Joined May 2025

- Tweets 1,242

- Following 318

- Followers 127

- Likes 808

Photos and videos

Jun 17

When one doesn't know what one owns. $asts

Jun 17

$ASTS is over. The company might do really well by the year's end, but the stock is poisoned. The reallity is that there are some ppl bought early and made shit tons of money of it and that’s why they are advertising for it like their life depands on it.

2

271

🅰️ncap retweeted

Jun 17

In orbit again with 3 more of the largest phased arrays ever deployed in LEO 🚀🚀🚀

124

236

1,895

81,029

🅰️ncap retweeted

Jun 11

$ASTS - The shield and the illusion: AST SpaceMobile, SpaceX's S-1 and what LATAM operators can still do

In May 2026, SpaceX's S-1 became the most explicit statement the market has seen regarding Elon Musk's intentions for the telecommunications business. By valuing its connectivity segment against a total market of $1.6 trillion, SpaceX isn't signaling a partnership with mobile carriers. It's signaling their replacement, to the greatest extent that physics allows. Not in twelve months. But the ten-year timeframe is clear.

In response, the industry has rallied around a single name: AST SpaceMobile. The question worth answering honestly is whether this protection is sufficient and what Latin American operators should do in the meantime.

The statement that changed the framework

From the beginning of this series, we've argued that the real danger of Starlink's MVNO isn't the percentage of satellite traffic. It's the control of the SIM card and the data ecosystem built around it. SpaceX's S-1 confirms that argument was correct, and amplifies it.

The document is not just a financial presentation for investors. It's a strategic positioning statement. By framing its connectivity segment against a $1.6 trillion TAM, SpaceX is telling markets—and regulators—that its ambition is not to be a complement to the mobile operator ecosystem. It's to be the ecosystem. Existing operators' terrestrial infrastructure appears in this narrative as a transient asset: useful until satellite density becomes sufficient to make it obsolete, but dispensable within a ten-year timeframe.

To understand the magnitude of that in Latin America: the combined revenue of the region's leading mobile operators—Claro, Movistar, Telcel, TIM, Tigo, Personal, and the local operators in the twelve main markets—is in the range of $80 to $90 billion annually. All of that is within the Total Asset Market (TAM) that SpaceX allocated to itself in its IPO prospectus. Not a portion. All of it.

Timing matters

SpaceX won't have the satellite density needed to eliminate terrestrial networks in urban areas in two years. Probably not even in five. But the MVNO doesn't need that density to start capturing what matters most: SIM cards, end-customer billing, and behavioral data. That can happen long before the first satellite replaces the first urban tower.

AST SpaceMobile: who it is and what it's really building

Founded in 2017 by Abel Avellan, AST SpaceMobile wasn't created to compete with mobile operators. It was created to be their orbital infrastructure. This fundamental difference has structural implications for everything the company does: how it raises capital, how it negotiates with partners, how it designs its technology, and how it positions its product with regulators.

The mission is technically ambitious: to connect conventional smartphones , without any modifications, directly to satellites in low Earth orbit. No specialized terminals. No additional equipment. Just the same iPhone or Galaxy that the user already has in their pocket.

The architecture that makes it possible

The technical difference between AST and Starlink isn't one of scale, it's one of design. Starlink uses thousands of small satellites with a high-volume approach: many nodes, narrower signals, and coverage based on density. It's effective for messaging and basic data, but the limited transmission power of a typical smartphone—around 0.2 watts—imposes a ceiling on what that architecture can deliver without modifying the device.

AST solves that problem by inverting the design: instead of putting intelligence in the number of satellites, it puts it in the size of the antenna. Its next-generation BlueBird satellites deploy antenna arrays of 2,400 square feet—about 223 square meters—the largest commercial communications array ever deployed in low Earth orbit. That aperture acts as a high-gain receiver capable of capturing and amplifying the weak signal from a smartphone from an altitude of 500 kilometers.

The computational core powering this is the proprietary AST5000 integrated circuit, developed over 150 man-years of engineering. It processes 10 GHz of instantaneous bandwidth per satellite, handles the Doppler shifts inherent in LEO flight, and delivers peak speeds of 120 Mbps per cell. In tests with its Block 1 satellites, AST achieved 98.9 Mbps of real-world speed on unmodified smartphones. For reference: that's residential broadband speed, not emergency connectivity.

The result of this design is that the AST satellite operates as an orbiting cellular base station, compatible with 3GPP 4G and 5G standards. The user's smartphone doesn't detect a different network; it detects their carrier's network, with the satellite acting as just another cell. The handover between the ground tower and the satellite occurs seamlessly, just as it does today between adjacent cells in an urban network.

Abel Avellan describes it bluntly: “Nobody is remotely close to our technical capability to deliver hundreds of megabits directly to a phone from something flying at 70,000 miles per hour 500 kilometers above you. That competitive advantage is unique.”

The business model: why operators are partners, not customers

AST's capital structure is not accidental. Its strategic investors include AT&T, Verizon, Vodafone, Rakuten, Alphabet (with 3.8 percent of the capital), in addition to institutional support from Vanguard with approximately 21.4 million shares and BlackRock with 14.5 million. The Cisneros Group, one of Latin America's largest media and technology conglomerates, is also a strategic shareholder.

That's not a customer list. It's a list of owners. The major global operators have a direct financial interest in AST succeeding as an infrastructure provider, not as a competitor. That alignment of incentives is the mechanism AST uses to protect itself in a market where it would otherwise be vulnerable.

The monetization model is equally clear: when a user connects via an AST satellite, they continue using their existing carrier plan, and the revenue generated is split 50/50 between AST and the carrier. The user does not sign any contract with AST. They do not activate any additional services. They do not switch carriers. The carrier retains the billing, the business relationship, and the data asset. AST charges for the satellite capacity provided.

This approach solves two of the most costly problems in the telecommunications business. First, customer acquisition costs: AST doesn't invest in marketing or distribution; it relies on the sales networks of its 60 global partner operators. Second, remote coverage capital expenditures: the operator can extend its coverage map to areas where building towers is economically unfeasible, without investing a single dollar in terrestrial infrastructure.

The scale in 2026

As of May 2026, AST has six operational satellites in orbit. The goal for the end of the year is to reach between 45 and 60 units, with launches scheduled every one or two months. Next June, a Falcon 9 will carry BlueBirds 8, 9, and 10; a critical mission that gained greater urgency after the loss of BlueBird 7 due to an anomaly in Blue Origin's New Glenn rocket, which led to an FAA moratorium on that launch platform.

