【一封台湾供应商的涨价通知,揭示了 AI 光子供应链最深处的"卡脖子"】

今天 @aleabitoreddit 转发了一封来自台湾公司 VPEC 全新光电的涨价通知书,并发表了她的判断。

这封通知书是真实的商业文件,原文是繁体中文,核心内容是:

"由于全球原材料成本持续上涨、供应短缺以及通货膨胀压力,本公司不得不对磊晶片(Epiwafer)产品进行价格调整。"

Serenity 看到这封信,立刻说:

"这对 $IQE 和 Landmark(3081)来说是一个正面的瓶颈信号——定价权和需求都在增强。"

先搞清楚:磊晶片(Epiwafer)是什么?

磊晶片是制造化合物半导体(如砷化镓 GaAs、磷化铟 InP、氮化镓 GaN)的核心中间材料。

你可以把它理解为:如果把芯片比作一栋楼,磊晶片就是建楼用的"预制板"——没有它,后续所有的芯片制造工序都无法进行。

它的主要应用场景包括:AI 数据中心的光模块、CPO 光源、5G 基站射频芯片、激光雷达等。

为什么 VPEC 涨价是一个重要信号?

Serenity 的逻辑是:供应商主动涨价,说明需求已经超过了供给,定价权正在向供应商转移。

这和她一贯的"瓶颈猎人"方法论完全一致——当一个供应链环节开始涨价,说明这个环节已经成为真正的瓶颈,而不只是理论上的瓶颈。

她还补充了一个重要的背景:$MTSI(MACOM Technology)刚刚战略投资了 $IQE,目的是锁定磊晶片产能。 一家大公司愿意花钱提前锁定供应,本身就是对供应紧张最有力的验证。

涉及标的说明:

A 股的对应视角:

磊晶片(外延片)的国产化,是 A 股半导体材料赛道中一个相对冷门但极为重要的方向。

A 股中,华芯半导体(未上市)、三安光电(600703.SH) 的化合物半导体业务(GaAs/GaN 外延片)与这条逻辑链最为接近。三安光电是目前 A 股中规模最大的化合物半导体垂直整合厂商,既做外延片,也做芯片。

此外,中晶科技(603290.SH) 和 有研新材(600206.SH) 在半导体衬底材料方向也有布局,但与磊晶片的直接关联度相对较低。

需要注意的是:

$IQE 是英国上市的小盘股,流动性有限,中国投资者无法直接购买。Serenity 本人持有 $IQE 仓位,存在利益相关。VPEC 的涨价通知是一个早期信号,从涨价到利润兑现还需要时间传导。

Jun 12

VPEC new price hikes on Epiwafers today.

Positive bottleneck read through on companies like $IQE and Landmark (3081) in terms of pricing power/demand for epiwafers.

This follows $MTSI investment into IQE to secure capacity, and shows how important some of these chokepoints are.

(disclosure: have positions in IQE)

1

169

$AMD • $ALAB • $ASML • $CLS • $CRDO • $INOD • $LITE • $LRCX • $MPWR • $MTSI • $MU • $SITM • $SKYT • $TER • $TSM

Free float in JLHL will soon be owned by those who hold, we know what that means, an RGC. 🚀🤑

$RGC $3-$3,780 = forward split $0.08-$99.47 = 1243x value‼️ $JLHL ATL $2.70 - $⁉️

Comparison of "The Setup":

$RGC: Slumped up on low volume until the news of the 38:1 forward split came – then volume exploded and the price went vertical (parabolic).

$JLHL: Doing exactly the same thing now. It "gates" up while testing resistance levels without facing any selling pressure.

Comparison 🟩

Feature Regencell Bioscience ( $RGC) ↔️ Julong Holding ( $JLHL)

Major Shareholder / Insider Owned 🟩 ~86% (Yat-Gai Au) ↔️ ~93.25% (Jiaqi Hu)

Insider Stock Status 🟩 Locked (Lock-up) ↔️ Locked (Lock-up)

Outstanding Shares (OS) 🟩 ~13.01 Million ↔️ ~21.45 Million

Free Float (Tradeable Shares) 🟩 ~790,000 ↔️ ~1.28 Million

Effective Float % 🟩 approx. 6% ↔️ approx. 6%

Trading Pattern 🟩 Low Volume / Upward "Grind" ↔️ Low Volume / Upward "Grind"

Catalyst 🟩 38:1 Forward Split (June 2025) ↔️ None announced yet

238

$BURU

.15 to .75 move coming

It all starts Monday with massive G7 summit mon-wed!

