Joined August 2025

- Tweets 1,671

- Following 4

- Followers 1,166

- Likes 1,232

378 Photos and videos

Pinned Tweet

May 15

🏛️ The Managed Fund Approach to Generating Bitcoin Yield

A conversation with the fund managers of @syphercapital

In this episode, we sit down with Steve Han and Michael Song of Sypher Capital to discuss how serious Bitcoin fund managers are approaching BTC-denominated yield for their LPs.

Topics Discussed:

0:00 - Managed BTC yield vs direct protocol deployment

4:15 - Changes in the Space the Last Year

6:35 - Sypher Capital Origin Story

9:30 - Assessing On-Chain vs Off-Chain Opportunities 13:50 - Performing Due Dilligence

20:42 - Lessons Operating Fund Last 1.5 years

22:50 - Creating the Perfect Yield Product

25:25 - Updating the BitcoinYield 5-Point Safety Framework

29:32 - What Innovations Are Exciting

32:00 -Tokenization

40:30 - Tax Implications

Watch the 45-minute conversation below 👇

5

2

16

2,804

Jun 12

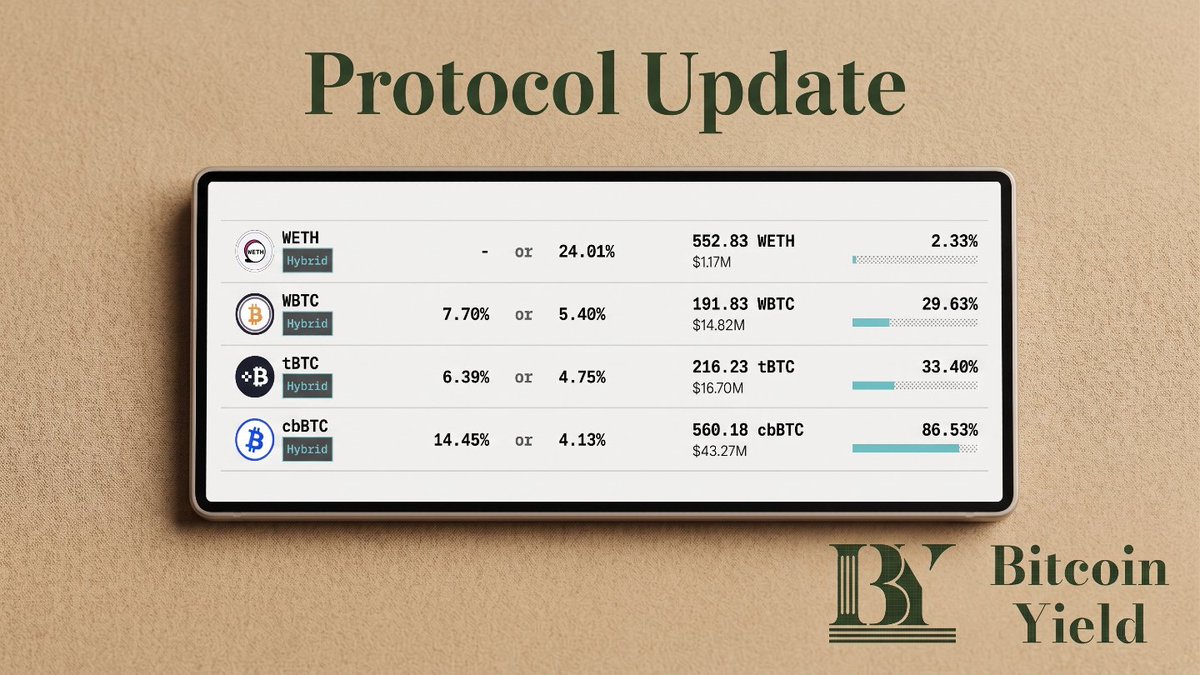

Bitcoin YIeld USD TVL fell across nearly every protocol in the last 30 days.

A lot of that is BTC repricing from ~$80K to ~$64K.

