Joined March 2009

- Tweets 6,096

- Following 368

- Followers 274

- Likes 9,576

126 Photos and videos

Jun 12

Why did it take 9 thefts for them to stop him, why wasn’t one enough?

Jun 12

Reece Fujioka stole nine high-value bikes from rail stations in Surrey.

We secured valuable CCTV evidence to secure justice 🎥

He’s now been jailed for two years.

More 👉 orlo.uk/gxeYT

1

94

Jun 11

RT @Perky_43: Royal Mail driver couldn't be bothered to avoid nesting ducks on Fishpond Lane, Holbeach, Spalding - they decided to run them…

1,091

Ben retweeted

This is amateur hour thermal analysis. If this proposal landed on my desk I would throw it in the trash can.

It took me 5 minutes to find a smoking gun with this design. With 110 m^2 and assuming only their average load (not the peak), and generously assuming perfect black body radiation, the outer surface of the radiator facing space would be at about 100 C. Uh oh. Dead right there.

Chip reliability goes down significantly when the junction temperature (the hottest temperature in the chip) exceeds 80 C. Every 10 degrees you go above this exponentially reduces chip life. This mostly occurs due to thermomechanical fatigue, where cycling stresses erode connections, cause further hot spots, and failure accelerates catastrophically.

Data centers on land are already having issues keeping $NVDA chips cooler than 80 C, and keeping the HBM next to the GPU under 90 C. $META published a notorious report about failure rates training Llama 3, where half of the chips failures were due to physical operational failure, and the failure rate was roughly 9% of chips PER YEAR.

This high failure rate is almost certainly due to thermal cycling.

Notice that the $SPCX engineer mentions that most of the solar tech is already used on the Starlink satellite, implying this design isn't even really that radical. But they are about to learn the hard way the insidious scaling of surface area to volume ratio.

Having worked on a number of high power cooling applications, scaling a system up almost inevitably makes it harder to cool because the volume grows so much faster than the surface area. Motor designers I know joke that if you make a motor big enough, eventually you just start making really good heaters. This happens because heat is generated in larger volumes with no commensurate increase in surface area to pull that heat out, so everything tends to get hotter internally.

As the power consumption in the volume of the satellite grows, the surface area required to support it grows comically large.

So lets come up with a reasonable estimate for the temperature of the GPU junctions based on their design. Keep in mind, even if the fluid convection had no resistance, and even if there was no conduction resistance through manifolding from the chip to the fluid, and even if there were no contact resistances anywhere in the system, and even if the chips were perfect conductors, the junctions would still be too hot at 100 C.

In reality they will be higher. A great back of the envelope estimate for thermal resistance between a chip package and the fluid in a cold plate heat exchanger is about 0.01 K/W. This is considered pretty good state of the art. Even if I give them the benefit of the doubt and make aggressive assumptions, I would be remiss to say they are getting better than 0.005 K/W with a cold plate. To get better they are going to have to rework the packaging at the chip level.

In this very rosy picture, they are looking at a temperature rise just to the inside of the packaging of around 7 C. Then you have the temperature variation inside the packaging which would make this worse (but we will ignore it).

So even in the rosiest picture I can paint for them, they are getting chip temperatures of 107 C. Again, dead on arrival.

In reality, the chips will get much hotter. Without doing the analysis, it's not unreasonable to think that these chips won't be able to operate at average power under about 150 C.

To get the radiator to emit at an average temperature of 100 C, the fluid actually has to get much hotter. As the fluid moves through the radiator, it will cool down, reducing the total heat dissipated by the radiator. You can get around this somewhat by massively overpowering your pumps so they are pumping an enormous amount of fluid, but the weight required will not be kind on the payload. For example, if you want a 1 degree temperature drop across the radiator, you will need around a 10-20 GPM pump, which generally is around 10-20 HP (7.5-15 kW) and weighs 200-300 lbs each! If they want redundancy, just the pumps will be 15% of the weight of the payload at 70 kW/metric ton!

