Joined February 2024

- Tweets 50,798

- Following 1,610

- Followers 3,346

- Likes 79,945

4,282 Photos and videos

Brilliant post covering next week’s macros.

Elon is now freed from the IPO - don’t discount something for $TSLA shareholders.

Cybercab unsupervised?

$SPCX branded Roadster reveal invites?

One the most important macro week of the year is about to start.

Here’s what I’m watching:

→ Warsh’s debut (Tue/Wed)

No rate move expected. That’s not the story. He’s signaled a leaner FED that communicates less. His first press conference is the closest thing we have to a 2026 rate preview.

Watch the language, that’s the decision going forward.

→ Iran deal (this week)

Still unsigned. Still contested.

But the draft includes Iran reopening the Strait of Hormuz within 30 days.

A signed deal removes the energy tail risk AND takes inflation pressure off Warsh’s table simultaneously. Two events. One outcome. Most coverage is missing that connection.

→ $MU earnings (June 24)

Entire 2026 HBM supply already sold out.

The AI memory thesis gets confirmed or cracked on one print.

→ $SPCX post-IPO follow-through

Largest IPO in history just listed. This week tells you whether the institutional demand was real. I’m watching how $RKLB $ASTS $PL trades relative to $SPCX.

Four events.

All connected by the same question: how much risk is this market actually pricing?

-BP

Not financial advice. DYOR.

1

5

710

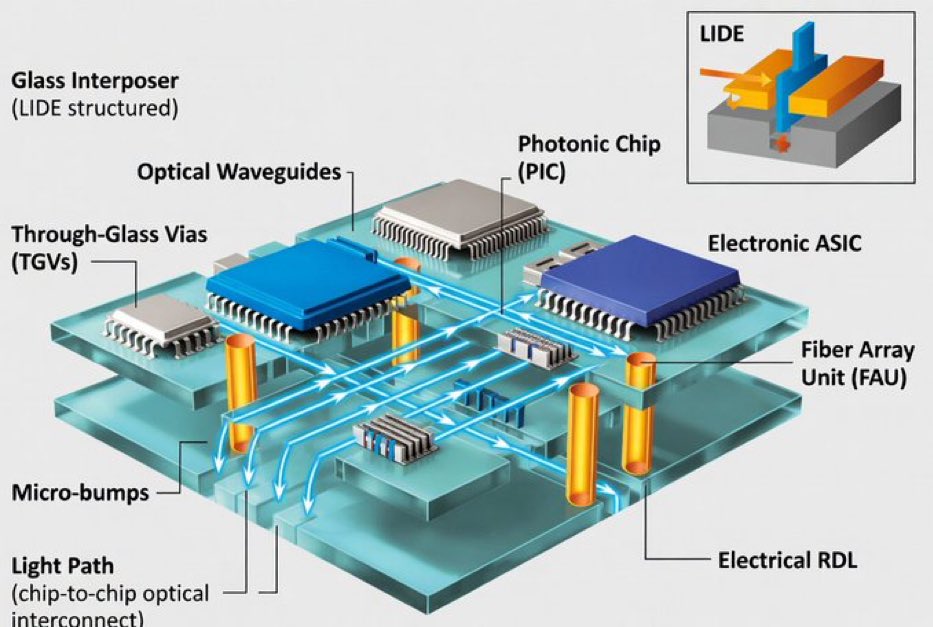

Okay let’s think like Elon setting up Terafab. First principles will firstly ignore photonics and memory.

You need to remove the heat from bigger, faster, harder working chips stupid! Elon knows that which is one reason he likes putting his chips in -270 deg space. Heat mgt was central to DOJO. That demands that we mount the chip to glass.

$LPK LPKF make the machine that laser erodes the cooling channels. The $ASML of glass!

Oh yeah, LPKF can also build waveguides directly into the glass for cleaner photonic solutions.