On the manufacturing side, the 500,000-square-foot facility in Midland, Texas, is currently processing BlueBirds 11 through 33, with a production rate targeting more than ten satellites per month. AST reported over $70 million in total revenue for 2025 with a gross margin of 68.6 percent and closed a $1.075 billion convertible note issuance in February 2026. Total available liquidity amounts to approximately $3.9 billion, sufficient to support the estimated annual capital expenditure of $1.2 billion.

The FCC has already authorized AST's commercial service in the United States under the Supplemental Coverage from Space (SCCS) program, with the capacity to operate a constellation of up to 248 satellites. With nearly 60 global operating partners representing more than 3 billion subscribers, and contractual revenue commitments exceeding $1.2 billion, AST has completed its transition from a demonstration company to a scaling infrastructure utility.

Architectural investment: why AST and Starlink are not the same game

For Latin American operators, understanding the structural difference between the AST model and Starlink Direct to Cell (D2C) is not a technicality. It is the key to the entire strategy.

Starlink operates its own satellite network and integrates it with operators who provide spectrum. The SpaceX satellite uses the operator's licensed frequencies to connect to the end user's device. The satellite technical layer is provided by SpaceX. The operator is the spectrum enabler and, in the best-case scenario, the commercial channel. If SpaceX moves toward becoming an MVNO, the operator ceases to be a channel and becomes an anonymous wholesale provider.

AST operates under a different logic. Its satellites act as orbiting base stations, integrated into the operator's core network as just another cell. The standard is 3GPP. The spectrum belongs to the operator. Billing is handled by the operator. The customer doesn't notice any difference. In the Starlink model, the risk is that SpaceX could retain the SIM card. In the AST model, the operator retains the SIM card while AST operates the infrastructure that extends its coverage into space.

Avellan's distinction regarding Amazon/Globalstar is relevant in this context: “Basically, we see that capacity as an emergency SOS system. To provide real broadband, you need hundreds of megahertz of allocated spectrum… our focus is broadband. That's a completely different proposition.” This isn't corporate modesty; it's product positioning that establishes AST as the only direct-to-device broadband alternative with native integration into the operator's core network.

The honest verdict: a royal shield, but not a permanent solution

The analysis of AST SpaceMobile circulating in telecom investment and strategy communities converges on an uncomfortable but correct point: AST is a lifeboat, not a silver bullet.

The distinction matters because many operators are treating AST as if solving the rural coverage problem were enough to win the strategic war. It isn't.

AST gives operators three concrete and valuable things. It gives them real coverage without terrestrial capex in areas where building towers is not feasible. It gives them customer relationship retention even when they are off the terrestrial network. And it gives them a line of defense against SpaceX in the battle for coverage. These three things have real value and are defensible.

What AST can't do is reverse the structural commoditization of the mobile business. SpaceX didn't create that process. It was the result of two decades of price competition, digital disintermediation, and the migration of value to application platforms. What SpaceX is doing is accelerating that process and adding a SIM capture threat that didn't exist before. AST blocks that capture, but it doesn't return the value that has already migrated.

In other words, with AST, operators can remain relevant in the future. Without AST (or an equivalent solution), they may remain as anonymous infrastructure. But remaining relevant in the future is not the same as having solved the underlying problem. It's about having bought time to solve it.

AST SpaceMobile is the mechanism that allows the telecommunications industry to buy time to survive the orbital era. What they do with that time is the real strategic question.

LATAM: the perfect geography, the most exposed regulatory position

Latin America possesses conditions that make it one of the most relevant markets for the next stage of satellite connectivity. These include challenging geography, low coverage density across vast territories, industrial sectors (mining, agribusiness, energy, logistics) with critical connectivity needs in the field, and a mobile market of over 700 million connections with expanding digital penetration. However, it also presents specific vulnerabilities.

AST's Latin American partners have already been identified

The agreements that AST SpaceMobile has formalized to date include operators with a direct presence in Latin America. However, one of them requires a closer look. Telefónica is listed among AST's partners, but its Latin American presence has changed radically in the last twelve months. Under the leadership of Marc Murtra, who took over as CEO in January 2025, the company executed an accelerated exit from Hispam: it sold its operations in Argentina to Telecom Argentina for $1.245 billion, in Peru to Integra Tec International for just $1 million, in Uruguay and Ecuador also in 2025, and in Colombia it sold 65 percent of its operation to Millicom for around $400 million.

In the first quarter of 2026, the operator completed its exits from Colombia and Chile, the latter sold to Millicom and Xavier Niel's fund. The sale of Mexico to Melisa Acquisition was announced in April 2026. Murtra himself stated it unequivocally: the goal is to concentrate on Germany, Spain, the United Kingdom, and Brazil (the only Latin American market that Telefónica considers strategic in the long term). In other words, Telefónica's agreement with AST is, in practice, an agreement with Vivo Brasil, not with a pan-regional operator.

The Latin American geographic coverage that the agreement represented on paper has been dramatically reduced. Millicom (Tigo) covers Bolivia, Paraguay, Honduras, Guatemala, El Salvador, Nicaragua, Costa Rica, Panama, and Colombia; and by partially absorbing Telefónica's Colombian operation, it expands its exposure precisely in the markets with the largest proportion of rural territory without coverage and the smallest scale to justify tower expansion. Telecom Argentina, which acquired Movistar Argentina's operations, consolidates its position in a market with vast stretches of the Pampas and Patagonia lacking viable coverage. Liberty Latin America operates in Puerto Rico, the Dominican Republic, Jamaica, Panama, Costa Rica, and other markets in the Caribbean and Central America.

The resulting map differs from what AST's partner ecosystem suggested a year ago. With Telefónica now focused on Brazil, the Latin American weight of the agreement falls on Millicom, Telecom Argentina, and Liberty Latin America—three operators with a real presence but without the pan-regional coverage that Telefónica Hispam provided. What remains missing from that list is equally revealing: operators without an agreement with AST (and who rely on the Starlink Direct to Cell model as their only satellite coverage option) are in a weaker strategic position.

