Crypto Enthusiast • Web3 Guy • Defi • AI • RWA • Gamefi • Multichain Analysis • Marketing Strategist • NFA • Threador 🧵🦅

Joined November 2010

- Tweets 22,540

- Following 2,362

- Followers 21,982

- Likes 32,966

977 Photos and videos

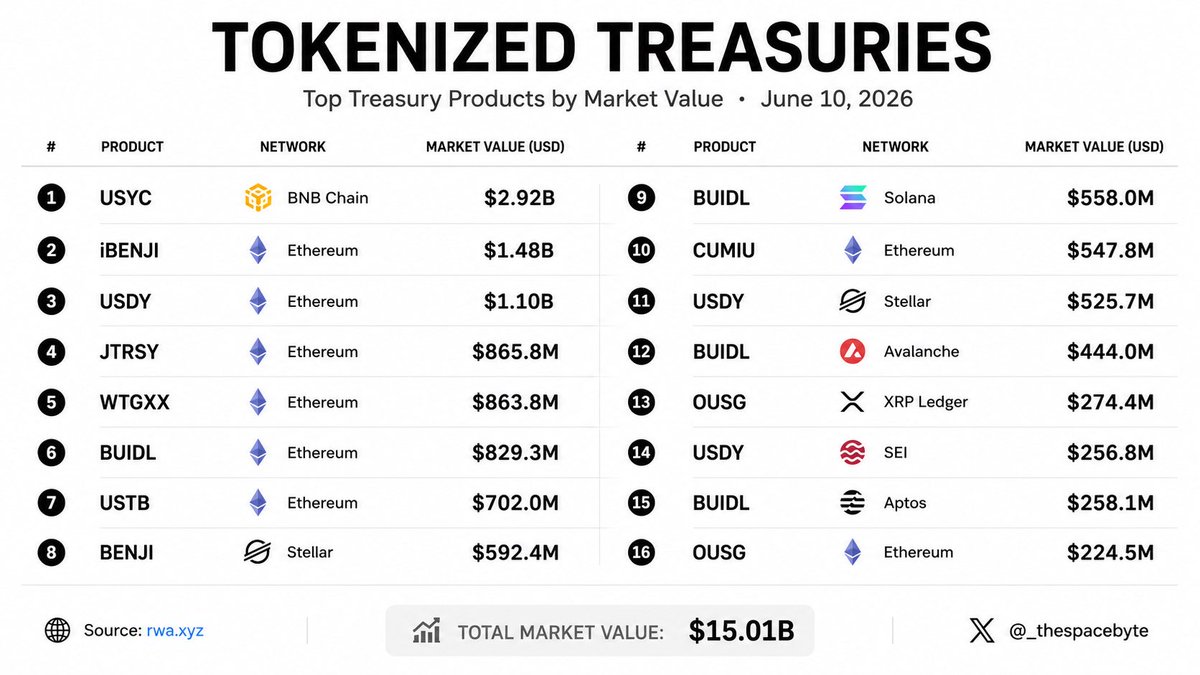

Six products control more than half of tokenized Treasury value.

BUIDL. BENJI. OUSG. USDY. WTGXX. mUSD.

Looks a lot like DeFi market structure in 2020.

Uniswap, Curve, Balancer, and SushiSwap had the same grip on liquidity.

Then fragmentation arrived.

New entrants undercut fees, expanded collateral types, and captured demand incumbents weren’t serving.

WisdomTree just received SEC approval for 24/7 secondary market trading with USDC settlement.

That’s the wedge.

Not another tokenized Treasury product.

A liquidity mechanism the largest funds don’t have yet.

Watch whether WTGXX pulls allocators that existing fund structures don’t serve.

Concentration always looks permanent until a new access model emerges.

This time, the unlock looks more like market infrastructure than yield competition.

16

2

37

366

Jun 13

Was expecting the USD1 campaign on @binance to end soon, but they just extended it to June 26.

178M $WLFI still up for grabs.

What I like most is how straightforward it is:

Hold USD1 → earn WLFI.

No extra steps. No complicated requirements.

Just keep holding.

Jun 12

We didn't stop.

178M $WLFI allocated to the $USD1 campaign on @binance, now EXTENDED through June 26.

Rules haven't changed → HODL 🦅☝️

details via @binance

binance.com/en/support/annou…

111

2

121

5,434

spacebyte ⛓ retweeted

Jun 13

.@worldlibertyfi is proud to serve as a presenting sponsor for the @ufc Freedom 250 event 🦅. We have added a $250 k $USD1 fighter of the night bonus ☝️. @danawhite

277

552

9,901

15,708,014

spacebyte ⛓ retweeted

Jun 11

5

4

16

1,170

spacebyte ⛓ retweeted

Jun 12

1/ Crypto adoption is entering a new phase.

For years, digital assets were largely viewed as experimental, speculative, or institutionally inaccessible.

But that narrative has changed meaningfully. BTC and particularly ETH, are increasingly being integrated into the product suites of major financial platforms, treasury companies, funds, and institutional trading venues.

As $ETH adoption deepens, the next question becomes less about whether institutions want ETH exposure, and more about how they should manage it.

Holding $ETH passively gives investors exposure to its long-term upside. But ETH is also a productive asset via PoS yield. For treasuries, funds, and sophisticated users, this creates an obvious opportunity: ETH should not simply sit idle.