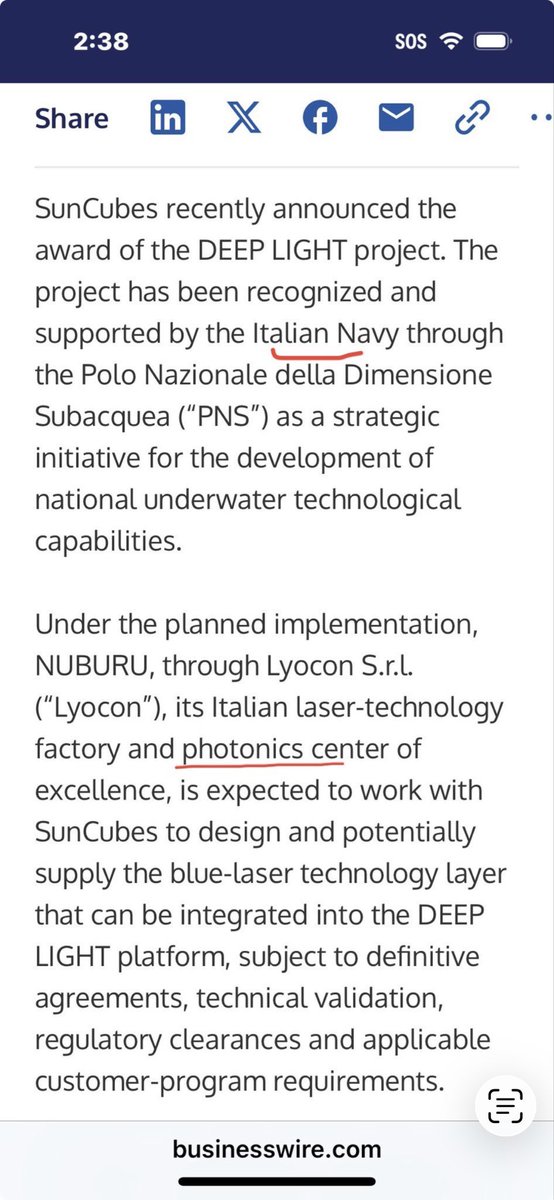

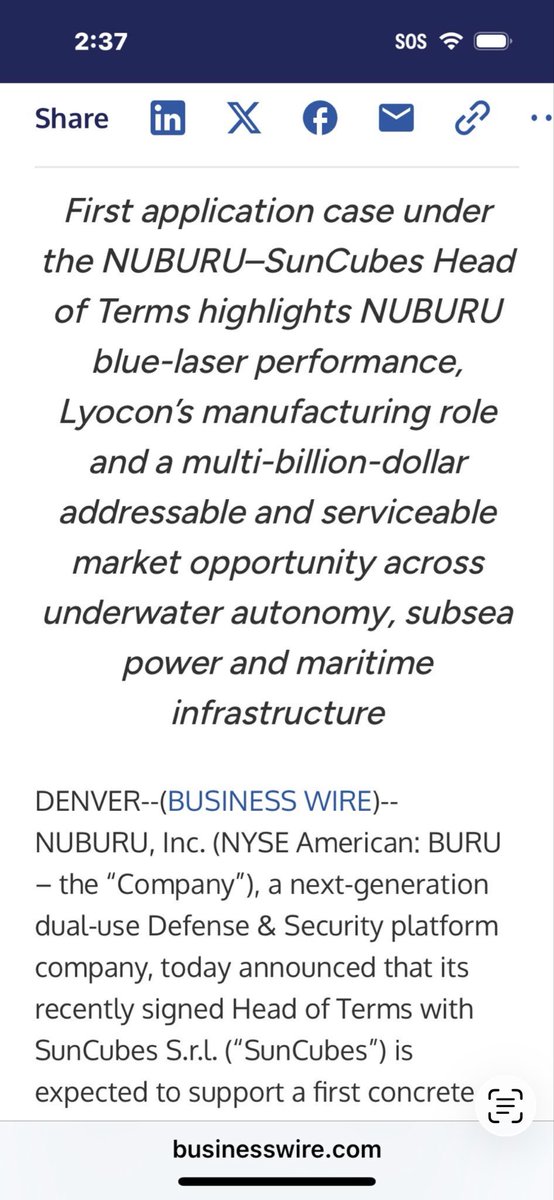

BURU is backed by ITALIAN NAVY! Unfound photonics and military industrial laser company!