If we reduce the pumps by 10x, expect a drop in fluid temperature around 10 C. So now the chip is nearly 120 C. Add in imperfect emissivity and contact resistances, and your junction temperatures will easily exceed 150 C in the chip and the chips will fail.

But again, these are all details. Even in a completely perfect system, the chips run at 100 C and will fail.

Now to be clear, do I think that with enough time and money you could get a GB300 rack to run in space? Sure. But this looks a a quagmire of a decade project that will either drastically under-deliver or just get canned because it's extremely impractical and is not competitive with land based systems.

Literally the only positive for putting these in space is the lack of regulations to put them there.

Watch @ElonMusk provide a technical update on SpaceX’s capability to manufacture, launch, and operate AI satellites at scale → spacexipo.com

86

49

287

70,813

Ben retweeted

I want to give a special shout out to @SGFansUnited for the work they have been doing since the cancellation of Stargate was announced.

They have been tirelessly rallying the fan base, pointing out ways to contacting Amazon, retweeting the petitions and boosting #SaveStargate

Make sure to give them a follow.

Everyone be sure to go follow @venturepictures @EverySG1Frame @StargateZone @StargateNow_EU @Jack2LOneill @CptCarterSG1 @GateWorld @dial_the_gate @JennyStiven

They're important members of the community to follow as we gear up to #SaveStargate! @AmazonMGMStudio

18

144

1,186

20,358

Ben retweeted

These are the top 3 atm. Sign them all!

change.org/savethegate

change.org/p/save-the-new-st…

change.org/p/save-stargate-o…

18

232

633

39,650

Ben retweeted

Trillionaire*

*Fake, no way to get it. I'm gonna have a lot to say about the SPCX IPO soon, but suffice to say, you're a damn fool if you become my exit liquidity on it.

Elmo would collapse the value of everything he has if he tried to sell even a little of his holding in it, and the entire company's valuation is based on positively nothing but a desire to create an artificial personal wealth figure.

7

8

69

5,486

Ben retweeted

Jun 3

Tesla has retroactively modified FSD purchase agreements to add "supervised" language that did not exist when owners originally bought the product.

Electrek has confirmed with multiple owners.

In some cases, the original contracts have been made entirely inaccessible from owners' Tesla accounts.

18

39

159

10,431

Ben retweeted

Jun 3

SPACEX IS COMPLETE GARBAGE

Run, don't walk from this train wreck.

The numbers are right there in the S-1 filing for anyone willing to look.

SHAME ON YOU ELON MUSK

YOU BELONG IN JAIL

SHAME ON YOU @SECGov and @SECPaulSAtkins for allowing this to proceed.

SHAME ON YOU MORGAN STANLEY and TED PICK

SHAME ON YOU GOLDMAN SACHS and DAVID SOLOMON

SHAME ON YOU Bank of America, Deutsche Bank, UBS, Citigroup, JPMorgan, Mizuho, RBC, Macquarie, Wells Fargo, Allen & Co, Needham, Raymond James, Stifel, Cantor Fitzgerald, Soc Gen, Mirae, Santander, ING, and BTG Pactual.

Have you no shame? Have you no decency? Have you no honor?

Or is it all about the fees?

And the index providers are making it even WORSE.

Nasdaq changed its rules so SpaceX auto-qualifies for the Nasdaq-100 after just 15 days of trading triggering up to $60 BILLION in forced buying from ETFs alone. S&P Dow Jones Indices is now consulting on whether to fast-track S&P 500 inclusion for unprofitable mega-cap IPOs of this scale.

To Adena Friedman at Nasdaq and Catherine Clay at S&P Dow Jones Indices:

You are about to force every retirement account in America to become EXIT LIQUIDITY for the most overpriced IPO in history.

This is a legally sanctioned wealth transfer from Main Street to Wall Street. The public will be badly injured and EVERY ONE of you knows it.

You all belong in jail for this.

David Solomon and Ted Pick, grow a pair and do the right thing and stop this epic travesty.