The challenge is that native staking is not always operationally simple.

The rabbit hole goes deep → Validator management, withdrawal queues, liquidity constraints, custody requirements & exchange collateral limitations all create friction.

This is esp. true for institutions, where operational resilience, risk management, and liquidity access matter as much as headline yield.

This is where liquid staking becomes increasingly important.

And in 2026, @mETHProtocol $mETH is positioning itself as one of the key yield layers for ETH 🧵

Jun 11

ETH staking is moving beyond yield alone.

“The next phase is about stronger security, deeper liquidity, and better distribution.” - @Defi_Maestro

Read more below on how mETH Protocol is building for 2026.

35

18

82

4,285

Jun 12

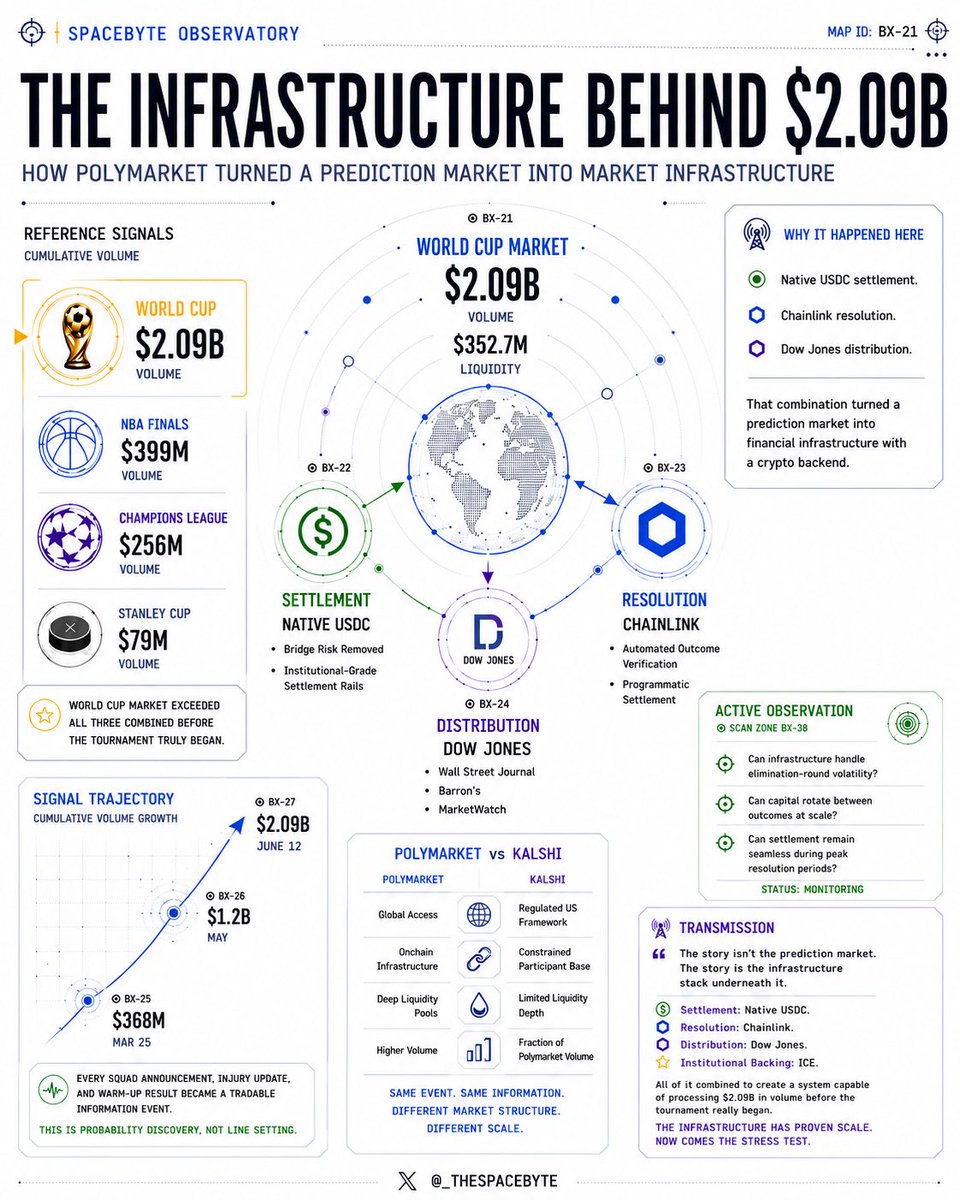

$2.1 billion. Before a single match.

I kept looking for a reason to dismiss that number. I couldn’t find one.

@Polymarket’s World Cup Winner market opened on July 2, 2025. By June 12, it had cleared $2.09B in cumulative volume with $352.7M in liquidity.

The scale becomes clearer when you compare it to:

● NBA Finals: $399M

● Champions League: $256M

● Stanley Cup: $79M

The World Cup market exceeded all three combined before the tournament truly began.

The interesting question isn’t whether $2.09B is impressive.

It’s why it happened here.

Polymarket didn’t win on brand. It won on infrastructure.

Three developments mattered:

● Circle migrated collateral from bridged USDC to native USDC, removing bridge risk and creating institutional-grade settlement rails.

● Chainlink became the resolution layer behind major World Cup prediction markets, enabling automated settlement and payouts at scale.

