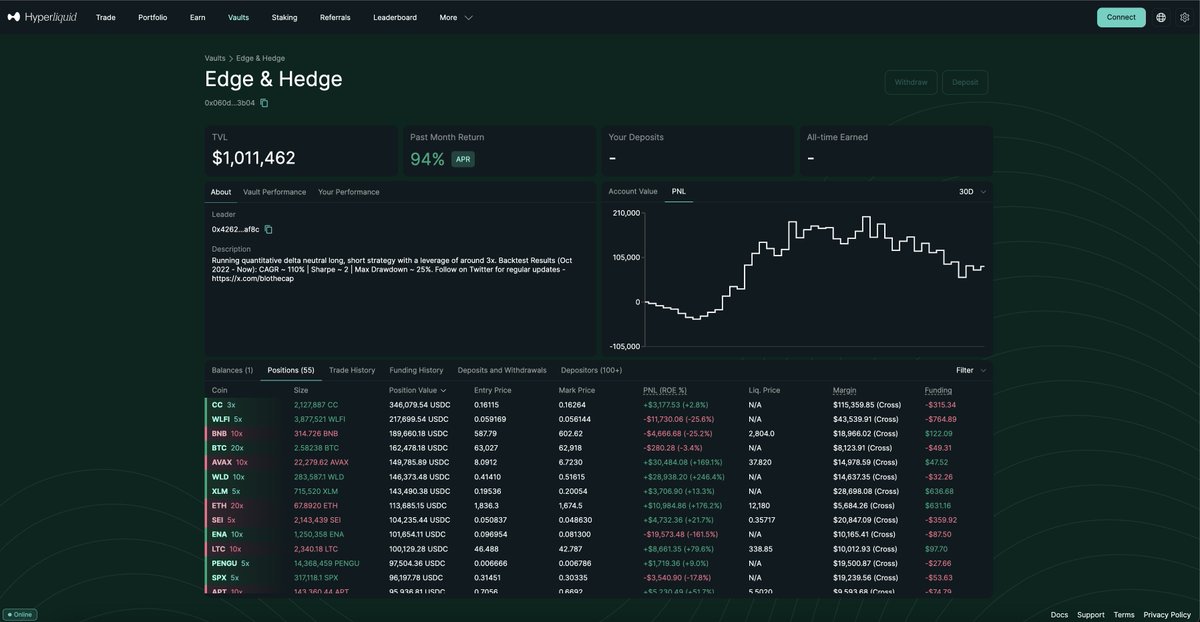

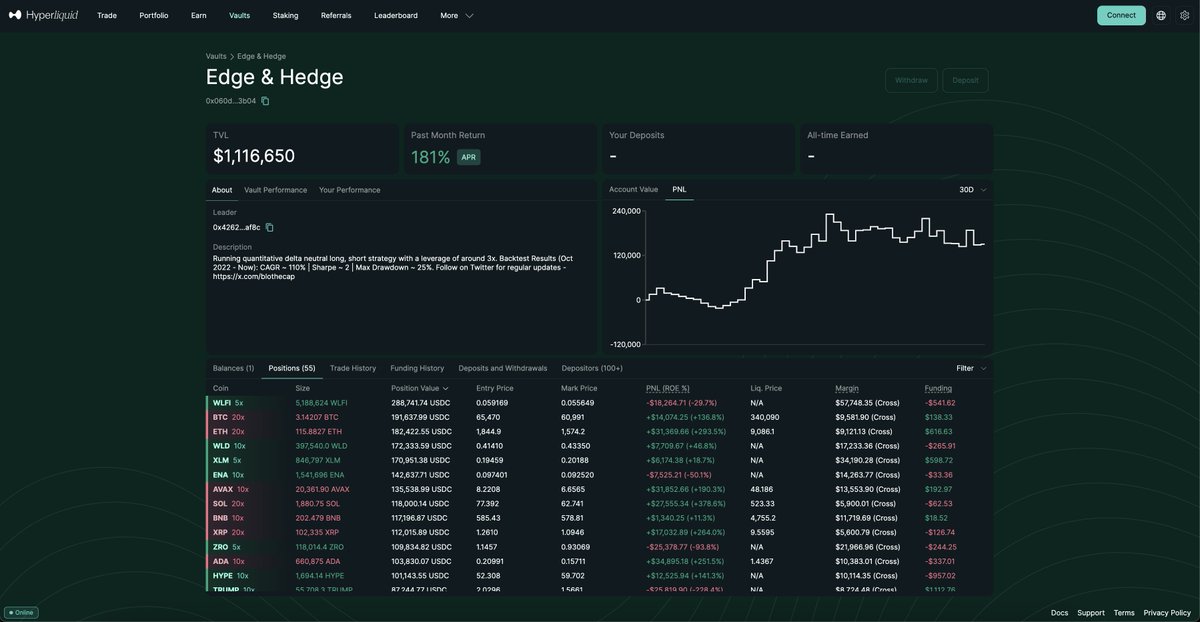

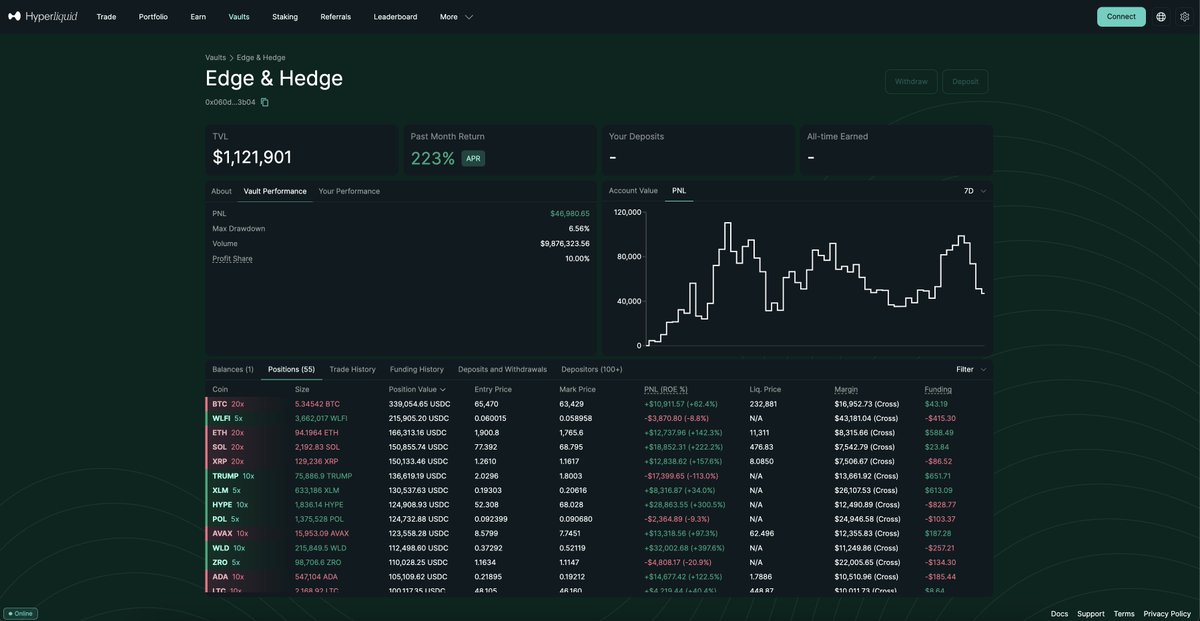

Market-neutral crypto vaults | Live: Edge & Hedge on Hyperliquid and Lighter | TVL: $3.7 Million | Public performance and risk updates | NFA

Joined February 2025

- Tweets 385

- Following 286

- Followers 1,038

- Likes 117

62 Photos and videos

Pinned Tweet

May 29

We published this article a while back predicting hyperliquid:native price at $105 based on buybacks and burns.

The reason its easier to sell hyperliquid:native to wall street is because of its structured buybacks and burns, you can build models such as these to value the token.

The point is not that our model is accurate, the bigger point is you can build models like these to price the token. Do give it a read if you have time.

blog.blothecap.xyz/how-to-pr…

2

1

6

950

Jun 13

We all know what happens to low MC, High FDV tokens. Thats what SpaceX is right now. The investor unlocks start next month. If you are buying I don't think you will make money for a long time on the stock. There is a very high probability that SpaceX will become much more valuable over long run but there will most likely be a much better opportunity to enter into SpaceX at a much better price.

For now it makes sense to short SpaceX. Its not really a bet against the company, its a bet against market perception of the valuation of the company. Not a financial advice, do your own research.

Jun 12

Former BlackRock fund manager Ed Dowd on the SpaceX IPO:

"people gotta understand... [SpaceX] raised $75 billion... [and only] floated 5% of the stock... it's a very small float"

"[But its valuation], that's a different story"

"$1.7 trillion did not go to SpaceX. [It is] $75 billion. So people need to understand that"

"then when Anthropic and OpenAI, if they ever make it to IPO, they're going to raise about $100 billion each. So the total raised actual real money is about $300 billion between these three IPOs"

"Their valuations, that's a different story. And those probably won't hold and they'll probably, you know, go down 80%. So anybody buying these stocks at these prices is probably going to lose a lot of money if they hold on to them"

@ShannonJoyRadio @DowdEdward

3

252

Jun 12

Someone please explain to him the meaning of local top and local bottom 🤯

Jun 11

Unpopular opinion👇

HYPE flippening Solana in price a week ago was the local top of HYPE and local bottom of Solana. Will never reflippen.