The most significant absence in this ecosystem is América Móvil. The dominant operator in Mexico and the largest in Latin America by number of subscribers (with Telcel, Claro, and their regional brands present in seventeen countries in the region) does not appear in any AST SpaceMobile filing , any public list of operator partners, or any corporate statement available as of the date of this publication. This omission is not a minor detail. It is, in itself, a strategic fact of paramount importance.

It could mean that América Móvil is evaluating the situation without making a commitment, waiting to see how the constellation scales before negotiating from a position of need. It could mean that it prefers the Starlink Direct-to-Cell model, which maintains coverage without relinquishing a 50 percent revenue share to a third party. Or it could mean that negotiations are underway, but no agreement has been reached on terms. What it cannot mean, given the size of the operator and the geographic coverage at stake, is indifference.

In Mexico, Telcel operates in the world's largest Spanish-speaking mobile market, with over 60 percent market share. If this operator reaches an agreement with AST, the satellite broadband layer will be integrated into the country's most extensive network, and rural access will become a Telcel asset. If it doesn't reach such an agreement, and Movistar Mexico—a Telefónica subsidiary—has it operational first, the coverage gap will be reversed for the first time in the competitive history of the Mexican market. And if América Móvil ends up relying solely on the Starlink model, customer relations in areas without terrestrial coverage will be subject to SpaceX's logic, not its own. Any of these three scenarios has consequences that extend far beyond the signal map.

The regulatory window is closing

The most underestimated risk in Latin America is not technological. It is regulatory, but in a different sense than is usually discussed.

The danger isn't that regulators will block AST. It's that operators who don't actively participate in defining the regulatory framework for supplemental satellite coverage will end up in an environment designed by their competitors. In Mexico, the Telecommunications Regulatory Commission (CRT), which replaced the IFT in October 2015 and operates under the Digital Transformation and Telecommunications Agency of the federal government, will have to define whether AST's satellites using spectrum licensed by Movistar or Telcel are an additional cell of that network, an independent satellite service, or something new. This categorization determines who can participate, under what conditions, and with what obligations regarding universal service, portability, data location, and lawful interception.

In Brazil, Anatel faces the same problem with Claro and TIM as potential partners for AST. In Colombia, Chile, and Peru (where Telefónica already has relationships with both satellite providers), the question is when, not if, this regulatory discussion will take place. The operator that approaches the regulator with a structured technical proposal, public policy arguments, and an implementation timeline will have an advantage over one that waits for authorization to come automatically.

The WRC-27 (World Radiocommunication Conference 2027) will establish global spectrum rules for non-terrestrial networks. What Latin American administrations present there will define the framework for the next decade. Operators not participating in that discussion today will not be part of the 2028 results.

What LATAM carriers should do — with or without AST

The strategic agenda for Latin American operators is not new. The three previous installments in this series have outlined it from different angles. What changes with SpaceX's S-1 and the consolidation of the AST ecosystem is the urgency: it's no longer about positioning for a future threat. The threat has a date, a legal structure, and a public offering document that quantifies it at $1.6 trillion.

Five actions define the difference between the operators who will emerge stronger from this transition and those who will end up as anonymous capacity providers.

1. Negotiate access to AST from an active position, not a position of need.

Operators entering negotiations with AST after SpaceX has achieved critical mass in their market will be negotiating from a position of weakness. Those entering now (with customers, spectrum, licenses, brand recognition, and regulatory relationships as assets) can negotiate terms that preserve control over the end-user relationship. The 50/50 revenue-sharing model is the current market benchmark, but that figure isn't set in stone for markets with different dynamics. What is clear, however, is that those who arrive late will have less leverage.

2. Monetize your own data assets before the competition arrives

Claro, Telcel, and Movistar have years of experience tracking the mobility, consumption, and behavior of hundreds of millions of users. This asset isn't being monetized to its full potential. The first step is to build their own data platform (geolocated advertising, market intelligence, alternative credit scoring, financial services) before Starlink arrives and does exactly the same thing with the same users on its own SIM card. The M-Pesa model in Kenya remains the most cited and least imitated benchmark in Latin America. The window of opportunity to be the operator that arrives before the bank is not permanent.

3. Build vertical proposals for high-value sectors

The most immediate opportunity lies not with the mass consumer. It lies with businesses and industrial sectors that require continuous and guaranteed connectivity in the field: mining in Chile and Peru, agribusiness in Brazil and Argentina, logistics and transportation in Mexico and Colombia, energy in Venezuela and Ecuador, and tourism in nature destinations throughout the region. These customers pay enterprise rates, have multi-year contracts, and don't switch providers based on price. The operator that arrives first with a guaranteed coverage proposal (using AST's satellite layer as an invisible part of its network) has a competitive advantage that no newcomer can immediately replicate.

4. To exert regulatory pressure for the principle of reciprocity

The correct regulatory argument is simple: same services, same rules. If Starlink bills the end user as a mobile operator, it must contribute to the universal service fund, respect number portability, and comply with data localization obligations under local legislation. If AST operates spectrum from a licensed operator in Mexico, Colombia, or Brazil as if it were a cell of that network, the regulatory framework must reflect that technical reality. Neither of these positions is anti-competitive. They are principles of regulatory equivalence that protect both the user and the historical investment of established operators.

5. Organize a common regional front on data

No single Latin American operator has the individual scale to compete with the global dataset SpaceX will build if it manages to position itself as an MVNO in ten markets simultaneously. But the combined scale of regional operators does. A data consortium among the leading operators in the six largest Latin American markets (without the need for a merger, by federating the information asset under shared governance) would create a comparable critical mass. In Europe, operators have explored similar schemes against Google and Meta. In Latin America, no one has yet implemented such a strategy. SpaceX's S-1 is the catalyst needed to make that conversation happen.

Time is not neutral

The four installments in this series have followed the same argument from different perspectives. Physics establishes the limits of what the satellite can do. Musk's strategy explains why those limits don't matter as much as they seem, because the real value lies not in the bits transmitted but in the data generated. The industry's response establishes that AST SpaceMobile is real, functional, and the most coherent counterproposal to SpaceX's progress. And this article concludes with the point all these elements make: time is not neutral.

Every week a Latin American operator remains silent on the AST conversation, every quarter it fails to build its data platform, every regulatory cycle it lets pass without actively participating, is time working in SpaceX's favor. Not because SpaceX is already winning—not yet—but because every delay by the operator reduces its negotiating leverage and widens the advantage of the one that arrives with greater scale, more data, and less reliance on local agreements.

