Learning, practicing, reading, and writing about financial markets, economics, policies & governance.

Joined June 2009

- Tweets 3,436

- Following 266

- Followers 17,388

- Likes 11,974

18 Photos and videos

Pinned Tweet

Jan 30

1/2 Despite our macros, net foreign flows to India have disappointed. In two @BSIndia pieces, I explore why.

Part 1: The domestic surge into equities has created an exit door for FPI/FDI and fewer entry points. We need better tax-adjusted savings options.

bit.ly/4k21mYC

1

1

6

1,457

Ananth Narayan retweeted

Jun 13

SpaceX IPO, listing, and beyond, is a true test for capitalism. The valuation does not fit any traditional matrix and is a huge bet on the future course of planet earth. Only time will tell whether we, the human race, have arrived into the fairy tale world we grew up in as children, or are in a mega bubble. Either ways, kudos to the man who came as an immigrant, and to the country that has allowed such boundless creativity to flourish despite all the risks it embeds.

274

496

5,130

297,857

Ananth Narayan retweeted

Making #India's international #taxation system attractive to investors doesn't require India to become a tax haven, or to compromise its revenue base. It requires it to be in line with global norms, be consistent, predictable & operationally frictionless.

Read the article here!

#Opinion | #India is looking to boost foreign #investment by reforming its #tax system — making it competitive & predictable for global investors, attracting more capital & driving #economicgrowth.

@AshishDhawanTCF, Sudhir Kapadia, Amrita Agarwal write for the @EconomicTimes.

13

26

5,433

Ananth Narayan retweeted

Jun 10

Understanding the dilemma of falling markets at a time of rising GDP -moneycontrol.com/news/opinio…

@CafeEconomics @RBI @ananthng @FinMinIndia @MotilalOswalLtd @CNBCTV18News

7

6

52

24,845

Ananth Narayan retweeted

Q4 FY26 external flows data plus RBis schemes to attract dollars will be positive for rupee @RBI @FinMinIndia @ananthng

3/3 Q4 BOP DATA BETTER THAN EXPECTED

*India's current acct and capital account showed a surprising surplus for Q4

*Q4 curr acct saw a surplus of $7.1 bn or 0.7% of GDP

*Surplus driven by 28% rise in remittances and 13% rise in net services exports (GCCs, software)

*Q4 Capital acct $1.6 bn surplus due to FDI, NRI deposits, ECB flows

*Alert: Capital acct was expected to be deficit due to FPI outflows from equities

*Now FY26 BoP deficit at $23.6bn vs fears of around $50 bn

*Rupee can see a leg up due to the data and the schemes 3/3

6

42

8,723

Ananth Narayan retweeted

Jun 8

'RBI's Measures Will Break The Vicious Cycle Of Rupee', says @ananthng , Former Whole-Time Member, SEBI

'Oil & Gas & Banking Stocks Are Some Sectors To Look At', says S Naren , ED & CIO, ICICI Prudential AMC

Can India's growth story continue despite global uncertainty, AI disruption and geopolitical risks? Watch Indianomics with @latha_venkatesh

Watch: youtu.be/DfaYaP1w3EE

#RBI #Rupee #Oil #Gas #Stocks #India #Growth #CNBCTV18Digital

1

3

7

3,414

Ananth Narayan retweeted

Jun 8

#ICICISecInvestorConference 2026 | RBI Measures Could Mark A Turning Point For Capital Flows

Ananth Narayan Says

* FPIs can bring in $25-30 bn in G-sec investments

* RBI has created market access by making more G-secs available

@ICICIPruMF CEO S Naren Says

* RBI measures help break the negative feedback loop around the Rupee

* Think Bloomberg can consider including India G-Secs in their global bond index

#Watch: youtu.be/BUoGOsJhUlI?si=MOvx…

@latha_venkatesh #CNBCTV18Market #CNBCTV18News #ICICISecInvestorConference2026 #InvestorConference #InstitutionalInvestors #CapitalFlows #IndiaMarkets

1

10

3,249

Ananth Narayan retweeted

Column This Week |

Wars, Tariffs, Paper Leaks: Silence of Answers Deepens Sense of Drift

An eerie sense of foreboding defines the global moment. Whether it is unresolved wars, the chaos around tariffs, the plunge of rupee and stocks, consequential questions are hanging in the air. Amid a vacuum of response to crises, here are a few observations

West Asia War: 100 days in, Trump’s “dip-in, dip-out” operation has no exit. Ceasefires aren’t ceasefires. Inflation is the foster child of this war racking national balance sheets globally.

