stablecoins @moderntreasury || prev founder @beam_cash (acq) & before that @visa

Joined December 2020

- Tweets 1,937

- Following 2,097

- Followers 3,043

- Likes 10,051

74 Photos and videos

Pinned Tweet

May 19

throughout my years building in this space, i've integrated nearly every iteration of named U.S. account infra on the market and built versions from scratch.

i can say with confidence: this is the best product out there.

via one API, MT's Global USD Accounts offer:

- unique routing and account numbers for users in 90 countries

- embedded stablecoin orchestration

- ACH debits and credits

- instant fiat payouts via RTP/FedNow and push to card

- built-in ledgering & compliance

- soon: international wires, FDIC pass-through, bill pay, RfP, and check issuance

it's full-stack U.S. payment infra, now available worldwide through a few lines of code

if dollar movement is a core need in your product and you want to explore what this can do for you, DM me

May 19

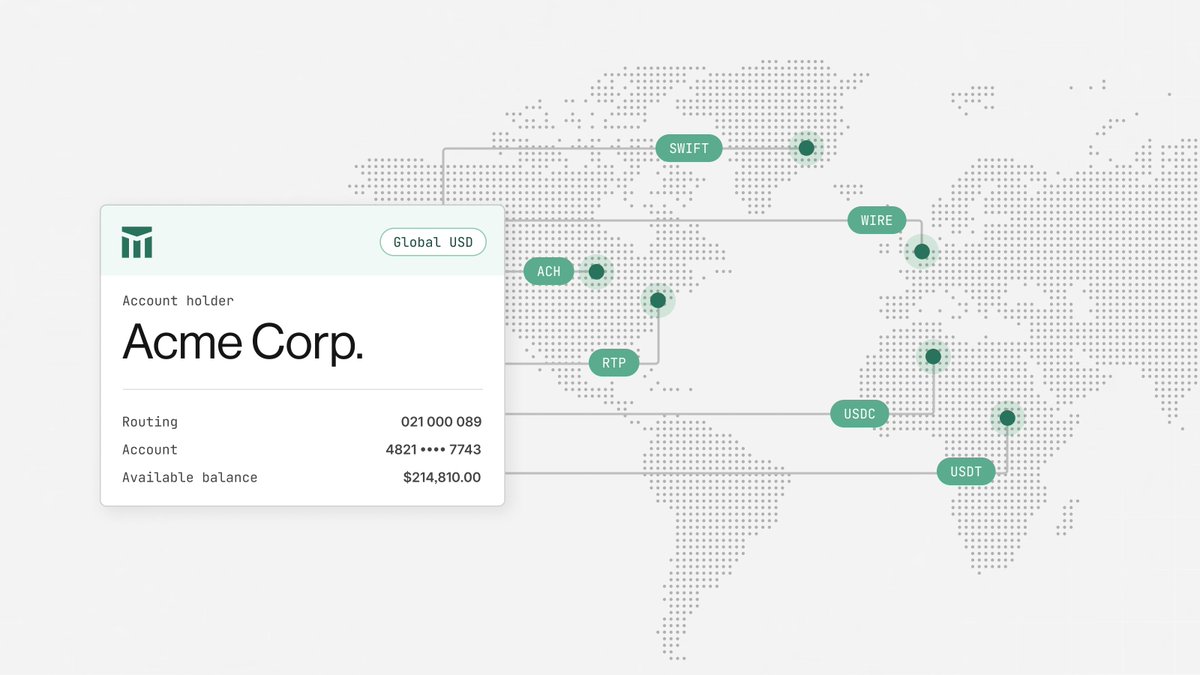

Breaking: platforms can now offer access to the U.S. financial system for users in 90 countries, with a single API call.

Introducing Global USD Accounts: named U.S. accounts with personal routing and account numbers, available to individuals and businesses worldwide.

Platforms can now offer users the ability to:

- Collect USD via ACH or wire from any U.S. payer, with native ACH pull support for on-demand or recurring funding flows

- Hold balances in USD, or convert to stablecoins and earn rewards

- Send USD via ACH, wire, RTP, or FedNow

- Reconcile fiat and stablecoin transactions against one ledger in real time

All with compliance built in, on infrastructure that's moved nearly half a trillion dollars.