Nailed $AMPG and $LASE at dead bottoms before their 500% runs!

$GLW $OCC $AAOI $LITE $COHR $IPGP $LASR $MTSI $GLW $AXTI $LWLG $ALMU $LPTH $OPTX $FN $POET $AMKR $MRVL $NVDA $AVGO $CIEN $CSCO $INTC $NOK $CREO $ASTS $AEHR $AEVA $ALGM $APH $ONTO $MKSI $GFS $TER $FORM $USO $BA

2

3

13

1,139

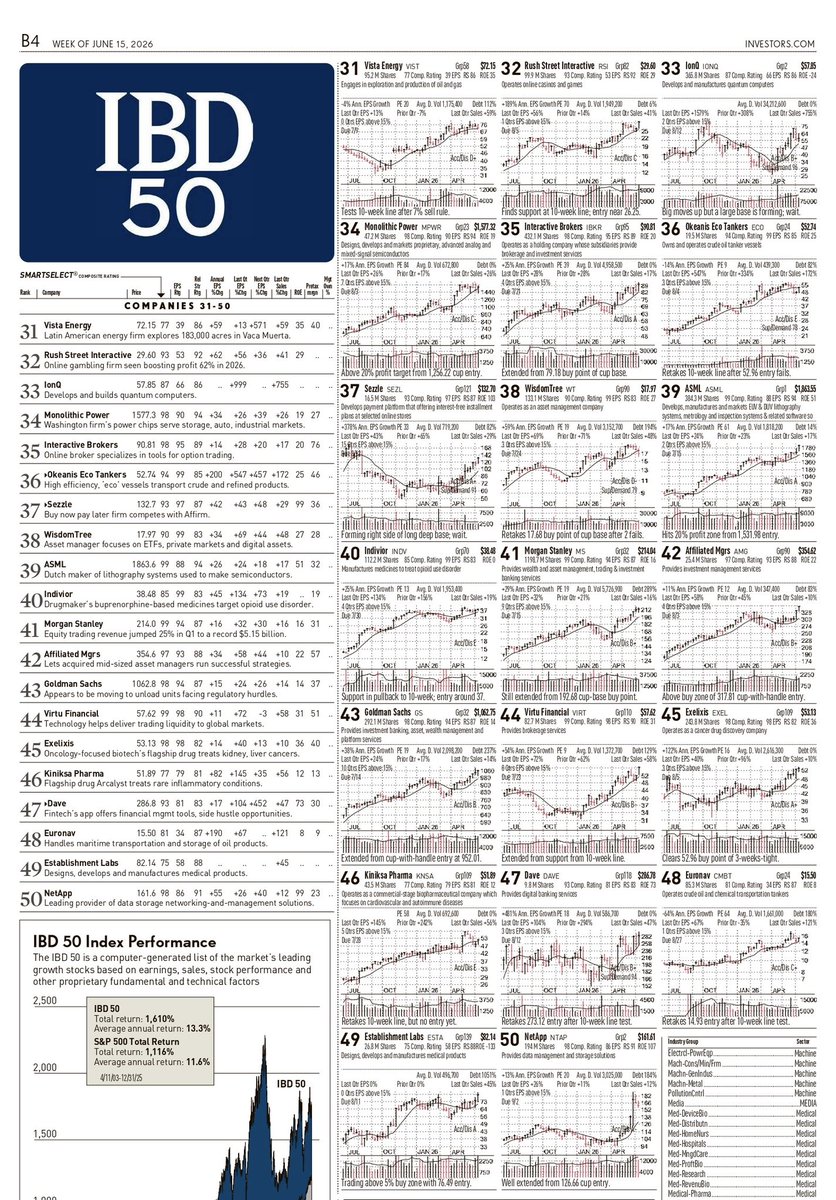

🚨 IBD 50 STOCKS TO WATCH NEXT WEEK

AI & SEMICONDUCTORS

$AMD • $ALAB • $ASML • $CLS • $CRDO • $INOD • $LITE • $LRCX • $MPWR • $MTSI • $MU • $SITM • $SKYT • $TER • $TSM

BIOTECH & HEALTHCARE

$AXSM • $EXEL • $GH • $KNSA • $KRYS • $LQDA • $OSCR • $TGTX • $TVTX

FINANCIALS

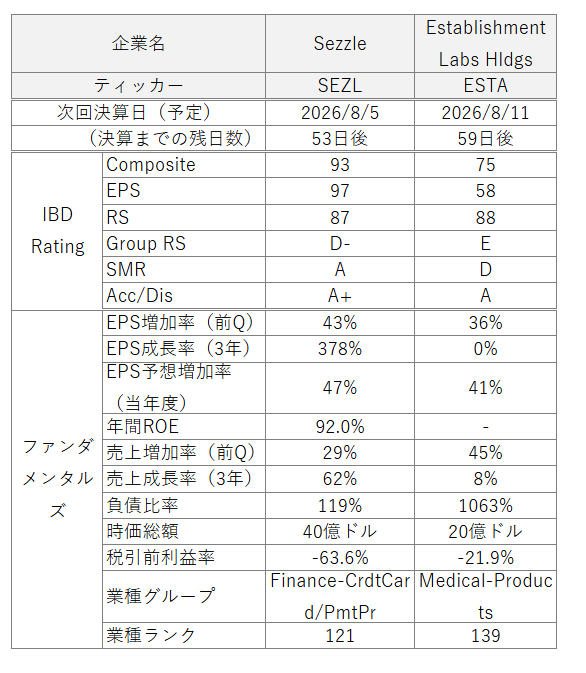

$GS • $IBKR • $MS • $RSI • $SEZL • $SNEX • $VIRT

INDUSTRIALS & INFRASTRUCTURE

$CECO • $CRS • $DY • $FIX

ENERGY & RESOURCES

$BE • $HUT • $VIST

CONSUMER & SPECIALTY

$AMG • $COCO • $INDV • $WT

EMERGING TECHNOLOGY

$IONQ

📈 The strongest stocks tend to cluster in leading sectors. Watch for earnings strength, institutional accumulation, relative strength, and high-volume breakouts as the new trading week unfolds.

Save this watchlist and stay prepared.

3

27

118

11,810

$MSFT - You do not need to know what will happen next.

@grok assess the validity and value of the content taken from the URL (3rd June; tradingview.com/chart/MSFT/1…)

In MSFT the TradeSentinel framework calls for restraint and patience. This message is not excitement and no dopamine kick.

The edge right now belongs to those who can sit on their hands and wait for the structure to either repair or fully break.

The next few sessions will likely decide if this is a healthy shakeout or the beginning of a real reversal. Don’t confuse a still-elevated price with a healthy trend.

👉 There is no need to rush. There is no need to forecast prices.

👉 The key is confidence and a positive expectancy of your trading system.. Look at linked posts about DELL (DELL:Worrying About Entering Late Would Have Cost Me a 115% Gain) and MTSI (How to add up on a position which is 50% up and on fire?). This is how I can act with calm and confidence.