9

384

Jun 10

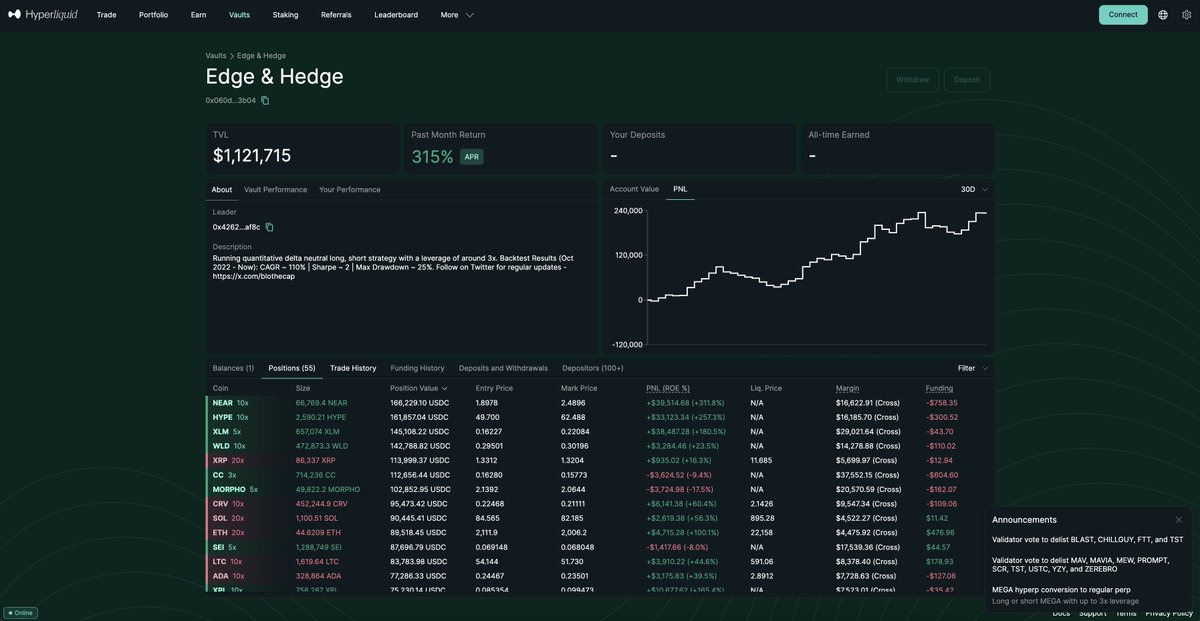

Our Vault has an expected drawdown of 25% based on our backtests. i.e. You should be willing to risk that much of the capital while investing. Invest only if you can tolerate this kind of risk.

Thanks @TokensWolf for pointing out that we do not include this in our vault updates. Going forward every update will have this risk disclaimer.

5

18

985

Jun 9

Vault Update:

The last few days have been difficult. The vault is currently in a drawdown of around 12%, and some investors who entered near the recent highs are now in loss. A few have also chosen to withdraw.

I want to be very clear about this: drawdowns are part of this strategy. Based on our backtests, a drawdown of up to around 24% is within the expected range for the vault. The current drawdown is uncomfortable, but it is not outside the risk profile we have communicated internally and built the strategy around.

That also means this vault is not suitable for everyone.

If you cannot tolerate this kind of drawdown, you should not be invested in the vault. We do not want investors taking risk they are not prepared for, and we sincerely do not want anyone to lose money because they entered without understanding the volatility involved.

The worst outcome is usually not the drawdown itself. The worst outcome is entering during good performance, panicking during a drawdown, and withdrawing at the exact point where patience is required. That is how temporary mark-to-market losses become realized losses.

This vault is built for investors who understand that returns come with volatility, and who are willing to stay through difficult periods as long as the strategy remains within its expected risk range.

If that does not describe you, it is better to stay out than to enter, panic, and exit at the wrong time.

1

11

1,032

Jun 6

Vault Update:

One of the primary goals we set for ourselves with this vault was simple: beat bitcoin:native returns.

So far, the vault is up 15%, while BTC is down 25%. That puts us roughly 40 percentage points ahead of Bitcoin.

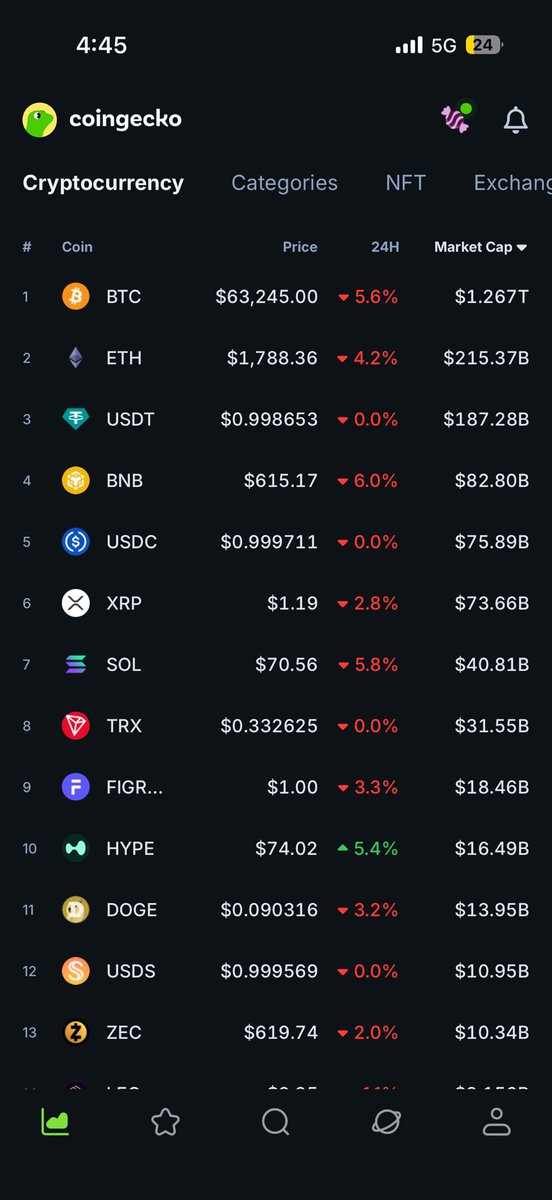

There is only one major coin we clearly lost to: $HYPE. No surprises there.