● Dow Jones integrated Polymarket odds across publications including the Wall Street Journal, Barron’s, and MarketWatch, expanding distribution far beyond crypto-native audiences.

Native USDC settlement.

Chainlink resolution.

Dow Jones distribution.

That combination turned a prediction market into financial infrastructure with a crypto backend.

The volume curve reflects it:

$368M by March 25 → $1.2B by May → $2.09B by June 12.

Every squad announcement, injury update, and warm-up result became a tradable information event.

That’s what makes this different from a sportsbook.

A sportsbook sets a line.

Polymarket continuously discovers probability.

Every new piece of information reprices the market in real time.

Now compare Kalshi.

Same event.

Same underlying information.

Yet volume remains a fraction of Polymarket’s.

The difference isn’t prediction quality. Probabilities are often nearly identical.

The difference is market structure.

One operates inside a regulated US framework with a constrained participant base.

The other is globally accessible, onchain, and connected to a far larger liquidity pool.

Regulation doesn’t just affect compliance.

It affects scale.

Which raises the bigger question.

At what point does Polymarket stop looking like a prediction market startup?

Settlement: native USDC.

Resolution: Chainlink.

Distribution: Dow Jones.

Institutional backing: ICE.

That looks increasingly like market infrastructure.

The $2.09B was accumulated before the tournament really began.

The true stress test comes during elimination rounds, when large positions resolve instantly and capital rotates into surviving teams.

The infrastructure has already handled $2.09B in volume.

Now it has to prove it can handle the chaos that follows.

54

7

90

8,636

Jun 12

The @CFTradercom campaign got everyone talking, but the product is what stood out to me.

Most prop firms make you choose between cheap challenges with impossible rules or fair rules with expensive entry fees.

BREAK simplifies it.

One phase. Up to 90% profit split. On demand payouts. No unnecessary complexity.

50% off with my code: cft-spacebyte

Jun 11

The biggest pain point for prop traders?

The cheap challenges are the ones built to break you. And the fair ones cost too much.

That's why we introduced BREAK accounts:

One phase, low entry, keep up to 90% of your profits and get paid on demand.

Pass once, get funded and BREAK your limits.

44

2

65

5,228

spacebyte ⛓ retweeted

Jun 11

Market Outlok #8

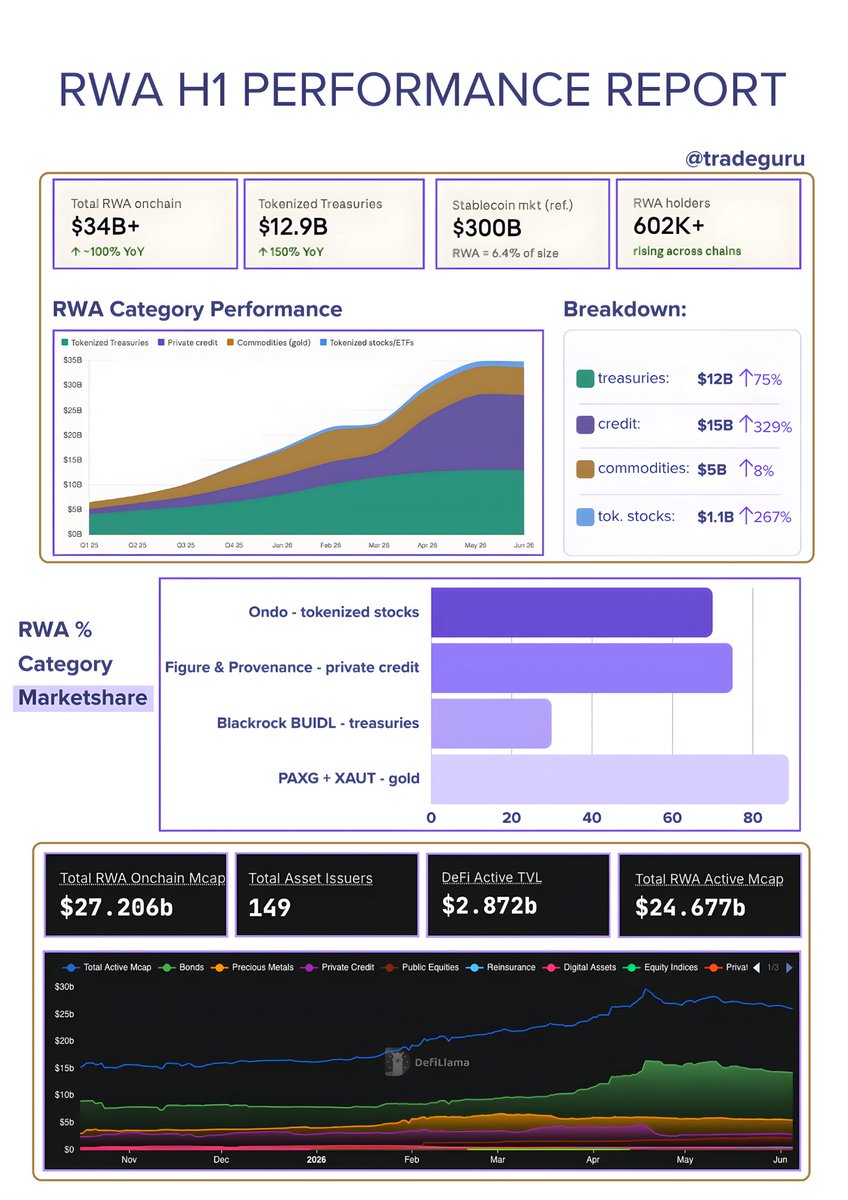

1/8 On-chain RWAs have surpassed $34B, up roughly 100% Year-over-Year.