AST SpaceMobile is the most concrete mechanism the industry has today to buy that time. But buying time only makes sense if it's used. The question that defines the next stage of mobility in Latin America isn't whether satellites will win. It's who will be on the other side of the table when that happens.

Operators who come to that table with customers, data, spectrum, and a strong regulatory position will remain players. Those who arrive without those assets will be someone else's infrastructure.

This text is a translation of an article from TeleSemana: telesemana.com/blog/2026/06/…

7

15

108

14,657

Jun 5

Jun 4

Merlin has completed the Critical Design Review for its C-130J autonomy program with @USSOCOM. CDR is the milestone where our government customer reviews the detailed design of the system and accepts it is mature enough to move toward the aircraft. We cleared it.

Learn more about what this milestone means in the press release. globenewswire.com/news-relea…

9

1,004

🅰️ncap retweeted

Jun 1

$ASTS: Quote from AST SpaceMobile in recent article:

“None of the missions planned for the next few months are scheduled with Blue Origin,” the statement said.

“Our satellites are designed to be launcher-agnostic, and we have agreements in place with multiple launch providers, giving us flexibility across our launch program,” AST SpaceMobile added.

29

113

989

86,872

May 31

$ASTS

This guy will eventually see sizable revenue, but by then he might do x2 or x4, not x10 or x20.

I genuinely don’t get the hype around space stocks…

Billion dollar valuations. Cult-like following. And what have we actually achieved?

In 1969, we landed on the Moon. With slide rules and 4KB of computing power.

55 years later, the big “innovation” is reusable rockets. Which is genuinely impressive engineering, but it’s a cost reduction story, not a giant leap. We’re still going to the same low Earth orbit. Still haven’t put boots back on the Moon. Mars remains a press release.

Meanwhile these companies trade on vibes, Elon tweets, and government contracts dressed up as revolution.

$RKLB, $ASTS, $LUNR all priced like they’ve already colonised the solar system. Most are burning cash at a rate that would make a pre-revenue SaaS startup blush.

Space is cool. Space stocks? No thanks.

Show me some real revenue. Show me the margin. Show me a business model that doesn’t rely on the next hype cycle to stay afloat.

I’ll pass.

1

14

1,597

🅰️ncap retweeted

May 31

This is high level DD. I have mentioned it before, but too few discuss it

$ASTS has an aggregate interference margin big enough to scale up a lot!

Starlink spam-a-lots has to ask waiver just to operate and immediately hits diminishing returns from self interference when scaling

May 30

$ASTS ✨

Why this matters for $ASTS investors

An AST SpaceMobile employee highlighted a key technical issue for the future of NTN and direct-to-device satellite networks:

“Launching more satellites alone does not solve everything.”

The core issue is aggregate interference.

In a simple model, one satellite talks to one user.

But in a dense NGSO constellation, many satellites may be visible to the same user at the same time.

Even if each satellite individually follows the rules, the combined interference can still increase at the user level.

That matters because higher interference can lead to:

• Lower SINR

• Lower throughput

• Weaker edge performance

• Worse user experience

The key message:

Future NTN success will not depend only on satellite count.

It will depend on:

• Network design

• Beam management

• Spectrum efficiency

• Constellation-wide interference control

• Real user experience

This is why “more satellites” is not the full answer.

For ASTS investors, the bigger takeaway is that the long-term winner in direct-to-device may not simply be the company with the most satellites.

It may be the company that can design the best coexistence between satellite networks and terrestrial mobile networks.

$ASTS #ASTSpaceMobile #NTN #DirectToDevice #Satellite #Telecom #SpaceTech #5G

linkedin.com/posts/aliesswie…

1

11

167

15,165

May 25

Most people still think D2D is “emergency texting from space.”

$ASTS already demonstrated ~100 Mbps broadband directly to normal phones.

That isn’t just rural coverage. It’s a new global wireless layer.

And that’s why the carrier alignment matters more than the retail hype around a $1.75T IPO.

AT&T, Verizon, Vodafone, Google, 60 MNOs.

These companies don’t write equity checks for science projects. They have done their due diligence.

Meanwhile the market is pricing: $ASTS as uncertainty @SpaceX as perfection.

One is expected to dominate everything. The other only needs to execute in a market SpaceX itself sized at $740B.

That asymmetry at play here.

$ASTS 🛰️

May 24

A message for my $TSLA friends eyeing the SpaceX IPO $SPCX.

I traded $TSLA for years. I know the community. I know the excitement when Elon takes something public. But before you chase @SpaceX at $1.75 trillion, read the S-1 carefully.

SpaceX doesn't need your money.

They raised at $800B in private tenders six months ago. They could raise $50B privately tomorrow with a phone call. This IPO isn't about raising capital. It's about giving insiders liquidity.

95% of @SpaceX shares are held by insiders. Only 5% will be publicly traded. Insiders hold $1.66 trillion in paper wealth they currently can't sell. The IPO changes that.

And they've structured it so insiders can sell BEFORE the standard 180-day lock-up expires. @SpaceX built in early release provisions -- after the first earnings report, insiders can sell up to 20% of their shares.

They're also reserving 30% of IPO shares for retail. Ask yourself -- when has Wall Street ever given retail the best seats in the house unless retail was the product?

100x revenue.

$4.9B net loss.

xAI burning $6.4B a year while @Starlink subsidizes it.

This isn't 2020 Tesla at 20x revenue with a clear path to profitability. This is a different risk profile.

Now here's the part I want you to actually consider.

SpaceX's S-1 sizes their satellite-to-phone business (Starlink Mobile) at a $740 billion TAM. Their Connectivity segment does $11.4B at 63% EBITDA margins. Those numbers are real and impressive.

But buried in the S-1, @SpaceX names their D2D competitor: $ASTS .

@AST_SpaceMobile $40 billion market cap.

Not $1.75 trillion. $40 billion.

Here's what $40B buys you:

98.9 Mbps proven from space to unmodified phones (SpaceX does 3-5 Mbps)

The only low-band D2D spectrum access on Earth (indoor coverage SpaceX can't match)

All three US carriers forming a joint venture around ASTS technology

Google invested $358M

their largest public equity holding

AT&T, Verizon, Vodafone as equity investors

$3.5B cash, $1.2B contracted backlog

3,900 patents, custom ASIC in production

Three satellites launching on a Falcon 9 next month

60 carrier partners covering 3 billion subscribers

@SpaceX at $1.75T is pricing perfection across rockets, satellites, AI, and Mars. One miss and it corrects hard.