$ 1.5 Trillion Crash: On Friday, over $1 trillion was wiped out between breakfast and lunch; stocks, metals, bonds and Bitcoin all moved in unison on rate-hike fears — correlated shock made visible.

AI & Systemic Risk: Top 10 AI-linked tech stocks command $28 trillion in market cap — larger than China’s GDP, with OpenAI, Anthropic and SpaceX IPOs yet to land.

Tariff War: 432 days since Liberation Day, chaos persists. After the US Supreme Court struck down tariffs Trump imposed 10% & 12% tariffs under Section 301. The 'forced labour' is code for targeting nations using Chinese imports for exports.

India’s Growth Stress: GDP grew 7.7% last year but India has slid from 4th to 6th largest economy. And RBI cut its growth forecast to 6.6% and raised inflation forecast to 5.1%.

The Rupee Raga: Its the villain and the victim sliding 10% in a year from ₹86 to ₹95 to the dollar. FII sales drive the fall; the fall drives FII sales.

RBI’s Combo Offer: Opens long-tenure bonds to FIIs and offers to pay currency hedge costs to banks fetching dollar deposits. Will it lure depositors with conditions tighter than in 2013?

India Inc Splutters: Why is the private sector not investing, why is it sitting on ₹15 lakh crore in cash reserves? Can India sustain growth ambitions without ramping up R&D spend.

Stalled Reforms Ideas: The ₹1-lakh-crore RDI Fund and Urban Challenge Fund exist on paper. Two regulatory reform panels set up in February 2025 — no answers yet. A solar project still needs 116 approvals.

Shame of Paper Leaks: Parliament’s standing committee flagged NTA’s credibility crisis in December 2025. By 2026, NTA had proved them right. Can’t the pool of techies be tapped to end the litany of leaks?

The Bottom Line: Margaret Heffernan’s maxim applies — “Silence is the language of inertia.” In India’s political economy, that inertia is sustained by the politics of complicity.