More importantly, RWA growth is now outpacing stablecoin growth by 6.4%, up from 2.7% in 2025.

The data is becoming impossible to ignore.

A breakdown of where that growth is coming from🧵

May 18

Market Outlook Series #7

1/4 30 days post-Kelp hack, the cross-chain map has redrawn itself.

Solv, Re, Kraken, Lombard, and others, gone from LayerZero. All now live on CCIP.

Despite @PrimordialAA's public mea culpa, L0 has bled $4B in TVL. So why CCIP specifically?

19

23

106

5,049

spacebyte ⛓ retweeted

Jun 11

I’ve always said the best growth strategy is simple:

Give people a reason to use your product, then give them a reason to stay.

That’s exactly what I’m seeing with USD1.

In the last few weeks alone, USD1 has been hard to miss. Binance Earn, Gate, Bybit, lending markets, trading incentives, reward pools, vaults… every time I look up, it seems to be showing up somewhere new.

The latest example came from @Gate.

They just launched a USD1 Flexible Term event offering up to 20% APR with no lock-up, meaning users can earn yield while keeping full flexibility over their capital.

@binance has also rolled out its own USD1 campaign offering up to 10.5% APR on the first $2,000 deposited.

What stands out isn’t the yield itself.

It’s the fact that @worldlibertyfi keeps expanding the number of places where USD1 can actually be used.

At this point, seeing USD1 pop up somewhere new almost feels expected.

One week it’s incentives.

The next it’s lending markets.

Then it’s Binance Earn.

Now it’s Gate.

The expansion has been hard to miss.

The more places people can earn, lend, trade, borrow, and deploy USD1, the stronger the network effect becomes.

That’s why watching USD1 climb the stablecoin rankings hasn’t been surprising.

Growth follows utility.

And utility is exactly what $USD1 keeps adding.

31

4

71

10,245

spacebyte ⛓ retweeted

26

9

48

4,991

Jun 10

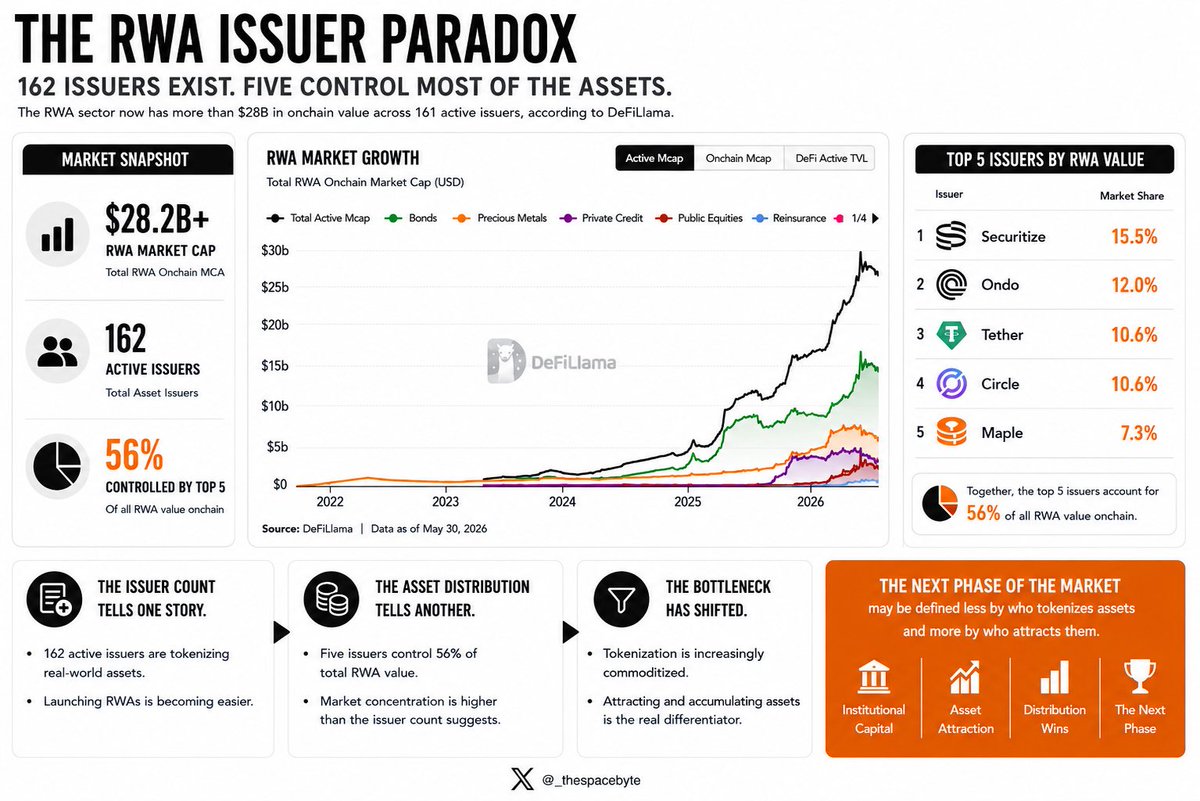

The RWA sector now has more than $28B in onchain value across 161 active issuers, according to DeFiLlama.

