Founder @magnolia_rails | banking 🤝 crypto 🤝 fintech

Joined August 2013

- Tweets 6,904

- Following 1,002

- Followers 2,851

- Likes 14,057

434 Photos and videos

Jun 11

> Could make me an idiot, who knows. But I’m not going to pretend I understand things I don’t.

Me every time I ask a “dumb” question no one else in the room has a good answer for

Jun 11

What? I’m not going to get invited to Bitcoin events and my career will fail for asking questions?

I’ve always held myself to be honest and authentic. I have questions about some of this stuff. Could make me an idiot, who knows. But I’m not going to pretend I understand things I don’t.

And for what it’s worth, I was literally on my way back to my hotel when I got a text asking me to come back and ask those questions publicly.

I’m just a guy with questions. It’s really not more complicated than that.

2

7

955

Jun 10

Incredibly true.

Jun 9

JUST IN: Traditional financial firms are rapidly embracing crypto, Axios reports.

2

237

Harsha Goli retweeted

Jun 5

Fiat is a sham, the banking class is corrupt, decentralized digital currency and the blockchain are the inevitable future, and the incumbents will fight it to the death.

291

275

2,841

701,874

Jun 5

Is truly private money without a publicly verifiable backstop a good thing?

Inability to verify integrity is quite devastating

Jun 5

How would we know a white hat was the first person to discover it?

🤷🏻♂️

The upside of zcash is now the downside. You can’t prove one way or another.

6

562

Jun 4

Your stablecoin may not be redeemable for cash!

Especially during a bank run.

Let me explain: genius compliant stablecoins require 1:1 reserve backing, with few permissible cash alternatives like Tbills (which most people use).

Tbills are like cash, but not cash. Just like any asset, if you sell enough of it there are liquidity concerns.

If the reserve partner is suddenly faced with a need to liquidate 5B for instant conversions, there’s probably blood in the water and everyone’s doing it too.

This could mean terrible spot prices for Tbills, resulting in an actual death spiral for the stablecoin and maybe even the bank.

How do you, as the account controller solve this scenario?

Simple. You don’t serve during a bank run (which could be a catastrophic event for you).

Which means, during a bank run - your stablecoins may not convert into cash, because there’s a run going on.

Theoretically, once the run is over (or over the next few weeks) the bank will process cash conversions on their schedule to prevent liquidation issues with the Tbills.

Or another well capitalized lender could step in to help alleviate in the short term (in tradfi, this is the lender of last resort aka the central bank).

But all this means there is bank run liquidation risk for your 1:1 backed stablecoin.

Don’t hodl your net worth in a stable that isn’t paying you for the risk!

3

328

Jun 2

What if instead of monopoly busting the DOJ funded direct competitors.

AWS controls 90% of data centers? Inject Digital Ocean with some cash.

Adobe/Figma merger super anticompetitive? Buy out figma for the taxpayers

4 companies control all meat packing? Start a government run 5th with competitive prices.

It’d lower prices and cultivate innovation (instead of destroying value)

Congress should start the next venture fund

1

2

303

May 28

The bank partner for @bridge everyone.

You’re all crazy, debanking isn’t real

May 28

uh. major major miss.

1

8

1,285

May 28

There can never be a world where your savings device makes good money.

Never.

As long as the economy grows (which is has to to support a growing population) money needs to be slightly deflationary.

Why? Because if money gained value over time no one would spend anything (anyone remember the pizza purchase?)

That is direct friction against money’s main purpose, to be interchange between assets.

The second it’s an asset is the second it’s not money anymore.

Hodling stablecoins should be just as stupid (if not more) as hodling cash.

10

5

3,124

May 28

As more services drop fiat 🔁 stablecoin conversions down to zero, interesting patterns and problems emerge.

Stablecoin 🔁 fiat requires liquidity management, expensive licenses, and is still at risk to chargebacks (for fiat -> stable).

These costs aren’t negligible. Who bears them?

What’s even more interesting is how low margin all stablecoin service products tend to be.

Stablecoin issueance for example may sound glam, but is actually low margin/loss leader for many.

Liquidity management while maintaining yield is complex, especially for smaller stables that could experience sharp spikes of activity.

If you investigate where dedicated, licensed issuers are now, they’ve expanded product offerings to try to capitalize on their stablecoin clients.

All this to say, there’s a lot of cost here for something that’s dropped down to no fee in less than a year (rightfully so).

So where’s the margin?

Are stablecoins doomed to become CAC?

May 28

zero

3

7

2,676

Harsha Goli retweeted

May 26

Bitcoin/crypto/stablecoins will never succeed at replacing visa or the dollar.