• LIDE creates smooth microfluidic channels in glass for in-package liquid cooling of high-power chips (e.g. AI/HPC hotspots), delivering coolant directly where needed; glass’s electrical insulation routes these channels right beside metallized TGVs and high-speed signals without interference or shorts—impossible in conductive silicon.

• Glass’s low thermal conductivity (~1 W/mK) acts as a thermal barrier/insulator to isolate chiplets or reduce crosstalk, while LIDE’s defect-free TGVs and channels silicon-matched CTE enable stable, efficient heat extraction and cycling without warpage or electrical compromise.

1

66

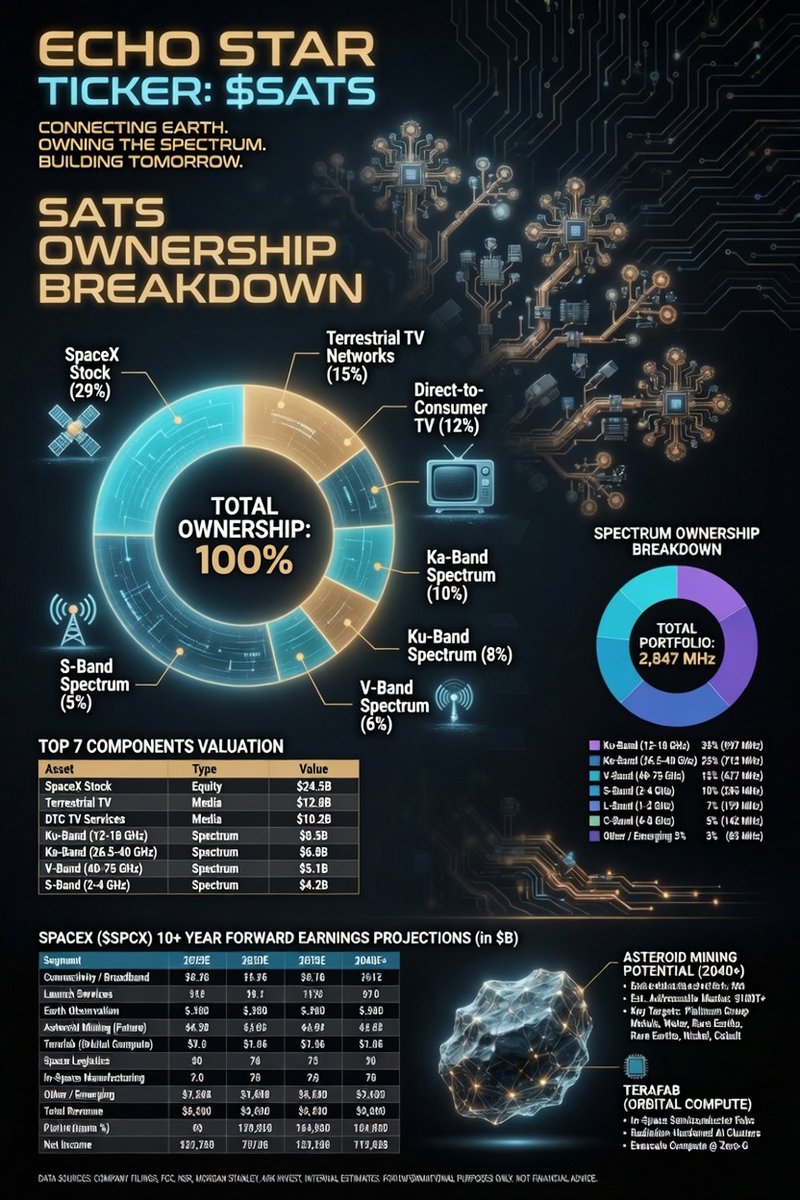

• $SATS is the stealth 2X $SPCX cheat code with a $TSLA merger airbag. Owns 0.75 $SPCX shares per share ($121 embedded value at current prices). That stake already covers most of $SATS’s market cap — the rest of the business (net cash spectrum) is basically free upside.

