Senior Integration Engineer - DevRel @morpho, the open credit network for the world

Joined September 2022

- Tweets 1,214

- Following 2,483

- Followers 1,490

- Likes 10,842

144 Photos and videos

Morpho Association has raised $175M to build the open credit network for the world.

Co-led by @paradigm, @a16zcrypto, @RibbitCapital with strategic participation from @apolloglobal, @vaneck_us, @circle_ventures, and @Ledger @Cathayinnov.

The round also included participation from @variantfund, @wmt_ventures, @preludexyz, @IOSGVC, @HashKey_Capital, @sbigroup, @Bpifrance, @mirana, @bamazizimesh, NJJ Capital and 10 other strategic partners.

The funding will help accelerate Morpho's position as the foundation for onchain credit.

257

118

1,112

770,138

Tom - Morpho 🕛 retweeted

Jun 3

We’re redefining how the world gets paid.

Introducing the Deel stablecoin wallet allowing contractors to hold earnings in DLUSD, earn rewards and spend anywhere.

All on @deel.

Big thanks to our partners at @Stablecoin @privy_io @tempo @Morpho @SentoraHQ for making this possible.

20

15

108

18,748

.@deel Stablecoin Wallet, powered by Morpho

Deel puts dollar-backed balances into the hands of contractors in Latin America. Morpho now enables those balances to earn onchain rewards via @SentoraHQ curated Morpho Vaults on @tempo

28

27

263

39,634

Jun 3

Any WDK integrator can now leverage the module we built, on top of the audited morpho sdk! Let's goooo

You can implement earn & borrow capabilities in only a few lines of code!

Integrate Morpho via @WDK_tether

A simple path to embedding onchain yield and crypto-backed loans into any wallet, app, or agentic flow with a few lines of code

