Joined February 2025

- Tweets 275

- Following 505

- Followers 239

- Likes 65

Photos and videos

Pinned Tweet

Mar 18

We take the risk for you. You just concentrate on making profit.

readies.biz — Your payment solution

#HighRiskMerchants #HighRiskPayments #HighRiskBusiness #PaymentProcessing #MerchantServices #HighRiskMerchantAccount

7

687

Jun 13

#PaymentScams #FintechScam #MerchantServices #ScamAlert #PaymentGateway #ScammersExposed #OnlineBusiness #WarnMerchants

⚠️ SCAM ALERT – Payment Industry Crooks

Stay away from these sharks. robbed merchants of millions:

DCP (Digital Crypto Payments) – Yousef Kamel

4

May 31

Peter Thiel's move to Argentina reflects a growing trend businessinsider.com/peter-th… via @businessinsider

How can that be a surprise didn't his ancestors move there when they couldent life with them self because of there past actions and just suprted the wrong guy

2

44

May 29

Payment 365 team will be at Sigma this weekend! 🇲🇹

We'll be there from Sunday through Monday, catching up with old friends and industry colleagues. Always great to hear there experiences from the past year the wins with new solid payment partners, but also the growing creativity of online payment scammers who continue to target even the most experienced merchants.

We’ll be listening and learning from victims about the latest tricks so we can better advise where to be extra careful when onboarding new PSPs, APMs, or payment solutions.

next week, we'll exposing the new proven fraudsters in the industry and sharing our updated list of the most dishonest and fraudulent providers again

Safe travels everyone! Have a great weekend!

Payment 365

Excited to announce that the Payment 365 team will be at Sigma this weekend! 🇲🇹

We'll be there from Sunday through Monday, catching up with old friends and industry colleagues. Always great to hear your experiences from the past year — the wins with new solid payment partners, but also the growing creativity of online payment scammers who continue to target even the most experienced merchants.

We’ll be listening and learning from victims about the latest tricks so we can better advise where to be extra careful when onboarding new PSPs, APMs, or payment solutions.

Starting next week, we’ll begin regularly exposing proven fraudsters in the industry and sharing our updated list of the most dishonest and fraudulent providers.

Safe travels everyone! Have a great weekend!

Payment 365

1

42

May 29

Payment 365 team will be at Sigma this weekend! 🇲🇹

We'll be there from Sunday through Monday, catching up with old friends and industry colleagues. Always great to hear there experiences from the past year the wins with new solid payment partners, but also the growing creativity of online payment scammers who continue to target even the most experienced merchants.

We’ll be listening and learning from victims about the latest tricks so we can better advise where to be extra careful when onboarding new PSPs, APMs, or payment solutions.

next week, we'll exposing the new proven fraudsters in the industry and sharing our updated list of the most dishonest and fraudulent providers again

Safe travels everyone! Have a great weekend!

Payment 365

Excited to announce that the Payment 365 team will be at Sigma this weekend! 🇲🇹

We'll be there from Sunday through Monday, catching up with old friends and industry colleagues. Always great to hear your experiences from the past year — the wins with new solid payment partners, but also the growing creativity of online payment scammers who continue to target even the most experienced merchants.

We’ll be listening and learning from victims about the latest tricks so we can better advise where to be extra careful when onboarding new PSPs, APMs, or payment solutions.

Starting next week, we’ll begin regularly exposing proven fraudsters in the industry and sharing our updated list of the most dishonest and fraudulent providers.

Safe travels everyone! Have a great weekend!

Payment 365

1

25

May 29

#iGaming #OnlineGambling #GamblingIndustry #Casino #SportsBetting #GamingIndustry #iGamingMalta #Betting #Gambling

Payment 365 team will be at Sigma this weekend! 🇲🇹

We'll be there from Sunday through Monday, catching up with old friends and industry colleagues. Always great to hear there experiences from the past year the wins with new solid payment partners, but also the growing creativity of online payment scammers who continue to target even the most experienced merchants.

We’ll be listening and learning from victims about the latest tricks so we can better advise where to be extra careful when onboarding new PSPs, APMs, or payment solutions.

next week, we'll exposing the new proven fraudsters in the industry and sharing our updated list of the most dishonest and fraudulent providers again

Safe travels everyone! Have a great weekend!