• Pure torque play: When $SPCX rips, $SATS amplifies the move because the volatile stake dominates valuation. Add the $TSLA $SPCX merger rocket fuel (Starlink in every Tesla, Optimus, robotaxis, energy) and this thing can go parabolic while you pay almost nothing for the non-SpaceX assets.

• Real downside edge no 2X ETF can match: Big spectrum cash deals already cleared most debt. If $SPCX dips, $SATS still has a cash spectrum floor. Mechanical 2X products just double your losses straight down — $SATS laughs and waits for the rebound.

• Asymmetric alpha: Levered $SPCX upside $TSLA synergy lottery ticket actual protection on red days. The closest thing to a “smart” leveraged SpaceX bet that exists.

4

378

Jun 13

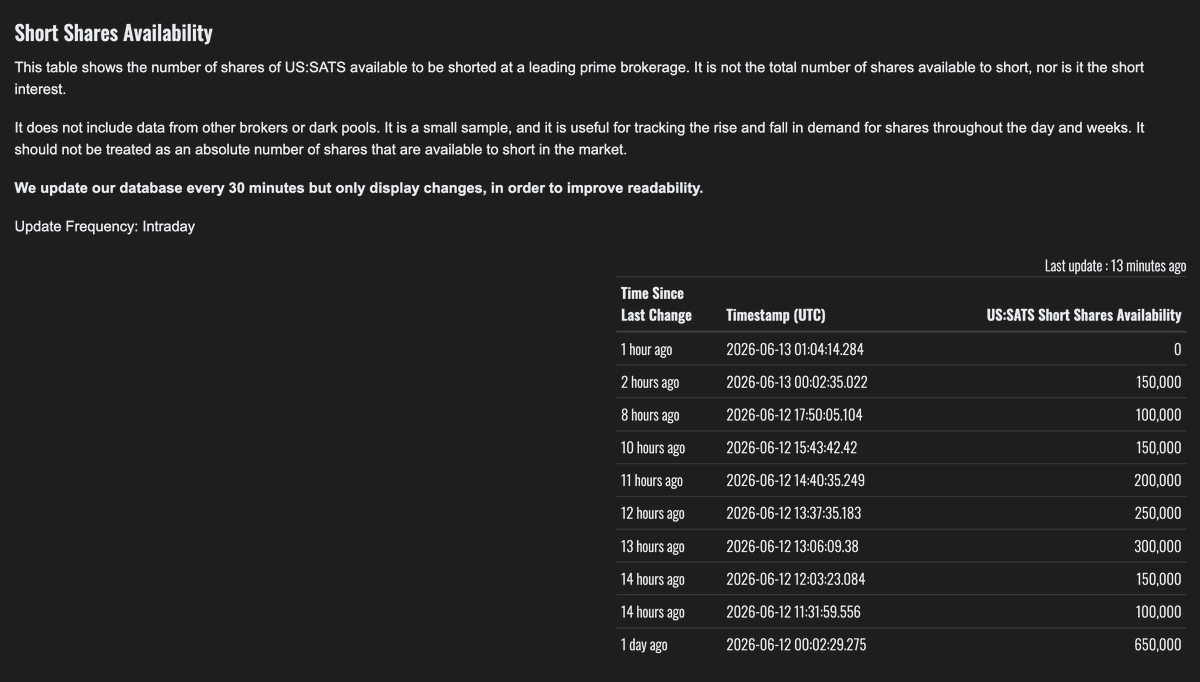

Potential $SATS short squeeze!

Jun 13

So $sats is down a mere $3 from $117 entry and you guys are asking why.

zzzz

The entire space sector just rotated into $spcx. $sats is down the LEAST. Ain't that fking good?

On top of that, MMs needed to cover their ASS. They needed calls to expire worthless.

90% options were calls!

How do we know that?

Short Shares Availability tanked. LOOK AT THE PICTURE. $60 million was used to pushed price down on a 35 Billion Mcap stock. WTF.

With short interest already 32% on a 50% of float thats not available to short?!?!!!! AT&T deal to be closed in less than a month.