BTC-denominated TVL separates capital from price. The 30-day movers:

In:

Mezo Earn: 414 → 663 BTC ( 60%)

Hermetica hBTC: 51 → 62 BTC ( 21%)

Out:

Botanix: 23 → 5 BTC (-79%)

Lombard Finance: 12,940 → 11,803 BTC (-9%)

YieldBasis (all six vaults): ~1,697 → ~1,137 BTC (-33%)

Flat / Mixed:

Babylon: 50,914 → 51,418 BTC ( 1%)

Lightning tracked capacity: 5,057 → 5,701 BTC ( 13%)

1

172

Jun 12

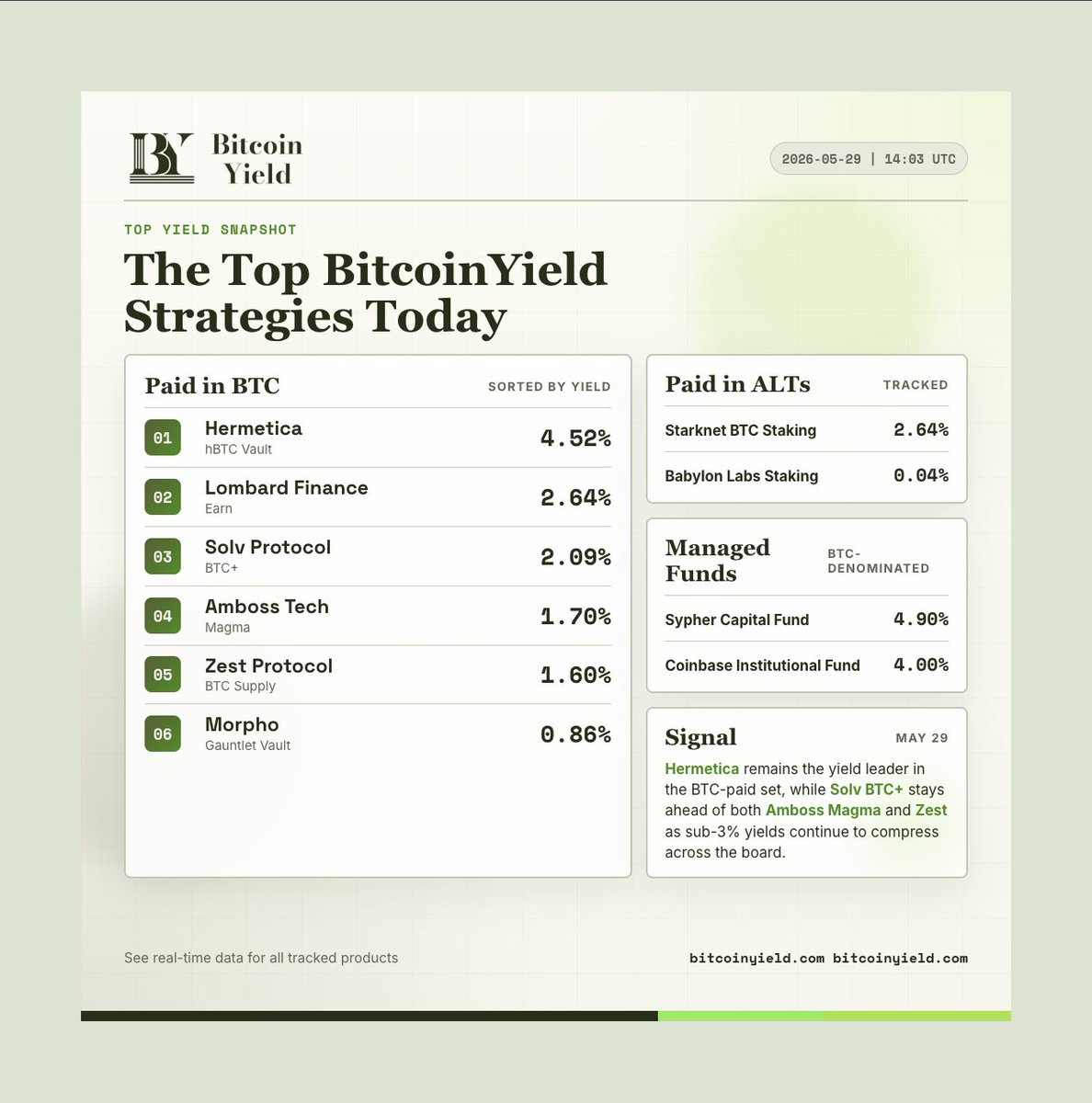

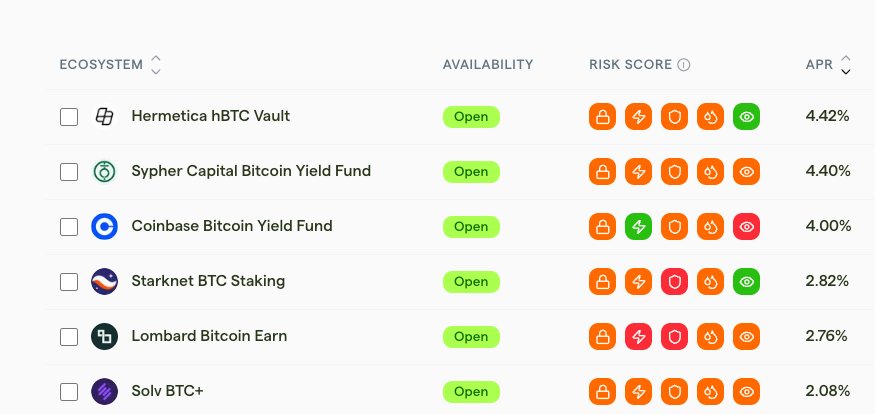

The Top BitcoinYield Strategies Today 📈

🔸Paid in BTC:

@SolvProtocol BTC : 3.08%

@Lombard_Finance Earn: 2.37%

@HermeticaFi hBTC Vault: 1.79%

@AmbossTech Magma: 1.70%

@ZestProtocol: 1.61%

🎪 Paid in ALTs:

@Starknet BTC Staking: 2.82%

@babylonlabs_io Staking: 0.04%

🏦 BTC-Denominated Managed Funds:

@syphercapital Fund: 4.90%

@CoinbaseInsto Fund: 4.00%

See real-time data for all tracked products at bitcoinyield.com bitcoinyield.com

1

112

Jun 10

The Top BitcoinYield Strategies Today 📈

🔸Paid in BTC:

@SolvProtocol BTC : 3.06%

@Lombard_Finance Earn: 2.49%

@HermeticaFi hBTC Vault: 2.06%

@ZestProtocol: 1.61%

@AmbossTech Magma: 1.35%

🎪 Paid in ALTs:

@Starknet BTC Staking: 3.03%

@babylonlabs_io Staking: 0.05%

🏦 BTC-Denominated Managed Funds:

@syphercapital Fund: 4.90%

@CoinbaseInsto Fund: 4.00%

See real-time data for all tracked products at bitcoinyield.com bitcoinyield.com

1

12

491

Jun 9

YIELD UPDATE: Botanix stBTC yield-bearing vault has fallen below our $1m TVL requirement.

We will be removing the product from our public facing database shortly.

2

11

1,099

Jun 9

Update: Botanix announced they will be sunsetting the network next month.

Jun 9

It is with a heavy heart that we announce we are winding down the Botanix network.

This decision is the hardest one we have made in four years, and we want to share the reasoning openly because the people who backed us, built with us, and used what we shipped deserve more than a quiet shutdown notice.

First off, an immediate practical consideration for the Botanix community: please withdraw your Bitcoin and other assets before July 9th, 2026.