How are you able to sleep

at night?

You and your firms are PATHETIC.

314

696

2,086

78,601

Ben retweeted

It's hard to believe how many people are investing in absolute shit these days without the first clue about things like the fundamentals of a company. Or what makes an asset an asset, and how that asset is supposed to create additional value for the investor.

A lot of people got lucky over COVID investing in bubbles. Then they confused this luck with investing acumen - basically getting high from sniffing their own farts.

Some of the COVID bubble popped already. Peloton is great example. Zoom would be another. A year into COVID, Peloton was trading at $160. Today? $6. Zoom was around $500, and it's done 80% currently. Docusign, similar story. $310 at the height, and down to $52 today.

The point is, eventually every stock price will revert to a value based on what it actually is. Not what it's promised to be in five or ten years - especially when the past five or ten years have been hollow promises.

There's one more giant COVID bubble stock left to pop. The biggest one in the market today. Tesla.

The difference between fundamentals and market cap of Tesla is mindboggling. $1.5 trillion market cap for a company that sells as many cars as Subaru annually, that has lost three models in the past year. A middling, struggling automaker that, being generous MIGHT be worth $50B when judged against what are called comparables for professionals who adjudicate business values in advance of a sale. What are the other companies doing, what do they own for assets and IP, then how does this company compare to assign an appropriate sale price. Judged accordingly, Tesla shares should be sitting at about $15 - as they were in October of 2019.

NOBODY in their right mind would pay $1.5 trillion to acquire Tesla outright. Yet that's what people buying shares in Tesla today are paying for the fraction of the company they purchase.

The market cap cannot be justified using company activities. It's unsupported by sales that are in decline, margins that are in decline, and the promises of taking over in the international taxi industry carry no true weight. They are fantasy, and worth absolutely nothing in the long run.

So, whether Tesla retail investors like it or not, they should expect a drastic cut in stock price in the next year or so, as the product pipeline completely dries up in favour of a useless short range coupe that remains illegal to sell to consumers, and their AI ambitions for the cars and the tele-operated mannequins fall flatter than the Cybertruck fiasco.

Tesla is a bubble. If you made money in it, you weren't clever. You got lucky. Luck runs out. And, the clever money has already left you holding their bags.

15

16

100

5,139

Ben retweeted

Jun 2

PETL has acquired the Kleandrive bus re-powering operation as a going concern through administration.

The acquisition preserves a specialist British engineering capability in heavy vehicle decarbonisation. Live customer programmes continue without interruption.

Kleandrive's technology converts existing diesel buses to fully electric powertrains, allowing fleet operators to decarbonise without the capital cost or embedded carbon of buying new vehicles. For many regional operators and local transport authorities working under tight budgets, it is the most commercially viable route to zero emission running.

The acquisition extends the PETL group's clean propulsion portfolio. PETL is one of the UK's leading developers of battery and battery management system technology, including through our wholly owned subsidiary Brill Power, a University of Oxford spin-out. Adding repowering capability gives us a direct route to deploy that technology at scale in one of the highest impact segments of UK transport decarbonisation.

Dr Andy Palmer CMG, Co-Founder and CEO of PETL, said:

"Britain keeps losing its industrial base one company at a time. Repowering existing diesel buses is one of the most cost-effective ways for operators to decarbonise their fleets. It deserves to be built here, by British engineers, and we intend to make sure it is."

More information about the acquisition can be found here:

palmerenergytechnology.com/p…

1

9

33

1,505

May 26

Hey @Tesco I am sick and bloody tired of your delivery drivers blocking my driveway to deliver to the neighbours. It’s sheer laziness, to save less than the length of the truck. Next time they will get blocked in themselves and good luck getting home that day.

295

29

746

359,859

Ben retweeted

May 24

A message for my $TSLA friends eyeing the SpaceX IPO $SPCX.

I traded $TSLA for years. I know the community. I know the excitement when Elon takes something public. But before you chase @SpaceX at $1.75 trillion, read the S-1 carefully.