Any strategy that took a strong fundamental view that HYPE would outperform almost everything else would have beaten us comfortably. Some of them have. That is fine.

But that is not what we are trying to build.

We do not run this vault by taking discretionary fundamental calls on individual coins. We do not decide that we “like” a token and therefore force the portfolio to be long it. We let the algorithms make the decisions.

There have been times when the system has been short HYPE. As people who believe deeply in Hyperliquid, we obviously hate seeing that. But the moment we override the model because of our personal bias, the vault stops being systematic and becomes just another discretionary trading account.

That is not the mandate.

The mandate is not to always be long the coin we like most. The mandate is to compound capital with discipline, manage downside, and beat BTC over time.

So far, that is what the vault has done.

1

19

883

Jun 5

A lot of people who invested in zcash:native are probably feeling let down today. That reaction is understandable. When a protocol built around privacy faces a serious question around hidden state, it naturally shakes confidence.

But the right way to evaluate your investment decision is not by judging it only through hindsight. The real question is: given what you knew at the time, was investing in Zcash a rational decision?

I think for many people, the answer is yes.

Privacy remains one of the most important unsolved problems in crypto. Transparent blockchains are easier to audit, but they expose too much. Fully private systems protect users better, but they also make verification, detection and crisis resolution much harder. That tradeoff was always part of the bet.

Zcash was, and still is, one of the most serious attempts to solve that problem.

So yes, people can be disappointed. They can be angry. They can demand better answers. But regret is different. A bad outcome does not automatically mean the original decision was bad.

Sometimes you make the right bet, for the right reasons, and still get hit by the hardest risk embedded inside that bet.

2

263

Jun 5

The zcash:native vulnerability is not only about the current code. The deeper issue is that it puts the entire historical shielded state under scrutiny.

In a transparent blockchain, a critical bug can still be catastrophic. Public chains are not magically safe. But when something breaks, the detection and resolution path is usually clearer because the state is observable. You can inspect balances, trace flows, identify abnormal supply changes, and reason about remediation with evidence.

With shielded state, the problem becomes much harder. The chain can prove rules were followed only if the proving system itself was sound. If that proving system had a bug, you may be left with a painful question: was the hidden state ever corrupted? And because the state is private by design, the answer may not be directly observable.

That is the real cost of privacy. Not that privacy is bad. Privacy is absolutely necessary for blockchains to become serious financial infrastructure. Without it, public blockchains are structurally hostile to real users, businesses, and institutions.

But privacy changes the failure mode. A minor-looking circuit bug can create uncertainty worth billions because it attacks not only today’s code, but confidence in the validity of the historical private state.

I do not think this is a reason to blame the developers. Anyone who has built software knows that writing bug-free code is almost impossible. The real question is not whether bugs will happen. They will.

The question is whether the system has a clear path to detect, contain, and resolve those bugs before the damage becomes existential.

For transparent chains, that path is difficult but visible.

For chains with hidden state, that path is much less clear.

6

255

Jun 5

A small Investment thesis derived from Fear of AI

It has never been easier to have an affair, and at the same time it has never been easier to get caught.

That same paradox now applies to software.

It has never been easier to write code. AI copilots, open-source libraries, cloud infrastructure, APIs, and low-code tools have compressed software creation to a point where one person can now ship what previously required a team. The cost of creation is collapsing. The speed of creation is exploding. More software will be written, by more people, with less friction than ever before.

But the other side of that equation is brutal: it has also never been easier to get exploited if there is a bug.

A single leaked key, a vulnerable dependency, a misconfigured permission, an exposed API, or an AI-generated function that nobody properly reviewed can become the entry point for a real attack. The bug itself may be small. The consequence may not be. In modern software, one mistake can connect directly to customer data, financial infrastructure, production systems, cloud accounts, or internal tools. The blast radius of a single defect has become much larger than the defect itself.

This is the real conundrum AI is creating. Software creation is getting faster, but software assurance is not improving at the same rate. We are increasing the volume of code, the number of applications, the number of integrations, and the number of people capable of shipping software. But we are not proportionally increasing the ability to verify that all of it is safe.

That gap is where the security opportunity sits.

The biggest winners may not be the companies promising “bugless code.” That is probably the wrong framing. Bugs will exist. The more interesting companies are the ones that assume bugs will exist and make sure those bugs do not become catastrophic exploits. They help companies understand which vulnerabilities are actually reachable, which systems are exposed, which permissions are dangerous, which secrets have leaked, which APIs are vulnerable, and which attacks are happening in production.

Security is therefore moving from a prevention-only market to a resilience market. It is no longer enough to say, “Did we find the bug before shipping?” The more important question is becoming, “If there is a bug, can it actually be exploited — and if yes, how much damage can it cause?”

That question will matter more as AI increases software velocity. More code means more attack surface. More attack surface means more fear. And fear is one of the most powerful drivers of enterprise software budgets.

The paradox is simple: AI may make software cheaper to create, but it will make software security more valuable.