When we started in 2022, the pitch was simple enough to say in a sentence: bring real utility to Bitcoin. What that actually meant in practice, and what we have spent nearly four years building toward, was more ambitious than that sentence made it sound. We were trying to build a Bitcoin-based blockchain that could find genuine product-market fit as a platform for Bitcoin applications, without using token incentives to drive growth, manufacture users, or simulate utility. Almost every chain that has launched in the last cycle has reached for the same playbook (issue a token without PMF, engineer the incentive surface, point at the resulting metrics), and we did not believe this route is a viable strategy in the long term. We wanted to know whether a Bitcoin chain could earn its users on the strength of what was built on top of it, the value it brings in the market with Bitcoin itself as the only meaningful economic primitive in the system.

And we built it. The Spiderchain went live and stayed live, a year of mainnet operation with one hundred percent uptime and zero security incidents on a genuinely novel cryptographic architecture. We built Dynafed, a dynamic federation that turned the Spiderchain from a static multisig set into a rotating, decentralized one, the technical milestone that most people in this space said could not be built on Bitcoin without compromising trust assumptions. Twenty-five million transactions, two hundred thousand wallets, and tens of millions of dollars in assets moved across the chain, every single number of that earned organically without a token, without airdrops, without points programs, or any of the manufactured-demand machinery. Chainlink, Morpho, GMX, Dolomite, Fireblocks, Alchemy, Galaxy, OKX Wallet, all integrated. We shipped a Bitcoin neobank with BINK on iOS and Android, with self-custodial email login for Bitcoin (something that had never existed before), native Bitcoin yield, and the lowest borrowing rates against Bitcoin anywhere in the world, all of it downstream of owning the infrastructure. The point of saying this is not to argue with our own conclusion. The protocol works, the product works, and our team and ecosystem worked in concert to do exceptional work.

We have run this experiment in earnest, with a working protocol, real applications, and a serious team, for over a year on mainnet and nearly four years in total. The honest answer we have arrived at, after living inside it every day, is that it did not work, at least not in this market and not on this timeline.

We want to share what we think we learned, with the caveat that some of this is conviction and some of this is still suspicion, and we would rather be transparent about the difference than pretend to have clarity we do not have.

The first thing I've had to sit with is timing. Bitcoin utility, making Bitcoin programmable, productive, and integrated into real financial activity, isn't where the real world users sit right now. The conversation is still on Bitcoin as a reserve asset, on its monetary and political positioning, on base-layer conservatism. Those questions are upstream of the ones a Bitcoin L2 needs people to be asking. I still believe Bitcoin gets there, but belief in the destination is not the same as being able to predict when, and nobody can. It's also possible the destination never materialises at all, and that Bitcoin's role as a reserve asset is simply where it settles. If that's true, there will never be a market for what we were building, and no amount of time or capital would change that.

The second is the token question. We intended to eventually launch a token. We saw it, and still see it, as a genuinely new form of equity, something closer to an IPO than an airdrop, to be done when you reach product market fit and the moment is right. That moment never came. What became clear over the last year is that the market largely stopped rewarding even the more considered versions of that playbook. Token launches across the board have broadly underperformed, and those that did go to market with tokens haven't seen the outcomes or PMF that the model is supposed to produce.

The third lesson is about where DeFi demand on Bitcoin actually lives. For most use cases that exist today, lending, yield, leveraged exposure, WBTC on a mature general-purpose L2 is genuinely sufficient. Users have voted with their behaviour, and the verdict is that the trust assumptions of a wrapped representation on Ethereum are acceptable to almost everyone who wants Bitcoin-denominated DeFi. Decentralisation matters to people in principle and in conversation; in practice, when something cheaper and easier is in front of them, they use it. The security case for a dedicated Bitcoin L2 is real, but it only matters for a narrower band of applications than our thesis required, one of the clearer lessons this market has taught us.

The fourth lesson is structural. The on-chain economy is consolidating around venues that own the user relationship: Hyperliquid, Robinhood, the major CEXes, and now TradFi participants absorbing an ever-larger share of attention, flow, and revenue. Convenience and institutional credibility win, every time, as soon as they're available. As retail participation thins, that concentration only deepens. We were, and still are, believers in decentralisation, but the current direction of on-chain growth is running through distribution, and any team building base-layer infrastructure today is rowing upstream against that current. We were no exception.