SpaceX doesn't need your money.

They raised at $800B in private tenders six months ago. They could raise $50B privately tomorrow with a phone call. This IPO isn't about raising capital. It's about giving insiders liquidity.

95% of @SpaceX shares are held by insiders. Only 5% will be publicly traded. Insiders hold $1.66 trillion in paper wealth they currently can't sell. The IPO changes that.

And they've structured it so insiders can sell BEFORE the standard 180-day lock-up expires. @SpaceX built in early release provisions -- after the first earnings report, insiders can sell up to 20% of their shares.

They're also reserving 30% of IPO shares for retail. Ask yourself -- when has Wall Street ever given retail the best seats in the house unless retail was the product?

100x revenue.

$4.9B net loss.

xAI burning $6.4B a year while @Starlink subsidizes it.

This isn't 2020 Tesla at 20x revenue with a clear path to profitability. This is a different risk profile.

Now here's the part I want you to actually consider.

SpaceX's S-1 sizes their satellite-to-phone business (Starlink Mobile) at a $740 billion TAM. Their Connectivity segment does $11.4B at 63% EBITDA margins. Those numbers are real and impressive.

But buried in the S-1, @SpaceX names their D2D competitor: $ASTS .

@AST_SpaceMobile $40 billion market cap.

Not $1.75 trillion. $40 billion.

Here's what $40B buys you:

98.9 Mbps proven from space to unmodified phones (SpaceX does 3-5 Mbps)

The only low-band D2D spectrum access on Earth (indoor coverage SpaceX can't match)

All three US carriers forming a joint venture around ASTS technology

Google invested $358M

their largest public equity holding

AT&T, Verizon, Vodafone as equity investors

$3.5B cash, $1.2B contracted backlog

3,900 patents, custom ASIC in production

Three satellites launching on a Falcon 9 next month

60 carrier partners covering 3 billion subscribers

@SpaceX at $1.75T is pricing perfection across rockets, satellites, AI, and Mars. One miss and it corrects hard.

$ASTS at $40B is pricing uncertainty in a $740B market where the technology is already proven and the carriers have already chosen sides.

The Tesla community knows what it feels like to find a mispriced stock before the world catches on. $TSLA at $30 pre-split wasn't obvious to anyone except the people who did the work.

$ASTS at $106 in a $740B market with 33x faster speeds than SpaceX D2D, a carrier JV, and institutional discovery just beginning -- that's the same kind of setup.

So before you throw money at a $1.75T IPO where insiders are building exit ramps, maybe look at the $40B competitor they named in their own filing.

Not financial advice. Just math.

