The blockchain for payments at scale. Live on mainnet.

Joined September 2006

- Tweets 485

- Following 1

- Followers 89,882

- Likes 714

53 Photos and videos

Tempo retweeted

The @mpp Hackathon tracks are here - $15,000 prize pool 🏆

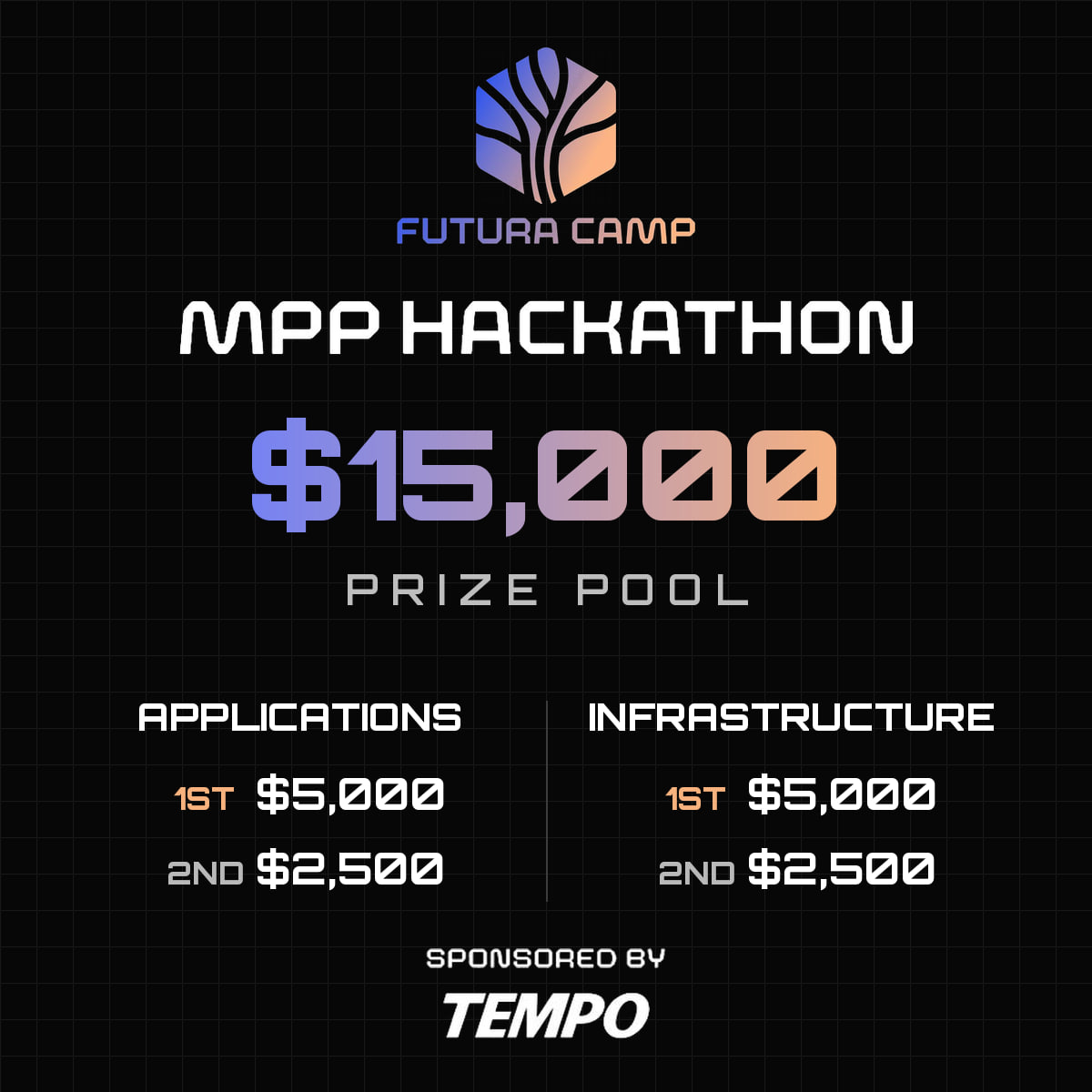

Judged and sponsored by @tempo:

🚀 Apps: $5,000 🥇 / $2,500 🥈

🛠 Infra: $5,000 🥇 / $2,500 🥈

Build the future of agentic payments, live at Futura.

Apply: join.futura.camp/mpp-hackath…

10

20

141

8,269

Maple is now live on Tempo

Jun 11

Maple is live on @tempo, bringing institutional yield opportunities to fintechs building on their network.

Fintechs building payments and payouts on Tempo hold stablecoin balances that earn nothing while they sit.

Maple puts that idle float to work.