The distribution is less broad than the issuer count suggests.

- @Securitize: 15.5%

- @OndoFinance: 12.0%

- @Tether: 10.6%

- @Circle: 10.6%

- @maplefinance: 7.3%

Together, they account for roughly 56% of all RWA value onchain.

The issuer count tells one story.

The asset distribution tells another.

Launching RWAs is becoming easier.

Accumulating assets is not.

The next phase of the market may be defined less by who tokenizes assets and more by who attracts them.

31

3

71

6,412

spacebyte ⛓ retweeted

Jun 10

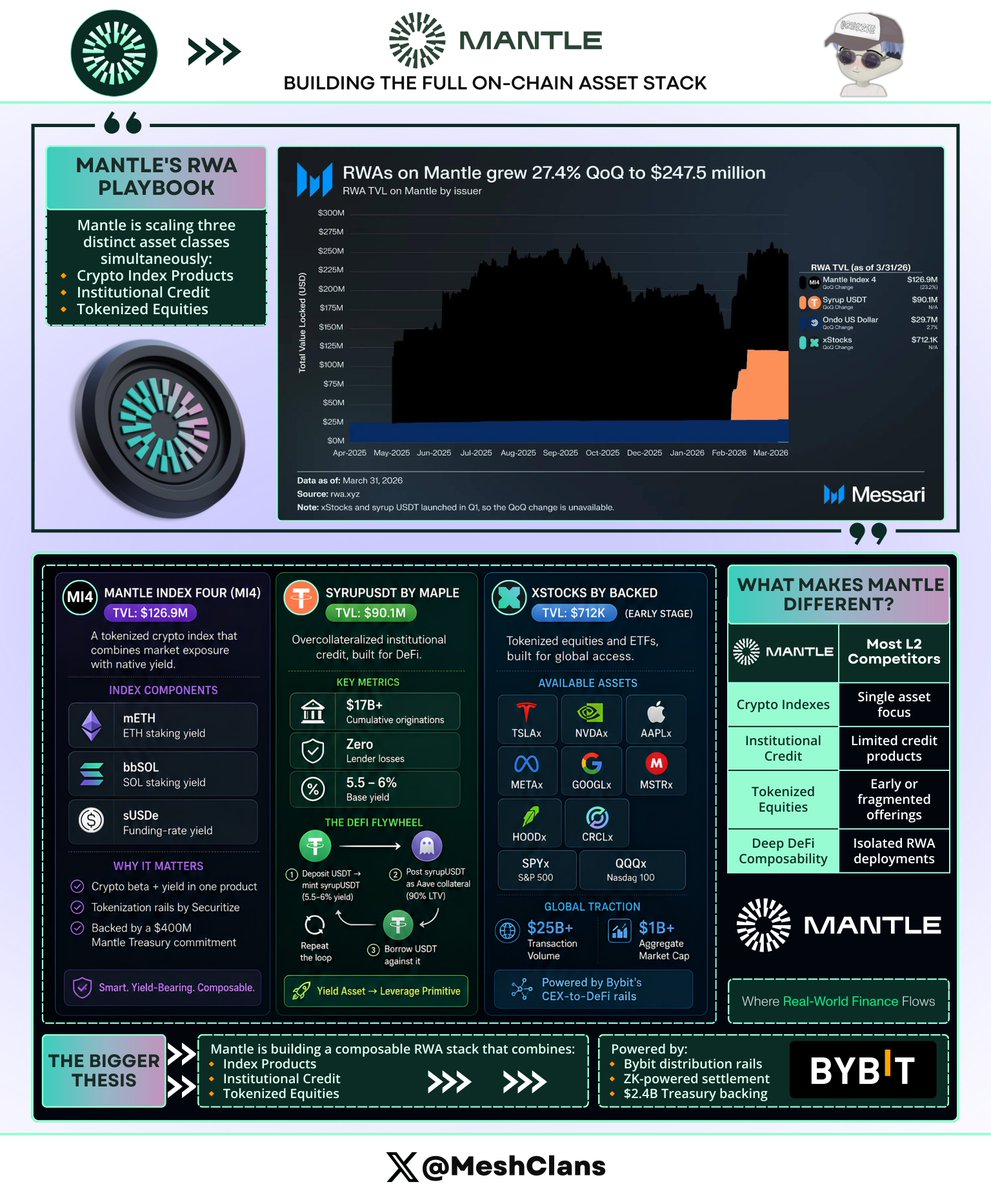

Mantle's RWA ecosystem is doing something most chains aren't, and very few people tracking this space have noticed yet.

The $247.5M TVL with 27.4% qoq growth is only half the story. The more interesting part is how it's built.

Most RWA plays on L2s look like this: one dominant issuer, one asset class, one narrative.

@Mantle_Official 's running three simultaneously across three completely different real-world asset categories, and that architectural decision is what makes this worth paying attention to.

Mantle Index 4 ($126.9M TVL): think crypto S&P 500, except smarter than what TradFi would build. Instead of just holding spot BTC/ETH, MI4 wraps the yield-bearing versions:

- mETH: ETH staking yield

- bbSOL: SOL staking yield

- sUSDe: funding rate arbitrage

So you're getting crypto beta and native DeFi yield inside a traditional fund structure. That combination doesn't exist in TradFi, and that's kind of the whole point.