$ASTS 🛰️

cc @SawyerMerritt @unusual_whales @DanBTC916

167

287

2,273

539,765

Ben retweeted

May 23

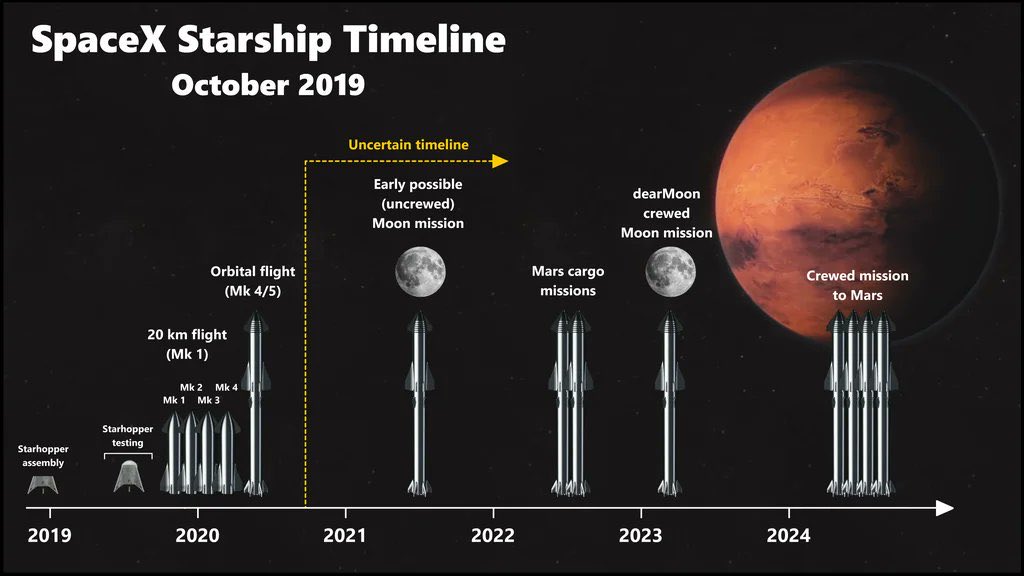

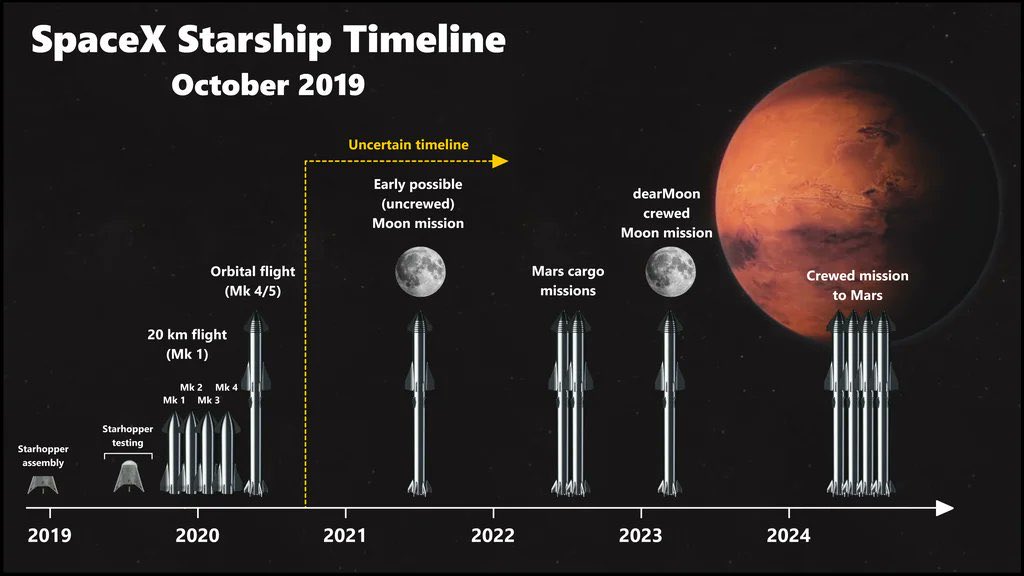

Starship exploded. Again. Like it always explodes. It explodes because it's a dead-end design. SpaceX will never reach the moon. SpaceX will never reach Mars. SpaceX sets the US space program back every day we foolishly decide to rely on it.

THE STARSHIP PROGRAM

EXCITEMENT GUARANTEED

1,173

2,935

40,293

2,620,226

Ben retweeted

Farmers have figured out that the cheapest pesticide is a strip of flowers.

When you plant wildflowers through a crop field, not just around the edge but in strips running through the middle, you get ladybugs, lacewings, hoverflies, and parasitic wasps living in the field instead of visiting it.

They eat the aphids, the caterpillars, and the mites for free, all summer long.

In controlled trials, fields with tailored flower strips had leaf-beetle numbers 40 to 50% lower and crop damage cut by around 60%, enough to drop below the threshold where spraying was even considered worth it.

The flowers attract a standing army to our fields.

We spent decades engineering chemicals to kill the insects eating the crop, when the insects that eat those insects would have worked for the price of seed.

761

18,961

63,635

3,074,443

Ben retweeted

May 19

Elon literally said the Cybertruck could 'serve briefly as a boat'. So either @Tesla owes this man a new cybertruck or @elonmusk needs to correct his fraudulent claim.