@NewIndianXpress

newindianexpress.com/opinion…

🎧AI Podcast: A World Adrift Amid Anxieties 🎧

thoughtcapital27.substack.co…

3

8

1,072

Ananth Narayan retweeted

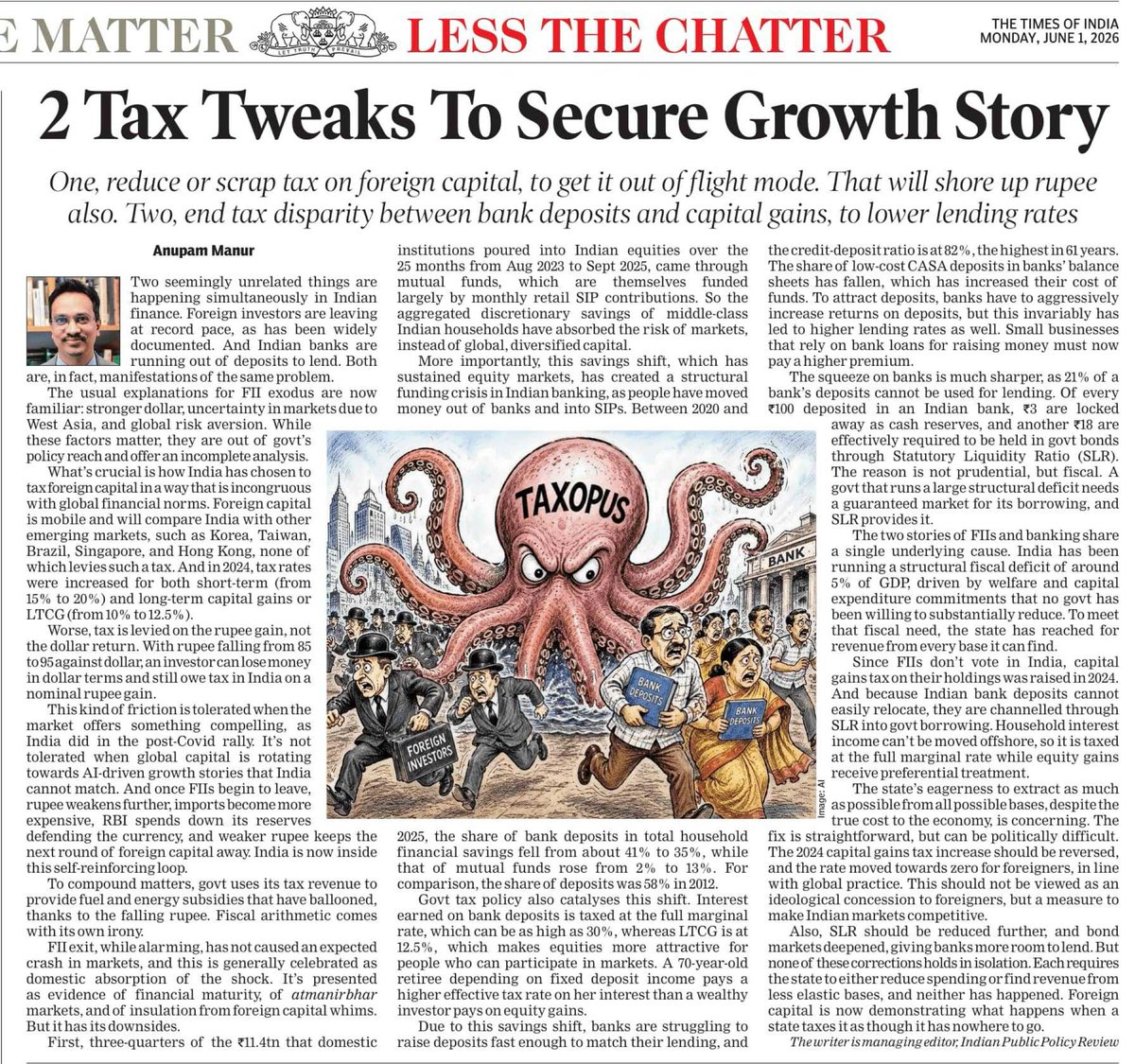

Govt backs RBi steps; withdraws withholding tax and capital gains tax on Foreign funds buying Indian govt bonds.

FPI sources say sheer fall in volume of paper work and tax niggles can bring mor FPI investments in bonds. IMpt: even so far hardly any outflows from FX bond portfolios 2/3

1

5

30

8,250

Ananth Narayan retweeted

I believe it's an excellent move not to tax FIIs. When you and I make gains on say Nvidia shares we pay capital gains tax here in India, not in the U.S. Likewise FPIs are governed by the tax laws of their country of origin. That's destination based taxes. We shouldnt have taxed them in the first place

FIIs are a relatively small participant in India’s debt market. Why offer special tax treatment to fiis while taxing domestic investors at the highest rates for investing in one of the lowest-risk asset classes? Is this really the right policy choice? @latha_venkatesh

64

32

267

70,925

Ananth Narayan retweeted

Jun 1

Fundamentally flawed argument. Mutual fund investments do not remove money from the banking system. @ananthng

Jun 1

India's rapacious tax policy is driving out foreign investors. That void is being filled by retail investors who are moving money out of their fixed deposits into mutual funds, which is leaving the banking system short of funds to lend. In today's ToI

19

12

107

36,428

Ananth Narayan retweeted

Jun 1

Watch this episode of #TheGrowwingIndiaPodcast with @ananthng as a masterclass in understanding the relationship between low interest rates and the rupee.

The impact financial repression has on investor choices.

And do not miss the last part where we discuss @Polymarket and a first-principle approach to markets for future prices and events.

youtube.com/watch?v=xcch2Fa3…

In collaboration with @_groww

3

1

18

2,840

Ananth Narayan retweeted

'The combined net profit (adjusted for exceptional gains & losses) of listed companies grew at a much faster pace of 15.1 per cent year-on-year (Y-o-Y) in Q4FY26, as compared to 9.2 per cent Y-o-Y growth in the year-ago period. Q4 was the 3rd consecutive quarter of double-digit profit growth for India Inc, and was also the first in 12 quarters to see double-digit revenue growth'

business-standard.com/compan…

2

10

42

5,245

Ananth Narayan retweeted

May 31

One of the best, @ananthng @monikahalan

Despite being a long 1 hour, it got me glued with attention.