Details: go.moderntreasury.com/4wKlMv…

4

2

55

9,205

daniel mottice retweeted

Jun 11

We're growing!

We're helping businesses navigate the next era of global money movement across bank rails, stablecoins, and everything in between.

Interested in joining us? Explore our open roles: go.moderntreasury.com/4v3uIL…

3

2

25

2,410

Jun 11

beautiful and deeply inspiring

Jun 10

Barcelona, you win. Sagrada Família. Just incredible.

Watch the whole thing with the sound on

2

7

437

daniel mottice retweeted

Jun 10

the backend of corporate finance is moving onchain

modern treasury now runs on @base — payments, reconciliation, compliance, all running 24/7, 365, globally

Move money, reconcile, and manage compliance all in one system

Starting today, @ModernTreasury supports USDC on Base, allowing teams to connect their financial operations with onchain payments

75

59

404

24,236

Jun 2

congrats to the symphony team on their launch!

Jun 2

We built the first app that lets you travel the world by saving money

Credit cards give you points for spending

Symphony rewards you with points for saving

Earn a fixed 5% APY, plus points transferable to the largest airlines and hotels

Let your savings take you places

3

19

7,454

Jun 1

and we are hiring across several functions!

Jun 1

100 days ago, we launched Payments, our PSP for fiat and stablecoins.

In May, we surpassed $100M in monthly payment volume.

A few things we've learned from the first $100M:

5

1

46

10,898

May 29

just sent a wire for the first time through Robinhood Banking. seamless UX, no notes

this is what mobile banking in 2026 should look like

NOW to add global accounts via embedded stablecoin wallets and orchestration 😎

4

13

1,228

May 28

uh. major major miss.

May 28

"I don't believe there was debanking. I think it's a crock of shit. An absolute crock of shit."

— @Lead_Bank CEO @jackiereses

"There's 5,000 banks in the United States. We have a lot of red states. Are you telling me that in lots of red states, including where my company is headquartered, Kansas City, Missouri—those banks were not willing to bank, for example, conservative companies?"

"What debanking actually means is that banks transitioned out of offering crypto products or risky products like adult entertainment or something like that."

"That's legit. That happened to lots of companies. But that is not systematically debanking. That's choosing not to invest in the industry."

"There might be cases where a bank decides to not include executives in a particular industry, or they choose they don't want the risk associated with something. That is their prerogative, and banks can make decisions based on their own reputational risk."

"Thankfully, you have 50 states and 5,000 banks, and there are plenty of people who would take a pro and con of each side of those judgments, and be able to offer services to many of those people who say they were excluded from the banking system."

3

60

11,459

daniel mottice retweeted

May 28

Through @ModernTreasury, we made it simple to send, receive, and reconcile stablecoin payments on Polygon.

One integration for instant money movement.

May 28

Stablecoin volume is accelerating.

@0xPolygon recently crossed $2.5 TRILLION in stablecoin transfer volume, and we're building the infrastructure to help move the next trillions.

20

32

193

13,792

May 27

heading back to Amsterdam next week for Money20/20 Europe

if you’re around and want to talk stablecoins, Global USD Accounts or payments, DM me and let’s connect

we’re also hosting a breakfast on June 4th alongside @openfx_ and @thestablecon for folks in town:

go.moderntreasury.com/4uivqn…

1

15

1,554

May 21

during Stablecon EMEA, i got firsthand exposure to how stablecoins are evolving differently across Europe and the U.S.

Europe is still meaningfully behind the U.S. in terms of market maturity, even though MiCA arrived before the GENIUS Act.

in Europe, the private sector remains significantly more risk averse and is still largely waiting for clearer guidance before deploying at scale, while the U.S. continues to be driven primarily by the private sector that hasn’t let regulatory uncertainty halt growth.

that divergence is also reflected at the sovereign level: Europe appears substantially more focused on CBDCs and preserving monetary control through public-sector infra, while the U.S. continues to lean toward privately issued dollar stablecoins on open networks.

historically, the U.S. has been far more comfortable with privately issued credit and market-based funding means. as a rough proxy, the U.S. commercial paper market alone has ~$1.5T outstanding. Europe, by comparison, has traditionally leaned toward centralized banking and ECB-led monetary coordination. that difference in institutional DNA feels similar to how each region is approaching stables.

