core concern is that the market is capitalizing peak-cycle earnings as though they represent a sustainable long-term earnings base.

The report argues that NAND pricing is likely to peak in CY2027 and normalize into CY2028 as supply additions begin to catch up with demand. Bernstein’s SOTP framework treats the current earnings surge as a temporary windfall rather than a repeatable margin structure, assigning value to excess cash generation through CY2028 but applying normalized multiples to longer-term earnings. Under that framework, the firm estimates fair value at roughly ¥40,000 per share, implying approximately 50% downside from the current share price.

A key focus of the report is whether long-term agreements can reduce cyclicality in NAND earnings. Bernstein concludes that LTAs and financial guarantees may improve trough profitability but are unlikely to prevent meaningful earnings volatility. If spot prices fall sufficiently below LTA floor prices, customers may be economically incentivized to walk away from agreements and forfeit guarantees. Bernstein estimates that the current stock price would require either a 65% normalized gross margin, an 80% financial guarantee on LTA value, or a shortage lasting until CY2032, none of which it views as realistic.

The broader structural concern is China. Bernstein argues that aggressive NAND price increases could give YMTC and other Chinese suppliers greater room to scale, potentially allowing YMTC to become the third-largest NAND supplier by CY2028. The implication is not that memory fundamentals are weak near term, but rather that current profitability may be too high to sustain without attracting new supply and customer substitution.

3

19

5,776

10h

Lots of frustration & absorption this morning in $ASTS and $RKLB. Wonder if this is the last of the tourists rage quitting into $SPCX. The sell algo may get shut off soon, esp with $RKLB's Nas-100 inclusion.

Just speculation, but I added some juice at $ASTS $85 and $RKLB $107.

Jun 12

11

3

153

21,956

10h

The Anthropic/Mythos drama had me thinking about model-agnostic platforms: not over-relying on any one lab, having a neutral third party with deep AI expertise on your side. Led me to buy a chunk of $PLTR this AM.

$128 has held well. Easier to size up big when risk is defined.

8

58

9,494

19h

One less concern for $IQE with the China InP supply news.

The Tower Semi deal also helps with the others.

Jun 11

Appreciate the writeup. Funny timing, was deep in $IQE overnight myself. Few things I'd pick your brain on if you have a minute.

The LandMark comp is the one I keep chewing on. Same layer, wildly different economics. LandMark runs epi as a high margin business while IQE does ~3% adjusted EBITDA. Why do you think the gap is that wide? Customer mix, utilization, fab footprint? Genuinely asking, because "same layer, 15x cheaper" only works if the margin gap is fixable. Why the hell is it so wide?

The sale process is a head scratcher too. In January the board was negotiating non-binding offers for the whole group plus separate asset bids. The outcome was the review ended, takeover talks dead, dilutive raise at 19.8p? So everyone who saw the inside numbers either walked or bid below what the board would take near 20p? Stock now sits at 39.7p, 2x where the process died and where MACOM and insiders were willing to fund it. What was that about?

Balance sheet isn't fully clean either. There's a new £15M secured convertible at 19.8p, and MACOM holds warrants over another ~76M shares that only kick in if IQE redeems the notes early. Either path it's ~76M shares of overhang struck at half the current price.

Also some of the FY25 photonics strength was defence funding pulled forward from '26, per their own January update. Makes the >20% FY26 guide a tougher comp than it looks on the surface.

And the guide itself is H2 weighted, but there are InP supply constraints and "fixed cost pressure" flagged as risks in their own release. The InP supply contraints in particular are concerning. Might jam them up.

4

1

27

8,679

Jun 15

Kioxia 285A now up 30%.

With $SNDK at $2,060 (9.5x annualized sales), Kioxia would need another 40% from here to trade at the same price-to-sales. Same wafers, same JV fabs.

And that's assuming $SNDK doesn't run further (good luck with that).

Nasdaq up-listing also coming.

Jun 11

Sized up Kioxia 285A $KXIAY a good bit during this past week.

$SNDK continues to be a freight-train. The full NAND/HBF/CXL thesis hasn't even kicked in yet. Kioxia is where I've been adding as a better relative value. Held strong this past week while everything else got punched in the face.

Same NAND, same JV fabs. One trades in Tokyo at ~8-11x earnings, one on Nasdaq at ~14-16x. The gap likely starts to close with the upcoming up-listing.