Securitize built the tokenization rails, Mantle Treasury put up $400M as anchor. This wasn't a small commitment.

syrupUSDT by @maplefinance ($90.1M TVL): overcollateralized institutional credit, over $17B in cumulative originations, zero lender losses. The ERC-4626 structure means it plugs into any DeFi protocol without custom work, which is exactly why it spread so fast.

When Aave listed it as collateral at 90% LTV, the $50M cap filled in hours. I honestly didn't expect it to move that fast. The loop people are running:

- Deposit USDT → mint syrupUSDT (5.5-6% base yield)

- Post syrupUSDT as Aave collateral at 90% LTV

- Borrow USDT against it and repeat

It went from yield instrument to leverage primitive overnight. That's a proven composability story, not just a promising one.

@xStocksFi by @BackedFi ($712K TVL on Mantle, early): tokenized equities on Mantle, structured across Jersey and Switzerland under the Swiss DLT Act, with Kraken's December acquisition making the long-term infrastructure picture a lot cleaner.

The current lineup:

- Single stocks: TSLAx, NVDAx, AAPLx, METAx, GOOGLx, MSTRx, HOODx, CRCLx

- ETFs: SPYx (S&P 500), QQQx (Nasdaq 100)

Bybit's CEX-to-chain rails are what most people are sleeping on here. That distribution flywheel between the world's second largest exchange and Mantle's DeFi ecosystem isn't something most L2s can replicate.

xStocks crossed $25B in transaction volume and $1B aggregate market cap globally by March 2026. The product has proven itself, it's just early on Mantle specifically.

Here's what's overlooked in most RWA coverage. No other Ethereum L2 has institutional credit, a tokenized crypto index, and tokenized equities all live simultaneously at meaningful scale.

The competition isn't really doing the same thing:

- Arbitrum: 2,000 RWA assets but fragmented across dozens of small issuers with no coherent single-chain narrative

- Base: growing retail distribution via Coinbase rails, not DeFi composability

- Stellar: going deep on TradFi compliance, a fundamentally different model altogether

Mantle's building the full stack and betting that composability does the rest.

The Bybit rails, ZK settlement for compliance-sensitive issuers, and a $2.4B treasury that actually convinces institutional issuers to show up rather than deploy elsewhere.

Blockstreet's integration should deepen xStocks liquidity meaningfully, more tokenized funds are coming, and the AI agent angle is genuinely underrated.

As agents need programmable yield-bearing collateral to operate autonomously, this stack starts looking less like a financial product and more like critical infrastructure.

Most chains are building one asset class. Mantle's building the venue.

h/t: @MessariCrypto for the Q1 2026 snapshot.

46

7

75

3,785

Jun 10

Imagine launching a prop firm challenge so well that half of CT thinks a crime happened.