2

70

Tom - Morpho 🕛 retweeted

May 28

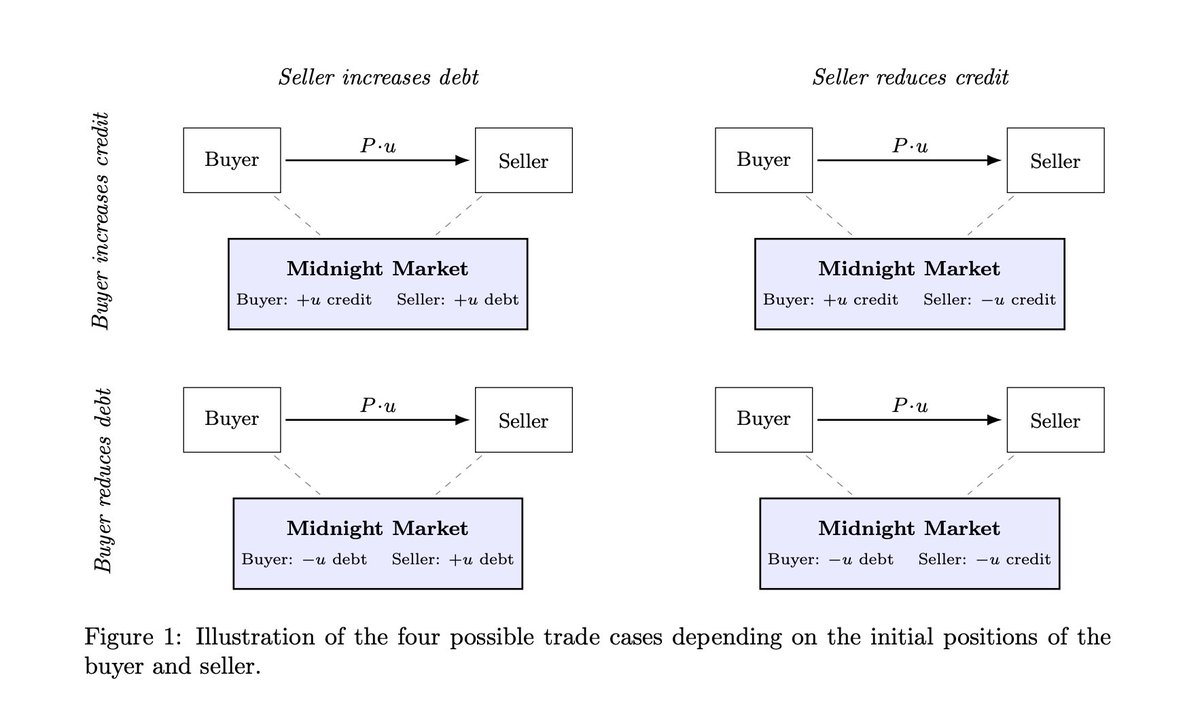

The whitepaper confirms what I've been mapping for a while now: fixed-rate isn't an upgrade to variable-rate lending. It's a different primitive, and @Morpho Midnight shipped the cleanest version of it.

Two details that are doing the work (worth not scrolling past).

1) The maker callback.

- A lender can keep capital deployed in a variable-rate Morpho Blue market and quote a fixed-rate offer on Midnight at the same time.

- The offer locks nothing; when it's filled, the callback pulls the capital and settles in the same transaction. Until then, nothing sits idle.

That one mechanic dissolves the problem that killed every prior attempt. @term_labs spent three years learning that fixed-term markets cold-start at every maturity, because capital has to be committed upfront with no certainty of a fill.

Midnight makes the quote free. Liquidity sourced only at execution, so a market can function before flow exists.

It also makes @AnthonyBowman43's argument literal: good fixed-rate quotes need great variable-rate markets underneath. Here they're mechanically linked, the maker earns variable while quoting fixed. Capital does two jobs.

2) There's no separate lend / borrow / repay / withdraw.

- There's one action. Trade a unit at a price, and whether you're lending, borrowing, entering, or exiting is just emergent from your net position.

- New loan, lender cashing out, borrower handing off debt, two positions cancelling: same mechanical trade, four outcomes.

That collapses primary issuance and secondary trading into a single primitive. It's also the answer to the oldest knock on fixed-rate, that a fixed position is a frozen position.

On Midnight every position is always tradable, because origination is the secondary market: same maturity, fungible unit, one book.

And it's intent-based, not a CLOB. No protocol queue, no reserved capital, routing off-protocol. That's the "route to where liquidity lives, don't pool it" thesis @dionchu has been making, now as base architecture.

For institutions, this is the rate axis closing.

Fixed rate fixed term immutable base optional gates = the four things a risk committee needs to actually allocate.

Pair it with tranching on the loss axis and PB on the counterparty axis, and the TradFi structured-credit toolkit is reassembling onchain.

Primitive by primitive.

The curve is starting to exist. That's a big unlock.