Payment 365

Excited to announce that the Payment 365 team will be at Sigma this weekend! 🇲🇹

We'll be there from Sunday through Monday, catching up with old friends and industry colleagues. Always great to hear your experiences from the past year — the wins with new solid payment partners, but also the growing creativity of online payment scammers who continue to target even the most experienced merchants.

We’ll be listening and learning from victims about the latest tricks so we can better advise where to be extra careful when onboarding new PSPs, APMs, or payment solutions.

Starting next week, we’ll begin regularly exposing proven fraudsters in the industry and sharing our updated list of the most dishonest and fraudulent providers.

Safe travels everyone! Have a great weekend!

Payment 365

12

May 27

The Shadow Empire of High-Risk Payments: How Merchants Are Being Robbed in Plain Sight

In the glittering world of online commerce, high-risk merchants — those operating in industries like online gambling, adult entertainment, nutraceuticals, crypto, or CBD — are told they are entering a land of opportunity. "Fast bucks," the promises say. "Global reach. Easy approvals."

The reality is a sophisticated machine designed to extract every possible cent from merchants who have already fought tooth and nail to acquire customers. What follows is not just bad service. It is, in many cases, daylight robbery dressed up in corporate suits, offshore licenses, and glossy websites.

The Setup: A Industry Built on Smoke and Mirrors

The high-risk payment sector has a handful of established, relatively compliant players who operate within legal boundaries. Surrounding them is an army of thousands of smaller processors, aggregators, and "solution providers" who treat regulations as suggestions rather than rules.

These companies register in jurisdictions where enforcement is weak or nonexistent — places where "licensed" often means little more than a piece of paper and an annual fee. Malta, certain Eastern European countries, Southeast Asian hubs, and various island nations have become favorite playgrounds. Some licenses come from regulators that exist mostly in name only.

Merchants, desperate for payment solutions after being rejected by mainstream banks, sign contracts without fully understanding the small print. They are sold on low MDR (Merchant Discount Rate), fast settlements, and "robust" compliance. What they get is something entirely different.

The Art of the Slow Bleed (and Sudden Death)

The scam rarely starts with outright theft. It begins with "innovative" fee structures that the industry itself invented:

Failed transaction fees — sometimes higher than successful ones. In the age of AI and smart retry logic, merchants are charged for declines as if an army of agents is manually retrying each one. This is the modern version of the three-card monte scam — you cannot win.

Rolling reserves that mysteriously grow.

Miscoding to bypass card scheme rules.

Arbitrary chargeback penalties, currency conversion gouges, and "compliance monitoring" fees.

Sudden account freezes right when payouts are due, followed by endless "reviews."

Many merchants report the same pattern: They spend heavily on affiliates, SEO, and advertising to drive traffic. Once the money starts flowing, the payment provider begins extracting it through creative fees and delays. By the time the merchant realizes what's happening, thousands or hundreds of thousands are locked up.

When merchants complain, they are often told the funds are being held for "risk reasons" or "pending investigation." Appeals go nowhere. Some providers simply rebrand, change legal entities, or disappear — only to pop up under a new name months later.

The Usual Suspects: Current Investigations

Payment 365’s investigation team has been tracking multiple players that keep appearing in merchant complaints. Among those currently under scrutiny:

Glodipay

Gpay Singapore

Buzipay

Paytoro

Vasu Pay

UK DCP (Digital Coin Payment)

Soft2Pay (associated with Mr. Yousef)

Simple2Pay

Payhound (Malta operations)

These names surface repeatedly in stories of delayed or vanished funds, aggressive fee structures, and questionable licensing claims. Payment 365 actively collects merchant experiences and forwards documented cases to relevant authorities while attempting recovery where possible.

Why This Persists

The core problem is simple: Most victims cannot easily go to the police or cybercrime units. The contracts are written to favor the processor. The companies operate across borders. Many merchants themselves operate in gray-area industries and fear drawing regulatory attention. The result is near-perfect impunity for the worst actors.

1

16

May 27

The Shadow Empire of High-Risk Payments: How Merchants Are Being Robbed in Plain Sight

In the glittering world of online commerce, high-risk merchants — those operating in industries like online gambling, adult entertainment, nutraceuticals, crypto, or CBD — are told they are entering a land of opportunity. "Fast bucks," the promises say. "Global reach. Easy approvals."

The reality is a sophisticated machine designed to extract every possible cent from merchants who have already fought tooth and nail to acquire customers. What follows is not just bad service. It is, in many cases, daylight robbery dressed up in corporate suits, offshore licenses, and glossy websites.