$ASTS at $40B is pricing uncertainty in a $740B market where the technology is already proven and the carriers have already chosen sides.

The Tesla community knows what it feels like to find a mispriced stock before the world catches on. $TSLA at $30 pre-split wasn't obvious to anyone except the people who did the work.

$ASTS at $106 in a $740B market with 33x faster speeds than SpaceX D2D, a carrier JV, and institutional discovery just beginning -- that's the same kind of setup.

So before you throw money at a $1.75T IPO where insiders are building exit ramps, maybe look at the $40B competitor they named in their own filing.

Not financial advice. Just math.

$ASTS 🛰️

cc @SawyerMerritt @unusual_whales @DanBTC916

5

3

56

4,960

May 21

$ASTS SpaceMob listen up, and listen carefully. If I won't manage to convince my real friends to become rich enough to stop working and go on all sorts of adventures, you guys will have to step up to the mark to go skiing, climbing and drinking wine. This is your duty.

3

34

1,190

🅰️ncap retweeted

May 20

Starlink now represents ~70% of SpaceX revenue making connectivity the core cash engine of the company.

Thats why $ASTS remains a top 5 position for me because D2D connectivity could become one of the most valuable layers of the space economy.

May 20

SPACEX FULL FINANCIALS

2025 Full Year

• Revenue: $18.7B ( 30% YoY)

• Net loss: $4.9B vs. $791M profit in 2024

• Capex: $20.7B

Q1 Performance

• Revenue: $4.69B

• Connectivity: $3.3B

• AI: $818M

• Space: $619M

Operating Metrics

• 650 total launches

• 9,600 Starlink satellites

• 10.3M Starlink subscribers

• 550M monthly active users on X

• 80% of 2025 global mass to orbit

• 1GW AI compute nameplate draw

• 85% missions with reused boosters

$SPCX is becoming a vertically integrated space, connectivity and AI infrastructure platform.

47

76

775

87,649

🅰️ncap retweeted

May 20

$ASTS $SPCX

🚨🚨 SPACEX JUST VALIDATED THE SPACE BASED CONNECTIVITY SUPER CYCLE

1/3

SpaceX’s S 1 is not bearish for AST SpaceMobile. It is the clearest public market validation yet that satellite communications, direct to device connectivity, reusable launch, government space demand, and orbital AI infrastructure are no longer niche aerospace themes. They are being valued as core technology infrastructure. For @AST_SpaceMobile, that is the point: the market is being forced to reprice space based networks from speculative science projects into strategic communications platforms. SpaceX may be the giant, but AST remains the cleanest public pure play on carrier integrated broadband direct to ordinary mobile phones.

reuters.com/legal/transactio…

Here’s the read: assuming Reuters’ report is accurately describing the public SpaceX IPO filing, this is broadly bullish for AST because it drags the entire space based communications category into the center of public market valuation. I could not retrieve a clean SEC hosted prospectus URL through the search path available here, so the SpaceX side of this analysis is grounded in Reuters’ filing based reporting, not a directly opened SEC S 1 document.

Reuters says SpaceX “took the wraps off its IPO filing” on May 20, with ambitions that include Starlink expansion, Mars, and AI data centers in space. The reported valuation target is about $1.75 trillion, with Reuters also reporting a potential $75 billion raise, Nasdaq listing, and ticker SPCX. Reuters describes Starlink as SpaceX’s main revenue engine, with roughly 10,000 satellites and broadband service for consumers, governments, aviation, maritime, and enterprise customers.

For AST, the most important point is category validation. Public investors are now being asked to underwrite satellite connectivity, reusable launch, AI infrastructure, government space demand, and orbital compute as one integrated mega platform. That makes AST easier to explain to generalist institutions: not as a speculative satellite story, but as a scarce public equity tied to space based broadband, carrier infrastructure, spectrum, government resilience, and future space infrastructure.

The first corroboration is that SpaceX’s filing appears to confirm that satellite connectivity is no longer a niche aerospace subsegment. Reuters reports that Starlink generated $11.4 billion of SpaceX’s $18.7 billion 2025 revenue and $4.4 billion of operating profit, while SpaceX’s total addressable market claim reaches $28.5 trillion, with $26.5 trillion attributed to AI and $22.7 trillion to enterprise AI. That directly helps AST because it tells the market to stop valuing space connectivity only against legacy telecom or old aerospace multiples. Space based communications can be a platform market.

The second corroboration is that direct to device is now clearly an industry architecture, not a side experiment. AT&T, T Mobile, and Verizon announced a proposed joint venture to address wireless dead zones using satellite based direct to device technologies, pooled spectrum resources, and common technical specifications. The release says the goal is to extend mobile connectivity in underserved areas and help satellite providers reach more customers through a unified platform. ASTS already sits directly in that lane, and its own release says the proposed collaboration should accelerate technical integration, improve customer experience, enhance coverage, and help eliminate dead zones.

See 2/3

1

2

42

1,321

🅰️ncap retweeted

May 18

$ASTS: 🚨 ABEL AVELLAN ANNOUNCES THAT BLOCK-2 BLUEBIRD SATELLITES HAVE BEEN SHIPPED TO CAPE CANAVERAL AND CONFIRMS AST SPACEMOBILE WILL PLAY KEY ENABLING ROLE IN AT&T/VERIZON/T-MOBILE JOINT VENTURE

Credit: u/TheEventualHorizon - Reddit

66

234

1,538

137,216

May 17

Hennessy funds on the $ASTS.

We're not bullish enough!

May 17

$ASTS: Transforming How the World Connects - Hennessy Funds May 2026 AST SpaceMobile Update

AST is building the first and only space-based cellular broadband network accessible directly by everyday smartphones with both commercial and government applications.1 With strategic investments from leading technology players such as AT&T, Verizon, Vodafone and Google, AST has the bold goal to provide uninterrupted broadband connectivity, everywhere.

✅ Eliminating Connectivity Gaps in Broadband

AST’s vision is to provide mobile broadband wireless coverage to existing cell phones in partnership with today’s global, mobile network operators (MNOs). Supplemental coverage from space through AST’s satellites would be a breakthrough for the wireless and satellite industries, allowing satellite delivered mobile wireless service to expand beyond niche applications we see today to broad consumer adoption.