Kudos to the entire morpho team.🦋

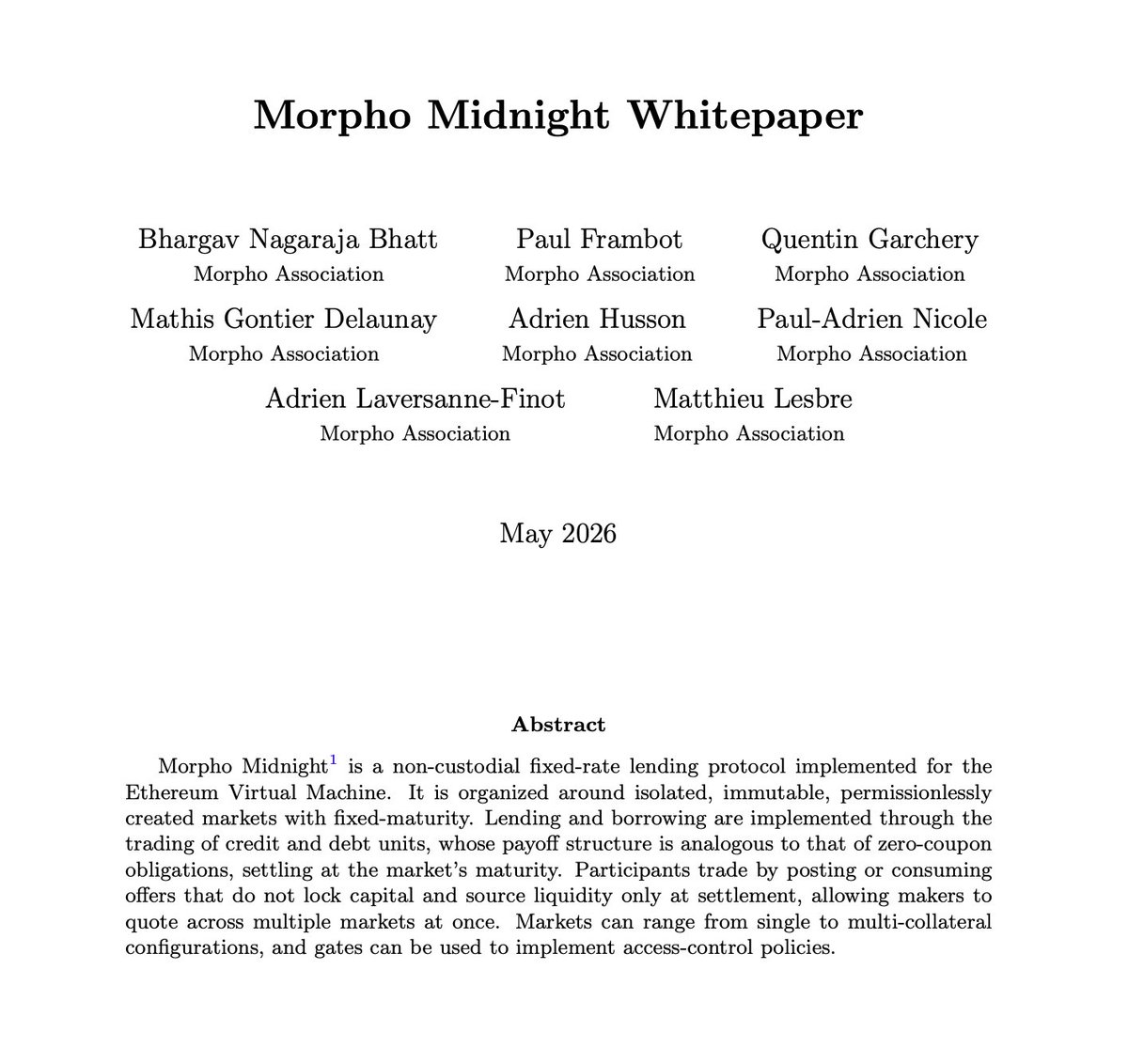

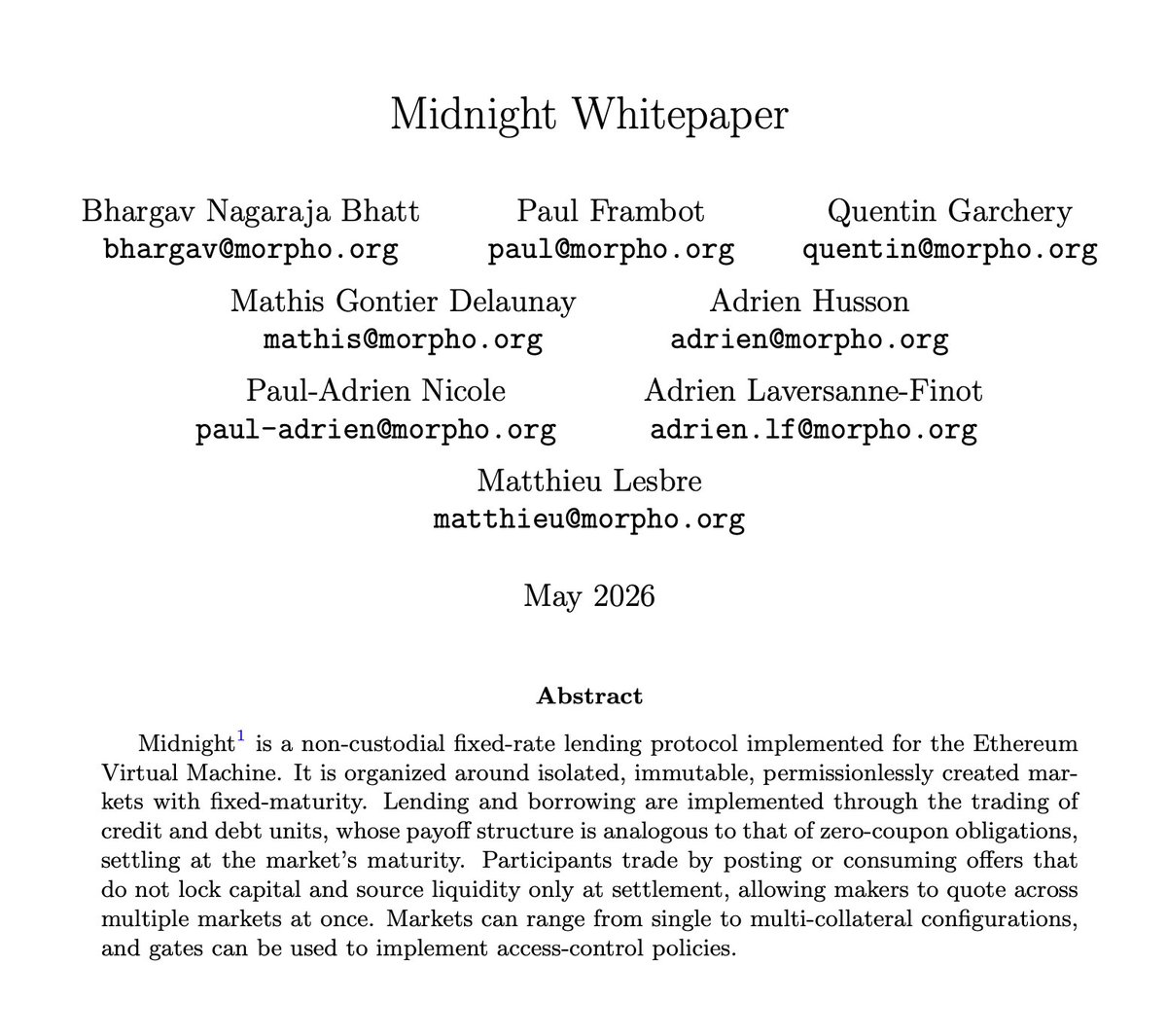

The Morpho Midnight Whitepaper

A noncustodial protocol for fixed rate, fixed term credit markets

morpho.org/whitepapers/midni…

4

10

67

7,963