5

2

66

6,119

Build on Tempo and MPP with free @Quicknode requests

Jun 11

1,000,000 free requests per month, per agent, now available with @MPP on Quicknode. No account, no API keys. Pay with a stablecoin and query 140 networks.

Refreshes every month.

3

10

75

6,582

Tempo retweeted

Jun 10

At Stripe, we're empowering agents to become buyers

We launched @mpp with our friends at @tempo to enable businesses to programmatically sell to agents

Excited to see Mastercard invest in agent-led payments, and looking forward to working with them on MPP!

Jun 10

As AI agents begin to act, payments move into the background — at machine speed and massive scale.

Today we’re introducing Mastercard Agent Pay for Machines — bringing structure, governance, and trust to this new class of payments.

Launching with 30 partners to bring this to life from day one.

This isn’t just more payments. It’s a new operating model for commerce.

👉 Learn more: mastercard.com/us/en/news-an…

7

8

68

11,869

Agentic commerce needs open standards at the protocol layer and open settlement rails underneath.

We're excited to work with @Mastercard to make their new Agent Pay service compatible with the Machine Payments Protocol (@mpp), with Tempo providing stablecoin settlement for agent-driven payments at scale.

15

14

166

10,925

Learn more: x.com/Mastercard/status/2064…

Jun 10

As AI agents begin to act, payments move into the background — at machine speed and massive scale.

Today we’re introducing Mastercard Agent Pay for Machines — bringing structure, governance, and trust to this new class of payments.

Launching with 30 partners to bring this to life from day one.

This isn’t just more payments. It’s a new operating model for commerce.

👉 Learn more: mastercard.com/us/en/news-an…

1

17

3,294

Tempo retweeted

Jun 9

new stack pushed on neobank.build

Pretty incredible selection of providers by @Bouazizalex and team

Jun 3

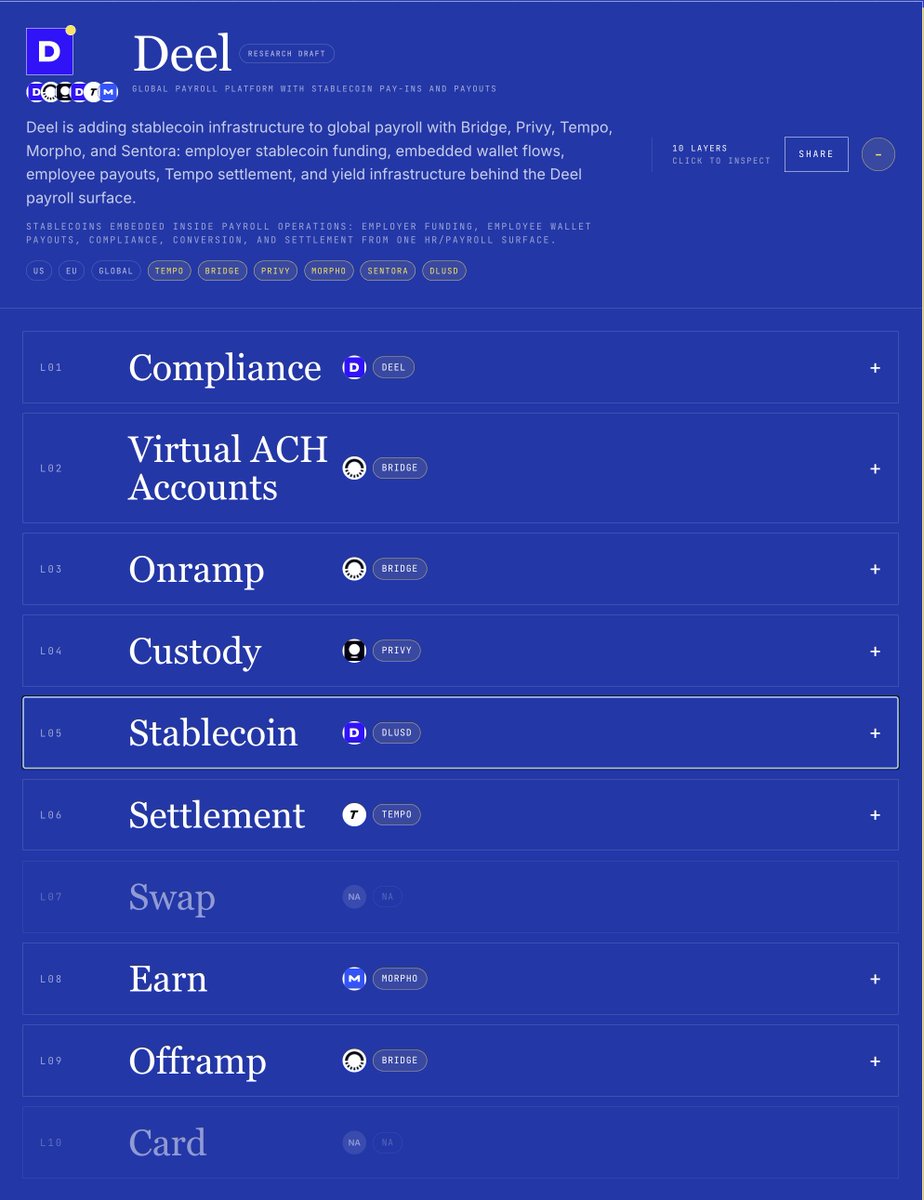

For the first time, contractors can get paid, hold, earn and spend, all inside the same app 💸