The fifth lesson is the most concrete. Both of the above played out directly in our economics. The users we attracted were primarily using Bitcoin as a store of value for yield, a legitimate use case, but not the high-frequency transaction volume that drives fee revenue on a network like ours. BINK was our answer to that: a Bitcoin neobank designed to bring daily usage of BTC and stablecoins on-chain, driving the transaction volume the network needed. It was the right strategic instinct, and one we never got the chance to fully test. BINK only landed on both app stores in the last few weeks, a product that by its nature could only be built once the underlying infrastructure was proven and live. When users choose the convenient option and economic gravity pulls toward distribution, what's left on a decentralised infrastructure layer is a user base that costs more to serve than it generates. Infrastructure costs are what they are, and the fee income never came close to covering them.

If you would like to see how we were imagining a Bitcoin future and what we have been working on since September, feel free to download BINK and give it a spin: it’s a full-fledged self-custodial Bitcoin Neobank with email login, one click borrowing, a Lightning integration and more.

App store: apps.apple.com/us/app/bink-b…

Play store: play.google.com/store/apps/d…

This UX is where we think Bitcoin is ultimately heading towards although it feels too early. You can use invite code 1SD31R, but remember to remove your funds by July 9th.

We could keep going. We have chosen not to, however, because continuing past the point where additional time stops producing additional learning is not conviction, it is something that looks like conviction from the outside while corroding into something else on the inside. We would rather stop now, with integrity intact and resources available to take care of the people who took a chance on us, than push the experiment past the point where it still has something to teach us.

Reminder: Please withdraw all your assets by July 9th. After this, the federation will sweep the remaining Bitcoin. Any other assets or tokens on the network from then onwards will unfortunately be unrecoverable.

After this, the federation will sweep the remaining Bitcoin. Any other assets or tokens on the network from then onwards will unfortunately be unrecoverable.

To our investors, who backed a thesis that was harder to defend than it should have been, to our partners who built alongside us and bet pieces of their own roadmaps on ours, to the developers who deployed on Spiderchain, to our users and the BINK community who showed up for something experimental and stayed, and most of all to the Botanix team who shipped a genuinely novel system with rigour and care and who made every hard day worth the difficulty: Thank you, more than the words available here can carry.

3

243

Jun 9

Babylon is the cleanest example of why BTC TVL matters.

Last 7 days:

USD TVL: -11.59%

BTC TVL: 0.63%

The dollar chart looks weak. The BTC chart says exposure held steady and even ticked higher.

8

176

Jun 8

May 15

🏛️ The Managed Fund Approach to Generating Bitcoin Yield

A conversation with the fund managers of @syphercapital

In this episode, we sit down with Steve Han and Michael Song of Sypher Capital to discuss how serious Bitcoin fund managers are approaching BTC-denominated yield for their LPs.

Topics Discussed:

0:00 - Managed BTC yield vs direct protocol deployment

4:15 - Changes in the Space the Last Year

6:35 - Sypher Capital Origin Story

9:30 - Assessing On-Chain vs Off-Chain Opportunities 13:50 - Performing Due Dilligence

20:42 - Lessons Operating Fund Last 1.5 years

22:50 - Creating the Perfect Yield Product

25:25 - Updating the BitcoinYield 5-Point Safety Framework

29:32 - What Innovations Are Exciting

32:00 -Tokenization

40:30 - Tax Implications

Watch the 45-minute conversation below 👇

1

4

214

Jun 8

The Top BitcoinYield Strategies Today 📈

🔸Paid in BTC:

@HermeticaFi hBTC Vault: 2.43%

@Lombard_Finance Earn: 2.40%

@SolvProtocol BTC : 2.12%

@ZestProtocol: 1.60%

@AmbossTech Magma: 1.47%

🎪 Paid in ALTs:

@Starknet BTC Staking: 2.97%

@babylonlabs_io Staking: 0.05%

🏦 BTC-Denominated Managed Funds:

@syphercapital Fund: 4.90%

@CoinbaseInsto Fund: 4.00%

See real-time data for all tracked products at bitcoinyield.com bitcoinyield.com

3

1

14

1,351

Jun 7

With 22% of BTC secured by Ledger devices.