The gap:

Valuation (annualizing each company's OWN current-quarter guidance)

• Kioxia ¥75,500: 10.6x run-rate EPS, 5.7x sales, $250B cap

• SNDK $1,880: 14-16x run-rate EPS, 8.7x sales, $278B cap

• Kioxia on FY3/27 consensus EPS: 8.4x

Upside to analyst targets

• Kioxia: 14% to consensus (¥86,250), 23% to Goldman (¥93k), 165% to street high (¥200k)

• SNDK: roughly at consensus ($1,751), 73% to street high ($3,250)

Manufacturing control

• Kioxia owns 51% of Flash Ventures, the JV that makes BOTH companies' NAND

• SNDK's wafer supply runs through fabs Kioxia controls

• Same wafers, ~30% cheaper per earnings dollar via Tokyo (for now)

Earnings power (company guidance, not estimates)

• Kioxia Q1 guide: ¥1.3T op profit at a 74% OP margin, ROIC >60%

• Kioxia FY3/26 actuals: OP margin 37.2% (up from 26.5%), ROE 51.9%, ¥470B cash vs ¥203B short-term debt

• SNDK Q4 guide: $7.75-8.25B revenue, $30-33 non-GAAP EPS for the quarter

HBF and the AI storage stack

• SNDK originated HBF, MOU with SK Hynix

• Kioxia already demo'd a 5TB / 64GB/s HBF prototype and co-manufactures through the same JV

• Kioxia is also co-developing GPU-adjacent SSDs with Nvidia aimed at partially offloading HBM, plus a 10M IOPS AI SSD sampling 2H26

• If HBF works, both win on the same wafers but one trades at a relative discount.

Catalysts

• Kioxia: Q1 print Aug 7 (guide already public), OTC ADR uplisting to a major US exchange in preparation (F-6 on file with the SEC), first dividend FY27 plus up to 50% of net cash flow in shareholder returns, BiCS10 mass production targeted within 12 months

• SNDK: fiscal Q4 print ~Aug, HBF samples 2H26

The bear case on the discount: float is still constrained, Toshiba is the largest holder (~22% as of Nov '25), and Bain's remaining stake. That supply is the overhang. The uplisting helps the access problem directly.

Both work if NAND stays tight through 2027, which is Kioxia's own stated view. One is just cheaper.

Run-rate = annualized current-quarter guidance, not a full-year forecast. 1 $KXIAY ADR = 1/10 of a Tokyo share. Not investment advice, verify everything yourself.

9

3

181

63,504

Jun 12

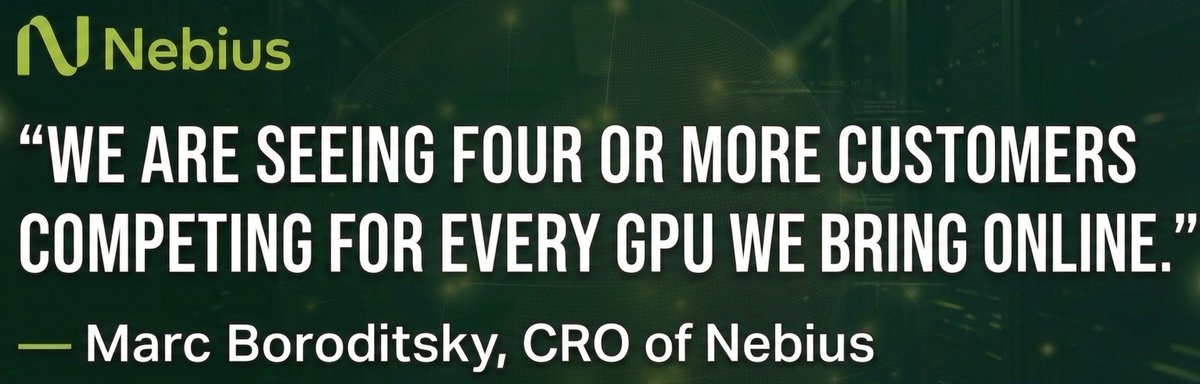

One of the more underappreciated parts of the $NBIS hyperscaler thesis. This ability to disaggregate tasks also sets the foundation to being hardware agnostic.

The guys who design their own racks can integrate whatever comes next: $NVDA GPUs/CPUs, $AMD CPUs, $GOOG TPUs, etc.