6

237

Jun 5

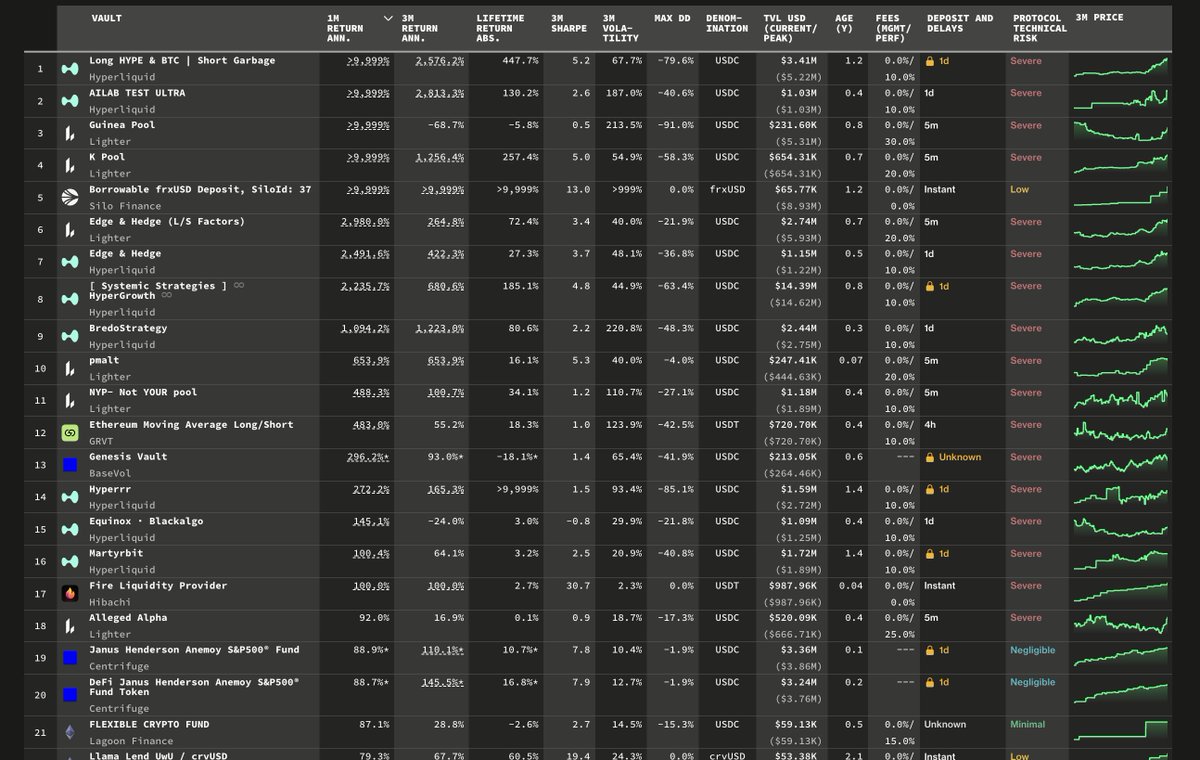

6 and 7

Top 20 most profitable vaults for the last month

tradingstrategy.ai/trading-v…

1

1

9

607

blothecap retweeted

May 25

I want to explain the most misunderstood factor for Hyperliquid. If what I lay out is going to happen, the price will easily go to $350 this year. 🧵

Right now, everyone is overly fixated on the launch of the ETFs. The Hyperliquid ETFs are a drop in the bucket for the wall of capital that is going to hit the market

This is very straightforward if you understand global interest rates, fx, and the supply of money in the system. Most people have ZERO clue about how these markets function because they have never traded G7 rates. People think they understand liquidity because they traded Bitcoin during a dollar devaluation narrative but when asked about the most important input into macro liquidity, interest rates, they have no clue.

It is IMPOSSIBLE to have a view on macro liquidity and money in the system without understanding interest rates. These are two sides to the same coin.

Let me lay out this thesis very simply: 👇

Interest rates are all about the price you pay for money in the system. FX markets are the flip side of the coin, which is denominated the actual currency you are borrowing relative to other currencies and their respective interest rates.

Why does this matter for Hyperliquid? Because the largest markets in the world are all about interest rates and FX. Bitcoin and crypto are a drop in the bucket for large players who are managing massive balance sheets. If Hyperliquid can provide enough value via liquidity and low-cost leverage, then the largest players in the world will start moving more capital onto the platform to transact in the most important markets, interest rates, and FX.

Simply put, if you have enough liquidity on your platform, the price you pay for leverage can be LOWER than what you might pay somewhere else. Simple example: If you need a mortgage for your house, you are going to try to get the best rate possible. This is you trying to find the "cheapest leverage" possible in the system. If someone offers you a lower interest rate, with no trade offs, people will take it. Many brokerage accounts compete with each other on the margin rates you have to pay in order to use the firms margin.

The same dynamic is true for Hyperliquid. If they can provide attractive margin rates (or what we can funding rates on Hyperliquid), then this is the real value proposition for Hyperliquid. While everyone is focused on ETF flows, you want to ask what are the drivers of value that would catalyze the flows of the largest players to begin using Hyperliquid every single day.

Clearly, the regulatory constraint is holding capital back like a dam holding back water that wants to pour into a new market. But the most important thing to understand is that if the funding rates for interest rates and FX are low enough on Hyperliquid, this begins to attract capital from the largest players in the world. This especially attracts capital from the entire Eurodollar market that is constantly trying to hedge the surplus of dollar liquidity that is in the system due to the dollars reserve currency status and the historic level of trade the US has conducted which has pushed an unprecedented level of dollars through the entire system.