✅ Addressable Market

Even in 2026, billions of people around the world have no or limited mobile internet access. Among a global population of 8.2 billion, 5.8 billion unique cellular subscribers move in and out of basic and broadband wireless coverage daily, while more than 3.4 billion people are unable to access cellular broadband. Of these, 3 billion have a usage gap and 400 million have no cell coverage.

In fact, ~90% of the Earth’s surface has no cell coverage whatsoever. Even in covered areas, there are millions of dead zones and grey zones in existing terrestrial networks. AST plans to eliminate these gaps by providing an overlay or supplemental broadband service that mobile subscribers can opt into through their MNO’s domestic service plans—resulting in broadband coverage for the unconnected billions.

✅ AST’s Vision

AST has announced plans to launch over 540 dual-use satellites over the next seven years designed to eliminate global connectivity gaps for commercial and government users. Four separate constellations are envisioned, engineered to serve either C-band, midband and low-band communications spectrum. The first constellation will consist of up to 248 low-band satellites orbiting between 285-329 miles above earth. Seven years in development, these low-band BlueBird satellites use a novel design, internally developed software and custom hardware that is then spliced into the wireless operators’ “core” network through an equipment partnership with Nokia. This technique allows a cell phone to see a virtual cell tower broadcasting on either their MNO partner’s existing terrestrial spectrum or later on Mobile Satellite Service (MSS) spectrum owned or leased by AST.

✅ Worldwide Military and First Responder Opportunities

Importance of Space-Based Defense Systems

If the war in Iran has taught us anything it is that ground-based radar is vulnerable to missiles and drones guided by satellite systems. If our ground-based radars are knocked out our defensive interceptors are blind. This vulnerability is being rapidly incorporated into U.S defense thinking. We have heard such comments repeatedly at several of the defense related conferences we recently attended. It is quickly becoming imperative that the U.S. and allied forces have a second set of eyes in every global theatre not subject to the same ground-based risks seen in the Middle East.

Our legacy missile defense systems—often composed of ground radar, GEO (Geosynchronous Equatorial Orbit) satellites, and terrestrial interceptor batteries—are designed to neutralize traditional short- and long-range missiles. The trajectory of these missiles is predictable from shortly after launch, making them relatively straightforward to intercept.

However, newer long-range missiles, such as hypersonic and advanced ICBMs, can change trajectory during travel, and sometimes include decoys and multiple warheads made to fool existing missile defense systems. This makes these missiles much more challenging to neutralize. The U.S. and its allies are vulnerable to these advanced weapons and need a faster, more accurate, and more distributed missile defense system in response.

The unprecedented size and power of AST’s LEO (Low Earth Orbit) satellites make them especially well-suited to assist in tracking modern missiles, along with a variety of other high value functions. Research reveals excellent effective isotropic radiated power (output power of a signal when it is concentrated into a smaller area by the antenna) and gain-to-noise temperature (how well the system can detect weak signals amidst noise), enabling a variety of novel capabilities.

AST’s work with the Federal government continues to build with both defense and communications applications in various stages of testing and development. In terms of defense, AST was awarded a contract with the Missile Defense Agency’s (SHIELD) program, which is part of the broader Golden Dome strategy, focused on building resilient, layered protection against air, missile, space, cyber, and hybrid threats from all operational domains. The selection positions AST SpaceMobile to compete for a wide range of future task orders across research, development, engineering, prototyping, and operations of critical Missile Defense Agency systems that support U.S. national security objectives.

Additional U.S. Department of War (DOW) uses include:

• Radar – Supporting high-value military radar applications such as synthetic aperture radar (high-resolution imaging using radar signal reflections), ground-moving target indication, and missile tracking.

• Assured and Alternative PNT (Position, Navigation, and Timing) – Providing a stronger, jam-resistant signal compared to existing GPS, improving indoor reception and cybersecurity through authentication and encryption.

• Blue Force Tracking (BFT) & Identify Friend or Foe (IFF) – Improving situational awareness of troop and asset locations, reducing friendly fire incidents.

• UAS/Drone Control – Enabling remote control of unmanned aerial systems (UAS) in areas lacking terrestrial infrastructure.

• Signal Intelligence – Detecting and reading electromagnetic emissions of the enemy.

• Signal Jamming – Jamming enemy signals over large geographical areas, such as maritime zones and remote areas, where terrestrial jammers are impractical.

✅ Europa Track 2 Opportunity

In February, AST entered into an agreement with the United States Space Development Agency (SDA) for the Europa Track 2 Commercial Solutions program. The agreement has a total contract value of approximately $30 million. The Europa Track 2 effort is focused on delivering immediate, operationally relevant tactical communications capabilities to U.S. forces around the globe. While just an initial agreement, successful trials could lead to large, recurring government service contracts that harness the dual-use BlueBirds’ global reach, broadband capabilities and encrypted communications.

✅ First Responder Opportunity

AST is also poised to enable supplemental coverage for U.S. first responders (law enforcement, fire/rescue, EMS, emergency management) who require full geographic coverage and 100% uptime, including during natural disasters, in order to provide mission-critical services.

AST is partnered with both AT&T and Verizon, and integration continues with AT&T’s FirstNet partnership in the U.S. AST recently announced a Definitive Agreement with Singapore’s DSTA (Defence Science and Technology Agency) which builds on a previous MOU and we believe AST is working with numerous MNOs and or governments in Europe, the Middle East and Central and South America to expand public safety connectivity. We believe these hybrid-partnerships will be an important and stable part of their business going forward.

✅ International Opportunity

Most developed nations will want defense and emergency services capabilities similar to the U.S. For example, we understand that NATO’s future SATCOM program is actively exploring using AST for 5G direct-to-device service. And Vodafone, AST’s joint venture partner in Europe, offers mission critical emergency services to first responders. They plan to add direct-to-device mobile broadband satellite services to this offering across the EU when it is available through their Satellite Connect Europe joint venture.

To estimate AST’s non-U.S. defense opportunity, we begin with our U.S. DOW revenue estimate of $1.0 to $2.5 billion per annum. We haircut this by half to reflect smaller NATO and non-NATO allied nation defense budgets (cumulatively $0.5 trillion vs. $1.0 trillion at DOW), and adjust further because these nations will likely spend a lower percentage of their budgets on satellite capabilities, leveraging the U.S. Golden Dome where permitted. In total, we estimate that AST will generate $300 to $750 million in annual revenue from non-U.S. defense spending in the intermediate term.