May 19

Cybertruck driver decides to drive his Truck into a local lake here in Texas. It ended exactly how you thought it would. 🤣

328

647

10,954

545,219

Ben retweeted

May 11

What we crave is an old-school government so boring no-one knows their names. Competent, professional.

But we're led by a story-hungry media desperate for new drama for sponsored podcasts.

If they had their way we'd have a new PM every month, each worse than the last.

137

642

3,828

79,686

Ben retweeted

May 8

It's wild that the world's richest man, the CEO of Tesla, has over the last few years:

— been caught emailing Epstein asking to attend his "wildest parties" on his island

— lied about the relationship, claiming he "always refused invites" when emails show he asked to go on at least 3 occasions — after Epstein was already convicted

— facilitated the production and distribution of AI images sexualizing unconsenting adults and minors (part of why France wants to criminally charge him)

— openly echoed white nationalist rhetoric, saying "white people need to reclaim their nations"

— dismantled several government orgs, including those that regulate his many businesses, and some that were directly responsible for saving lives

And yet somehow, people continue to support him and invest in his businesses.

Greed and low morals.

May 8

Elon is calling French prosecutors "f*gots".

No seriously. Elon loves to take credit for the great things his companies achieve, but he loses his mind the second someone tries to hold him responsible for the bad things his companies do.

He is losing his mind here. He says that french prosecutors are "faker than a chocolate euro" - presumably talking about the currency. And he is making a comeback with his "pedo" name-calling because it went so well last time.

In French, "pédé" translates directly to calling someone a "pedo" or "pedophile", but in practice, it is used more as a homophobic slur equivalent to "f*got."

Then he says, "Go away or I'll insult you a second time."

No joke, he is losing his mind.

44

165

920

41,488

Ben retweeted

May 3

Tesla is the most successful CON in the history of capital markets.

Not because the cars are bad.

But because the entire business is engineered to impress on first glance and collapse under scrutiny. And the culture around it has made facts completely IRRELEVANT.

I've never seen a company where the gap between what is promised and what is delivered is this wide, for this long, with this little accountability.

Tesla's Full Self-Driving system is marketed as autonomy. But it is not autonomy. It is a camera-only system running probabilistic inference.

The car is making statistical guesses about what it sees, thousands of times per second, with no redundancy when those guesses are wrong.

Probabilistic inference controlling a two-ton vehicle at highway speed with your family inside.

NHTSA has two open investigations covering 3.2 million Tesla vehicles. One was escalated to a formal Engineering Analysis in March after 9 crashes, including a fatality, where the system FAILED to detect sun glare, fog, and dust. The cameras went blind and the car kept driving.

In Austin, Tesla's robotaxi fleet has reported 15 crashes across roughly 800,000 miles. One crash every 57,000 miles.

The average American driver has a police-reported crash every 500,000 miles. Tesla's robotaxis crash at roughly 4x the human rate, WITH a safety monitor sitting in the car whose only job is to prevent crashes.

Waymo operates over 2,500 fully driverless vehicles across multiple cities with no human backup and maintains a crash rate 85% below human drivers across 127 million autonomous miles. Tesla has ONE unsupervised vehicle in a tiny section of Austin.

But here's what really makes Tesla different from every overvalued company I've ever analyzed:

The facts do not matter to the people who own this stock.

Every missed deadline, every broken promise gets filtered through the same response: attack the messenger.

Call them a short seller. Call them a hater. Anything to avoid looking at the actual numbers.

It's an online ecosystem that has made itself completely immune to facts. And Musk baked that dynamic into the culture from the beginning.

Every time the fundamentals deteriorate, the faithful don't sell. They double down.

When your shareholder base treats every dip as a buying opportunity regardless of the data, the stock becomes untethered from reality entirely.

That's literally a religion with a ticker symbol.

I highly suggest you read Edward Niedermeyer's book Ludicrous on this.