This flow mechanism connected to the larger macro picture is WHY I am so bullish on Hyperliquid. Notice that functionally, no one else has talked about this. They think this is just the regular "crypto cycle" where you buy momentum and fade the price once everyone starts talking about it on the timeline.

The place we are at with Hyperliquid is actually taking advantage of the biggest blind spots for both people in crypto and people in traditional markets. Crypto people have been conditioned to just think in terms of pump and dumps instead of value creation and flow mechanics in the global interest rate complex. Traditional finance people have functionally dismissed crypto as something that is worthless because no one has really provided true value that has lasted.

This is why I wrote this article on the blindspot that existed earlier this year, before Hyperliquid made its massive YTD rally: x.com/Globalflows/status/201…

There is a reason that no one is talking about these mechanics. The crypto influencers or VC establishments won't talk about it because they didnt get to invest in Hyperliquid before it launched or get a crypto allocation to schill. On the flip side, the largest institutions won't talk about Hyperliquid because they dont want to draw attention to a market that they havent established a dominant positioning in yet.

"Do you mean to tell me you've finally established a position, so you can price mine?" - The Big Short

My job is a trader. I get paid to hold risk and I have established a position in $PURR which is the largest Hyperliquid treasury company and the only treasury company in the world with a positive P&L right now. It is up over 140% since I originally published the view (see my pinned tweet). But we have only just begun to price what is possible for Hyperliquid and what is possible for $PURR.

Once you realize that Hyperliquid sits in a massive gap in the tradfi and crypto space, then you will realize why $PURR sits as the bridge to BOTH of these.

I continue to hold my $PURR position and it is my strong conviction that Hyperliquid will have a significant rally beyond anyone's expectations and $PURR will be the direct beneficiary of this in addition to adding additional shareholder value on top of HYPE returns.

There are several things that you need to know in order to navigate these changes in Hyperliquid:

1) Understand that we are in a credit cycle melt up that in its very nature is currently sowing the seeds of its own demise. None of this will end well given the amount of liquidity that is in the system but first we are melting up MUCH MUCH HIGHER.

2) Hyperliquid underlying drivers in its value proposition that could catalyze capital aggressively moving onto the platform to access cheap leverage.

3) All of the signals for positioning in global risk assets, interest rates, Hyperliquid, and $PURR.

I will be providing an entire playbook for #1-3 in a livestream tomorrow at 8:30am MST. You will walk away with a playbook for the credit cycle, a model with the code included on mapping funding rates on Hyperliquid, and Tradingview models for monitoring the positioning signals. This will be 100% free for everyone who is a subscriber here. I will send out the links tonight and resend them tomorrow morning so no one misses it: capitalflowsresearch.com/sub…

Below, I will link the most important tweets and videos I have done thus far that you should review before the livestream tomorrow

Welcome to global macro

HYPERLIQUID

53

130

966

240,903

Jun 4

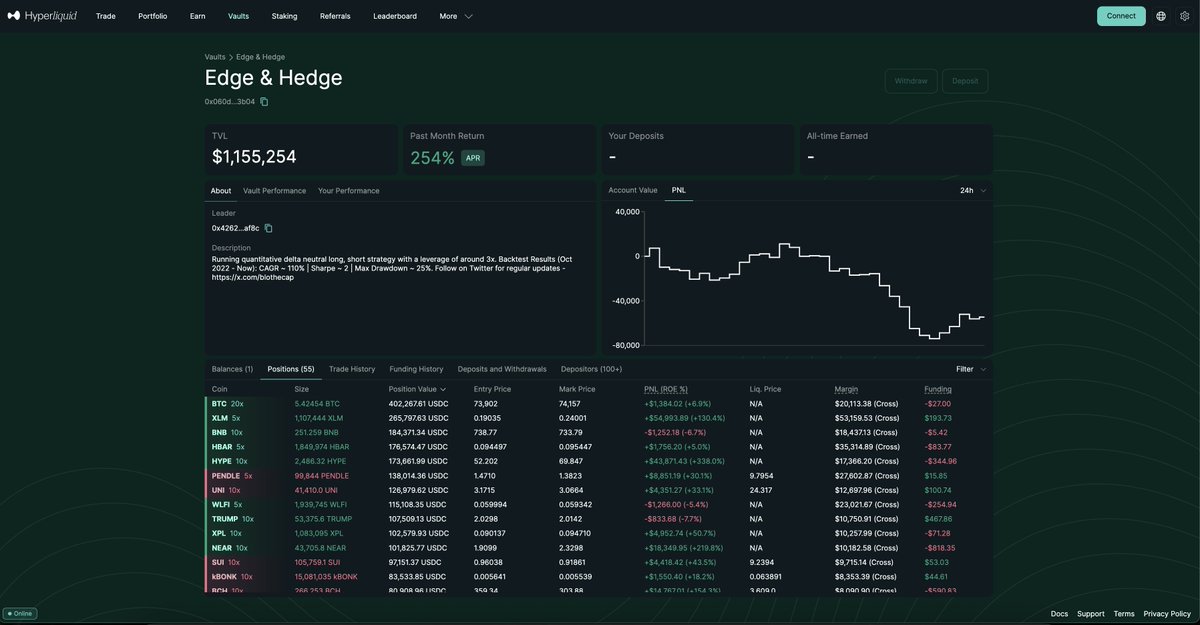

Our Vaults performance in last few days of blood bath.