Jun 12

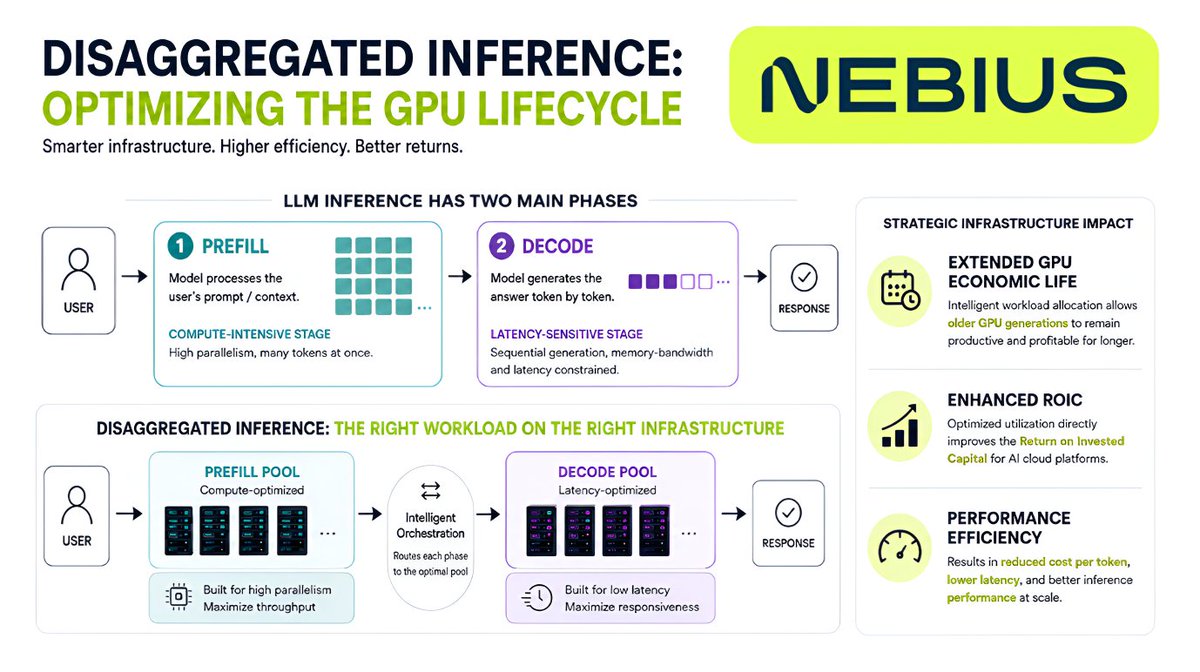

I’m writing a full piece about my insights from Nebius Inflection, but one topic I found particularly interesting was disaggregated inference.

$NBIS is already planning for it as a way to extend the useful life of GPUs.

Let me put it simply...

LLM inference has two main phases:

Prefill, when the model processes the user’s prompt/context.

Decode, when the model generates the answer token by token.

The important point is that these two phases stress infrastructure differently.

Prefill is more compute-intensive and benefits from processing many tokens in parallel, while decode is more latency-sensitive and often more memory-bandwidth constrained.

Disaggregated inference separates these workloads, allowing different infrastructure pools to be optimized for each stage.

Why does this matter?

Because it can improve GPU utilization, reduce cost per token, lower latency, and make inference more efficient at scale.

All of this can also help extend each GPU’s economic useful life.

Same old story...

As new GPU generations come out, older GPUs may become less attractive for cutting-edge training. But that doesn’t mean they become useless.

If $NBIS can intelligently allocate different parts of inference workloads across different types of hardware, older GPUs can remain productive for longer.

That has direct implications for ROIC.

In my view, this is exactly the kind of infrastructure-level optimization that separates a serious AI cloud platform from a simple GPU capacity reseller.

As I’ve been saying since the beginning, building a sustainable AI cloud isn’t just about plugging GPUs into electricity, and this is a good example of that.

$NBIS' engineering advantage is what can make this type of optimization possible.

1

2

52

9,808

Jun 12

Interesting prices in Space after a 30-50% pullback & the $SPCX IPO done.

$ASTS in the $70s gets really tempting. The real tell is where the next higher low lands. Ignore price targets, watch the lows:

$2->$17->$36->$48->$63->$70s?