THIS IS A FKING SHORT SQUEEZE IN THE MAKING

Now trading at $90 value to $170 $spcx per share.

It’s a fking no brainer.

A god candle will come. I live for god candles. It’s the best feeling in the world.

And I’ll be happy riding with you.

5

636

acceler8future retweeted

Jun 12

$SPCX - NASDAQ: IPO OF SPACEX TO BE RELEASED FOR QUOTATION AT 9:50AM ET

93

208

2,021

407,830

Jun 12

2

131

acceler8future retweeted

Jun 12

New like animation on 𝕏 to celebrate the SpaceX IPO

181

334

26,532

501,015

acceler8future retweeted

Jun 11

Elon has been focusing on the SpaceX IPO - crossing every t and dotting every i

After a successful IPO tomorrow, his attention will shift back to $TSLA, with many items on deck ready to go:

- Cybercab launch

- Robotaxi ramp in multiple states

- Roadster reveal

- Optimus 3 reveal

- Model YL in US

- Consumer unsupervised FSD

6

9

84

4,455

Jun 11

One of these days it’s going to be true!

🚨JUST IN: Trump just dropped big news.

Iran negotiations have been approved "at the highest level"

Additional strikes cancelled by Trump.

The naval blockade stays in full force until the deal is signed.

Big things happening.🔥

HT @EricLDaugh

x.com/EricLDaugh/status/2065…

1

5

126

acceler8future retweeted

Jun 11

AI startup CFO, CEO, CMO, and CTO

211

993

21,776

1,517,504

Jun 11

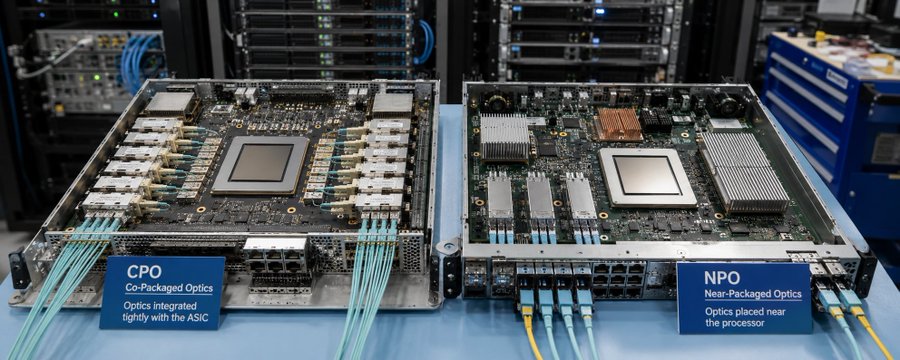

$LPK up 13% today on the news that Terafab is likely testing their kit. Potentially leapfrogging CPO and NPO in one giant leap!

Jun 11

x.com/acceler8future/status/… Elon heard me! He loves to jump the technology chasms where there is a real advantage.

Good chance they are testing LPKF equipment for a full photonics and cooled glass interposer for the AI1 satellite first launching maybe next year.