The Setup: A Industry Built on Smoke and Mirrors

The high-risk payment sector has a handful of established, relatively compliant players who operate within legal boundaries. Surrounding them is an army of thousands of smaller processors, aggregators, and "solution providers" who treat regulations as suggestions rather than rules.

These companies register in jurisdictions where enforcement is weak or nonexistent — places where "licensed" often means little more than a piece of paper and an annual fee. Malta, certain Eastern European countries, Southeast Asian hubs, and various island nations have become favorite playgrounds.

Merchants, desperate for payment solutions after being rejected by mainstream banks, sign contracts without fully understanding the small print. They are sold on low MDR, fast settlements, and "robust" compliance. What they get is something entirely different.

The Art of the Slow Bleed (and Sudden Death)

The scam rarely starts with outright theft. It begins with "innovative" fee structures that the industry itself invented:

Failed transaction fees (sometimes higher than successful ones)

Rolling reserves that grow mysteriously

Miscoding schemes

Arbitrary chargeback penalties

Sudden account freezes right before payouts

Many merchants report the same pattern: heavy spending on affiliates, advertising, and traffic — only for the payment provider to start bleeding them dry through creative fees and delays. By the time you realize it, your hard-earned revenue is locked up or gone.

The Usual Suspects: Current Investigations

Payment 365’s investigation team has been tracking multiple players that keep appearing in merchant complaints:

Glodipay, Gpay Singapore, Buzipay, Paytoro, Vasu Pay, UK DCP, Soft2Pay, Simple2Pay, Payhound (Malta) and others.

These names surface repeatedly in stories of delayed or vanished funds, aggressive fee structures, and questionable licensing.

Why This Persists

Merchants in gray-area industries often feel they cannot go to authorities. Contracts favor the processors. Companies change names, create new storefronts, or simply disappear with the money.

Fighting Back: The Payment 365 Blackbook

We maintain:

Weekly lists of problematic providers

A regularly updated Blackbook of providers to avoid

Active investigations and merchant evidence collection for authorities

If you’ve been affected by any of the names above or similar providers — contact us. Your experience could help shut them down.

Share this if you’re a merchant who’s been burned.

#HighRiskPayments #PaymentFraud #MerchantScams #PaymentScams #HighRiskMerchant #PaymentProcessors #OfflinePayments #ScamAlert #FinancialScams #OnlineBusinessScams #MerchantProtection #PaymentGateways #HighRiskIndustry #OffshoreScams #MaltaPayments #PaymentIndustry #FraudExposure #MerchantBlackbook #AvoidTheseCompanies #Glodipay #GpaySingapore #Buzipay #Paytoro #VasuPay #Soft2Pay #Payhound #Simple2Pay #DigitalCoinPayment #ChargebackScams #FailedTransactionFees #RollingReserves #Miscoding #AffiliateMarketing #OnlineGamblingPayments #CryptoPayments #AdultPayments #CBDPayments #NutraPayments #DaylightRobbery #BusinessProtection #ExposeTheScammers #Payment365 #MerchantStories #FraudInvestigation #StayAway #ScamWatch #HighRiskWarning #PaymentSolutions #EntrepreneurScams #EcommerceFraud

1

19

May 25

🚨 MAJOR EXPOSÉ ALERT – PAYMENTS365

This Friday we expose a network of Malta-based payment companies allegedly scamming merchants with smooth lies and disappearing acts.

From Payhound (linked to millions in global investment scams – as reported by Times of Malta & BusinessNow) to the DCP / Soft2Pay group.

Names we name:

Elton Dimech (Payhound)

Ramy Ben Fraj (Payhound & ex-DCP)

Yosef Kamel (CEO – Soft2Pay / Simple2Pay / DCP)

Luigi Spina (DCP)

Same tactics: Big promises → Take large deposits → Endless “settlement delays” → Ghosting merchants.

Multiple store fronts: Payhound • Soft2Pay • Simple2Pay • Digital Crypto Pay • S2P Services Ltd

Merchants are losing hundreds of thousands while these operators hide behind EMI & MiCA licenses.

The victim list is growing fast.

If you’ve been scammed by any of these companies — DM us. We want to hear your story.

Full episode drops this Friday.

Warning to all merchants: Stay away.