To estimate AST’s non-U.S. first responder opportunity, we begin with our U.S. first responder revenue estimate of $720 million per annum. We adjust our U.S. number to account for differences in population and GDP (across all developed nations, ex-China) and further adjust for the likelihood that AST will have lower first responder market share internationally. In total, we estimate that AST will generate $400 million in annual revenue from non-U.S. first responders in the intermediate term.

✅ Total Military, Intelligence, and First Responder Opportunity

In total, as previously itemized, we expect AST will generate $2.4 to $4.4 billion in annual revenue from worldwide military and first responder opportunities in the intermediate term.

Beyond this, the U.S. National Intelligence Program has a budget of about $80 billion (vs. about $1 trillion at the DOW), which we do not specifically account for in this exercise. That said, it seems clear that many of the capabilities that AST is potentially providing to the DOW would also be valuable to intelligence agencies both here and abroad.

✅ Strides Made in AST’s Satellite Fleet

Over the course of 2025, AST made enormous strides in the design, construction and assembly of its full-size (2,400 SF) dual-use, low-band communication satellites that will become the backbone of its fleet. In December 2025, after the successful launch of the first, full-sized Block 2 Bluebird 6 satellite, AST announced that it had stabilized the spacecraft and fully deployed its massive phased array. Our discussions with the company lead us to believe the satellite is performing as expected mechanically. The next step is to dial-in the software used to control beamforming and RF transmissions. This requires an iterative process that involves software elements that control the satellite, the ground station antennas and AST’s equipment that interconnects with the MNO’s core network. Though time consuming, these learnings will be adapted across all the satellites launched in the coming years.

✅ A Short-Term Setback

In February 2026, AST shipped B2BB 7 to Cape Canaveral for launch on a Blue Origin New Glenn rocket in mid-April 2026. A successful launch on a New Glenn rocket would represent the third global launch provider AST can use for launch services and an important milestone as AST seeks to diversify its service provider network and keep multiple parties competing for its launch business. Though the boost stage worked flawlessly, the second stage failed to lift B2BB 7 to its intended orbit. While the satellite separated from the launch vehicle and powered on, the altitude was too low to sustain operations. Consequently, the satellite was de-orbited a few days later and burned up in the atmosphere. One consolation is that the cost of the satellite is expected to be recovered under an insurance policy. The FAA is leading an investigation into the second stage failure and it may be a month or more before the findings are released and Blue Origin’s modifications are approved and implemented. Blue Origin is slated to be an important provider of launch services in the second half of the year for AST but a thorough investigation is warranted before they can resume launches from Florida.

AST is currently in production through BlueBird 32 with BlueBirds 8 to1 0 expected to be ready to ship to Cape Canaveral by mid-May with production and launch cadence picking up from there. As they ramp to six satellites per month, AST should be able to build and launch approximately 45 satellites this year which would result in activation of nearly continuous service in the U.S., as well as parts of Europe, Japan and the Middle East. Their goal remains a constellation of approximately 90-95 B2BBs in service by year end 2027.

In the spectrum arena, the company continues its global efforts. They reached a successful conclusion of the Ligado litigation which will allow AST access to North American L-band MSS for its Block 3 BlueBird satellites, the first of which is expected launch at the end of 2026 or early 2027. The B3BBs will use mid-band spectrum (both L & S- band) that will allow more data throughput at faster speeds than the B2BBs. Block 2s are more coverage focused while Block 3s are more capacity oriented. AST is pursing 2GHz S-band spectrum in Europe through regulatory channels and its partnership with Vodafone and is working on MSS applications in Brazil, Mexico and other international locations.

✅ Update on Competition

Starlink, a satellite internet constellation wholly owned by aerospace company SpaceX, is best known for its satellite to home internet service. But four years ago, Starlink teamed with T-Mobile USA to develop and launch a new and well-funded direct-to-cell competitor to AST. However, Starlink’s planned direct-to-cell voice and data service is now limited to simple text messaging, location sharing, and a few essential apps that offer VOIP but no broadband or internet connectivity. To work, the service requires users be outdoors with a direct view of the sky while their handoff puts a heavy strain on a cell phone’s battery. Starlink plans a reboot with newly designed direct-to-cell satellites with new capabilities. These are expected to launch on its larger Starship rocket after receiving regulatory approval.

In April, Amazon announced that it will acquire Globalstar, a mobile satellite services operator known for powering Apple’s Emergency SOS feature, in a $12bb transaction expected to close in 2027. This text only direct-to-cell offering will be paired with Amazon LEO, Amazon’s satellite to home internet service whose satellites are just now being launched. Amazon LEO will ultimately consist of thousands of satellites and compete directly with Starlink’s satellite to home internet services. It will likely be 2-5 yrs before Amazon LEO has the capacity or coverage to compete with Starlink on home internet services. And we believe that AST will not see any additional competition from a revamped or reconstituted Amazon / Globalstar based direct-to-cell service before 2030.

We believe Amazon will receive the necessary regulatory approvals over the next year to acquire Globalstar based on recent comments by Federal Communications Commission (FCC) Chairman Brendan Carr who went on record saying he supports three direct-to-cell competitors in the U.S. The question remains, will Amazon/Globalstar remain a bolt on service with the MNOs (like Starlink direct-to-cell or Apple SOS today) or will it take the much more difficult route over the remainder of the decade of engineering a service that integrates into an MNO’s core network as AST has already done.

✅ Excellent Management

Supporting our view, we believe that AST founder, Chairman, and CEO, Abel Avellan, has assembled a first-class space and wireless technical team, paired with strong commercial, regulatory and legal talent. They have now put in place a team of close to 2,000 employees in five countries. Over the last five years, we have had the opportunity to meet many of their senior leaders, engineers, scientists and Midland factory employees during our visits to headquarters in Midland, Texas and during the launch events in Cape Canaveral. In addition to their employee growth, AST continues to add industry thought leaders and partners to its Board of Directors.