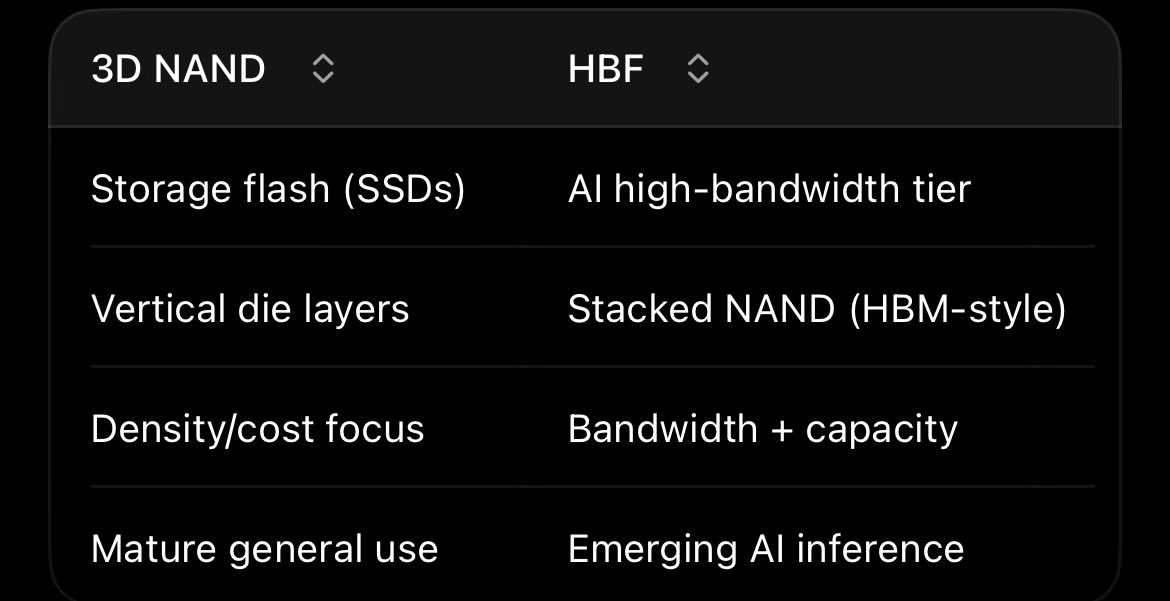

Probably something like 6 AI6 chips on one interposer / case. I think $SPCX might have Terafab build HBF memory ($SNDK tech like they are doing with $INTC) rather than HBM4.

1

4

615

Jun 11

x.com/acceler8future/status/… Elon heard me! He loves to jump the technology chasms where there is a real advantage.

Good chance they are testing LPKF equipment for a full photonics and cooled glass interposer for the AI1 satellite first launching maybe next year.

Probably something like 6 AI6 chips on one interposer / case. I think $SPCX might have Terafab build HBF memory ($SNDK tech like they are doing with $INTC) rather than HBM4.

Jun 11

Just thought this was interesting: $LPK is an unknown SpaceX supplier.

You can find it in SpaceX US import logs.

It's fun information discovery ahead of Space'x IPO this week. Though, not sure what the exact contract entails.

Disclosure: I have positions in LPK, NFA, credit to my follower Albert_TheVoid for the DM!

Especially since everyone seems to be talking about about SpaceX with Velo...

Just a fun, new direct relationship between $LPK and SpaceX if people want to do more digging.

1

3

992

acceler8future retweeted

Jun 11

OMG I massively increased my $LPK position but not nearly enough! Elon is going to love LIDE!

Now I just want to hear that he will add microLEDs to the mix!

May 22

Try reading this without thinking about $LPK LPKF and microLEDs ($KOPN and $FABC?). It’s impossible!

The memory wall isn’t going away anytime soon assuming the extra memory is connected by light.

1

2

6

1,742

Jun 11

How many hours do you average not on X per day?

Jun 11

How many hours on X do you average per day?

1

4

194

acceler8future retweeted

Jun 11

China clamping down on InP $AXTI wafers which are used in lasers for photonics.

What doesn’t use lasers? Oh yeah, microLEDs. Power is the long term terrestrial bottleneck and they use a fraction of the power of a laser (50% less according to $MSFT who are developing mediocre MediaTek microLEDs).

May 22

Try reading this without thinking about $LPK LPKF and microLEDs ($KOPN and $FABC?). It’s impossible!

The memory wall isn’t going away anytime soon assuming the extra memory is connected by light.

1

1

903

Jun 11

Glass interposers using LPKF tech looks like the future to me. But CoWoP is the next step beyond CoPoS. SLP is a fine detail PCB which sounds like the future for a lot of tech.

Ajinomoto (2802.T) have a monopoly in the SLP thin dielectric insulating film. $30bn MC.

I also like Ibiden (4062.T) and $TTMI in this sector.

TTM are 🇺🇸 company and their tech doesn’t require the base PCB.

4

342