1,619 Photos and videos

🔥😂

Handled @elonmusk at @BedBathBeyond … please send ticket to space at intern@beyond.com

2,407

4,087

46,959

3,772,284

Liquidity retweeted

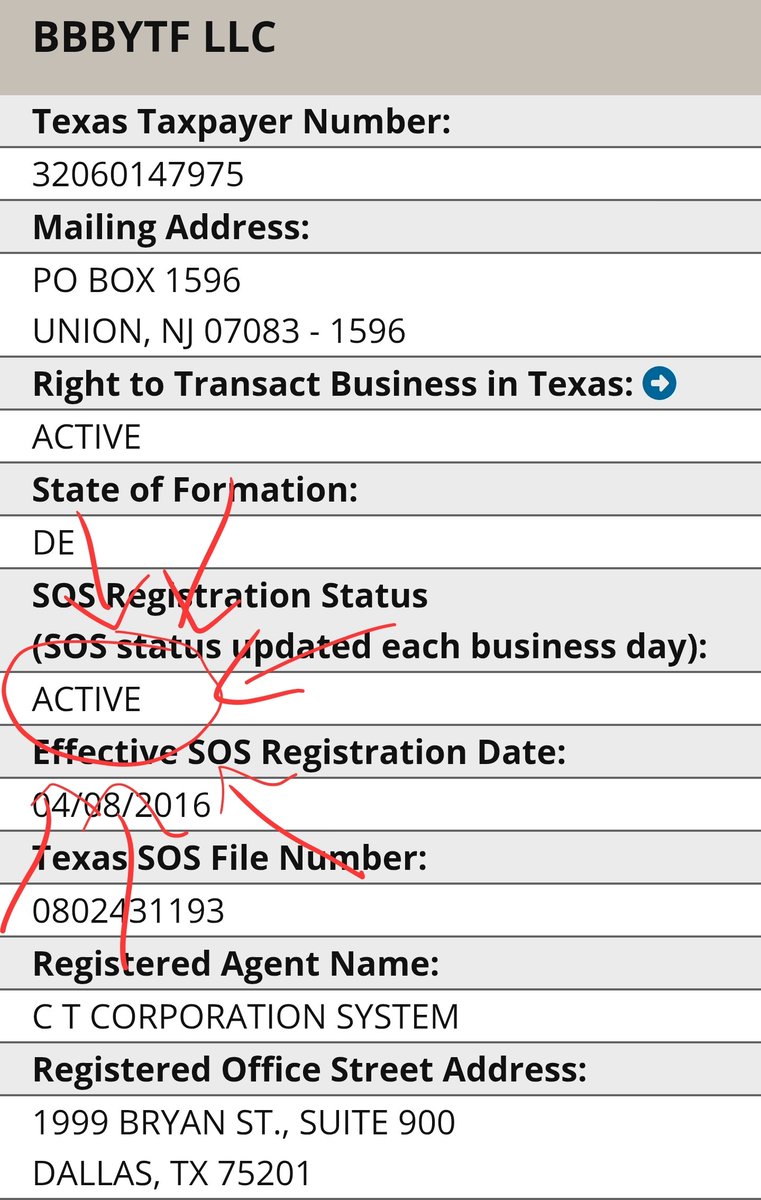

If you've seen Jake's latest video, here's a reminder that BBBYTF LLC owned by Flexport (👀) is still a tax paying ACTIVE operating entity in Texas as of today, despite the estate being "sold" in 2023