Yeah…

@CFTradercom deserves credit for this one 😂

53

3

74

7,647

Jun 9

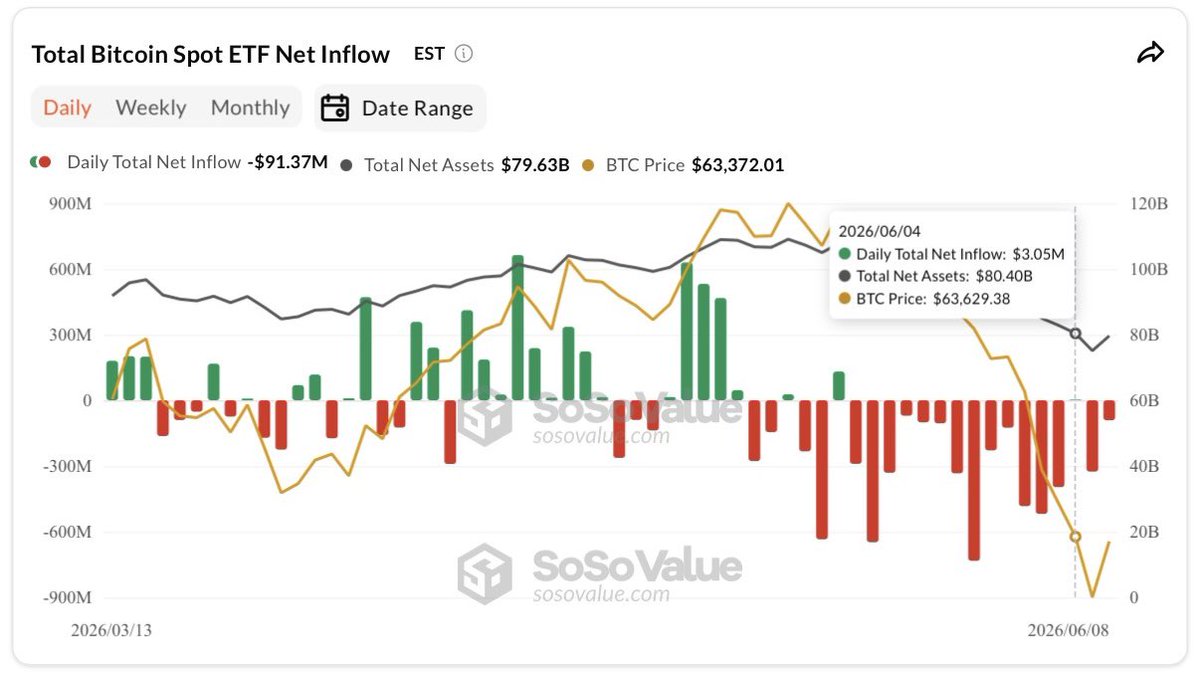

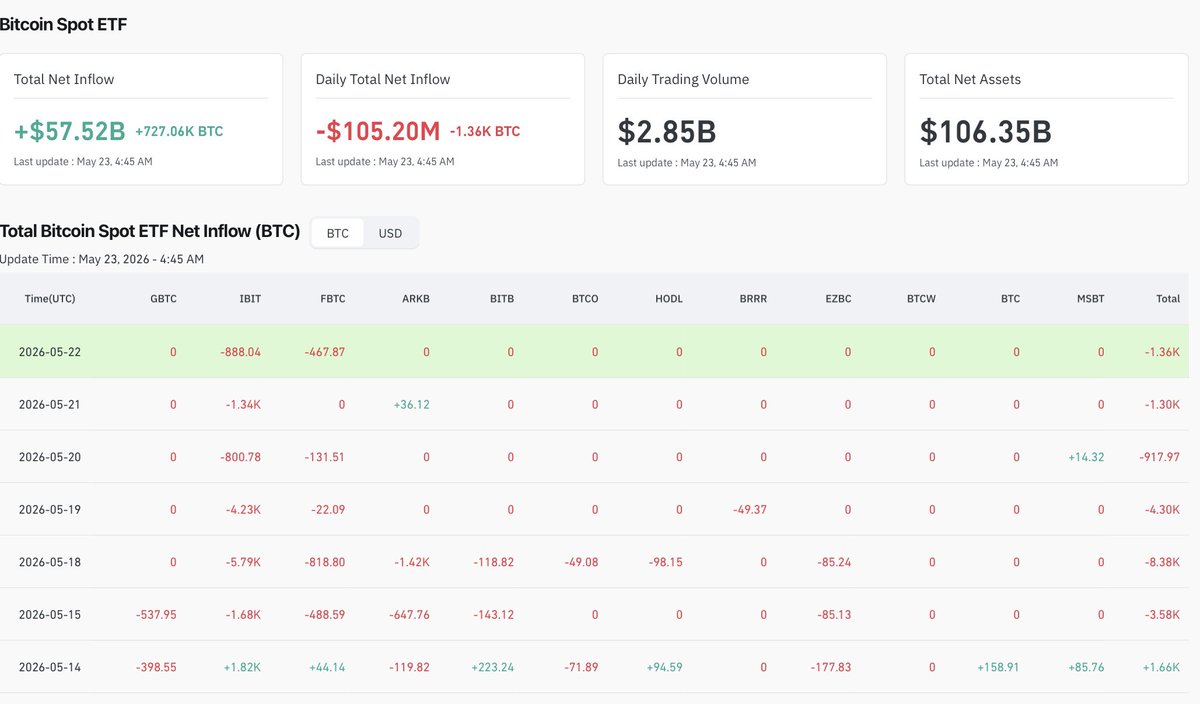

59,351 BTC left U.S. spot Bitcoin ETFs between May 15 and June 3.

According to data reports, that was the largest redemption streak since launch. The 20-day window was even larger: 73,080 BTC and $5.42B of outflows.

The timing is what makes the data interesting.

Just weeks earlier, April had been the strongest ETF month of 2026, attracting $1.97B of net inflows.

Then flows reversed abruptly.

Bitcoin’s fundamentals did not change that quickly.

Macro conditions did.

1. U.S.-Iran tensions escalated.

2. Equity volatility increased.

3. Rate-cut expectations repriced.

The selling appears less like a rejection of Bitcoin and more like a reduction in risk exposure.

That distinction matters.

The original ETF thesis assumed the wrapper would become a permanent source of demand.

Recent flows suggest something different.

ETFs are not a demand channel.

They are a liquidity channel.

Capital enters when risk appetite rises.

Capital leaves when risk appetite falls.

A second data point points in the same direction.

Bitcoin’s one-year whale balance change turned negative during the same period.

• ETF investors reduced exposure.

• Large holders reduced exposure.

Different cohorts. Same behavior.

The June 4 inflow of roughly $3M ended the streak, but it does not answer the bigger question.

The next 4–6 weeks of ETF flow data will.

For most of 2024 and 2025, ETF flows measured adoption.

In 2026, they increasingly measure institutional risk appetite.

That may be the more useful metric.