Introducing the Deel stablecoin wallet: hold earnings in DLUSD, earn rewards, spend anywhere, with no crypto exchange, separate accounts, or lost value in transit.

Launching in Latin America today, with APAC, MENA, and Africa to follow.

Coming soon for employees! 👀

Thanks to our partners at @Stablecoin, @privy_io, @tempo, @Morpho, and @Sentora for making this possible.

Read more in the comments 👇

13

6

86

22,048

Morpho Association has raised $175M to build the open credit network for the world.

Co-led by @paradigm, @a16zcrypto, @RibbitCapital with strategic participation from @apolloglobal, @vaneck_us, @circle_ventures, and @Ledger @Cathayinnov.

The round also included participation from @variantfund, @wmt_ventures, @preludexyz, @IOSGVC, @HashKey_Capital, @sbigroup, @Bpifrance, @mirana, @bamazizimesh, NJJ Capital and 10 other strategic partners.

The funding will help accelerate Morpho's position as the foundation for onchain credit.

254

119

1,111

768,805

Tempo retweeted

Jun 9

.@deel just launched a stablecoin wallet for LATAM contractors.

In Argentina, 85% of contractors chose USD over pesos last year. Now those dollar balances can earn yield.

RedStone is the data layer that makes it possible.

21

17

104

7,943

Tempo retweeted

Jun 8

Are traditional banking hours still fit for a global economy?

"Bank holidays are not a thing for stablecoins. Weekends are not a thing for stablecoins."

@sytaylor on how stablecoins are helping businesses solve a real operational challenge: moving capital when traditional banking infrastructure isn't available.

As adoption accelerates across payments, treasury, and financial infrastructure, 24/7 money movement is becoming less of a nice-to-have and more of an expectation.

#Stablecon

1

4

20

3,137

Tempo retweeted

Jun 9

A simple rubric for stablecoins vs tokenized deposits.

Tokenized deposits are money that rests. Stablecoins are money that moves.

Tokenized deposits cannot exist outside the bank, but can attract yield (easier), have no off-ramping issues, and handle unlimited volume. Typically, large corporations also receive preferential lending rates for parking large amounts of deposits with a bank.

Stablecoins can exist on ANY platform with a compatible wallet, in ANY country, instantly. They’re more open-loop and not stuck inside the walls of one organization.

These are not the same value proposition.

They're not in competition with each other.

Regulators and banks think tokenized deposits are better. Stablecoin proponents think stablecoins are better. The reality is they're a trade off between risk and speed.

And, counter to the bank lobby or crypto lobby narrative. Stablecoins are good for some banks. Standard chartered, SoFi, Coastal Community Bank and countless others are using stablecoins for cross-border payments, sponsoring card programs and even just lowering their own costs.

So here's a fairer assessment of the differences:

17

19

122

17,915

"Ecommerce today was built for humans. Humans browse websites, click pricing pages, enter cards, and navigate checkout flows. Agents do not do any of that.

They need a programmatic way to understand that a service requires payment, what it costs, and how to pay without a human clicking through a checkout UI."

Why we built @mpp with @stripe, and what we're seeing thus far:

20

8

100

9,229

Tempo retweeted

Jun 8

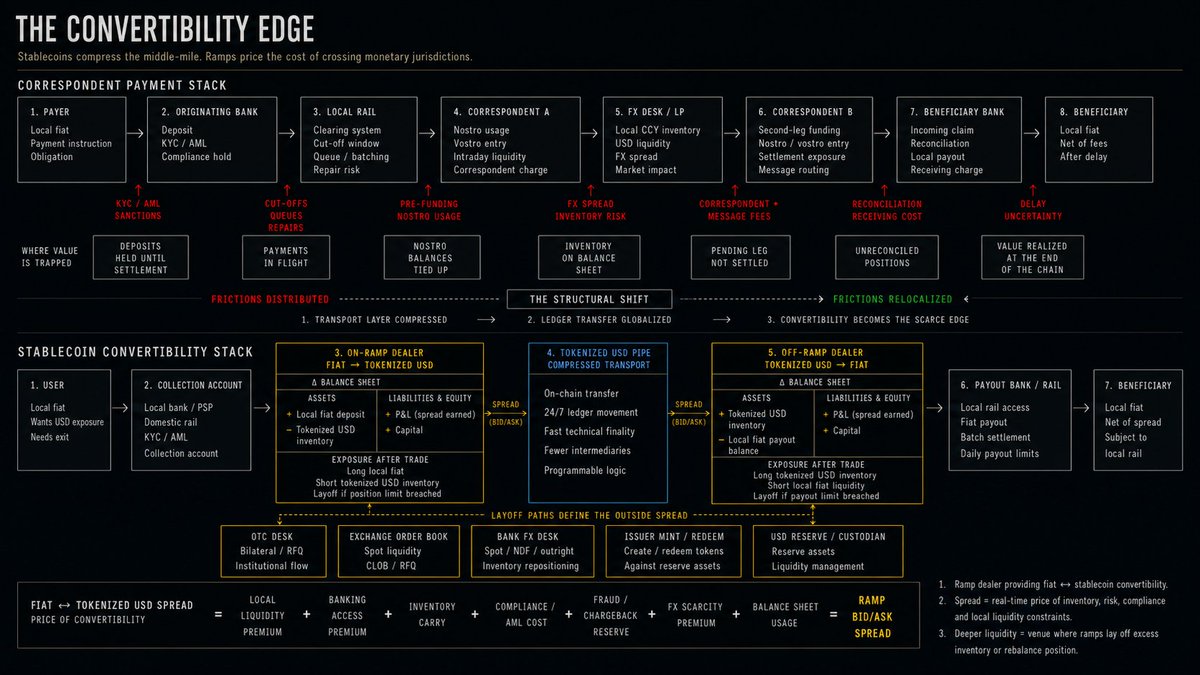

The stablecoin on/off-ramp must be understood as a dealer function situated at the boundary between two monetary hierarchies.

Stablecoins compress the transport of money: they reduce latency, intermediaries, reconciliation, and settlement frictions within the tokenized domain. However, they do not eliminate the scarcity of local convertibility. Instead, they displace it toward the edges.

Consequently, the ramp spread is the compressed price of an entire stack of constraints: fiat liquidity, banking access, inventory, compliance, fraud, regulation, FX scarcity, balance sheet capacity, and the cost of offloading positions into deeper layers of liquidity.

In the traditional system, these costs are distributed across correspondent banks, FX desks, domestic rails, payment intermediaries, and nostro/vostro structures. In the stablecoin model, many of these frictions condense into a single quote: the price at which local currency can be converted into tokenized dollars, or tokenized dollars into local currency, with size, speed, and certainty of execution.

This price is a form of jurisdictional basis. It does not merely measure the cost of moving money; it measures the difficulty of crossing a monetary border. In liquid, open jurisdictions, this basis will tend to compress due to competition. In jurisdictions with capital controls, dollar scarcity, inflation, banking fragility, or regulatory risk, the spread may persist because it essentially prices sovereignty, balance sheet capacity, and access.

Thus, stablecoins may commoditize global settlement, but they make local convertibility more valuable. They decentralize transport, yet they can recentralize economic rent at the points of entry and exit.

What this allows is that, provided the players operating these tolls are ultra-efficient, the aggregate cost of the overall structure could be driven down.

Therefore, the structural business is not simply moving stablecoins. It is market-making across incompatible monetary systems. The winner here will be whoever controls the scarce constraint within each respective corridor: licensing, banking access, local liquidity, distribution, compliance, or balance sheet capacity.

Stablecoins compress settlement. Ramps price convertibility. The spread is the market price of crossing monetary jurisdictions.

17

21

184

28,209

Come hack on agentic payments with @mpp at ZuBerlin 2026.

June 14-20. Limited spots. Apply below:

join.futura.camp/mpp-hackath…

The MPP Hackathon is here. 🚀

Build together the future of agentic payments, supported by @tempo as main sponsor, helping developers move from idea to implementation faster.

Full free ticket to futura.camp for all hackers 🎟️

Apply now: join.futura.camp/mpp-hackath…

7

8

45

4,922

Tempo retweeted

Kraken Institutional is proud to be @Tempo's US centralized exchange partner 🤝

Payment platforms, neobanks, stablecoins on Tempo get support for liquidity, on/off-ramps, custody, listings, and execution.

blog.kraken.com/product/360/…

16

9

64

11,852

Kraken is the first U.S. centralized exchange to support Tempo.

Teams building payments products on Tempo can now access liquidity, custody, on/off-ramps, execution, and listings support all in @KrakenInsto

11

13

147

8,887

Read more: tempo.xyz/blog/kraken-and-te…

1

8

1,765