Each de-risked milestone buys a better floor.

May 22

Going to start trimming and capturing some profits after multiple 100% weeks. Will likely start filling 13Fs soon, I gotta clean things up a bit.

In particular Space sector holdings are up an eye watering amount and I was strongly leveraged in this sector going in. I want to gradually scale out into $SPCX IPO on some of it. $RKLB and $ASTS are by far my largest positions and I don't plan on that changing.

Trimmed:

$DRAM - China entering the game sooner than I expected, will start to gradually scale out.

$FLY - captured from $20 to ~$50, will leave a little bit into the $SPCX IPO

$RDW - trimming half after $9 to $18. Cool projects and engineering, terrible management track record and margins/dilution. Some early signs of a turn around in Q1. Market cap is now basically double prior ATH. Will continue to scale out into the $20's/$SPCX IPO then watch to see if they are evolving into something I can hold long-term.

$ASTI - going to start scaling down gradually. Size is too big (started at just under 5% of company at $2) and I need to see more concrete progress rather than seemingly empty statements.

$BKSY - up over 600%, size is too big now/taking some profits.

$VELO - traded this for ~500% , going to trim from $20-$30 range into IPO. Very interested in their decentralized manufacturing move recently.

$OUST - held for over a year so going to trim LTCG positions a little into the $40's. Interesting general robotics play long term but they need to shrink things down much further to be viable for the humanoids.

$TE - trimmed around $9, been in since ~$2 with big size so it got too big relative to the weight I want it at now.

Also will be taking profits/closing on $VOYG, $PL.

Going to keep $BE, $LUNR, $OSS, $WOLF, $NVTS, $IFX, $PENG, $ALAB, $INFQ, $NBIS, $JOBY, $QS, $BAER.

Sorry for the ticker spam, but hopefully now people will stop asking. Not financial advice. Holdings could change any moment. These aren't all of my positions (don't want to get doxxed with 13F).

6

2

95

42,653

Jun 12

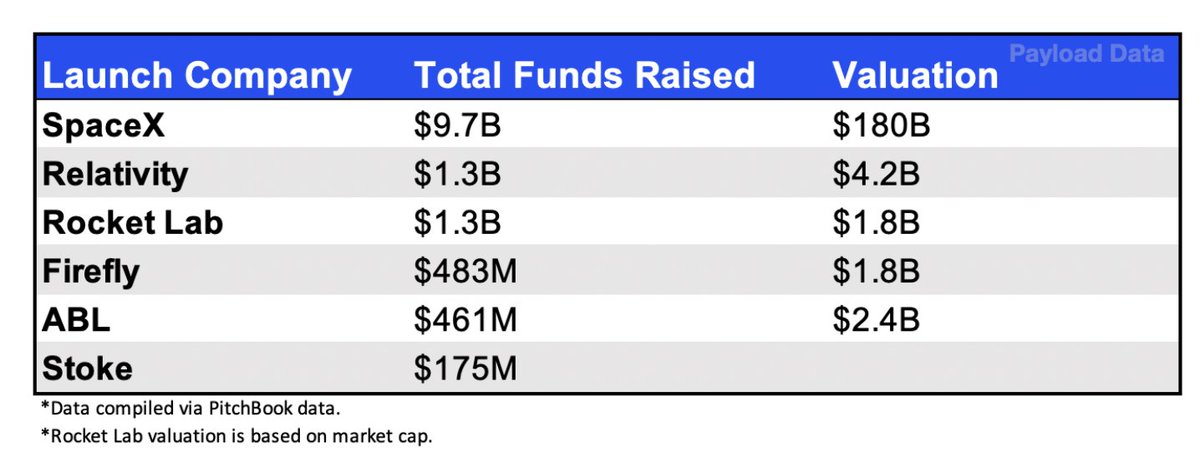

$RKLB has significantly outperformed $SPCX (~35x vs ~10x). Meanwhile others are still trying to get off the ground.