We emerge between July - December 🦋

source comptroller.texas.gov/taxes/…

28 Jan 2024

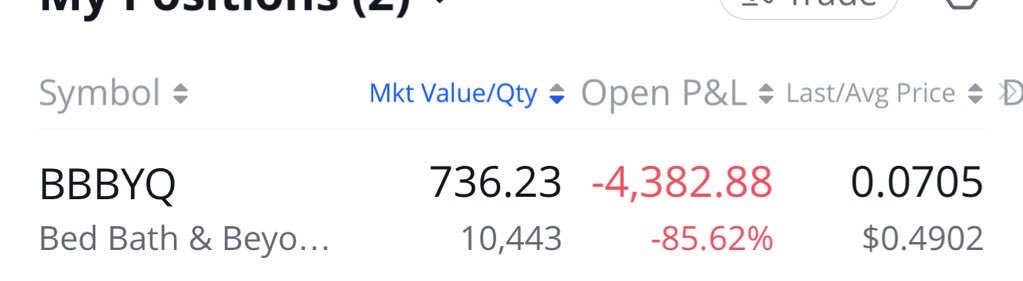

$BBBYQ - Emerging Entity

I firmly believe there’s enough circumstantial evidence to assume that, on the balance of probability a carve out of Buybuybaby is occurring and we are correct in the ongoing thesis that equity will be preserved through an emerging entity which will utilize the $1.6bn in NOL’s and delivery value to $BBBYQ shareholders and creditors.

To explain this, I can’t give you a simple one sentence in a docket that proves it, due to the complex nature of this billion-dollar Chapter 11, with strong indications of fraud, 380 redacted hours of legal services and thousands of dockets, we need a holistic analysis of all contributing factors pointing to a likely outcome.