even with that caution, it’s clear that European banks are moving more. one example was yesterday’s announcement from Qivalis that 25 more banks are joining the consortium for a Euro stablecoin initiative, bringing the consortium to 37 banks across 15 countries.

at the same time, though, talks at the conference suggested that European banks still trail their U.S. counterparts by at least a year in terms of internal conviction and operational readiness.

those convos also reinforced a broader macro reality: when 98% of stablecoin volume is USD-denominated, countries outside the U.S. naturally view that as a competitive threat & a monetary sovereignty issue.

if stablecoins become the default settlement layer for internet-native money movement, then the dominant currency on those rails inherits enormous network effects; hence, regions like Europe want local-currency stablecoins and alternative payment infra.

that said, one major hurdle to 24/7 global money movement is liquidity fragmentation across issuers, currencies, chains, banks, and regions. without interoperability and shared liquidity layers, the ecosystem risks creating isolated monetary networks rather than a unified global settlement system.

that’s why the meaningful stablecoin adoption will depend less on issuance itself and more on building institutional coordination between networks and banks who can create deep liquidity endpoints across geos and systems.

with the U.S. already ahead, it’ll be interesting to watch how players in Europe and other major markets continue responding, especially in what has become a global duopoly between USDC and USDT

side note - kudos to @NikMilanovic & the @thestablecon team for putting on a great event

4

2

17

1,110

May 20

tons of awesome feedback so far on yesterday's Global USD accounts announcement!

check out more details on what we heard from customers to get us here

new solution page here as well: moderntreasury.com/solutions…

May 20

Global money movement infra is being rebuilt.

Yesterday, we launched Global USD Accounts in 90 countries, bringing USD accounts, payments, compliance, ledgering, and stablecoin interoperability together in one API.

Read @Mottice's story behind it: go.moderntreasury.com/4wHWIV…

1

1

23

2,302

May 20

institutions, stablecoin platforms, neobanks and perps platforms…. it’s a good day for money to move onchain using MT

1

9

831

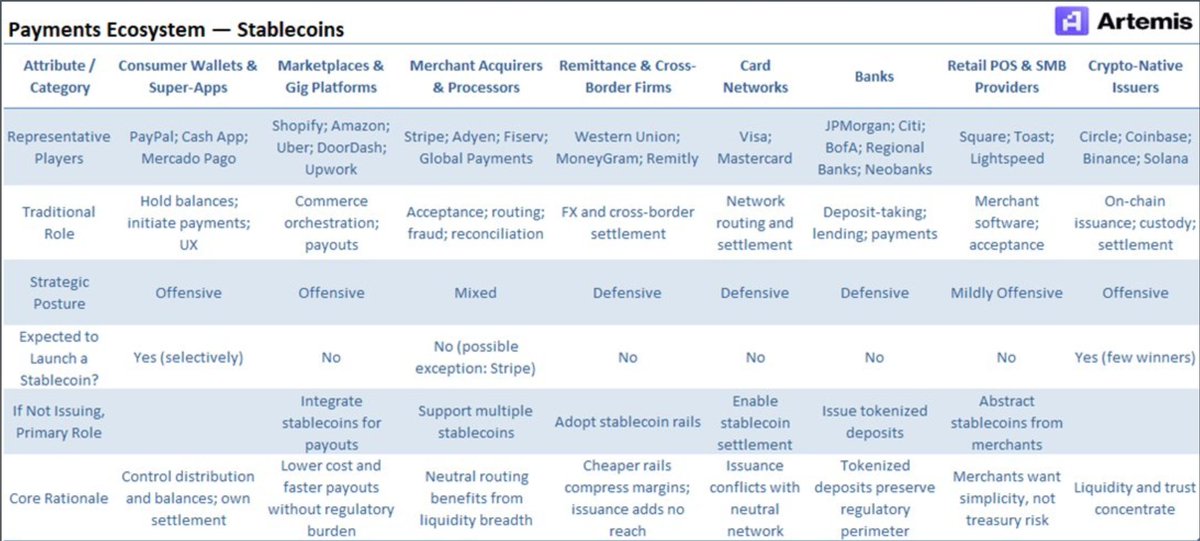

May 18

the number of vendors folks manage to ship a neobank today is… silly

much of this list is collapsible

as of today, @ModernTreasury collapses (3) (5) (7) (8) into one headless API...that numbered list is growing fast