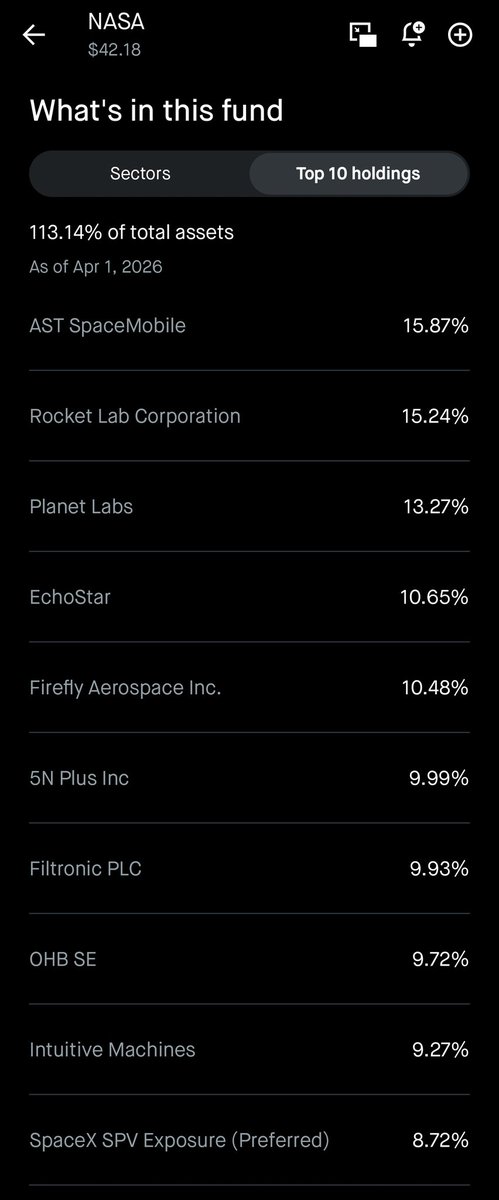

Valuation by launch company:

Payload Research turned the spotlight on Firefly this week with a focus on this *interesting* valuation chart. Article: payloadspace.com/payload-res…

3

4

67

20,311

Jun 12

Remarkable day AH Asia. Portfolio 45% in one "day" is absurd. Things got very dislocated to the downside.

$CRWV in particular was deeply discounted. Mob mentality works both ways.

Either way $NBIS $RKLB $CRWV $ALAB inclusions are a big deal. Significant forced buying incoming.

Jun 12

6

1

98

16,262

Jun 11

Sized up Kioxia 285A $KXIAY a good bit during this past week.

$SNDK continues to be a freight-train. The full NAND/HBF/CXL thesis hasn't even kicked in yet. Kioxia is where I've been adding as a better relative value. Held strong this past week while everything else got punched in the face.

Same NAND, same JV fabs. One trades in Tokyo at ~8-11x earnings, one on Nasdaq at ~14-16x. The gap likely starts to close with the upcoming up-listing.

The gap:

Valuation (annualizing each company's OWN current-quarter guidance)

• Kioxia ¥75,500: 10.6x run-rate EPS, 5.7x sales, $250B cap

• SNDK $1,880: 14-16x run-rate EPS, 8.7x sales, $278B cap

• Kioxia on FY3/27 consensus EPS: 8.4x

Upside to analyst targets

• Kioxia: 14% to consensus (¥86,250), 23% to Goldman (¥93k), 165% to street high (¥200k)

• SNDK: roughly at consensus ($1,751), 73% to street high ($3,250)

Manufacturing control

• Kioxia owns 51% of Flash Ventures, the JV that makes BOTH companies' NAND

• SNDK's wafer supply runs through fabs Kioxia controls

• Same wafers, ~30% cheaper per earnings dollar via Tokyo (for now)

Earnings power (company guidance, not estimates)

• Kioxia Q1 guide: ¥1.3T op profit at a 74% OP margin, ROIC >60%

• Kioxia FY3/26 actuals: OP margin 37.2% (up from 26.5%), ROE 51.9%, ¥470B cash vs ¥203B short-term debt

• SNDK Q4 guide: $7.75-8.25B revenue, $30-33 non-GAAP EPS for the quarter

HBF and the AI storage stack

• SNDK originated HBF, MOU with SK Hynix

• Kioxia already demo'd a 5TB / 64GB/s HBF prototype and co-manufactures through the same JV

• Kioxia is also co-developing GPU-adjacent SSDs with Nvidia aimed at partially offloading HBM, plus a 10M IOPS AI SSD sampling 2H26

• If HBF works, both win on the same wafers but one trades at a relative discount.