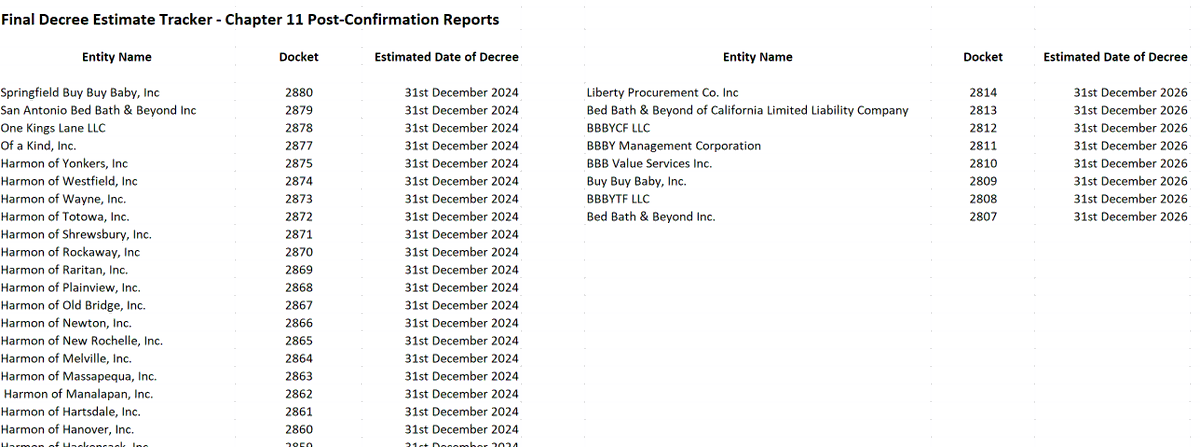

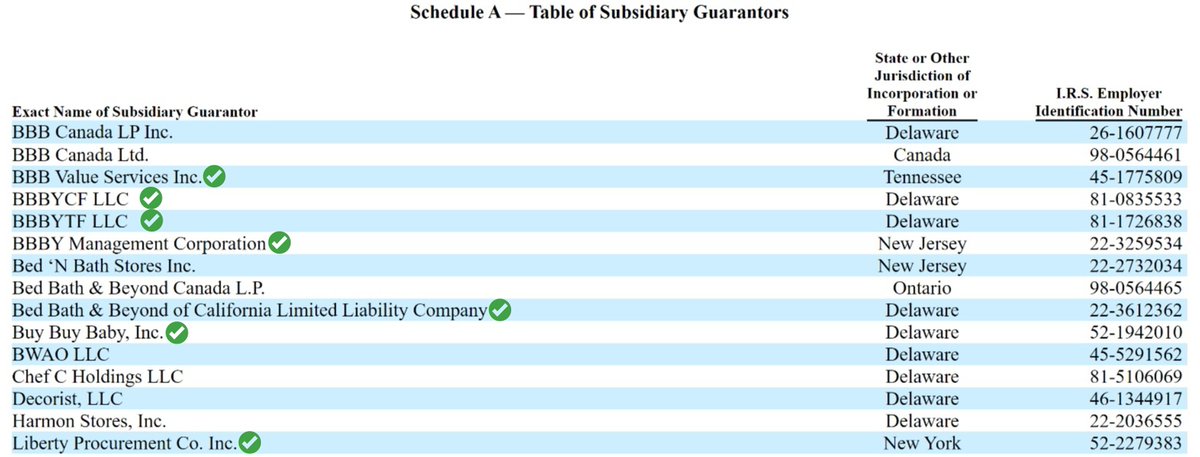

73 dockets were filed this week, which had Post Confirmation information, the most interesting part was the Plan Administrators estimate to when a final decree would be issued on 8 subsidiaries out of the 73 that were filed, with the remaining 64 subsidiaries given a more near term estimate of December 2024.

This is exciting to see, as it discredits the pocket watchers’ theories of the Chapter 11 being complete and that we’re heading into Chapter 7 liquidation and that will be the end, au contraire, because even the Plan Administrator can’t give an estimate to the end of this reorganization, let alone uninformed and uninvested pocket watchers.

While the Plan Administrator commented that he is unsure when the final application to close the chapter 11 bankruptcy cases will be filed. The date December 31, 2026, is just a temporary guess. The actual date will depend on various factors like the length of legal proceedings, asset collection, claim settlements, and the winding down the process.

But what do those 8 subsidiaries have in common?

Source:sec.gov/Archives/edgar/data/…

As pictured above 7/8 of them are Subsidiary Guarantors for the October 2022 note offerings by $BBBYQ. The ninth entity is Bed Bath & Beyond inc. which is now 20230930-DK-BUTTERFLY-1. Interestingly, the notes were offered exactly 60 days after Ryan Cohen sold his position, could there have been a cooldown period he was waiting for before buying convertible bonds in $BBBYQ? Would this explain why Ryan Cohen is listed as a creditor in the dockets?

To me, these correlated activities seem to infer that a creditor has control over the outcome of these subsidiaries, which is why the Plan Administrator can’t comment on the completion of their wind down attempts.

Here’s some key reminders that support the emerging entity via carveout theory:

- Ryan Cohen stated in his letter to the $BBBY board that Buybuybaby was extremely undervalued and projected it could be transformed into “The Ultimate Destination for Babies”

- Buybuybaby.com didn’t trade for 126 days post IP sale, as a comparison Overstock began using the Intellectual Property within 14 hours. Why lost 1/3 of your annual revenue?

- Buybuybaby Inc. hasn’t been renamed, the way that 20230930-DK-Butterfly-1, Inc. is formerly Bed Bath & Beyond Inc, are we correct in assuming it’s a shared service agreement?

- Go Global Retail offered up to $60M for IP rights and assets in Buybuybaby, however the debtors allowed a much lower bid of $15.5M for just the IP rights to be sold to Dream on Me, despite this being a value maximising Chapter 11.

- Sixth Street were in negotiations with Patty Wu for Baby in a Stand-Alone Basis/Scenario, referenced in Docket 2040. Did they suddenly lose interest? Unlikely.

- Holly Etlin mentioned recently on a Round Table panel that Sixth Street were still seeking recovery on their investment as DIP lender in $BBBYQ

- Sixth Street own 87% of the current secured debt and have positioned themselves to do so.

Buybuybaby is reported to be planning to open up to 100 stores within three years, reported in November 2023, one week before the website went live again

source: modernretail.co/operations/i…

Given the ambitious scope of this operation, aimed at rebuilding the brand to nearly its pre-Chapter 11 stature, considering there was a 126-day delay before resuming trading. This interval likely indicates that extensive negotiations and restructuring within the corporation were underway. Key focus areas during this period probably included legal and organizational restructuring, as well as addressing these securities-related matters:

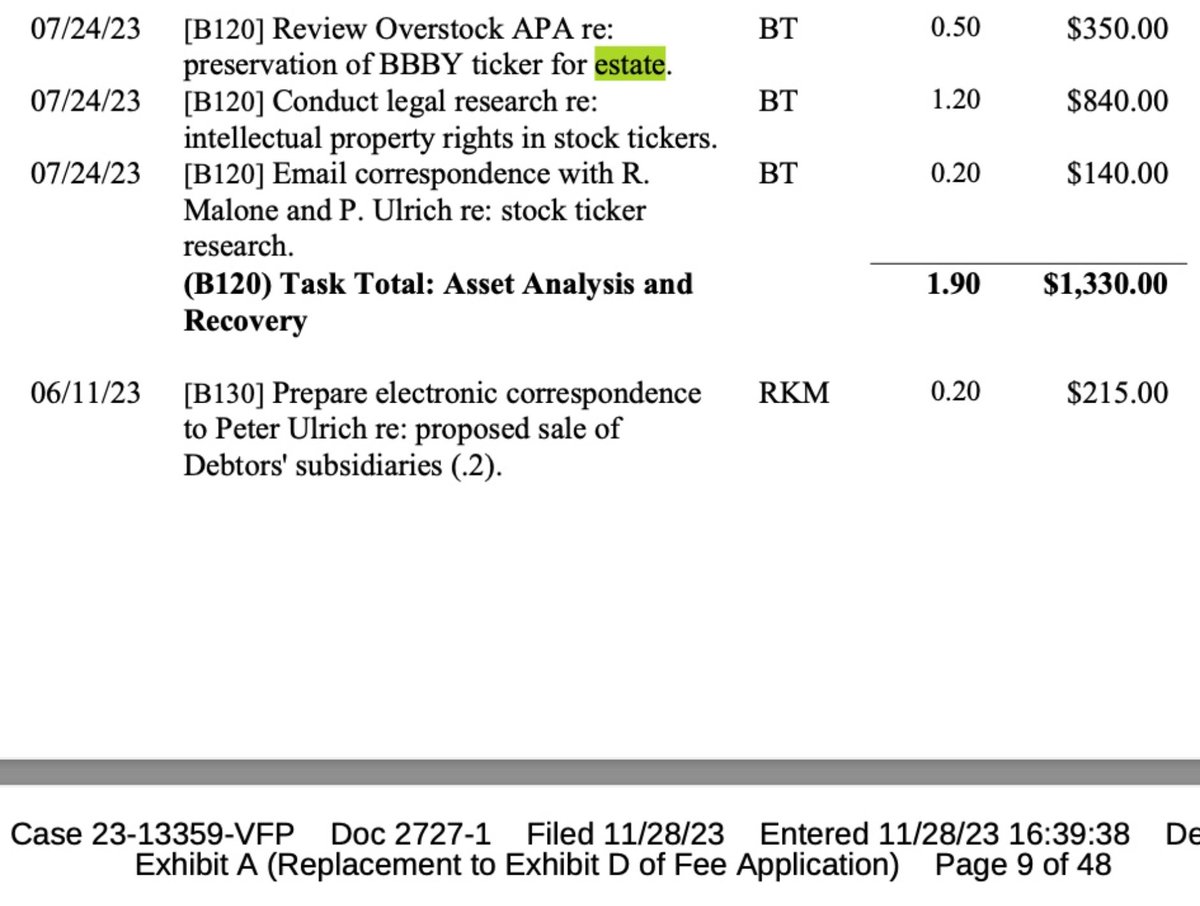

Docket 2727 Page 9 . Code [B120] is Asset Analysis and Recovery. Preservation of BBBY ticker for estate and conduct legal research into intellectual property rights in stock tickers, these are discussed nearly a month after the intellectual property rights auctions concluded.

Could this be why Overstock had to use the ticker BYON because BBBY have preserved the ticker?

Why are they researching intellectual property rights in stock tickers anyway? The bankruptcy judge wouldn’t sign off these legal services if they weren’t relevant to the outcome.

Also as confirmed by Delaware flings and the Buybuybaby website, the owners of Buybuybaby are listed as “BBBY Acquisition Co LLC” which I believe is a placeholder name for a SPAC while the finished corporate entity is completed. Why name the company after the ticker?