#PaymentScams #MaltaFintech #HighRiskPayments #FintechScams #MerchantWarning #CryptoPayments #iGamingPayments #PaymentProcessors #EMILicense #MiCA #ScamAlert #FinancialFraud #MaltaScams #PaymentsIndustry #FintechFraud #MerchantProtection #CryptoScams #HighRiskIndustry #Payments365 #ScamExposé

1

38

May 14

🚨 ATTENTION MERCHANTS 🚨

The next big exposure is coming… and this one hits close to home.

A crooked operation running out of Malta & Poland is about to be fully exposed.

We will name ALL companies involved and ALL persons behind them so every merchant knows exactly who to avoid.

This network is full of scammers who think they can keep cheating merchants without consequences.

They cheated the wrong people this time.

Tomorrow we drop the full list the complete story.

Stay tuned. Justice is coming.

#Payment365 #MerchantProtection #ScamExposure #HighRiskMerchant #PaymentProcessing #ChargebackHell #MerchantLife #ScamAlert #ExposeScammers #PaymentGateways #MerchantAccount #FraudPrevention #BusinessProtection #Fintech #Ecommerce #AvoidScams

35

Payment365 retweeted

Apr 3

we are sure they never worked with a licensed organisation so finexeble get scammed because glodipay miscoded

finexeble there account still waiting on visa and master to take there steps they mention they will investigate glodipay we will wait

1

38

Payment365 retweeted

Apr 4

🚨 Warning from Singapore:

Glodipay (based at 50 Raffles Place) has terrible Trustpilot reviews — merchants calling it a scam, with funds stolen or withheld.

Even GPay options linked to similar shady setups raise major red flags.

Your money deserves better. Stay far away and use established providers only.

#Glodipay #GPay #SingaporePayments #ScamAlert

1

1

101

Mar 31

@Davidddavies1

Mr Davies we should have a talk before broadcasting the podcast your name is mentioned more then several times related to a company how called paytoro.io

we so far are investigating your involvement in there work of scamming merchants for millions

1

1

146

Apr 28

This for sure should ring a bell PaymentFarm, Paytoro, Circoflows, Spectrepay, Smartpaynet

we keep the best one for last

1

60

Apr 20

HIGH-RISK MERCHANTS — RED ALERT! GlodiPay.com aka GPay (Singapore & Vietnam) are the NEXT CROOKS on the payment provider scam list! They let you build huge revenue… then confiscate your funds with completely made-up reasons. Straight-up thieves! Payment365 is exposing these industry scumbags. If you’re a victim — DM us your contact details RIGHT NOW. We WILL expose the REAL people behind this scam. #HighRiskPayments #HighRiskMerchants #PaymentProcessing #MerchantServices #PaymentScam #FintechScam #ExposeTheCrooks #ScamAlert #Singapore #Vietnam

90

Apr 11

🚨 HIGH-RISK MERCHANTS & CRYPTO BUSINESSES — MAJOR SCAM ALERT

Rei Oki (Moonduc Ltd) and his connected gateways Yobopay Buzipay are scamming merchants in the high-risk payment industry.

They withhold payouts currently stole funds from a number of merchants how ask us for help they invent fake excuses even when blockchain proves crypto token delivery.

Multiple merchants already affected. Do NOT use these gateways.

Stay safe. Verify before you integrate.

#HighRiskPayments #PaymentGateway #Yobopay #Buzipay #CryptoPayments #FintechScam #ScamAlert #MerchantWarning #Chargeback #PaymentProcessor