✅ Summary

The last six months showed increasing operational momentum, growing government interest, artful balance sheet management and new company forecasts of revenues approaching $1 billion in 2027, the first full year of continuous coverage across key markets. The company recently filed to increase its constellation shells to four and its satellite count from 248 to 543 at the ITU (International Telecommunications Union). These planned satellites will now include Mobile User Objective System (MUOS) augmentation bands, low-band and S-band capabilities and circle the globe in staggered attitudes up to 740km in two new inclinations of 40- and 55-degrees - including up to 28 sun synchronous and 18 equatorial satellites. Look for more information flow from Europe around their work with Vodafone on IRIS2, Satellite Connect Europe and S-band allocations over the course of the year. In the U.S., the FCC has granted AST full commercial authorization to deploy its initial shell of 248 non-geostationary satellites while the ITU application to expand to 543 is pending.

We continue to believe we are on the cusp of a new communication revolution with decades of potential growth in front of it, and believe AST will play an integral role. AST is a “special situation” investment for the Hennessy Focus Fund, as it does not meet the Fund’s typical compounder model of historically producing a sustained mid-teens or higher rate of earnings growth. However, we believe it presents a very compelling “emerging compounder” profile with a favorable risk-return profile at today’s price.

Original Weblink: hennessyfunds.com/insights/c…

3

204

May 17

May 17

$ASTS: "The D2D joint venture is a hedge or response against SpaceX."

In particular, the JV will focus on pooling spectrum as well as IP related to maximizing D2D capabilities. 🤝

@AST_SpaceMobile and @blueorigin voiced public support meanwhile @SpaceX's top brass expressed shock and basically "challenge accepted"!

Great discussion here by @anshelsag and @mikeddano!

1

27

966

🅰️ncap retweeted

May 15

AST SpaceMobile may launch some of its direct-to-device satellites on United Launch Alliance’s Vulcan rocket to expand the launch options for its constellation. bit.ly/3PjrdR6

6

44

349

25,066

🅰️ncap retweeted

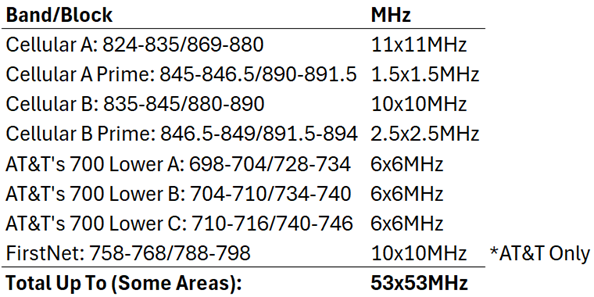

$ASTS Let’s talk details on AST SpaceMobile’s SCS Authorization that was issued last week. As part of the process, AT&T/Verizon leased AST access to the Cellular A/B, Lower 700MHz, and FirstNet (AT&T Only) bands under various scenarios (up to full access in Outages).

*Not an expert, just sharing my findings after doing some digging. Let me know if you find any errors.

1/n

4

14

135

29,547

🅰️ncap retweeted

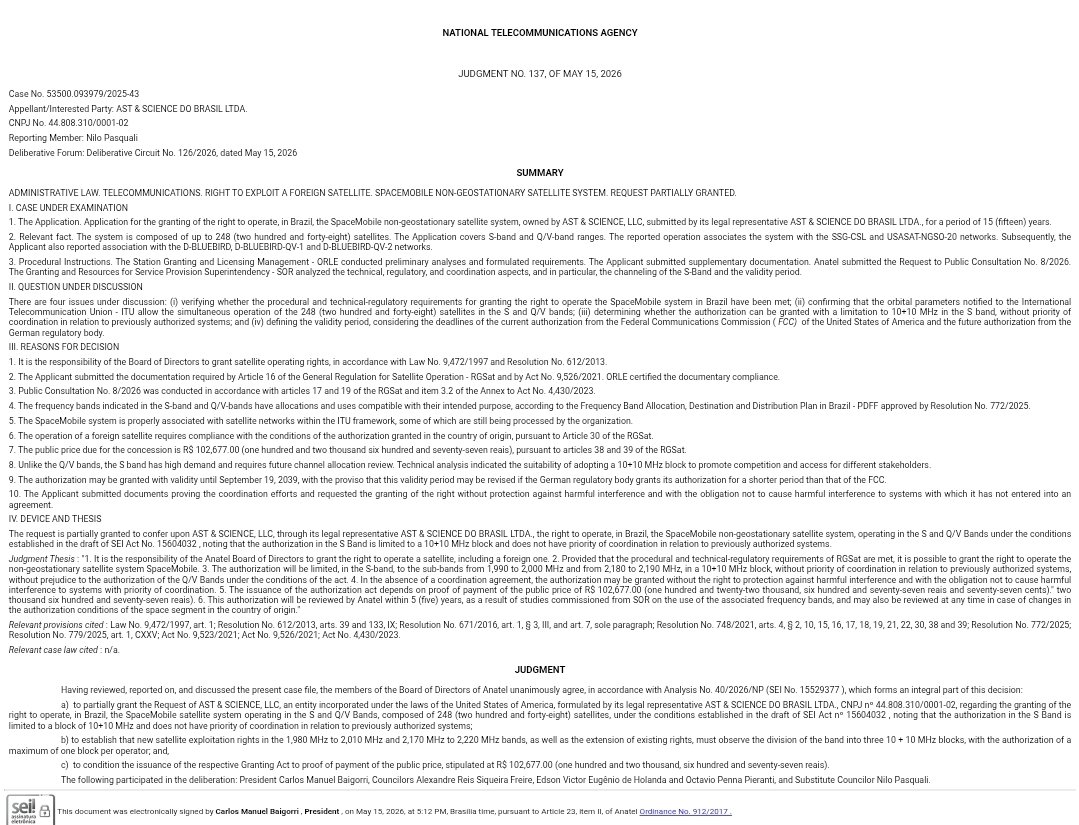

May 15

$ASTS Anatel Brazil authorized to operate the 248 satellite constellation. Brazil has over 200M inhabitants and over 100% penetration rate of mobile phone users.

May 15

$ASTS Breaking News! AST SpaceMobile is authorized by Brazil's ANATEL to operate a 248 Satellite Constellation consisting of S-Band and Q/V Feeder. Specifically ANATEL granted AST access to 10x10 MHz of S-Band Spectrum in the 1980-2010 and 2170-2200 range. A HUGE WIN for AST!!

2

18

176

6,335