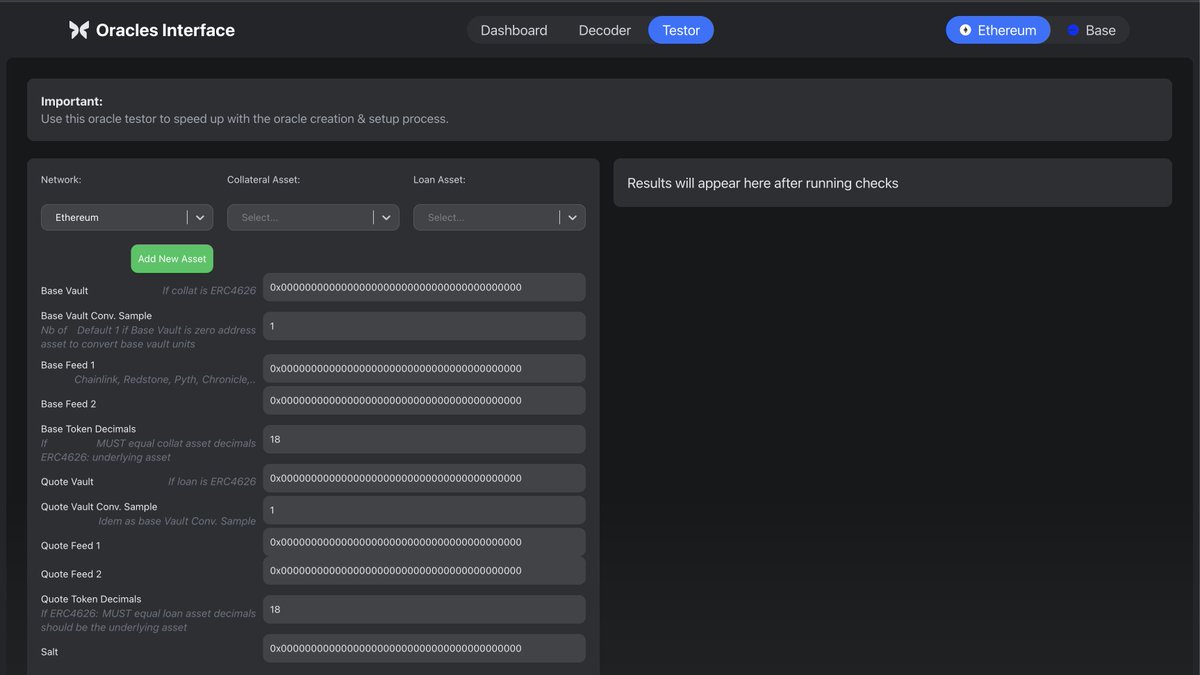

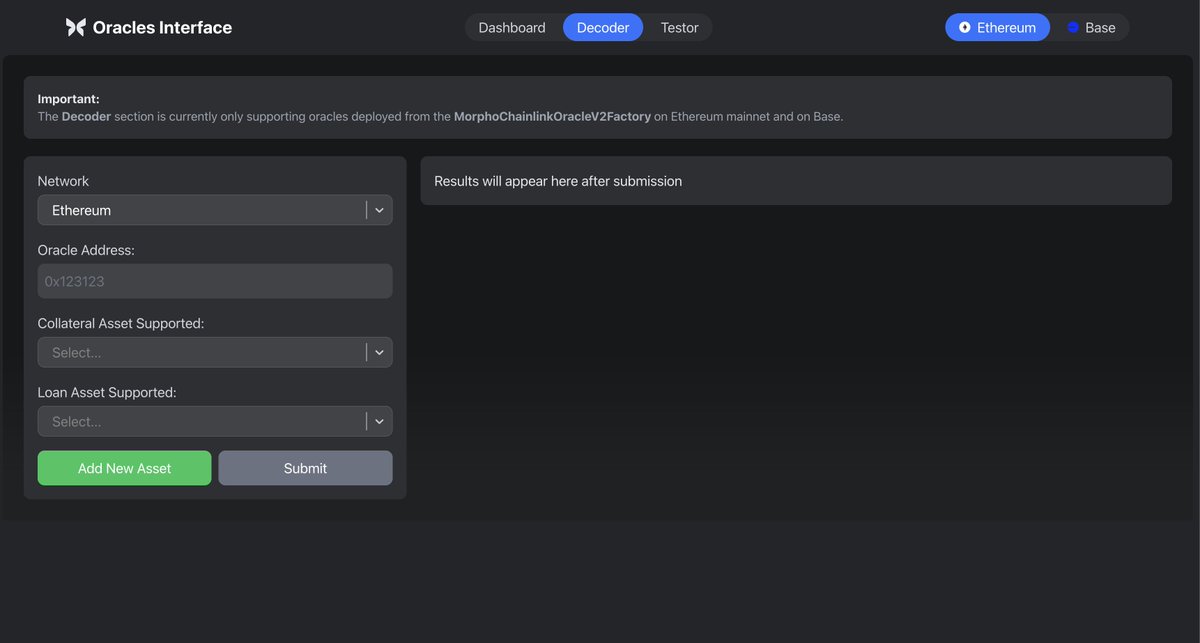

The Morpho Midnight code base is now public

github.com/morpho-org/midnig…

5

18

192

45,603

The Morpho Midnight Whitepaper

A noncustodial protocol for fixed rate, fixed term credit markets

morpho.org/whitepapers/midni…

46

107

744

376,951

Stablecoin Yield in @Trezor Suite, powered by Morpho

Trezor is bringing noncustodial yield curated by @SteakhouseFi to its 2M users, adding to existing on/off ramp, swap, and staking services, making Trezor Suite a complete hub for onchain finance.