There's no bigger opportunity to offer products than being in the Ledger app store.

3

5

381

Jun 4

The Top BitcoinYield Strategies Today 📈

🔸Paid in BTC:

@HermeticaFi hBTC Vault: 4.05%

@AmbossTech Magma: 3.62%

@Lombard_Finance Earn: 2.77%

@SolvProtocol BTC : 2.11%

@ZestProtocol: 1.60%

🎪 Paid in ALTs:

@Starknet BTC Staking: 3.09%

@babylonlabs_io Staking: 0.04%

🏦 BTC-Denominated Managed Funds:

@syphercapital Fund: 4.40%

@CoinbaseInsto Fund: 4.00%

See real-time data for all tracked products at bitcoinyield.com bitcoinyield.com

2

5

239

Jun 4

. @MezoNetwork is returning double-digit APRs recently.

To get the highest returns, you need to lock their native token $MEZO.

For BTC holders who want to maintain maximum exposure. matchbox.markets/ is an interesting solution.

Matchbox coordinates two sides.

BTC depositors want boosted yield without buying MEZO.

MEZO lockers want yield exposure without supplying BTC.

Current Mezo Earn fee yield is low at ~0.03%, but the boost design can take depositors up to 5x.

Using your voting power also increases your earnings.

Note: We have not deeply reviewed the mechanics of Mezo's vote-escrow yet.

bitcoinyield.com/product/mez…

5

13

1,409

BitcoinYield retweeted

Jun 3

Really like what @bitcoin_yield is doing.

Every emerging market needs people willing to publish independent data. Without it, everything runs on anecdotes.

With it, you get benchmarks, better questions, and better-informed capital.

4

2

16

455

Jun 3

Last week, @krakenfx launched a Bitcoin Vault with up to 2.5% BTC-denominated rewards.

BTC is wrapped to kBTC on Ink, deposited into a Veda vault, and curated by Sentora across onchain lending markets.

worth noting:

- variable APY

- 5-day withdrawal wait

- 25% performance fee on earnings

- BTC rewards, BTC price exposure

The easy UX and massive distribution of centralized exchanges is coming to BTC yield.

1

10

371

Jun 2

Bitcoin yield is splitting into a few distinct markets:

1. BTC-paid income (trading activity)

2. token-paid incentives (emissions)

3. volatility-driven vault returns (market making)

4. treasury-company BTC-per-share accretion (securities)

5. managed fund / structured product exposure

Which one do you find most interesting?

1

4

329

Jun 1

The Top BitcoinYield Strategies Today 📈

🔸Paid in BTC:

@HermeticaFi hBTC Vault: 4.37%

@AmbossTech Magma: 3.86%

@Lombard_Finance Earn: 2.73%

@SolvProtocol BTC : 2.10%

@ZestProtocol: 1.60%

🎪 Paid in ALTs:

@Starknet BTC Staking: 2.85%

@babylonlabs_io Staking: 0.04%

🏦 BTC-Denominated Managed Funds:

@syphercapital Fund: 4.90%

@CoinbaseInsto Fund: 4.00%

See real-time data for all tracked products at bitcoinyield.com

6

2

15

1,195

Jun 1

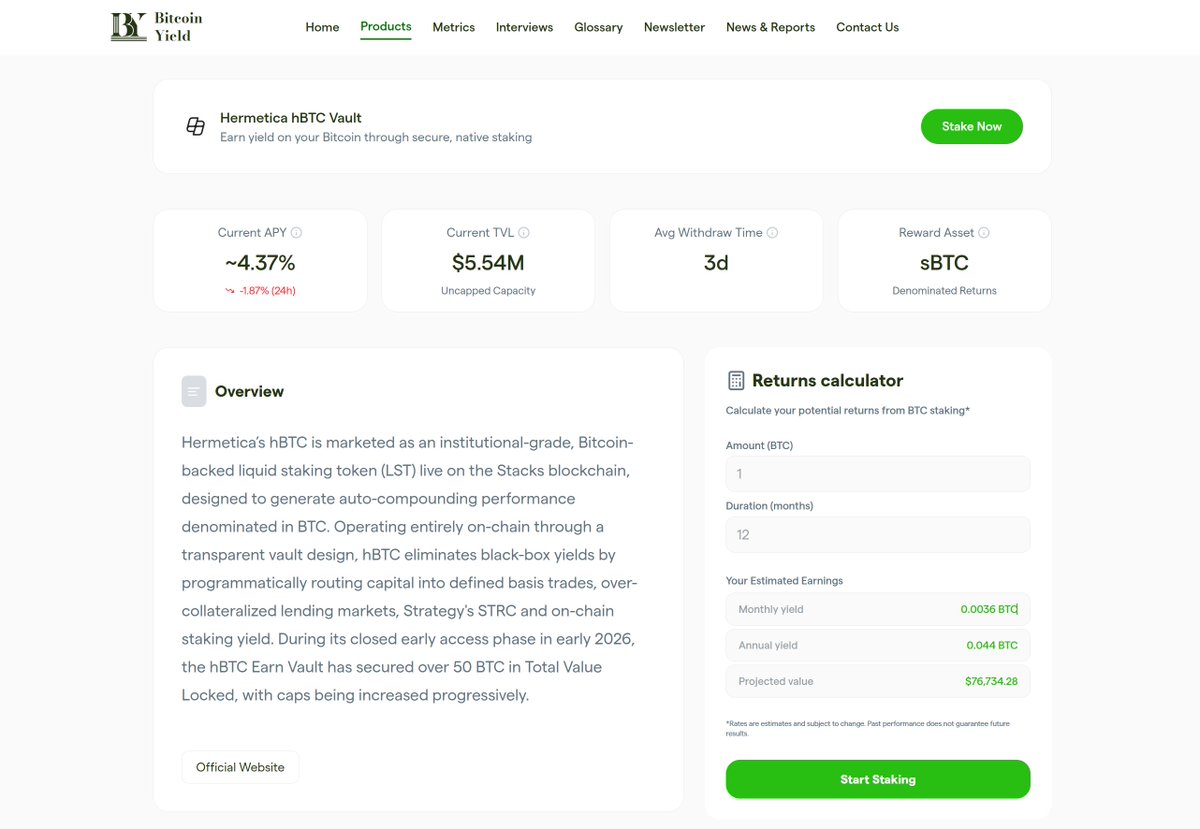

Note: Hermetica is currently at capacity. We have begun the 7-day count to remove them from the daily chart if capacity does not open.

1

96

Jun 1

Steve Han made the cleanest case for why institutional BTC yield will not be purely on-chain overnight:

On-chain is the better transparency experience.

It is also unforgiving if you make an operational mistake.

That tradeoff explains why managed products exist. Different holders are optimizing for different risks.

Direct protocol users want control and instant verification.

Institutional allocators want reporting, process, diligence, and fewer ways for an internal mistake to become a permanent loss.

x.com/bitcoin_yield/status/2…

1

5

146

Jun 1

STRC-linked yield is not native BTC yield.

It is issuer credit exposure showing up with a Bitcoin badge.

That was one of the best points in the Sypher Capital interview when talking about evaluating risk with a Wall Street mindset.

If you are evaluating a tokenized STRC product, smart contract risk is only the first layer.

You also have to underwrite MicroStrategy:

financials

capital stack

repayment priority

duration

liquidity

recovery path

The wrapper may be on-chain. The risk is still credit.

On-chain native investors are going to need accounting and credit-analysis muscles as RWAs move into Bitcoin yield portfolios.

Or read bitcoinyield.com as we expand how we cover these developments.

1

7

267

May 31

Most yield products have a scale issue.

Too much BTC too fast, something breaks.

What has @yieldbasis creator @newmichwill identified as the blockers for more capacity.

10

520