1️⃣ Overall State

Distribution Risk at 3M high. Sharp -4.17% rejection on high relative volume (3x) in extreme expanding volatility.

2️⃣ Thesis

MSFT showing exhaustion signals after failing to hold 3M high. Caution is warranted.

3️⃣ What Validates the Thesis?

Heavy volume red candle at highs

Extreme expanding volatility regime

Rejection after 3M high attempt

Poor absorption on selloff

4️⃣ What Invalidates the Thesis?

Strong bullish reversal on declining volume

Price holds above SMA20 (~421.3) with volume support

Volatility begins easing

🧩 FULL SIGNAL DECOMPOSITION

Trend Structure

Price still above SMA20 ( 4.8%) and SMA50 but rejected sharply at 3M high with large red candle. SMAs mostly upward-sloping but losing acceleration.

👉 Alone / Isolated: Moderately supportive (structure intact but decelerating).

👉 Combined: Weakened — distribution candle near highs undermines the uptrend.

Relative Strength

Little to no relative strength

👉 Alone / Isolated: low conviction

👉 Combined: reduces conviction

Volatility

Regime: Extreme

Change: Expanding / Steepening (highly unfavorable).

👉 Alone / Isolated: Strongly Bearish (increases risk of larger moves).

👉 Combined: Very negative — extreme expanding vol on distribution day significantly raises reversal probability.

Volume / Participation

High Relative Volume (during recent days) including last two days — clear effort vs poor result.

👉 Alone / Isolated: Bearish (distribution signal at highs).

👉 Combined: Strongly negative — high volume rejection confirms supply entering.

Price Behavior

Sharp -4.17% reversal candle failing to hold 3M high after recent attempt. Poor close near lows of day.

👉 Alone / Isolated: Bearish (rejection and loss of momentum).

👉 Combined: Dominant negative signal — overrides SMA support in current context.