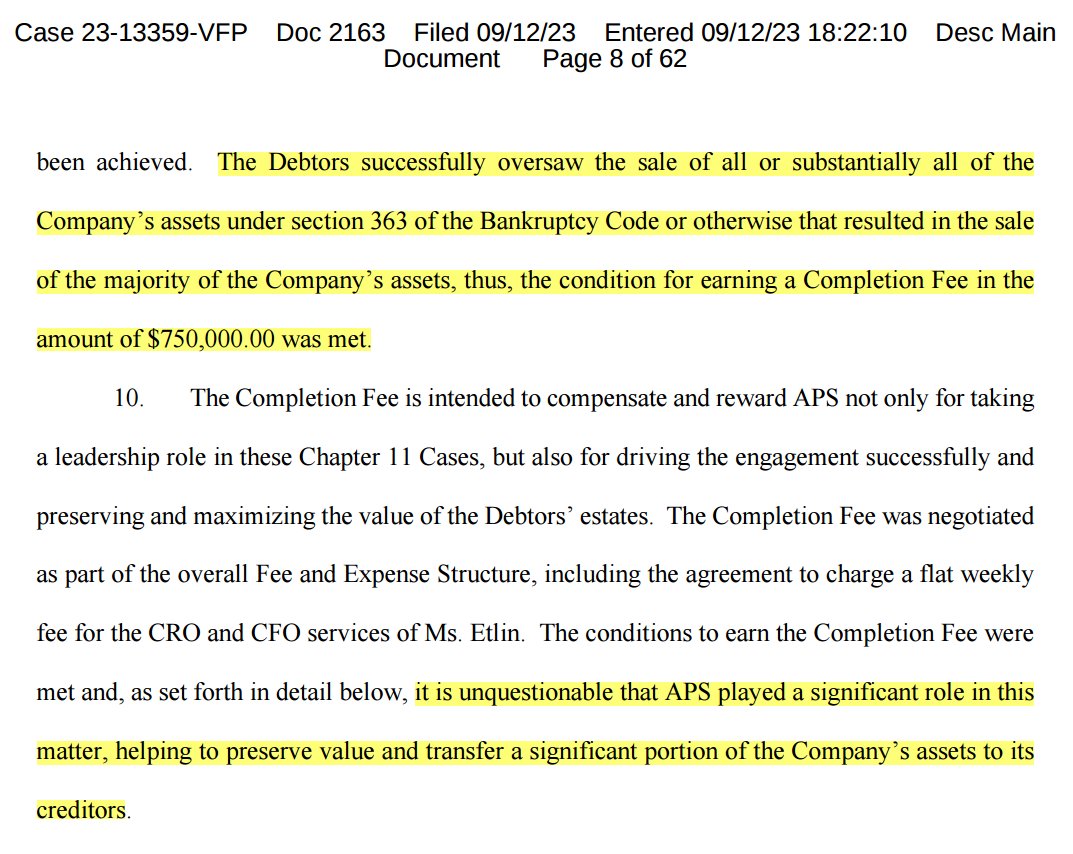

Lastly and most importantly, Docket 2163 page 8:

This is AlixPartners completion fee and tasks completed, filed 2 days before the plan was confirmed. “Preserve value and transfer a significant portion of the company’s assets to its creditors?” Where? The creditors have accepted a plan that gives them 0-2.5% projected recovery? Where is this waterfall distribution of proceeds?

I believe the credit bid is coming, the third amended plan is coming, debt for equity is coming and shareholders will also be coming. Jake2B/@jake2b has highlighted many times the amount of work that has gone into the NOL’s, the business enterprise continuity requirements have been satisfied. The value of the NOL’s until February 2023 is the same amount as the current secured and unsecured debt of $1.6bn. This is the only way Sixth Street make the best recovery on this investment.

🔁Please Repost if this titillated you.

12

38

294

22,797

Liquidity retweeted

Handled @elonmusk at @BedBathBeyond … please send ticket to space at intern@beyond.com

Time to get that volcano lair I’ve always wanted.

I think it’s in the “Beyond” section of BB&B.