While the focus was on the impact of top end of the pyramid, it would have been complete if some time was spent on the impact for the common man, the worst hit!

Next time!

1

2

3

2,626

Ananth Narayan retweeted

May 31

Excellent discussion between @monikahalan and @ananthng. Instructive and timely. Must listen.

May 31

Is the humble Indian SIPper causing the Rupee to decline?

Ex-WTM @SEBI_updates @ananthng debunks this narrative.

The story of the Rupee falling and lack of FDI goes way beyond trying to break the confidence of the Indian retail investor - like some 'experts' are doing.

Ananth calls for an asset-allocation approach with periodic rebalancing.

Also don't miss the section on @Polymarket and prediction markets.

youtube.com/watch?v=xcch2Fa3…

In partnership with @_groww

1

2

6

2,650

Ananth Narayan retweeted

May 31

Awesome interview ! A must watch. Addressed all my queries on the current equity markets, Rupee depreciation and taxation and their interplay ! Thank you @monikahalan

youtu.be/xcch2Fa3IOQ?si=suRP…

3

6

1,383

Ananth Narayan retweeted

May 31

Heard this Podcast in toto.

Am absolute gem on Macros and the current Indian economy

Excellent @monikahalan as always!

May 31

Is the humble Indian SIPper causing the Rupee to decline?

Ex-WTM @SEBI_updates @ananthng debunks this narrative.

The story of the Rupee falling and lack of FDI goes way beyond trying to break the confidence of the Indian retail investor - like some 'experts' are doing.

Ananth calls for an asset-allocation approach with periodic rebalancing.

Also don't miss the section on @Polymarket and prediction markets.

youtube.com/watch?v=xcch2Fa3…

In partnership with @_groww

1

4

2,336

Ananth Narayan retweeted

May 31

Ananth makes a good point re taxation for FPIs. We need to move from source-based taxation to residence-based taxation as is the global norm. It’s this taxation anomaly which is one of the reasons that’s reducing post-tax returns for FPIs and making India far less attractive.

May 27

In my latest @bsindia piece, following an Indianomics discussion with @latha_venkatesh and Mridul Saggar, I argue that while sharpening and articulating India’s growth story is critical, policy and market distortions may also have amplified negative sentiment around the INR and deterred capital flows.

Key points:

• No cause for panic: INR weakness warrants attention, but India’s external deficits remain manageable and RBI's buffers are substantial.

• The deeper issue: India’s prolonged struggle to attract sustained net foreign capital amid persistent negative sentiment on the rupee.

• Policy silos: Interest rates, liquidity, taxation, capital flows, and currency markets are deeply interconnected, though policy debates often treat them in silos.

• Unintended consequences: Interventions to suppress interest rates, alongside tax frictions, may have unintentionally weakened capital inflows and lowered the cost of speculative positioning against the rupee.

• Distorted savings: Distortions in taxation and markets have also stunted debt market development, pushing discretionary savings disproportionately into equities.

• Navigating the Trinity: The answer is not avoiding intervention, but engaging more holistically with the “impossible trinity” linking interest rates, exchange rates, and capital flows.

• The structural fix: Rather than introducing capital controls or fresh distortions, responses should aim for deeper debt markets, balanced taxation, and a globally competitive framework for foreign capital.

The piece argues against both panic and rigid orthodoxy, in favour of a more integrated approach to monetary, currency, and fiscal policy.

bit.ly/4tWs8Fi

1

4

9

3,020

Ananth Narayan retweeted

May 31

Thank you for a wonderfully insightful conversation @ananthng.

The 10-minute TV spots don't allow for this deep-dive that is needed on the topic.

May 31

Enjoyed a wide-ranging conversation with the one and only @monikahalan on how currency, interest rates, taxes and equities are interconnected, and shape savings, capital flows and the economy. We also discussed investing, regulation and market outlook. youtu.be/xcch2Fa3IOQ?si=Dm6g…

3

2

11

2,435