Overall Signal Composition Verdict: Bearish tilt due to high-conviction negative signals in Volatility Volume Price Behavior outweighing residual Trend/RS support.

1

78

I had an alert set on $MTSI Friday but didn't take the trade. Somehow it didn't look ready. Maybe Monday?

18

Jun 13

IBD50銘柄ランク推移 続き

■ランクアップ銘柄

$MU (2→1)

$ALAB (3→2)

$LQDA (7→4)

$SITM (8→5)

$CRDO (9→7)

$CRS (20→11)

$CECO (14→12)

$LRCX (15→13)

$CLS (38→15)

$TGTX (41→19)

$OSCR (28→21)

$GH (26→22)

$SNEX (27→26)

$RSI (34→32)

$IBKR (36→35)

$ASML (42→39)

$AMG (47→42)

$VIRT (49→44)

$DAVE (48→47)

※アップ幅が大きい順にソート

CLS (38→15)

TGTX (41→19)

CRS (20→11)

OSCR (28→21)

AMG (47→42)

VIRT (49→44)

GH (26→22)

LQDA (7→4)

SITM (8→5)

ASML (42→39)

CRDO (9→7)

CECO (14→12)

LRCX (15→13)

RSI (34→32)

MU (2→1)

ALAB (3→2)

SNEX (27→26)

IBKR (36→35)

DAVE (48→47)

■ランクダウン銘柄

$FIX (4→8)

$INOD (11→14)

$BE (13→17)

$COCO (17→18)

$SEI (12→20)

$SKYT (22→23)

$DY (21→25)

$OUST (18→27)

$MTSI (25→28)

$TSM (23→29)

$VIST (16→31)

$IONQ (19→33)

$MPWR (33→34)

$WT (37→38)

$INDV (31→40)

$MS (32→41)

$GS (39→43)

$EXEL (40→45)

$NTAP (43→50)

※ダウン幅が大きい順にソート

VIST (16→31)

IONQ (19→33)

OUST (18→27)

INDV (31→40)

MS (32→41)

SEI (12→20)

NTAP (43→50)

TSM (23→29)

EXEL (40→45)

FIX (4→8)

BE (13→17)

DY (21→25)

GS (39→43)

INOD (11→14)

MTSI (25→28)

COCO (17→18)

SKYT (22→23)

MPWR (33→34)

WT (37→38)

画像1枚目:ランクアップ幅が大きい4銘柄のランク推移グラフ (過去30週)

画像2枚目:ランクダウン幅が大きい4銘柄のランク推移グラフ (過去30週)

画像3枚目:今週初登場銘柄のファンダ情報

$TOYO が消えてくれて良かったです。胡散臭さに気づいたかな?

12

1,282

Jun 13

VPECがEpiwafersの価格を引き上げた。

この動きは、IQEやLandmark(3081)といった企業に価格決定力があることを示している。MTSIがIQEの生産能力確保のために先行投資した事実とも重なる。

Epiwafer製造におけるボトルネックが、そのまま価格に跳ね返る構造が続いている。

6,120

🚨Everyone is still buying the chips. The bottleneck already moved.

A GPU that computes in nanoseconds and waits microseconds for data is a stranded asset. At 1.6T speeds, copper runs out of physics. The constraint on AI is no longer how fast you can think. It's how fast you can move what you thought.

Jensen has now said it twice in three months.

At GTC in March: "Is copper going to still be important? The answer is yes... Are you going to scale up optical? Yes. Are you going to scale out optical? Yes... We need a lot more capacity for copper. We need a lot more capacity for optics. We need a lot more capacity for CPO."

Last week at Computex, on Marvell's stage: "Optics where you must, copper where you can." Then he called Marvell the next trillion-dollar company and the optical complex repriced within days. The same keynote put a date on the handoff: 200G per lane is the last generation where copper is sufficient. After that, optics takes the rack.

Translation: not copper OR light. Copper now, light next, unprecedented amounts of both. 🔥

The chain is unavoidable: AI tokens are profitable → more GPUs → more bandwidth → copper hits its wall → photonics becomes the chokepoint.

And the smart money stopped debating. Follow the closed deals:

→ $NVDA has committed at least $6.5B to photonics in three months: $2B into Lumentum, $2B into Coherent, a $500M stake in Corning, and a piece of Ayar Labs' $500M round. Direct investments to secure its own light supply.

→ $MRVL paid $3.25B for Celestial AI, up to $5.5B with milestones, to build what its CEO calls a silicon photonics powerhouse.