Catalysts

• Kioxia: Q1 print Aug 7 (guide already public), OTC ADR uplisting to a major US exchange in preparation (F-6 on file with the SEC), first dividend FY27 plus up to 50% of net cash flow in shareholder returns, BiCS10 mass production targeted within 12 months

• SNDK: fiscal Q4 print ~Aug, HBF samples 2H26

The bear case on the discount: float is still constrained, Toshiba is the largest holder (~22% as of Nov '25), and Bain's remaining stake. That supply is the overhang. The uplisting helps the access problem directly.

Both work if NAND stays tight through 2027, which is Kioxia's own stated view. One is just cheaper.

Run-rate = annualized current-quarter guidance, not a full-year forecast. 1 $KXIAY ADR = 1/10 of a Tokyo share. Not investment advice, verify everything yourself.

Jun 5

Sensing some market fatigue. Hopefully we get a brief period of healthy consolidation.

Sold a good chunk of $DRAM in this $66-$68 range. Could be a bit "early," but the memory run-up has been ridiculous and I wanted to add to the cash I built up from the space names. The narrative changing can also affect stock prices before the reality actually hits.

I've been increasing allocation into:

-CXL/NAND/HBF: $ALAB, $PENG and watching for a dip to add to Kioxia 285A. $SNDK if we get a big pullback.

-Photonics/CPO: $ALAB, added more $AAOI, plus smaller $XFAB and $SIVE; considering $SOI

-Power-semi/800V: added to $WOLF; have $NVTS, $IFX, $XFAB

-Testing: added to $AEHR; considering $COHU

-Token Factory: would add to $CRWV again in the $90s, bought back some $BRUN

I undersized some of these initially (lack of knowledge/confidence and a lot of capital was tied up in Space). Will look to add to any of these on a big pullback.

NFA, just my opinion.

15

19

160

84,543

Jun 11

The $SPX level held despite repeated testing and endless negative headlines (hot CPI, resumption of bombings, etc).

Got some good entries.

Looking forward to getting this $SPCX IPO over with as well.

Jun 9

Hitting some important MA's here at $SPX 7275, added another good chunk back to positions.

This is pre-planned discipline with zero emotions. Just like the profit taking and puts were.

2

1

49

8,663

Jun 9

For $ASTS the real gains are the mental illnesses we accumulate along the way.

17

13

297

31,942

Jun 9

If anything this would be beneficial for $AAOI. CPO was the supposed "existential threat" to pluggables. A delay just extends the pluggable optics era (800G now, 1.6T next). Tons of recent tourists in the name though, it may be messy for a bit.

I'm thinking this is potentially less good for $WOLF, $NVTS, $SIVE, etc if true. (big if)

Jun 9

Expect some short term selling in photonics names on the CPO/800V delay headline. The market will paint the whole sector with one brush.

Photonics is not just CPO. CPO is one slice of a much larger stack.

Pluggable transceivers are a $26B market in 2026 growing to $45B by 2030. CPO was modeled at $0.1B this year. The delay barely touches the revenue that actually exists today.

LPO/LRO scales from $1.2B in 2026 to $5B by 2030 and just became more important.

> NPO is the one SemiAnalysis says could accelerate.

>OCS grows from $1B to over $4B and saves power regardless of what happens with CPO.

Sell the headline if you want. But the TAM didn't move.

$AAOI $CRDO $SMTC $MTSI $COHR

16

6

171

49,820

Jun 9

Hitting some important MA's here at $SPX 7275, added another good chunk back to positions.

This is pre-planned discipline with zero emotions. Just like the profit taking and puts were.

Jun 5

7

2

66

23,925

Jun 9

and a major headline right after I posted this. Despite this major headline if buyers still step in then that would be a strong sign. Otherwise losing $SPX 7200 would have me put on the breaks on.

14

4,275

Jun 8

Added to Kioxia 285A on the open. We may not get much lower than 69000 and I don't want to be frozen out due to greed. I thought -15% from the highs on Japan's biggest company is worth a shot especially with all of the NAND/HBF/CXL news coming out.

Jun 5

Sensing some market fatigue. Hopefully we get a brief period of healthy consolidation.

Sold a good chunk of $DRAM in this $66-$68 range. Could be a bit "early," but the memory run-up has been ridiculous and I wanted to add to the cash I built up from the space names. The narrative changing can also affect stock prices before the reality actually hits.