May 16

API’s Every Neobank Needs:

1) Login/Wallet

@privy_io @dynamic_xyz @thirdweb @crossmint @turnkeyhq @magic_labs

2) Card Issuance

@raincards @Stablecoin @KulipaXYZ @wirexapp @reapglobal

3) Virtual ACH Accounts

@iron @BVNKFinance @UR_global @dakota_xyz

4) Privacy Layer

@SeismicSys @UmbraPrivacy

5) Yield

@yield @yield_xyz @blend_money @veda_labs

6) Swaps

@moonpay @lifiprotocol @0xProject @squidrouter @AcrossProtocol @wormhole @RelayProtocol

7) KYC/AML

@sumsub @persona @chainalysis

8) Stablecoin orchestration

@Paxos @openfx_ @CodexFX @m0 @ethena @OndoFinance

am i missing any?

10

3

82

20,874

daniel mottice retweeted

May 15

Heading to Stablecon EMEA next week?

Hear from Dan Mottice, our Head of Stablecoins, alongside leaders from Citi, Deutsche Bank, M0, NALA, and OpenFX in a discussion moderated by Chuk Okpalugo on the realities of always-on global payments.

5

14

1,005

May 14

take a look at what we’ve been up to at MT

May 14

1/ Prior to this year, we supported customers who already had established bank relationships.

This Spring, we took a big step to make it easier for teams to launch and scale payment products without stitching together a processor, a bank, a ledger, and the reconciliation layer in between with the launch of our integrated payment service provider (PSP).

10

2,269

daniel mottice retweeted

May 13

GENIUS led to a sea change in usage, perception, and acceptance of stablecoins. Don't understimate the effect of passing CLARITY on all things payments and markets.

13

6

44

24,701

May 12

USDT is the godfather of stablecoins. MT now supports it natively

reach out if you're interested in adding USDT payment capabilities for your customers

May 12

We now support USDT!

Combine USD <> USDT orchestration with built-in compliance controls, every major U.S. payment rail, and named U.S. accounts across 90 countries.

All through a single API. Powered by the same infra that's moved $400B .

Learn more: go.moderntreasury.com/4tzv8Y…

2

2

22

3,184

May 11

infrastructure bloat happens when you build around a problem instead of through it.

in US stablecoin orchestration, ACH pull has been that problem for years.

ACH pull is the funding mechanism that underpins most consumer and business fintech products in the US. when Robinhood lets you buy stock the moment you link a bank account, that's ACH pull with instant purchasing power. when Brex sweeps your operating account, that's ACH pull. under the hood, they their payment partners have built out a credit risk model that gives you access to the funds instantly even though ACH pull has a multi-day settlement lag.

the reason those products feel seamless is because the user never has to think about where the money is coming from. money just moves.

when a platform initiates the debit, it signals to the user that the product is in control of the flow.

when you ask a user to push funds themselves, you've handed them a step they can abandon. pull-based funding flows create a smoother UX.

so why don't most stablecoin orchestration platforms offer this? ACH debit origination requires a bank sponsor willing to take on return risk on your behalf. NSF and account closed returns typically resolve within a few business days, but unauthorized return claims can come back up to 60 days after settlement, long after stablecoins have already moved.

that's a recon headache & financial risk that compounds fast when handled incorrectly, so most PSPs decided to ship something simpler.

as a result, fixing this with a workaround is painful. you're typically integrating Plaid or MX for bank linking, a separate ACH originator for the debit, a conversion layer for USD <> stables, and an AML wrapper around all of it.

four vendors/contracts/failure points, all converging on the critical moment a new user tries to put money in for the first time.

it's bloat that traditional fintech solved years ago, but the stablecoin layer added enough complexity that most platforms retreated to ACH credits and called it good enough.

we didn't think that was good enough. that first funding moment is where users decide whether your product works. it's too important to route around.

so we faced it head on at Modern Treasury. we built one API for the full funding lifecycle: bank connection, ACH debit origination, stablecoin orchestration, compliance.

with the full funding lifecycle natively supported via one integration, users get a Venmo-like funding experience and platforms get better conversions eng time back to ship features that move the needle.

routing around hard problems is how you get to v1 but solving them is how you get to what stablecoins are actually capable of.

@ModernTreasury is committed to the latter and ACH pull is just one example of many more to come

12

3

59

4,733