16

17

124

23,247

May 28

🕛

The Morpho Midnight Whitepaper

A noncustodial protocol for fixed rate, fixed term credit markets

morpho.org/whitepapers/midni…

1

27

Tom - Morpho 🕛 retweeted

May 19

This is our 9th year in crypto

Nine years providing liquidity and staying active through every market condition

Today we're launching Armitage

Our take on vault curation, starting with two USDC vaults on @Morpho

46

39

490

105,645

Armitage, the new @wintermute_t vault curation team, joins Morpho as a curator.

Through Armitage, Wintermute brings its trading and risk management expertise to the Morpho network.

14

4

77

21,038

Tom - Morpho 🕛 retweeted

May 14

Many people have asked me why Morpho has not been more aggressive in positioning our model against existing ones over the past month.

Recent events have made the case for Morpho obvious: permissionless, isolated lending markets are the only architecture that can scale onchain finance safely.

That said, crypto sadly has a reputation of being brutal, toxic, and full of grave dancing. But this is not us. It’s not the brand we want to build with Morpho. Nor is it the impression we want people to have of crypto.

A brand is defined by the actions you take, in the eyes of the people who matter most to you. And most people who matter to us already understand why Morpho is different… and if they did not, we explained in private, not on twitter.

We have deep confidence in ourselves, model, and our mission. We don't need to tear others down to prove it.

33

21

366

34,684

Tom - Morpho 🕛 retweeted

Apr 30

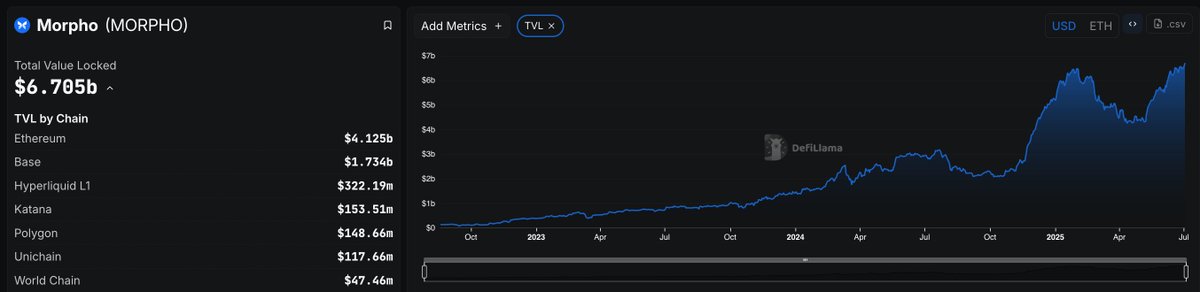

Very good month for Morpho's net TVL despite market events!

7

5

88

6,603

Tom - Morpho 🕛 retweeted

Apr 29

For a long time, people have conflated 'DeFi' with 'trustless finance.'

But 'only-up' technology doesn't exist. Claiming you'll never take a loss and will always have liquidity is foolish, if not dangerous.

In 2023, I wrote 'The Two Paths Ahead for DeFi: Decentralized Brokers vs. Protocols.' The core idea: what can be trustless isn't the finance/brokerage part. It's the tech, the infra, the protocol.

Finance is fundamentally probabilistic. When you finance people, risk is the product. The technology, though, can be deterministic.

This is this observation that led to launch @Morpho Blue as permissionless and isolated lending infrastructure.

DeFi is not a product. DeFi is infrastructure. Infrastructure that should empower existing underwriting models and bring them onto an open network, fostering more competitive pricing and better accessibility for end users. That's it.