I've been increasing allocation into:

-CXL/NAND/HBF: $ALAB, $PENG and watching for a dip to add to Kioxia 285A. $SNDK if we get a big pullback.

-Photonics/CPO: $ALAB, added more $AAOI, plus smaller $XFAB and $SIVE; considering $SOI

-Power-semi/800V: added to $WOLF; have $NVTS, $IFX, $XFAB

-Testing: added to $AEHR; considering $COHU

-Token Factory: would add to $CRWV again in the $90s, bought back some $BRUN

I undersized some of these initially (lack of knowledge/confidence and a lot of capital was tied up in Space). Will look to add to any of these on a big pullback.

NFA, just my opinion.

8

59

14,309

YeahDave retweeted

Jun 5

The people that keep pinging me to defend $BRUN seem to have missed the number of times I emphasized that this is just a small side play, not some "early $NBIS", accounting shenanigans, and other issues etc. I don't think everyone should be bullish on it, nor do I think it is inconceivable that the compute constraints could work in their favor in the end.

Just some things worth clarifying:

3. On "~21% of FY25 rev came from crypto":

Blockchain rewards were ~3% of revenue in Q1 2026 ($341k of $11M). If idle GPUs went to token networks during the 2025 buildout, that share is now shrinking as contracted lease revenue ramps, which is capacity getting absorbed and not a red flag.

4. "Customer book is basically adverse selection", "$BRUN got the leftovers"

"I do like TML since I've had some good experiences w/ some of their team, but cmon, they're a pre-rev startup."

This is an assertion, not evidence. The anchor is Thinking Machines, which raised $ 2B at a $12B valuation (a16z, Nvidia, AMD, Cisco, ServiceNow, Jane Street), ships Tinker, and just signed a multibillion-dollar Google Cloud deal. Not pre-rev, and not even the point anyway: the BRUN contract is take-or-pay, so TML pays the full $471.7M whether or not it uses the compute. The only way that backlog disappears is TML insolvency, which is not the bet you want to make against one of the best funded labs in the market. Fair concern is concentration (TML is ~a third of backlog), not customer quality.

Fluidstack as a broker customer, a frontier lab as an anchor, and $NBIS apparently as a customer are arguably the opposite of leftovers for such a tiny/early company.

7. "Being on $NVDA Exemplar list means very little imo.

Other neoclouds on the list all got Nvidia investment e.g.

$CRWV, $NBIS, Lambda, Crusoe.

But nothing for $BRUN...

And Nvidia literally writes cheques to any every company lol."

I think this is way overstated for a $2B company that just IPO'd and is just now starting to grow a backlog. It took a while for $NVDA to invest in $NBIS. Claiming "Exemplar designation means very little" makes it sound like you think $NVDA is sloppy and just hands this out to everybody.

People are also claiming 90% of the lock-up is expiring on Monday and you are affirming that? I think it is worth avoiding being fair and avoid being overly negative.

2

1

45

9,713

Jun 5

Pretty vicious move. I guess it was too much to hope for something more orderly after weeks of up only. At $SPX 7,450 we're already starting to hit RSI lvls not seen since the Iran war low. Starting to buy a decent bit here (non-space). Taking profits on the $ASTS $RKLB $QQQ puts

Jun 5

Sensing some market fatigue. Hopefully we get a brief period of healthy consolidation.

Sold a good chunk of $DRAM in this $66-$68 range. Could be a bit "early," but the memory run-up has been ridiculous and I wanted to add to the cash I built up from the space names. The narrative changing can also affect stock prices before the reality actually hits.

I've been increasing allocation into:

-CXL/NAND/HBF: $ALAB, $PENG and watching for a dip to add to Kioxia 285A. $SNDK if we get a big pullback.

-Photonics/CPO: $ALAB, added more $AAOI, plus smaller $XFAB and $SIVE; considering $SOI

-Power-semi/800V: added to $WOLF; have $NVTS, $IFX, $XFAB

-Testing: added to $AEHR; considering $COHU

-Token Factory: would add to $CRWV again in the $90s, bought back some $BRUN

I undersized some of these initially (lack of knowledge/confidence and a lot of capital was tied up in Space). Will look to add to any of these on a big pullback.

NFA, just my opinion.

19

2

114

37,311