The vault is up $47K which is around 4% return on capital while the market is overall down by 13-15%. Thats a 17-19% outperformance over market.

3

1

12

520

Jun 4

Time to remember why Hyperliquid is a great investment now that a big "KOL" is publicly out of hyperliquid:native after shilling it for months. I would call him more of a noise in Hyperliquid ecosystem rather than a signal.

Apple does not need to build every app in the App Store. It benefits when the ecosystem built on top of it generates economic activity.

Hyperliquid is creating a similar flywheel:

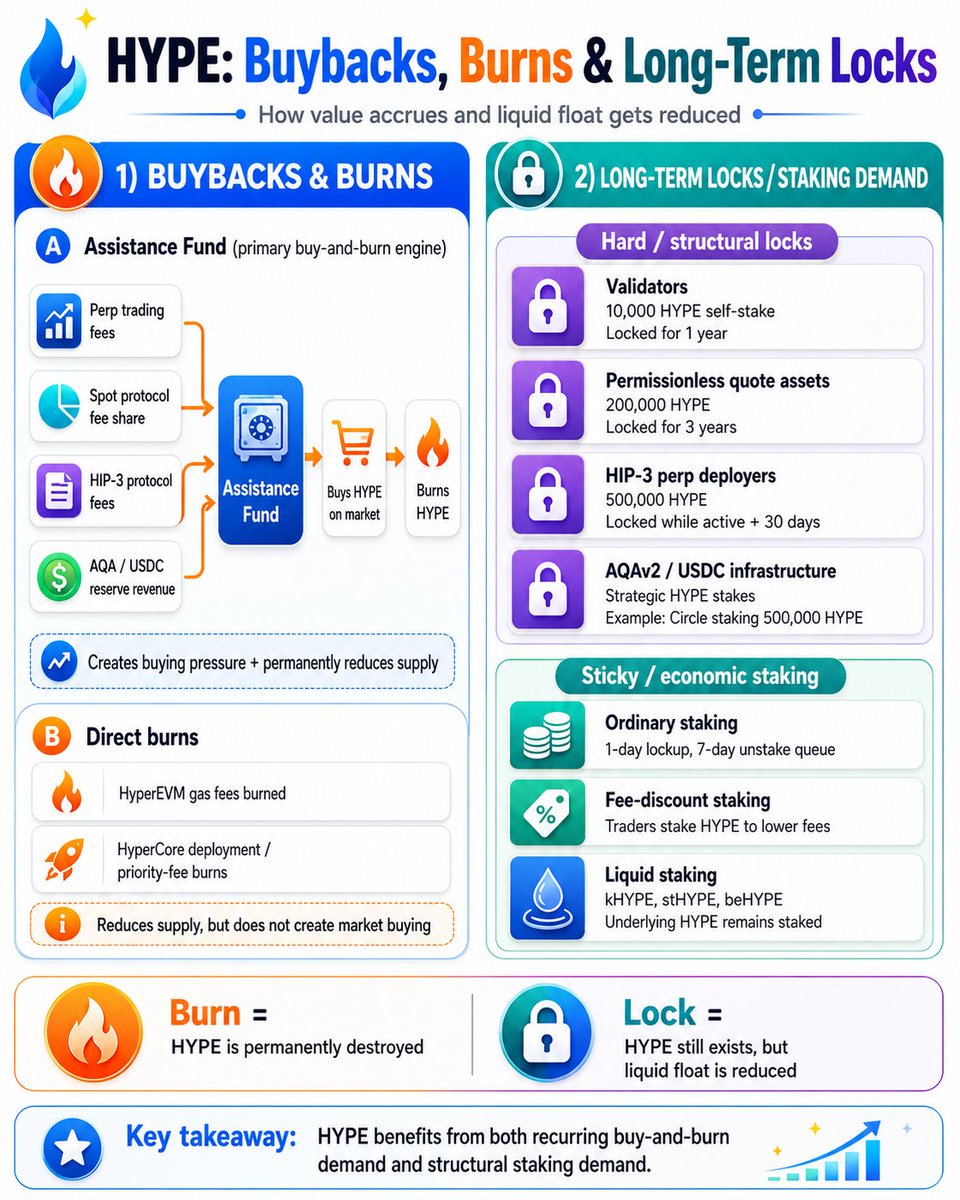

More trading → more HYPE bought and burned

More deployments → more fees and HYPE locked

More infrastructure → more structural demand for HYPE

That is the part of the hyperliquid:native thesis people are still underestimating.