444

660

8,173

3,980,779

Schedule Update: #UFCWhiteHouse live event coverage on @paramountplus will begin at 8pmET

390

415

6,095

2,194,060

Liquidity retweeted

Jun 14

Listen closely it says bed bath and beyond

Turn the volume all the way up 🔊

Have you Heard? "BBB" 👀👂

x.com/i/status/2065860524718…

18

14

166

15,522

Liquidity retweeted

Jun 14

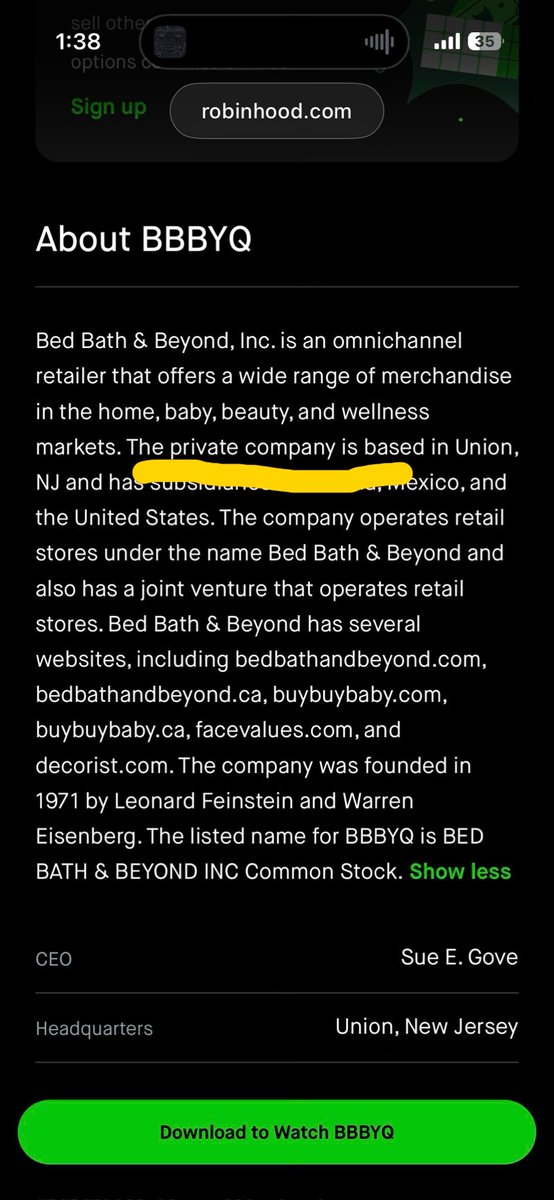

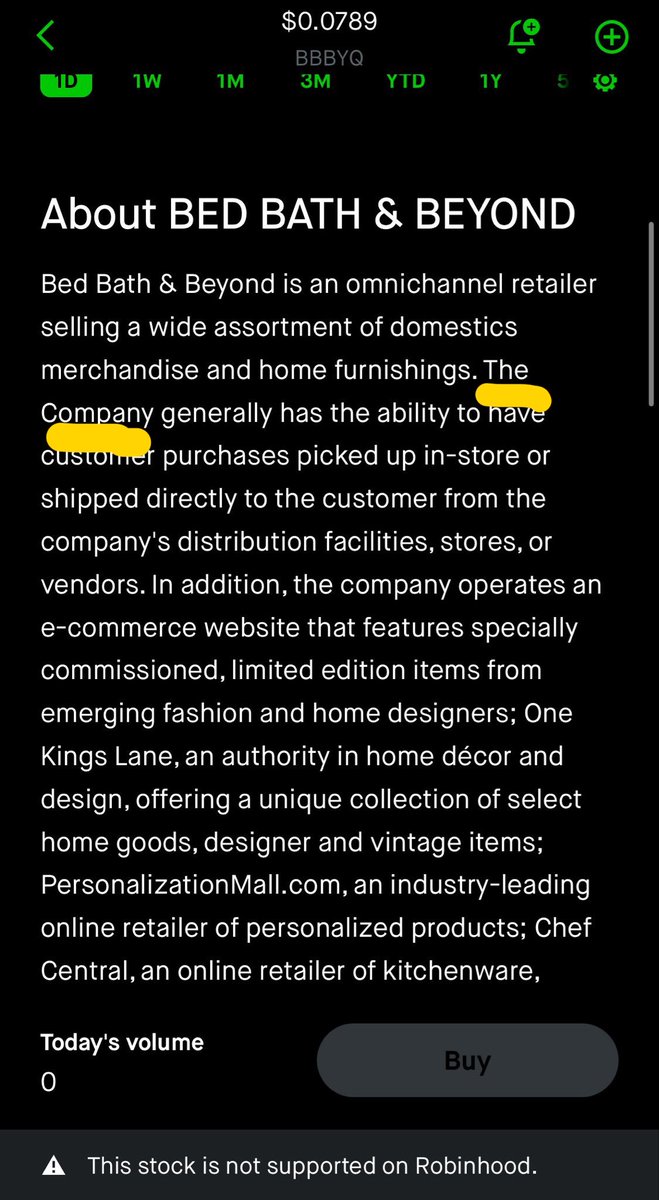

JUST IN 🚨

ROBINHOOD CHANGES BBBYQ DESCRIPTION LABELING IT AS A PRIVATE COMPANY. NEW DESCRIPTION TO THE LEFT OLD DESCRIPTION ON THE RIGHT.

CREDIT JON

34

76

737

43,303

Liquidity retweeted

Jun 12

My whole timeline is full of millionaires complaining about a trillionaire

1,546

8,152

107,281

1,398,218

yay! I've uploaded my $BBBYQ video series to YouTube.

the channel link is: YouTube.com/@jake2b and here is a playlist link for all of the videos: youtube.com/playlist?list=PL…

I hope they are still helpful and I'll be adding more videos soon. I appreciate everyone's kind words and support plus the naysayers for the good laughs!

68

104

621

37,181

I started a YouTube channel that will begin with my $BBBYQ video series uploaded if you prefer to watch or listen there. I've starting with Part 1: Interests; here is a direct link: youtu.be/s3aUVz1M_As

more soon!

Part 1: Interests

in my first video I explore the definition of the word "Interests" ...

youtube.com 76

186

874

72,889

Liquidity retweeted