93

Apr 11

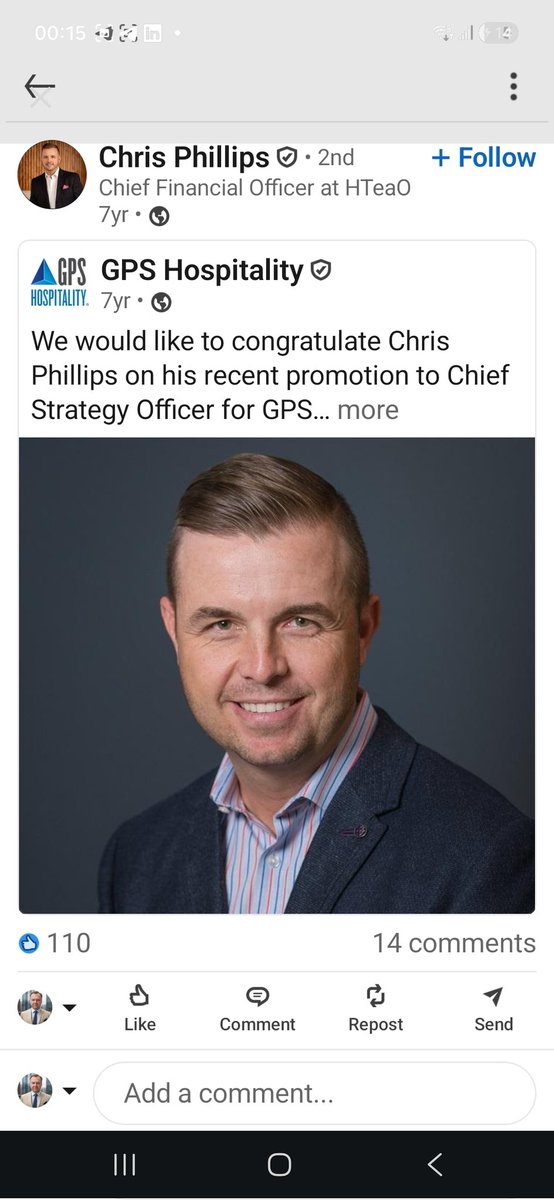

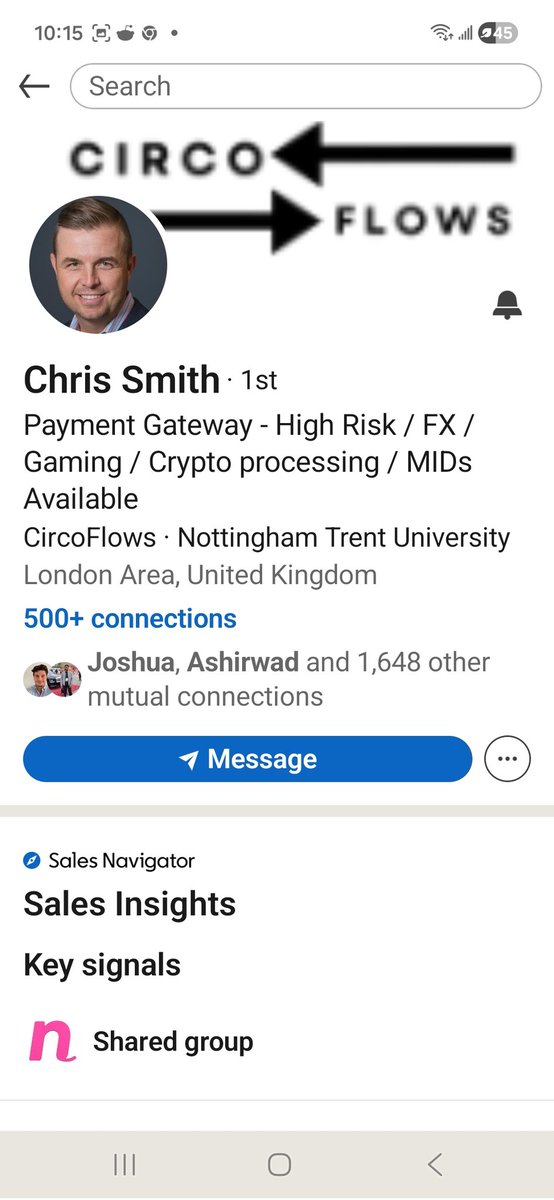

🚨 URGENT MERCHANT SCAM ALERT 🚨

Scammers at CircoFlows (and PG Paytech) are using STOLEN IDENTITIES on LinkedIn to trap merchants with fake “high-risk” payment gateways.

PROOF (attached):

The exact same professional photo belongs to the real Chris Phillips — Chief Strategy Officer at GPS Hospitality (later CFO at HTeaO).

Scammers turned it into a fake “Chris Smith” promoting CircoFlows payment processing for gaming/crypto/FX/high-risk merchants.

They have already stolen MILLIONS.

Merchants: DO NOT engage. Do not pay setup fees. This is a pure setup.

✅ Report both fake profiles to LinkedIn immediately

✅ Warn every merchant group you’re in

✅ Share this now

[Attach first image: GPS Hospitality real promotion post]

[Attach second image: Fake “Chris Smith” CircoFlows profile with arrows]

#ScamAlert #LinkedInScam #PaymentFraud #CircoFlows #PGPaytech #HighRiskPayments #MerchantWarning #IdentityTheft #FraudAlert #PaymentGatewayScam

2

1

103

Apr 11

the last name used has been paytoro they keep setting up store fronts to scam Merchants

84