I’m gonna make a lot of people mad with this one.

What does everyone complain about when it comes to trad rails?

- too slow to settle

- too expensive

- too permissioned

But does anyone know why these consumer rails behave this way? And why they continue to behave this way?

It’s not because “banks don’t care” (tho there is truth to this)

It’s not because “There’s no incentive to innovate in a monopoly” (tho there is truth to this)

It’s not because “the powers that be like it this way” (tho there is truth to this)

It’s because of 2 words. Consumer protections.

> too slow to settle

Settlement times range from 3 days for ach to land to 90 days for the chargeback window. Even more for credit card payments.

Y’all know what a chargeback is? We all hate them as merchants/providers, but when you’re a consumer and your card has been stolen - it’s the only thing protecting you from a devastating financial loss.

That’s it. That’s the only reason domestic payments take so long to fully settle, and why we have to rely on things like intermediary float accounts, why compliance costs are so high (it’s actually very easy to be aml compliant! It’s very hard to lower chargeback rates).

Stablecoins, bitcoin solve this… by eliminating consumer protections. Feel free to counter this point only if you’ve worked customer support at a crypto payments company. You’ve seen the jarring amounts of money these people have lost, sometimes through no fault of their own. It’s horrible, devastating, and sometimes tragic. People end their lives over these situations.

What we do is no joke, and it’s easy to forget that sometimes.

Chargebacks do prevent this. If you care about preventing these situations, they work quite well.

> too expensive

> too permissioned

Not just the 2-5% on each tx for visa/bank interchange that merchants pay. The compliance costs of stringent kyc (especially in EU, god have you seen the rates!!) and of kyt.

Yea it’s def too much. But it’s too much for 2 reasons.

1. Payment rails commoditize over time (sorry dozens of neobanks)

2. Laundering stolen crypto is common, and vigilance isn’t just a moral/social imperative, it’s a legal one (shoutout binance)

So you have this situation where in order to get people to use your rail, you have to add in direct incentives (merchants somehow still go along with this bc they just pass costs down) and you have to implement heavy compliance machinery to make sure you’re not touching dirty money.

High costs mean only one thing: high volume is the only way to maintain p&l

Visa & co have the upper hand here. They have 2 things that allow their throne to be virtually dethronable

- consumer protections

- extremely high volume

If you’re a monetary usecase maxi that’s totally fine. I used to be one too. But you have to acknowledge this reality and plan accordingly.

Stablecoins can only thrive in non-consumer usecases (b2b)

Bitcoin can only thrive in speculative usecases (ngu, financial engineering like mstr, long term savings)

19

4

44

7,348

May 26

Pour one out for a real one.

Tab was always the crown jewel of Atlanta’s bitcoin scene.

It always meant a lot to me to be able to bring all my friends to my city.

1

1

31

2,271

May 26

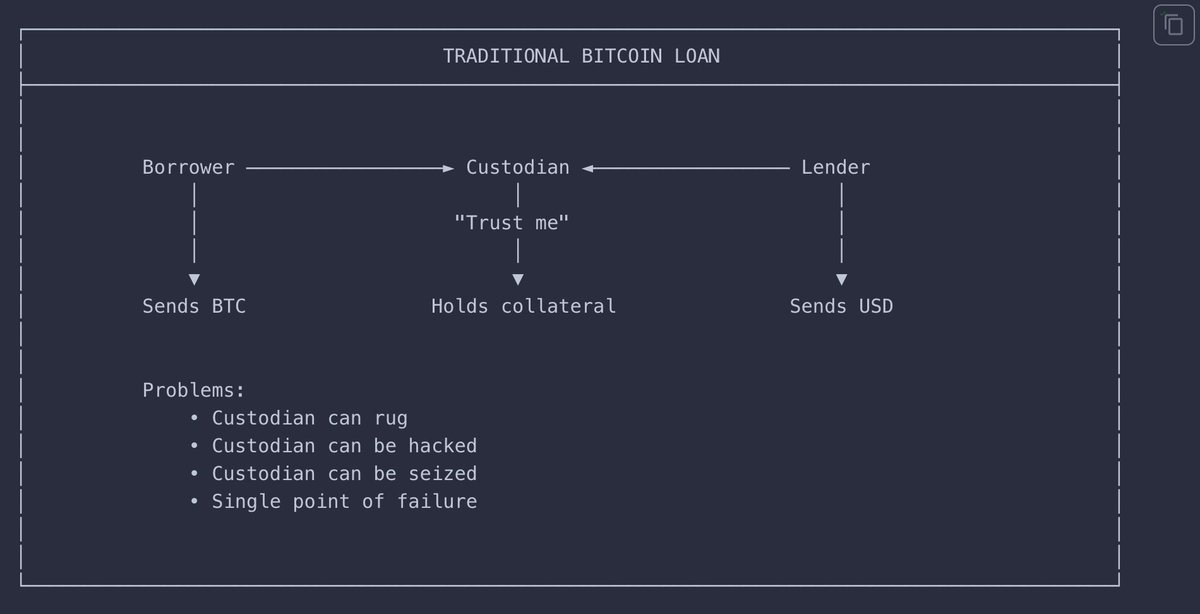

collateralized credit lines are where all asset spend cards will evolve to btw.