Jun 5

Ryan Cohen Is Ready to Talk About eBay. For Real. trib.al/EOAPflx

25

98

592

43,822

Liquidity retweeted

Jun 5

$EBAY - RYAN COHEN PUSHES eBAY BID DESPITE REJECTION

Ryan Cohen says he remains committed to acquiring eBay, despite the board rejecting GameStop’s offer as “not credible.” He told Barron’s he may take the bid directly to shareholders and argues the deal would unlock value through cost cuts and synergies in collectibles and e-commerce. GameStop now holds a 7.8% stake in eBay. Cohen says eBay is “underearning” and insists he can improve profitability significantly.

54

79

922

134,222

I’m excited about the share buyback authorization like everyone else but in my opinion, I don’t think it will be utilized now. lowering the balance sheet cash would make it more difficult to conduct the bond roadshow, both in the ability of how much can be raised and would result in higher interest rates from fixed-income investors based on risk. you want to look strong when marketing yourself for investment.

if a genie granted me a wish the ideal series of events would be to raise a ton of corporate debt, have the market sink the stock price to middle earth on this news (“oh no, huge leverage! they’re going bankrupt!”), buy back down there, note holder arbs go super long, the stock price explodes, present the tender offer to eBay shareholders at that price with the goal of dipping into authorized shares as little as possible.

we’ll see.