23

11

148

11,757

Tom - Morpho 🕛 retweeted

Apr 27

Spent the last week calling the largest institutions to get their read on the DeFi situation.

Key takeaways:

1- Institutional interest isn't going away, for a simple reason: distributors aren't going away. Massive AUM, payments, and loans are coming onchain. Every fintech wants to move fully onchain. As an institution, you don't have a choice.

2- That said, they've completely lost trust in pool/hub models. Institutions and distributors want control: over the code, over the risk, over the compliance. With the flexibility to isolate what they want, while plugging into the global network of liquidity that's compatible with them.

The promise of an open financial system is too big to fail: not because of ideology, but because it's going to create an immense amount of value for everybody involved.

63

44

486

89,023

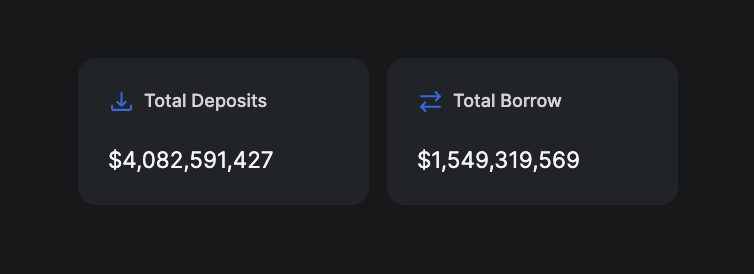

Apr 23

Just crossed $4B in deposits on @base. 🦋

As an integration engineer, watching giants like Coinbase route their user-facing products through Morpho is surreal. But they didn't just choose morpho infra for the liquidity; they chose the architecture.

1

4

117

Tom - Morpho 🕛 retweeted

Apr 16

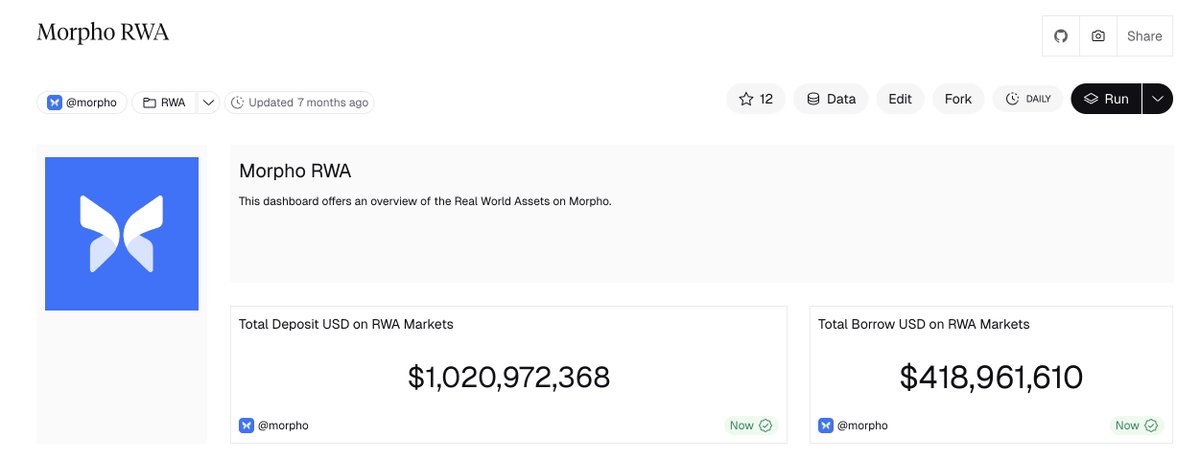

🚨TOTAL RWA DEPOSITS HAVE NOW CROSSED 1 BILLION US DOLLARS ON @Morpho🚨

thank you for your attention to this important matter

3

2

57

1,586

Earn on Fireblocks, powered by Morpho

$200B in stablecoins flow through @FireblocksHQ monthly, but none was put to work. Until today.

Fireblocks brings stablecoin yield opportunities by trusted institutional curators, such as @SentoraHQ, to its 2,400 enterprise customers.

14

18

130

22,689