→ $CRDO closed DustPhotonics two weeks ago. Ciena bought CPO startup Nubis for $270M.

North of $10B of strategic capital locked up one supply chain in under a year. Capital like that doesn't chase a theme. It secures a bottleneck.

LAYER 1: WAFER. Every laser starts as a crystal.

🟠 $AXTI: the InP substrate leader. The first chokepoint in the stack.

🟡 $IQE: compound-semi epiwafers feeding the laser makers. Speculative, but structurally upstream.

LAYER 2: LIGHT. Photons don't make themselves.

🟠 $LITE: revenue 90% YoY last quarter to $808M. EML shipments doubled and management says demand still exceeds supply across EMLs, pump lasers, and transceivers. NVIDIA just wired them $2B. OCS backlog past $400M plus a multi-hundred-million CPO order for 2027.

🟢 $SIVEF (Stockholm: SIVE): the external light source. CPO does not emit its own light. Every optical engine needs a continuous-wave InP laser feeding it, and that is the layer you cannot engineer around. ELS modules with POET hit production readiness end of this year. Disclosure: long.

🟣 $POET: the optical engine wildcard. Its Optical Interposer pairs with Sivers' lasers on external light sources for CPO, with a LITEON module deal stacked on top. Binary commercialization, real architecture.

LAYER 3: OPTICS AND MODULES. Where light meets the rack.

🟠 $COHR: the volume anchor in transceivers, holding NVIDIA's other $2B check.

🔵 $AAOI: Q1 revenue 51% to a record $151M, datacenter revenue more than doubled, $124M of 800G orders plus a $200M 1.6T order in hand. Scaling Texas capacity toward 500K units a month by year-end, targeting $1B revenue this year. Domestic supply while everyone fights over offshore. Disclosure: long.

🟠 $FN: the foundry of optics. When Fabrinet is building, the orders already exist.

THE INTERCONNECT: the layer the rack cannot route around.

🔵 $CRDO: just closed DustPhotonics. SerDes → DSP → silicon photonics → system integration, one company, 800G through 3.2T. Electrical AND optical, end to end. FY26 revenue tripled to $1.34B at 68% gross margin. The toll booth on both roads. Disclosure: long.

🟠 $MRVL: $3.25B for Celestial AI, and Jensen's trillion-dollar nod on the Computex stage.

🟠 $AVGO: switch silicon, optical DSPs, CPO engines. They define the socket.

🟠 $ANET: the AI spine. 100K-GPU clusters get stitched together in light.

LAYER 4: PACKAGING, FIBER, FOUNDRY. Where photons get industrialized.

🔵 $TSEM: the neutral silicon photonics foundry. Prints wafers for whoever wins.

🟣 $LPKF: glass-substrate packaging for glass-based CPO. Real technology, binary commercialization.

🟠 $GLW: AI racks demand several times the fiber density of legacy cloud, and NVIDIA just took a $500M stake. Corning sells density.

LAYER 5: TEST AND THE ANALOG UNDERLAYER. Complexity is a tax paid in validation.

🔵 $AEHR: silicon photonics test, ramping with the cycle. '

🔵 $VIAV: every 800G and 1.6T transceiver gets validated before it ships. The gate the market prices like an accessory.

🔵 $SMTC: the drivers and TIAs that fire the lasers. Sits directly under the LPO trade.

🔵 $MTSI: the high-speed analog behind 1.6T engines.

🟠 $CIEN: transport. Even long-haul is buying light.

💡The counter-thesis, because every map needs one. The honest debate on this stack is whether these are genuine bottleneck assets or cyclical optics suppliers enjoying peak demand at peak multiples. Lumentum's May print showed 90% growth with the stock up roughly 1,400% over the prior year at a triple-digit trailing multiple. That is a price for perfection. Most of these names live or die on a handful of hyperscaler capex lines, and one digestion quarter hits the whole stack at once. CPO timing has already slipped once. Architecture risk is real: LPO, CPO, and stretched copper are still fighting for the same sockets. The cycle is real. So is the gravity. 🔥

But the bears have to explain one thing: $NVDA, $MRVL, $CRDO, and $CIEN just spent over $10B securing this supply chain with their own balance sheets. The people with the best information are paying up for the layers.

The market owns the top of this stack. The asymmetry is at the edges: wafer, light, packaging, test.

Own the layers, not the logo.

Bookmark this for the weekend. Then tag the one investor you know who's still all compute and no interconnect. 👀

27

142

782

70,610