8

14

225

7,746

Liquidity retweeted

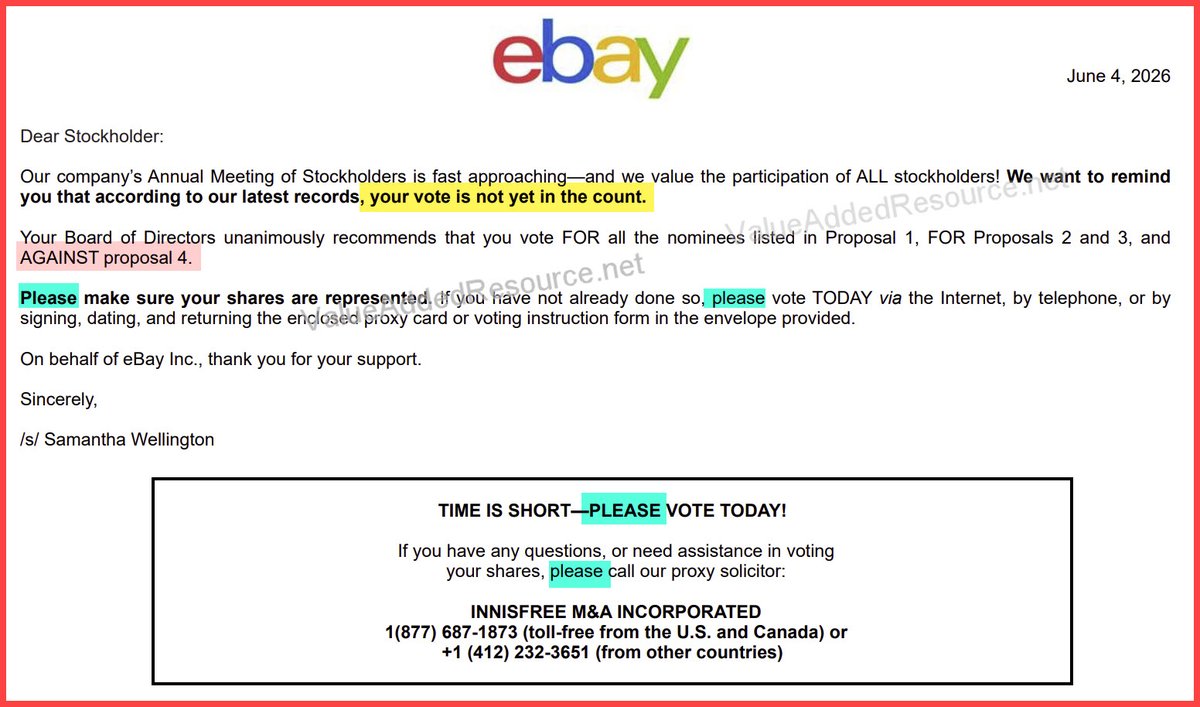

The eBay board are begging shareholders not to let Proposal 4 pass.

If it passes it could give Ryan Cohen an expedited path into the $EBAY board

More information here 👇

x.com/PhantomBlack699/status…

"Again, if you are an $EBAY shareholder...Please, Please, Please, Please vote AGAINST Proposal 4!"

🙏❤️ Desperate Entrenched eBay Board

$GME @ryancohen 😂

x.com/ValueAddedRS/status/20…

12

94

626

45,739

Liquidity retweeted

The walls are closing in for $GME naked short sellers

🚀 $9bn cash on hand

🚀 Profitable company with no short term debt

🚀 Bitcoin Treasury reserve company

🚀 Roaring Kitty can return at any time

🚀 CEO that takes no salary and owns ~9% of the outstanding shares

🚀 CEO that will do whatever it takes to acquire eBay and bring customer delight to the 135M global customer base through a combined business

🚀 Historical short sellers and stock antagonists such as Andrew Left are facing upto 25 years in prison

🚀 GENIUS & CLARITY Acts are rapidly progressing allowing Tokenized Securities (Overstock V2)

🚀 S&P at all time high

🚀 Huge retail investor base Direct Registered and holding for the long term

🚀 TEDDY 😉

This will dwarf the VW/Porsche squeeze in magnitude. Be excited.

14

74

754

27,868

part 7: I would like to share compelling points relating to the HBC equity raise and its use to secure the position of the Holder of Interests, which forced participation in the $BBBYQ third-party release. I hope you like it.

$BBBY

(old).

part 6: my thoughts on the January 13, 2023 LBO and its intended (and failed) use to force $BBBYQ into insolvency.

I hope you like it. $BBBY (old).

79

154

648

58,495