And now it even gets WORSE...

CapeFearAdvisors published a piece this week that should be required reading.

Tesla's 2025 CEO Performance Award contains a change-of-control provision:

In the event of a change of control, ALL operational milestones are disregarded.

No million robotaxis, Optimus robots, or $400 billion EBITDA.

NONE of it.

So if SpaceX acquires Tesla at $8.5 trillion, every tranche of Musk's 423 million share award vests immediately. A single acquisition at that price triggers the full vesting of both plans at once, with no way to claw them back.

The milestones everyone argues about are just a distraction. The mechanism is the change-of-control language buried in the SEC filing.

This is about engineering the largest personal wealth transfer in modern financial history and using the narrative machine to keep the price elevated long enough to execute it.

I've seen every bust of the last four decades.

But this one is different because the cult of personality is stronger than anything I've witnessed. The movement around this stock cannot be touched by facts, and that is what makes it so dangerous.

But the math always wins. ALWAYS.

It just takes longer when the con is this good.

269

558

1,987

171,184

Ben retweeted

Apr 23

Last night was the biggest disaster in the history of Tesla.

Let me walk you through what actually happened on that earnings call, because the headlines are doing you a disservice:

Elon Musk got on the call and admitted (his words) that Hardware 3 "simply does not have the capability to achieve unsupervised FSD."

He said he wished it were otherwise. He said the memory bandwidth is one-eighth of what Hardware 4 has. And that's the end of the conversation.

Approximately 4 million Tesla vehicles on the road right now have Hardware 3. Many of those owners paid $8,000 to $15,000 for Full Self-Driving capability based on Musk's repeated promises (going back to 2016) that the hardware was sufficient for full autonomy. As recently as 2022, Musk was publicly assuring owners that HW3 had the processing power to get it done.

BUT IT DIDN'T

Those promises are now officially broken.

The solution is a "discounted trade-in" toward a new car with Hardware 4.

Not a refund or a free upgrade...

A discount on buying ANOTHER Tesla.

Investor Ross Gerber said it too - all HW3 owners got screwed, and with roughly 285,000 FSD purchasers affected, the potential liability runs into the BILLIONS.

But that's not even the worst part.

Musk was asked if the current FSD v14.3 was ready for unsupervised deployment. He said yes. Then immediately walked it back and admitted Tesla has "major architectural improvements" in the pipeline that would significantly improve safety.

What he really means: the software isn't SAFE ENOUGH to deploy without a human watching. Full unsupervised FSD for consumer cars is pushed to Q4 2026. At the earliest... Maybe.

How many times has this deadline been pushed? I've lost count. And trust me, I've seen a lot of broken promises. But this one takes the cake.

Now let's talk about the numbers everyone is celebrating:

Tesla reported $22.4 billion in revenue and $0.41 in non-GAAP earnings. A "double beat." The stock popped 4% after hours. Victory, right?

WRONG

Dig into the actual filing:

The number one driver of operating income improvement wasn't cost reductions, wasn't volume growth, wasn't FSD revenue. It was - and Tesla listed this FIRST in their own shareholder letter - "one-time benefits related to warranty and tariffs."

They released warranty reserves. They booked tariff refund windfalls. They stretched supplier payments by 10 days. They took on billions in new debt. Then they presented everything through non-GAAP metrics that strip out over $1 billion in stock-based compensation.

GAAP net income was $477 million on $22.4 billion in revenue. That's a 2.1% net margin. On a $1.4 trillion market cap.

Let me put that in perspective:

3.75 billion shares outstanding. Annualize the Q1 GAAP profit and you get roughly $1.9 billion. That's a trailing P/E ratio north of 700. Use the adjusted number - strip out stock comp, which is a REAL cost to shareholders through dilution - and you're still at around 250x earnings.

All of this is extremely bad, but I didn't even talk about the CAPEX BOMB yet...