1

5

327

Jun 3

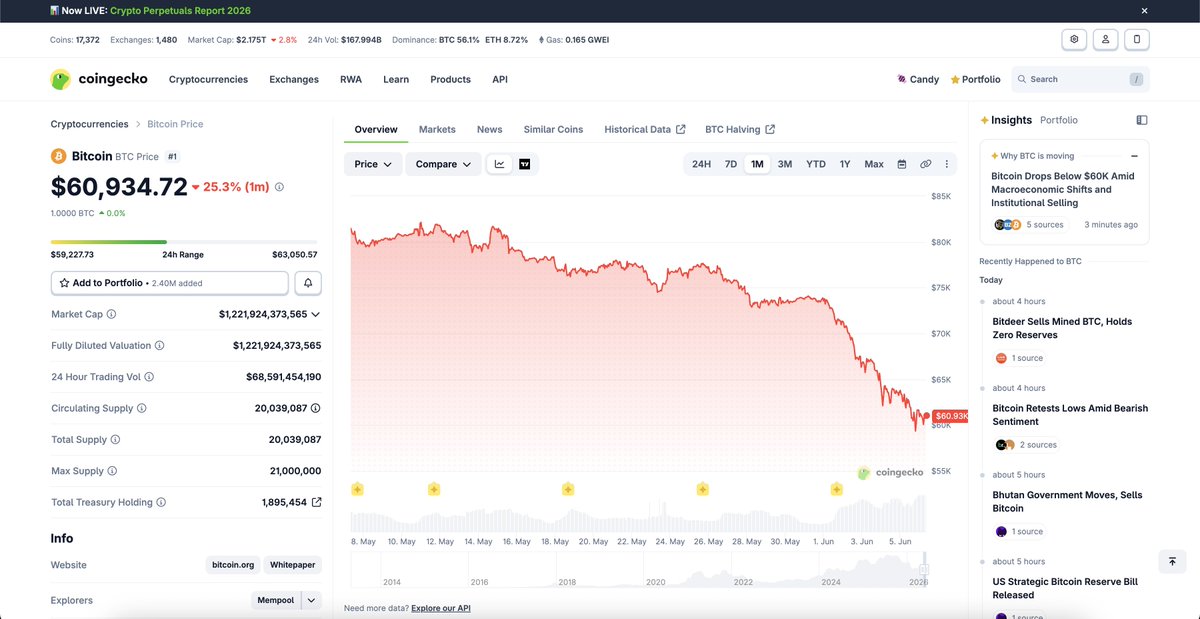

Yesterday was one of those days when the market was reacting not merely to price, but to a change in belief.

Bitcoin has always occupied a unique position in crypto. It is the asset the rest of the market looks to for direction, the closest thing the industry has to a reserve asset, and for the last several years one of the strongest pillars supporting its institutional narrative has been Strategy, formerly MicroStrategy. Michael Saylor did not just buy Bitcoin; he built an entire corporate identity around the idea that Bitcoin was the ultimate treasury asset, something to accumulate permanently rather than trade opportunistically. Strategy became, in the eyes of the market, the infinite bid: the buyer that would keep raising capital, keep accumulating BTC and, most importantly, never sell.

That is why the disclosure that Strategy sold 32 BTC mattered far more than the size of the sale itself.

Thirty-two Bitcoin is almost irrelevant against a holding of more than 843,000 BTC. It is not enough supply to explain a major move in price, and it would be simplistic to argue that this transaction alone caused Bitcoin to fall. But markets often care more about the breaking of a narrative than the immediate economic impact of the event that broke it. Until now, the market could treat Strategy’s Bitcoin holdings as effectively removed from supply. The moment Strategy sold even a small amount of BTC to meet obligations created by its own capital structure, that assumption stopped being absolute.

The important shift is that Strategy can no longer be seen only as a source of demand for Bitcoin. It is now, at least conditionally, also a potential source of supply.

That is a meaningful change because the company has become one of the largest and most visible expressions of institutional conviction in Bitcoin. A structure that looked highly supportive while capital was flowing in can begin to look different when its obligations require liquidity. The issue is not that Strategy is suddenly about to liquidate its Bitcoin holdings. There is no evidence of that. The issue is that the market has now been reminded that even the strongest holder of Bitcoin operates within financial constraints.

This came at an already fragile moment for crypto. Bitcoin fell sharply, and as usually happens when BTC weakens, much of the broader market followed. Confidence was already thin; the Strategy sale gave investors one more reason to question a narrative they had previously treated as almost unquestionable.

Yet market-wide stress is also when relative strength becomes most visible. When everything is rising, it is difficult to distinguish genuine strength from general liquidity. When Bitcoin is falling and most of the market is being sold indiscriminately, assets that hold up or continue to attract demand become far more interesting. In this sell-off, $HYPE stood out. While BTC was under pressure and much of crypto moved lower, HYPE continued to show unusual resilience, trading near record highs rather than simply following the market down.

That distinction matters for how we think about the vault. The objective of a market-neutral strategy is not to correctly predict whether crypto as a whole will go up or down on any given day. It is to identify where strength persists and where weakness is emerging, while limiting the portfolio’s dependence on broad market direction.

Over the last 24 hours, the market declined by roughly 5–6%. Our vault was not completely immune to the move, ending the period down approximately 1%. But in a market where Bitcoin led a broad drawdown, limiting losses to a fraction of the market decline is precisely what the strategy is designed to do.

The most important takeaway from yesterday is not simply that Bitcoin fell, or that one asset outperformed. It is that markets can reprice long-held beliefs very quickly. Strategy’s sale was small in size, but large in symbolism. At the same time, the sell-off helped reveal where genuine relative strength may be emerging.

In markets like these, capital protection and selectivity matter more than blind exposure.

1

1

3

251