Much harder than it seems!

Stop selling your bitcoin to cover everyday spending.

@AvenCard lets you borrow against it with up to a $1 million credit line, up to 10-year fixed terms, and unlimited cash back.

Keep your bitcoin. Spend on your terms.

tftc.io/aven-bitcoin-visa-ca…

3

605

Harsha Goli retweeted

May 26

imo a lot of new founders don't understand the LP-GP dynamic well (i.e. that LPs keep GPs in business, and GPs are expected to pursue strategies they sold to LPs when fundraising). This usually leads to the following sequence of events:

> Fund-fundraising is very hard (I may take crap for this, but fundraising is the only task I think is harder for a GP than a founder). GPs simplify their job of selling their product to LPs by pitching the "hot" thing (e.g. AI), and inventing some narrative about how they are uniquely positioned to acquire the best positions in the "hot" thing (there is already pre-existing allocation interest in the "hot" thing)

> If you sold your LPs "access" to the hot thing, and the market becomes wholly irrational (like it is currently), you're basically stuck having to choose either: 1) overpaying for a "hot" company (questionable long-term DPI strategy) or 2) keeping discipline and passing (but with the risk that your LPs give you short-term crap — read: threat to your n 1 fund — for missing out on the kind of access you sold them on)

Most GPs here will optimize to not have short-term pain (i.e. overpay) and kick the can on returns down the road with (imo, unsubstantiated) platitudes like "what if it's the next Facebook?"

(this also means there is no room for your weird, non-AI startup in their portfolio btw)

May 26

To quote @skupor: “Sins of omission are worse than sins of commission. It’s okay for a VC to invest in a company that ultimately fails, that’s par for the course in this business. What’s not okay is to fail to invest in a company that becomes the next Facebook.”

This becomes a real problem for small and emerging managers if their proposition to LPs is access to consensus-type opportunities.

They end up with a dilemma; to face scrutiny for overpaying, or even greater scrutiny for missing out on seemingly obvious winners. There's also real systematic risk in tying a fund to a particular category where the window of opportunity may close at any moment.

Deal-by-deal SPVs are one answer, but that approach amplifies venture capital's principal-agent conflicts as GPs pass most of the risk to their LPs.

In truth, it's probably just not a strategy that small and emerging managers should pursue. The scaled venture platforms, on the other hand, are relatively price-insensitive, and can pay up when required.

Enjoyed chatting to @arian_ghashghai of @EarthlingVC about this, and many other topics, in the recent episode of Going Solo. Links below.

17

9

87

14,764

Harsha Goli retweeted

May 21

1/5

**The Freedom to Speak: Reflecting on Risk Management, Regulatory Overreach, and Yesterday's SEC Decision**

Yesterday, the SEC made a historic announcement: it officially rescinded its 50-year-old “gag rule” (Rule 202.5(e)), ending the policy that prohibited settling defendants from publicly denying or criticizing the agency's allegations. As Chairman Paul Atkins noted, “Speech critical of the government is an important part of the American tradition.”

3

15

65

8,297

May 19

I’ll be the first to admit, I was dead wrong about this.

Congrats to everyone I fudded!

1

13

1,612

May 18

"They're token people" is probably my favorite crypto vc slur.

Token vc's suck because:

- overly focused on short return window

- might force you to launch a token to rug your users

- are very annoying on calls looking for the token launch oppurtunity (i'm b2b)

4

32

1,275

Harsha Goli retweeted

May 16

Prime Trust would be a 100 Billion dollar company today if they didn’t explode btw

2

22

1,365

May 18

Great simple idea.

Total tarpit.

May 18

someone should build OneKYC

kyc once and get instant access to neobanks, trading platforms, CEXs, etc

there’s massive consumer demand for this, everyone is tired of spending 30 minutes scanning their eyelids every time they sign up for a new app

also massive demand from the platforms themselves

auto kyced users = lower onboarding friction

which equates to higher conversion rates, more funded accounts and more volume

banger of an idea

6

10

3,592