3 months ago, Tesla guided to "over $20 billion" in 2026 capital expenditure. Last night they raised it to over $25 billion. A $5 billion increase in a single quarter. That's 3x their historical annual capex run rate - $8.5 billion in 2025, $11.3 billion in 2024. The CFO confirmed on the call that Tesla expects NEGATIVE free cash flow for the rest of the year.

So you have a company generating roughly $6 billion in annual free cash flow on a good year, and they're about to spend $25 billion.

The math doesn't work.

They will almost certainly need to issue equity. Which means dilution. Which means the $1.9 billion in annual earnings gets spread across even MORE shares.

The core auto business is literally deteriorating in real time:

Tesla delivered 358,000 vehicles in Q1 (missed estimates again).

They produced 408,000. That's 50,000 cars sitting on lots that nobody bought.

Inventory days jumped from 10 to 27 in just a few quarters. California (their most important US market) saw registrations crash 24% year over year.

Their market share in the state fell from 9.2% to 7.7%. That's on top of a Q1 2025 that was ALREADY weak from Model Y retooling. They're declining off a decline.

And here's what really kills the bull case...

The entire valuation rests on robotaxis, Optimus robots, and autonomy. So let's put numbers on it:

Waymo - the actual leader in autonomous driving with 15 million completed rides in 2025 alone, over 127 million autonomous miles driven, operating commercially across 6 US cities with plans to expand to 20 more - just raised $16 billion at a $126 billion valuation.

That's the market's verdict on what the LEADING robotaxi company is worth. $126 billion.

And Waymo is YEARS ahead of Tesla in actual deployment.

Tesla has 3.75 billion shares outstanding. So even if you assign $126 billion in robotaxi value (giving Tesla full credit for matching Waymo despite being nowhere close) that's $33 a share. Add the auto business at generous auto-industry multiples, maybe $20 a share. Throw in energy storage and services, $10-15.

Sum of the parts gets you to roughly $65-70 a share if you're feeling generous. Maybe $50 if you're not.

The stock is $387.

So what exactly are you paying for?

You're paying for a STORY. You're paying for PROMISES that keep getting pushed back, technology that keeps falling short, and a business plan that requires spending $25 billion a year while the core product sells fewer units at declining margins in a market where California sales just fell 24% and the federal EV tax credit is gone.

I managed the number one mutual fund in America. I founded two billion-dollar hedge funds. I've been doing this since 1981.

And I am telling you:

Tesla at $387 is one of the most egregious mispricings I have seen in my entire career.

THE CRASH WILL BE EPIC

1,184

2,556

10,387

1,219,957

Ben retweeted

Apr 22

Tesla basically cooked the books to show one last quarter of positive cash flow before going negative.

Between the tariff refunds, warranty accounting changes, pushing supplier payments by 10 extra days (up 30% in 6 months), Tesla would have almost certainly lost money in Q1 also.

Meanwhile, Elon admits he was wrong to think robotaxi/FSD would start to meaningfully contribute financially in 2026, pushes it "maybe" next year.

He readmits that HW3 will never support unsupervised - comes up with a new stalling tactics about retrofit mini factories that will never happen.

Man, this was a mess of earnigs. I understand that $TSLA retail investors buy this stuff, but the fact that so-called "smart money" on Wall Street is still buying into that shit baffles me.

Apr 22

Tesla $TSLA earnings might look good on the surface, but they are in complete shambles if you dig even a little:

- Tesla Listed "one-time warranty and tariff benefits" as the #1 driver of profitability — refused to disclose the dollar amount

- Seemingly Booked IEEPA tariff refunds as income in both auto AND energy segments after the Supreme Court ruling — a one-quarter windfall

- Stretched supplier payments from 61 to 71 days — up from 52 days two quarters ago — adding $1.3B to payables to juice cash flow

- Issued $4.3B in new debt (3x last quarter) to keep the cash position flat after a $2B SpaceX investment

Meanwhile: deliveries missed, inventory piling up to 27 days of supply, energy storage down 15%, and GAAP net margin was just 2.1%

62

213

1,570

125,557