52

8

138

10,972

Jun 8

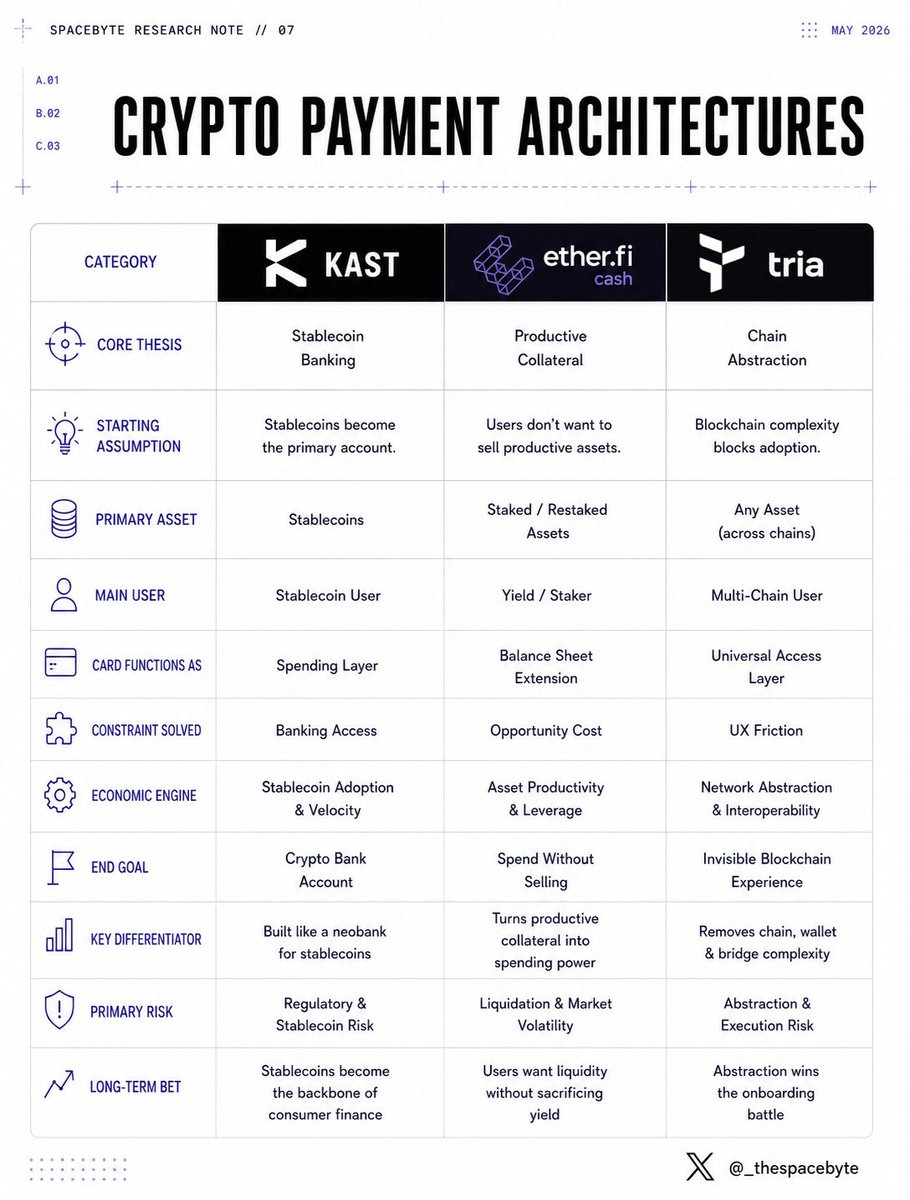

Crypto payments have spent years chasing the same outcome: allowing users to spend digital assets as easily as fiat.

What has changed over the past year is that “crypto payments” no longer means one thing.

Some teams are building stablecoin-native banking products. Others are turning productive collateral into spending power. A third group is focused on abstracting blockchain complexity altogether.

The result is an emerging onchain card stack where products look increasingly similar on the surface but are built on fundamentally different architectures underneath.

___

◢ The Market Is Fragmenting Into Three Models

The first generation of crypto cards functioned primarily as conversion layers.

Users held crypto, assets were converted into fiat, and traditional payment rails handled settlement.

The next generation is different.

Cards are becoming distribution layers for broader financial systems.

Three approaches are beginning to emerge:

- Stablecoin-native banking

- Productive collateral spending

- Chain-abstracted financial access

Kast, EtherFi Cash, and Tria represent each of these categories.

___

1. @KASTxyz

Kast is built around a simple assumption: stablecoins become the primary consumer account.

Rather than treating payments as an extension of investing, Kast treats payments as the core use case.

The strategy aligns with broader industry trends. Stablecoin supply has surpassed $310B, cross-border settlement volumes continue to grow, and payment-focused ecosystems like Solana are increasingly positioning themselves as financial infrastructure.

Under this model, the card becomes the spending layer for a stablecoin-native checking account.

2. @ether_fi Cash

EtherFi Cash starts from a different observation.

Many crypto users hold productive assets they do not want to sell.

Staked ETH generates yield. Restaked assets earn rewards. Liquidating those positions to spend creates opportunity cost.

EtherFi’s solution is to transform productive collateral into spending power.

Rather than converting assets into cash, users spend against assets that remain productive.

The card functions as an extension of a balance sheet rather than a payment account.

3. @useTria

Tria focuses on a different constraint entirely.

Its assumption is that blockchain complexity remains one of the largest barriers to adoption.

Users operate across wallets, chains, bridges, and assets. Every additional decision introduces friction.

Tria attempts to remove these decisions from the user experience.

The objective is not maximizing yield or replacing banks. It is making blockchain infrastructure invisible.

The card becomes a universal access layer across fragmented ecosystems.

___

◢ What We’re Watching

Three products.

Three assumptions.

- Kast: stablecoins become the primary account.

- EtherFi Cash: users spend without selling productive assets.

- Tria: blockchain complexity disappears behind abstraction.

All three solve the same problem through different architectures.

The card looks similar.

The system underneath is entirely different.

72

6

87

10,140

spacebyte ⛓ retweeted

Jun 8

just a sneak peek into the flux dapp 👀

4

3

11

528

Jun 8

Crisis reveals character.

Good to see CFT addressing this head on.

20

3

32

3,923